The tumultuous environment resulting from the Middle East tensions has prompted a noticeable upswing in Gold and Oil prices today, yet the forex markets remain relatively unaffected. Swiss Franc is currently leading the pack, its ascent likely attributed to the ongoing geopolitical unrest, though its rise is modest. US President Joe Biden’s diplomatic mission to Israel aims to alleviate the regional tensions; however, the impact of this intervention remains uncertain.

Yen is claiming the spot as the second strongest performer, bolstered by 10-year JGB yield reaching its peak since 2013. This surge in yield is ostensibly linked to anticipations of BoJ revising its inflation forecast upwards, potentially allowing for more yield curve control flexibility.

Conversely, Australian Dollar’s gains, initially sparked by encouraging Chinese economic indicators, were short-lived. Euro presently trails as the day’s weakest currency, with New Zealand Dollar and Dollar following suit. British Pound is maintaining a neutral stance, seemingly unaffected by the marginally higher consumer inflation figures.

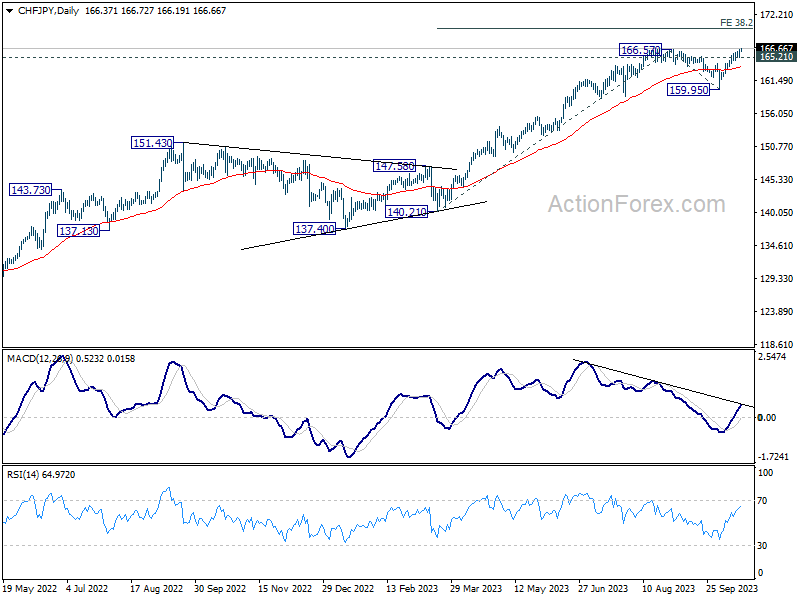

From a technical standpoint, CHF/JPY’s break of 166.57 resistance suggests that long term up trend is trying to resume. Further rally is expected as long as 165.21 minor support holds. Next target is 38.2% projection of 140.21 to 166.57 from 159.95 at 170.01. However, break of 165.21 will delay the bullish case and bring more consolidations first.

In Europe, at the time of writing, FTSE is down -0.57%. DAX is down -0.48%. CAC is down -0.44%. Germany 10-year yield is up 0.029 at 2.901. Earlier in Asia, Nikkei rose 0.01%. Hong Kong HSI dropped -0.23%. China Shanghai SSE dropped -0.80%. Singapore Strait Times dropped -1.11%. Japan 10-year JGB yield rose 0.0230 to 0.808.

Eurozone CPI finalized at 4.3% yoy in Sep, core CPI at 4.5% yoy

Eurozone CPI was finalized at 4.3% yoy in September, down from 5.2% yoy in August. Core CPI was finalized at 4.5% yoy, down from prior month’s 5.3% yoy.

The highest contribution to the annual Eurozone inflation rate came from services (+2.05 percentage points, pp), followed by food, alcohol & tobacco (+1.78 pp), non-energy industrial goods (+1.06 pp) and energy (-0.55 pp).

EU CPI was finalized 4.9% yoy, down from August’s 5.9% yoy. The lowest annual rates were registered in the Netherlands (-0.3%), Denmark (0.6%) and Belgium (0.7%). The highest annual rates were recorded in Hungary (12.2%), Romania (9.2%) and Slovakia (9.0%). Compared with August, annual inflation fell in twenty-one Member States, remained stable in one and rose in five.

UK CPI unchanged at 6.7% yoy in Sep, services inflation back at 3-decade high

UK CPI was unchanged at 6.7% yoy in September, above expectation of slowing to 6.6% yoy. CPI core (excluding energy, food, alcohol and tobacco) slowed from 6.2% yoy to 6.1% yoy, above expectation of 6.0% yoy.

CPI goods annual rate fell slightly from 6.3% to 6.2%. CPI services annual rate rose from 6.8% to 6.9%, joint highest rate (with May 2023) since March 1992.

On a monthly basis, CPI rose 0.5% mom, above expectation of 0.4% mom, quickly than prior month’s 0.3% mom.

