Yen languishes as the day’s worst performer, with sentiments taking a hit due to BoJ’s silence on potential policy tweaks. European majors aren’t faring much better, as subpar PMI data from both Eurozone and UK echo the sentiment that further tightening might not be on the cards for ECB and BoE. The Swiss Franc also feels the pressure, even if the pace of its earlier slide has decelerated.

Conversely, commodity currencies are flexing their muscles, spearheaded by the New Zealand Dollar. The notable rebound in Hong Kong stocks could be providing a boost to both Aussie and Kiwi. Enthusiasm is mounting over the possibility of China’s economic recovery picking up pace during the latter part of the year. Meanwhile, Dollar offers a mixed performance, battling to re-establish its momentum against the likes of the Yen and the Euro.

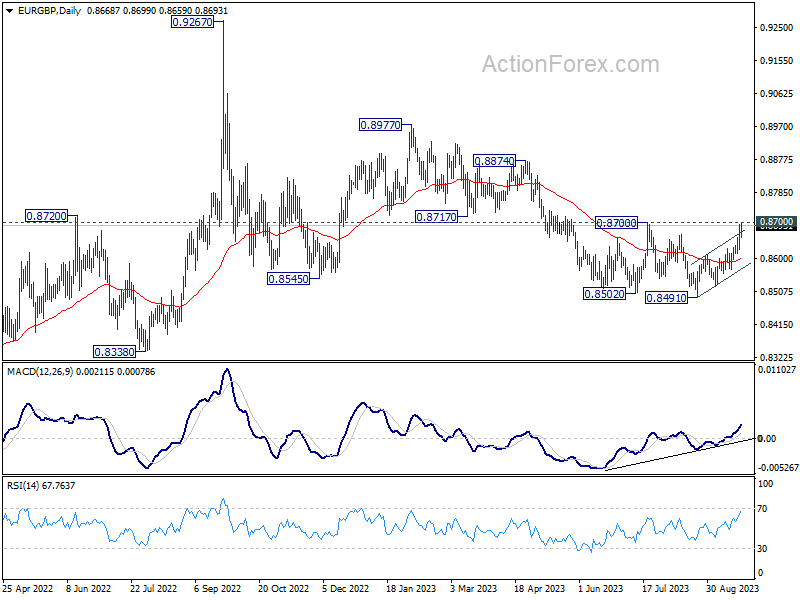

Technically, as the week comes to a close, a focus will be on whether EUR/GBP could close above 0.8700 resistance. If realized, that would be an indication what fall from 0.8977 has completed, as well as the three wave down trend from 0.9267. That would set the stage for more medium term rally back to 0.8977 resistance levels.

In Europe, at the time of writing, FTSE is up 0.65%. DAX is up 0.00%. CAC is down -0.41%. Germany 10-year yield is up 0.013 at 2.752. Earlier in Asia, Nikkei dropped -0.52%. Hong Kong HSI rose 2.28%. China Shanghai SSE is rose 1.55%. Singapore Strait Times dropped -0.33%. Japan 10-year JGB yield dropped -0.0041 to 0.749.

Canada retail sales rose 0.3% mom in Jul, missed expectations

retail sales rose 0.3% mom to CAD 66.1B in July, below expectation of 0.4% mom. Core retail sales—which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers—were up 1.3% mom. In volume terms, retail sales was down -0.2% mom.

Advance estimate suggests that sales declined -0.3% mom in August.

Eurozone PMIs point to -0.4% GDP contraction in Q3

Eurozone Manufacturing PMI was slightly disappointing in September, dipping from 43.5 to 43.4, failing to meet expectations set at 44.0. On the other hand, Services PMI indicated a slight revival, progressing from 47.9 to 48.4, surpassing the anticipated 47.5. Composite PMI reflected this marginal uplift, moving from 46.7 to 47.1.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank predicts a contraction for Eurozone in the third quarter, with a potential decrease of -0.4% relative to the previous quarter.

In services sector, “the heat on input prices shows that the risk of a wage-price spiral must remain very much on the radar of the ECB.” Manufacturing continues to be a drag. But “destocking process” may bottom out over the next few months, which is crucial for the manufacturing sector’s recovery for the beginning of next year.

