In today’s rather subdued trading sessions, most of the movements in the financial markets are limited. European indexes are somewhat in red, albeit with contained losses for the time being. Meanwhile, yields in US and Europe have experienced a minor increase. In the currency sphere, Sterling is mildly weaker, closely followed by Dollar and Euro. Conversely, Canadian Dollar is showing strength, with Yen and Kiwi Dollar tailing not far behind.

As we look forward to the upcoming Asian session, all eyes are on Australian Dollar, gearing up to be the focal point. This heightened attention comes as RBA plans to publish the minutes of its meeting held on September 5. Remarkably, the meeting marked the third consecutive time RBA chose to maintain the status quo on interest rate.

The financial streets are buzzing with speculation as market participants are split in their expectations; while RBA hasn’t definitively closed the door on another rate hike, a segment of the market conjectures that the interest rates have attained their peak. The upcoming minutes are set to offer a deep well of insights, providing a closer look at the discussions held during the meeting — mainly focusing on whether there was serious contemplation on a rate hike, thereby presenting a clearer picture of the likelihood of such a move later.

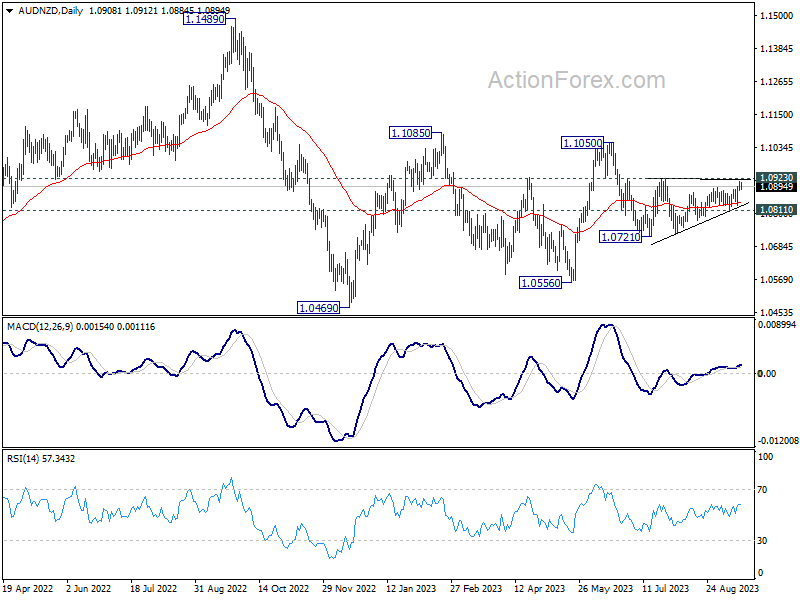

On the technical front, AUD/NZD is seen oscillating in a triangular consolidation pattern since dipping to 1.0721. This pattern hints that the decline from 1.1050 has yet to reach its end. A set of RBA minutes that leans more towards the dovish end of the spectrum could potentially knock down the cross from 1.0923 resistance. Further break of 1.0811 support will argue that AUD/NZD is ready to fall through 1.0721 support towards 1.0056. However, firm break of 1.0923 resistance will dampen this view, and target 1.1050/1.1085 resistance zone instead.

In Europe, at the time of writing, FTSE is down -0.46%. DAX is down -0.82%. CAC is down -1.20%. Germany 10-year yield is up 0.0273 at 2.707, above 2.7 handle. Earlier in Asia, Japan was on holiday. Hong Kong HSI dropped -1.39%. China Shanghai SSE rose 0.26%. Singapore Strait Times dropped -0.53%.

ECB’s Kazimir: Cannot rule out further hike, premature to bet on cut

ECB Governing Council member and head of Slovakia’s central bank, Peter Kazimir, indicated in an opinion piece that the possibility of further rate hikes remains on the table. Also, it’s premature to bet on the timing of the first rate cut.

Kazimir emphasized that the forthcoming March forecast will be a decisive factor in ascertaining whether the inflation target is within reachable limits, stating, “Only the March forecast can confirm that we are heading unequivocally and steadily towards our inflation goal.”

“That is why I cannot rule out the possibility of further rate increases today,: he added.

Elaborating on the current stance of the policy rates, Kazimir metaphorically commented, “Assume we’re at the top. If so, we may have to stay camping here for quite some time and spend the winter, spring, and summer here.”

Hence, it would be “premature to place market bets on when the first interest rate cuts will occur.”

Meanwhile, he did leave the door open for potential adjustments in the bank’s quantitative tightening measures, contingent on economic data. He noted, “As soon as incoming economic data and analyses confirm that further tightening is unnecessary, I see room for a debate about adjusting the pace of our quantitative tightening.”

New Zealand’s services sector continues its descent, a deeper dive

New Zealand’s BusinessNZ Performance of Services Index reported another slump in August, marking the third consecutive month of declining in the services sector. This downturn saw PSI slip from 48.0 in July to 47.1 in August, notably falling short of long-term average of 53.5.