RBA’s Bullock highlights sticky services inflation, housing and job market

RBA Governor Michele Bullock voiced concerns over stickiness in services inflation, rising house prices and tight labor market at an Australian Financial Security Authority event.

“We’re seeing a slowdown in consumption,” Bullock said, pointing out a decline in per capita consumption. This can be attributed to the central bank’s policy measures, as indicated by her remark, “monetary policy is starting to bite.” She elaborated that businesses were starting to find it hard to pass on cost increases as demand begins to taper.

However, the stickiness of inflation remains a significant concern. Bullock highlighted a stubborn rise in services inflation, which encompasses various sectors, from restaurants to hairdressers. “That inflation is running at a bit over 4 per cent,” she noted, acknowledging it exceeds RBA’s target and mirrors inflationary trends observed globally.

Additionally, housing prices are on the rise again, coupled with a tight employment market, contributing to inflationary pressures. These economic elements, combined with external factors such as the Israel-Gaza conflict escalating fuel costs, suggest that inflation might remain a persistent issue.

Australia’s Westpac Index reports fourteenth month in red, despite marginal improvement.

Australia’s economic outlook remains subdued as indicated by the Westpac Leading Index, which, though it rose slightly from -0.48% to -0.34% in September, continues to signal prolonged weak conditions. Fourteen successive months of subzero readings on the headline index growth rate project that the anaemic sub-trend growth momentum is anticipated to linger into 2024.

Westpac anticipates the nation’s GDP growth to decelerate to 1.2% in 2023, maintaining this tepid pace into the initial half of 2024, with an annualized growth rate pegged at 1.1%. This projection is notably beneath the expected population growth, which is projected to hover around 2.3%.

The recent minutes from RBA’s October meeting shed light on the central bank’s discomfort with the current inflationary environment, revealing its “low tolerance” towards unexpected inflationary spikes.

As the market casts its gaze towards the upcoming RBA meeting slated for November 7, Westpac anticipates revisions in the near-term forecasts for headline inflation. However, adjustments to the central bank’s medium-term view, a critical determinant for any further rate hike, are not expected.

However, this anticipation hinges significantly on the unveiling of the September quarter CPI, scheduled for release on October 25. Any significant surprises in this data could recalibrate expectations and potentially prompt the RBA to rethink its stance.

China’s Q3 GDP growth beats expectations; IMF cautions on future prospects

China’s economy exhibited resilience in Q3, with GDP growing at 4.9% yoy, outpacing anticipated 4.5% yoy increase. However, this growth rate reflects deceleration from 6.3% yoy expansion observed in Q2. On quarterly basis, the economy grew 1.3% qoq, marking an improvement from revised 0.5% qoq in the preceding quarter and outpacing anticipated 1.0% qoq expansion.

Industrial output in September echoed the positive trend, registering a 4.5% yoy uptick, marginally above 4.3% yoy forecast. Retail sales also followed suit, with 5.5% yoy increase, surpassing expected 4.9% yoy rise. However, fixed asset investments underperformed expectations, with year-to-date growth of 3.1% yoy, slightly below anticipated 3.2%.

Despite these seemingly positive indicators, China’s National Bureau of Statistics sounded a note of caution. The NBS underscored the challenges posed by a complicated external environment and lackluster domestic demand, calling for enhanced efforts to fortify the economic recovery’s foundation.

Separately, International Monetary Fund adjusted its growth outlook for China downward, citing a “losing steam” recovery impacted significantly by the property sector’s frailty. IMF now projects China’s economy to grow by 5% in 2023 and 4.2% in 2024, a downward revision from its earlier forecast of 5.2% and 4.5% respectively.

The IMF’s report highlighted contraction in manufacturing purchasing managers’ indexes from April to August, coupled with additional weaknesses in real estate sector, as pivotal factors behind the revised forecast.

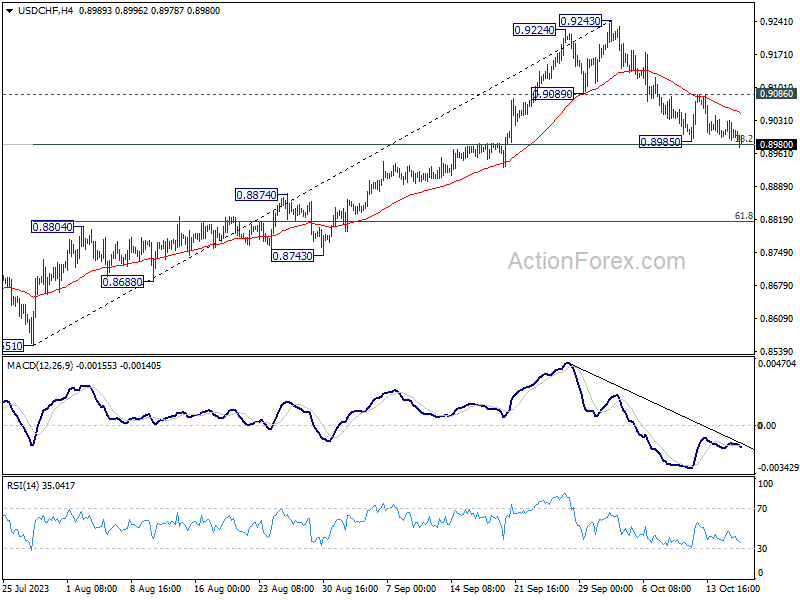

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8985; (P) 0.9008; (R1) 0.9027; More….