Making a comparison between the two European giants, de la Rubia pointed out that while the French manufacturing sector “catching up” with Germany’s weaknesses. When it comes to services, France’s sector is “in a much worse state”.

Germany PMI Manufacturing saw a slight climb from 39.1 to 39.8. Similarly, PMI Services edged up from 47.3 to just below the 50 mark at 49.8. Composite PMI experienced an uptick, moving from 44.6 to 46.2.

France PMI Manufacturing slumped to 43.6 in September, marking a 40-month low. PMI Services and Composite figures too painted a grim picture, both plummeting to a 34-month low, with values of 43.9 and 43.5, respectively.

UK PMI composite fell to 46.0, heightened recession risk supports BoE pause

UK PMI Manufacturing sector had a slight uptick in September, moving from 43.0 to 44.2, surpassing expectations set at 43.0. Services PMI disappointed, recording a drop from 49.5 to 47.2, underperforming against the forecasted 49.0, marking a 32-month low. Consequently, PMI Composite followed suit, declining from 48.6 to 46.8, also registering a 32-month low.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, stated, “The disappointing PMI survey results for September mean a recession is looking increasingly likely in the UK.”

The current PMI data aligns with a potential GDP contraction of over -0.4% on a quarterly basis. Williamson mentioned, “September’s downturn is the steepest since the height of the global financial crisis in early 2009 barring only the pandemic lockdown months.”

A significant point of apprehension in the inflation framework remains wage growth. However, with the survey indicating the most significant employment decline since 2009, wage negotiation leverage appears to be dwindling swiftly.

Williamson believes the unsettling indications of heightened recession risk coupled with diminishing inflationary pressures are likely to have “added to calls to halt rate hikes” by BoE.

UK sales volume up 0.4% mom, sales value up 0.8% mom

UK retail sales showed some growth in August, albeit falling short of market expectations. On a month-on-month basis, sales volumes increased by 0.4% mom, slightly under the anticipated 0.5% rise. When removing the impact of fuel, the volume rose by a slightly better 0.6% mom. In terms of the monetary value, sales were up 0.8% mom, with the figures excluding fuel at 0.7% mom.

Taking a step back to analyze a broader timeframe, the three-month period leading up to August 2023 witnessed a 0.3% rise in sales volumes compared to the previous three months. Same growth of 0.3% was observed for volumes that excluded auto sales. In value terms, the increase was more pronounced with a 1.3% growth, and the value excluding fuel sales experienced an even more robust growth of 2.0%.

BoJ stands pat, drops no hint on future adjustment

BoJ maintains a steady course today and keeps monetary policy unchanged. It also chooses choosing not to make any adjustments in the statement that would suggest a departure from its existing negative interest rate stance or the yield curve control measures. The central bank even retains the pledge that it “will not hesitate to take additional easing measures if necessary.”

In unanimous decisions, short-term policy interest rate is held at -0.10%. 10-year JGB yield target is held at 0%, with a band of plus and minus 0.5%. Moreover, the bank’s offer to purchase 10-year JGBs at a rate of 1.0% daily through fixed-rate market operations remains unchanged.

BoJ anticipates the Japanese economy to maintain a moderate recovery in the near term. However, it has also flagged concerns, noting that the economy is “under downward pressure stemming from a slowdown in the pace of recovery in overseas economies.” Beyond this phase, the central bank is optimistic that the economy will exhibit growth “at a pace above its potential growth rate” due to the strengthening of a “virtuous cycle from income to spending.”

Regarding inflation, BoJ foresees the year-on-year core CPI to “decelerate” owing to diminishing import price effects. Nevertheless, in the subsequent period, the CPI is projected to “accelerate again moderately”, spurred by an improving output gap, along with rising medium-to-long-term inflation expectations and wage growth.

Released earlier, Japan headline CPI slowed slightly from 3.3% yoy to 3.2% yoy in August. CPI core (ex-food) was unchanged at 3.1% yoy. CPI core-core (ex food and energy) was unchanged at 4.3% yoy.