Looking into the components, while there were marginal improvements in activity/sales, which climbed from 39.7 to 43.4, and employment, which rose from 49.1 to 50.9, other areas did not fare as well. New orders/business made a meager ascent from 44.5 to 47.3. Conversely, stocks/inventories dipped from 54.0 to 52.5, and supplier deliveries took a hit, declining from 52.0 to 49.2.

BusinessNZ’s Chief Executive, Kirk Hope, offered a bleak perspective, highlighting that August’s data provided little hope for a swift recovery.

This sentiment was further cemented by the proportion of negative comments received in the survey. In August, 63.9% of the comments were negative, a slight improvement from July’s 67% but a significant jump from June’s 55.6%. The cloud of uncertainty hanging over the upcoming General Election, combined with persisting challenging economic conditions, were predominant themes among these comments.

BNZ’s Senior Economist Doug Steel noted that the PSI and PMI results resonate with RBNZ’s projections of an impending recession rather than Treasury’s more optimistic forecast of sustained, albeit moderate, growth in the near future.

NZ economic growth to remain subdued according to NZIER forecasts

Latest forecasts from New Zealand Institute of Economic Research anticipate a period of subdued economic growth over the next few years. The annual average GDP growth is expected to decline to 0.4% in the fiscal year ending March 2024, followed by modest growth of 1.1% in 2025.

This sluggish pace is partly attributable to the ripple effect of consecutive hikes in RBNZ’s OCR, currently standing at 5.50%, which have started to curb demand in the broader economy. Moreover, diminishing demand for exports, spurred mainly by China’s weaker growth outlook, poses downside risk to the nation’s economic vitality.

Shifting focus to inflation sphere, there has been a notable upward revision for the projections as of March 2024, with annual CPI inflation predicted to retreat to 4.3% in 2024, and further dip to 2.4% in the subsequent year.

As for currency outlook, NZD Trade Weighted Index forecasts have undergone revisions, showing a downturn for the approaching year but portraying an uplift in 2025.

NZD has not encountered significant fluctuations against other currencies in recent times in terms of yield attractiveness. This steadiness, however, is anticipated to meet challenges due to reduced export demand from China.

The forecast encapsulates expectation of NZD TWI oscillating between 70.8 and 71.6 in the period spanning 2024 to 2027.

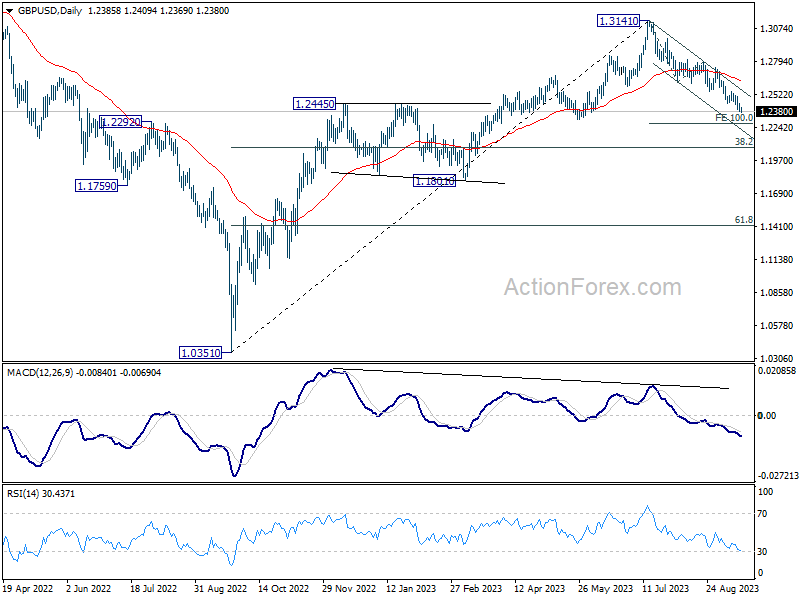

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2359; (P) 1.2402; (R1) 1.2426; More…

No change in GBP/USD’s outlook as fall from 1.3141 is extending today. Intraday bias remains on the downside for 100% projection of 1.3141 to 1.2618 from 1.2799 at 1.2276. On the upside, though, firm break of 1.2547 resistance will now indicate short term bottoming, and bring stronger rebound.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. However, sustained break of 1.2075 will raise the chance of bearish trend reversal.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Aug | 47.1 | 47.8 | 48 | |

| 23:01 | GBP | Rightmove House Price Index M/M Sep | 0.40% | -1.90% | ||

| 12:15 | CAD | Housing Starts Aug | 253K | 257K | 255K | |

| 12:30 | CAD | Industrial Product Price M/M Aug | 1.30% | 0.50% | 0.40% | |

| 12:30 | CAD | Raw Material Price Index Aug | 3.00% | 3.80% | 3.50% | |

| 14:00 | USD | NAHB Housing Market Index Sep | 50 | 50 |

{kind=link}