Immediate focus is now on 38.2% retracement of 0.8551 to 0.9243 at 0.8979. Sustained break there will extend the fall from 0.9243 to 61.8% retracement at 0.8815. That would also carry larger bearish implications. On the upside, however, , break of 0.9086 resistance will indicate that pull back from 0.9243 has completed, and turn bias to the upside for retesting this high.

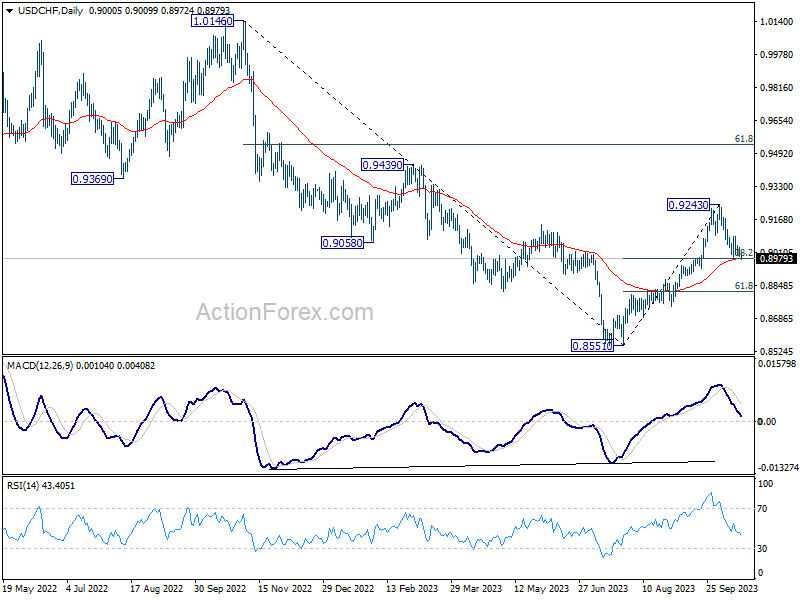

In the bigger picture, as long as 55 D EMA (now at 0.8976) holds rise from 0.8551 is viewed as reversing whole down trend from 1.0146 (2022 high). On resumption, further rise should be seen to 61.8% retracement of 1.0146 to 0.8551 at 0.9537 and above. However, sustained break of 55 D EMA will revive medium term bearishness, for retesting 0.8551 low at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/M Sep | 0.10% | -0.04% | ||

| 02:00 | CNY | GDP Y/Y Q3 | 4.90% | 4.50% | 6.30% | |

| 02:00 | CNY | Retail Sales Y/Y Sep | 5.50% | 4.90% | 4.60% | |

| 02:00 | CNY | Industrial Production Y/Y Sep | 4.50% | 4.30% | 4.50% | |

| 02:00 | CNY | Fixed Asset Investment (YTD) Y/Y Sep | 3.10% | 3.20% | 3.20% | |

| 06:00 | GBP | CPI M/M Sep | 0.50% | 0.40% | 0.30% | |

| 06:00 | GBP | CPI Y/Y Sep | 6.70% | 6.60% | 6.70% | |

| 06:00 | GBP | Core CPI Y/Y Sep | 6.10% | 6.00% | 6.20% | |

| 06:00 | GBP | RPI M/M Sep | 0.50% | 0.50% | 0.60% | |

| 06:00 | GBP | RPI Y/Y Sep | 8.90% | 8.90% | 9.10% | |

| 06:00 | GBP | PPI Input M/M Sep | 0.40% | 0.20% | 0.40% | 0.80% |

| 06:00 | GBP | PPI Input Y/Y Sep | -2.60% | -2.30% | -2.00% | |

| 06:00 | GBP | PPI Output M/M Sep | 0.40% | 0.30% | 0.20% | |

| 06:00 | GBP | PPI Output Y/Y Sep | -0.10% | -0.40% | -0.50% | |

| 06:00 | GBP | PPI Core Output M/M Sep | 0% | -0.10% | ||

| 06:00 | GBP | PPI Core Output Y/Y Sep | 0.70% | 1.60% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Sep F | 4.30% | 4.30% | 4.30% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Sep F | 4.50% | 4.50% | 4.50% | |

| 12:30 | USD | Building Permits M/M Sep | 1.47M | 1.45M | 1.54M | |

| 12:30 | USD | Housing Starts M/M Sep | 1.36M | 1.39M | 1.28M | |

| 14:30 | USD | Crude Oil Inventories | -0.5M | 10.2M | ||

| 18:00 | USD | Fed’s Beige Book |

{kind=link}