Japan’s PMI manufacturing fell to 48.6, slackening demand and lower employment

Japan’s Manufacturing PMI further declined from 49.6 to 48.6 in September, falling short of the anticipated 49.9, marking the most pronounced contraction since February. PMI Services also receded from 54.3 to 53.3. PMI Composite, which gives a holistic view of the broader economy, tapered off from 52.6 to 51.8.

Usamah Bhatti, an Economist at S&P Global Market Intelligence, noted that the future doesn’t seem particularly rosy, with forward-looking indicators hinting at a possible slackening of demand and activity. While service firms did experience a rise, manufacturing segment reported a sharp decline in new orders, the most pronounced in seven months.

Another worrisome development is the reduced employment levels in the private sector. Bhatti stated, “As pressure on capacity eased, there was a renewed reduction in employment levels.” This trend was “the first since the start of the year and the quickest since August 2020.” He attributed this to companies not replacing those who voluntarily exited, often as a strategy “amid elevated cost burdens.”

Australia PMI composite back to expansion, risk of “no land” for the economy

In September, Australia’s Manufacturing PMI slipped to a 3-month low, declining from 49.6 to 48.2. In contrast, PMI Services showcased resilience, rising from 47.8 to a 4-month high of 50.5. PMI Composite also surged from 48.0 to 50.2, a 4-month peak, signaling a return to expansion in the broader economy.

Warren Hogan, Chief Economic Advisor at Judo Bank,said that “demand in the economy is holding up, and business activity remains on a sound footing.” He further remarked that, contrary to some expectations, the present economic scenario isn’t about choosing between a “hard or soft landing.” Instead, he proposed that the real risk is of “no landing” for the economy.

Hogan further touched upon the inflation concerns that have been a pivotal discussion in financial circles. “The inflation indicators remain elevated at levels pointing to above-target CPI over the next 6-9 months,” he stated. He pointed out that input prices remained unchanged in September, hinting at continued cost pressures. However, the final prices index experienced a slight dip in the September flash report. Despite this marginal decline, Hogan suggested that “inflation over the second half of 2023 could be higher than desired.”

This latest PMI data follows a trend of stronger-than-predicted figures emerging from Australia in recent weeks. While this demonstrates economic stamina and persisting inflation, all eyes are on RBA’s next steps. Hogan postulates that the RBA Board, under leadership of the new Governor Michele Bullock, will likely adopt a patient stance. However, he doesn’t rule out further monetary tightening, possibly “in early November on Melbourne Cup day,” should the economic indicators not align with RBA’s projections of a slowdown.

New Zealand’s trade data sees China dominates decline in exports and imports

In August, New Zealand observed a dip in both its goods exports and imports compared to the previous year, leading to a monthly trade deficit of NZD -2.3B.

Compared to figures from August 2022, goods exports saw a reduction of NZD -296m, marking a -5.6% yoy drop, settling at NZD 5.0B. On the other hand, goods imports displayed an even steeper decline, shrinking by NZD -639m or -8.1% yoy, amounting to NZD 7.3B.

A deeper dive into the export figures revealed China as the major contributor to the monthly dip. Exports to China fell sharply by NZD -262m, representing an -18% yoy decline. Other notable declines were witnessed in exports to Australia, which dipped by NZD -71m (-9.0% yoy), and Japan, with a decrease of NZD -34m (-11% yoy). However, there was some silver lining with US and EU. Exports to the USA grew by NZD 62m, marking a 9.6% yoy increase, and those to the EU surged by NZD 28m, a 7.7% yoy rise.

China also took the lead in the contraction in imports. Imports from China plummeted by NZD -363m, a stark -19% yoy decline. Other significant reductions in imports were observed from Australia, down by NZD -92m (-9.7% yoy), South Korea with a drop of NZD -74m (-13% yoy), and US decreasing by NZD -36m (-5.4% yoy). In contrast, imports from EU displayed a robust growth, climbing by NZD 120m or 12% yoy.

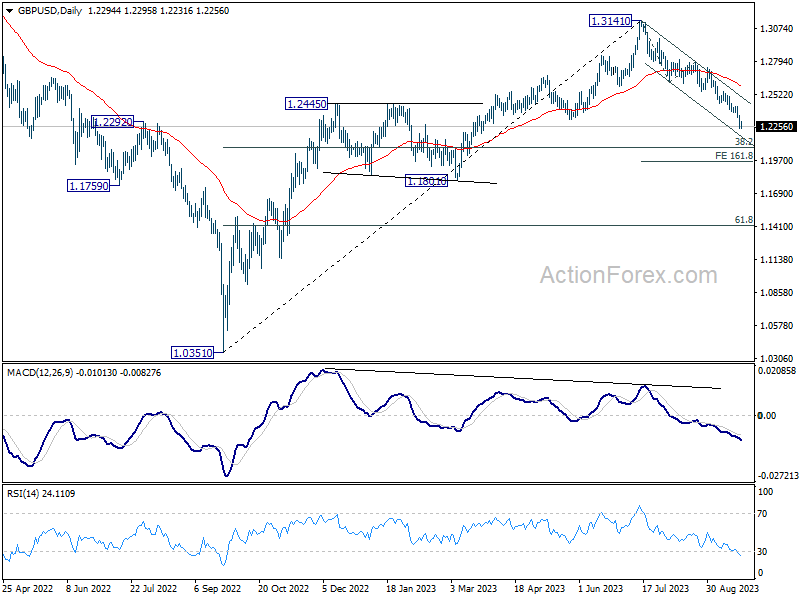

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2237; (P) 1.2293; (R1) 1.2352; More…

GBP/USD’s decline continues today and intraday bias stays on the downside. Current fall from 1.3141 should target 1.2075 fibonacci level. On the upside, above 1.2369 minor resistance will turn intraday bias neutral and bring consolidations. But near term outlook will stay bearish as long as 1.2618 support turned resistance holds, in case of strong recovery.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. However, sustained break of 1.2075 will raise the chance of bearish trend reversal.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Aug | -2291M | -1107M | -1177M | |

| 23:00 | AUD | Manufacturing PMI Sep P | 48.2 | 49.6 | ||

| 23:00 | AUD | Services PMI Sep P | 50.5 | 47.8 | ||

| 23:01 | GBP | GfK Consumer Confidence Sep | -21 | -27 | -25 | |

| 23:30 | JPY | National CPI Y/Y Aug | 3.20% | 3.30% | ||

| 23:30 | JPY | National CPI ex-Fresh Food Y/Y Aug | 3.10% | 3.00% | 3.10% | |

| 23:30 | JPY | National CPI ex Food Energy Y/Y Aug | 4.30% | 4.30% | ||

| 00:30 | JPY | Manufacturing PMI Sep P | 48.6 | 49.9 | 49.6 | |

| 02:52 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 06:00 | GBP | Retail Sales M/M Aug | 0.40% | 0.50% | -1.20% | -1.10% |

| 07:15 | EUR | France Manufacturing PMI Sep P | 43.6 | 46 | 46 | |

| 07:15 | EUR | France Services PMI Sep P | 43.9 | 46 | 46 | |

| 07:30 | EUR | Germany Manufacturing PMI Sep P | 39.8 | 39.5 | 39.1 | |

| 07:30 | EUR | Germany Services PMI Sep P | 49.8 | 47.1 | 47.3 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Sep P | 43.4 | 44 | 43.5 | |

| 08:00 | EUR | Eurozone Services PMI Sep P | 48.4 | 47.5 | 47.9 | |

| 08:30 | GBP | Manufacturing PMI Sep P | 44.2 | 43 | 43 | |

| 08:30 | GBP | Services PMI Sep P | 47.2 | 49 | 49.5 | |

| 12:30 | CAD | Retail Sales M/M Jul | 0.30% | 0.40% | 0.10% | |

| 12:30 | CAD | Retail Sales ex Autos M/M Jul | 1.00% | 0.50% | -0.80% | -0.70% |

| 13:45 | USD | Manufacturing PMI Sep P | 47.8 | 47.9 | ||

| 13:45 | USD | Services PMI Sep P | 50.3 | 50.5 |

{kind=link}