Yen is having a moderate rebound today, spurred by slightly stronger-than-expected corporate services price inflation data. However, this uptick in is showing only restrained momentum, especially noticeable even against a weaker Dollar. The limited rise can be attributed to low market activity, as there are no significant events scheduled for the day.

Nevertheless, this tranquility in the market is expected to be short-lived, as volatility is likely to escalate with the unfolding of high-profile events later in the week. Key events include inflation data releases from US, Eurozone, and Australia, along with RBNZ rate decision.

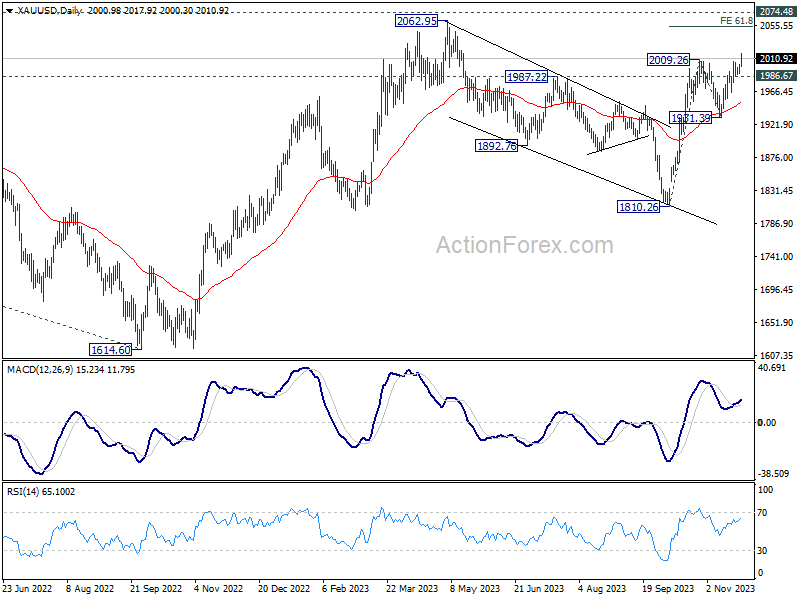

Technically, Gold finally breaks through 2009.26 resistance and resume near term rally to a six-month high in Asian session. Technically, further rally is expected as long as 1986.67 support holds. Next short-term target is 61.8% projection of 1810.26 to 2009.26 from 1931.39 at 2054.37. It remains to be seen if Gold is strong enough to break through 2074.48 long term resistance.

In Asia, Nikkei dropped -0.53%. Hong Kong HSI is down -0.16% China Shanghai SSE is down -0.30%. Singapore Strait Times is down -0.07%. Japan 10-year JGB yield closed flat at 0.778.

BoJ’s Ueda repeats uncertainty on stably achieving inflation target

In today’s address to the parliament, BoJ Governor Kazuo Ueda provided note that the economy is “recovering moderately,” which is further evidenced by the narrowing of the output gap to “near zero”.

Ueda also highlighted “We’re seeing some positive signs in wages and inflation”. However, he tempered this optimism by acknowledging the “high uncertainty on whether this cycle will strengthen”

A key point in Ueda’s commentary was BoJ’s stance on inflation. Despite the positive signs, he stated that the central bank cannot yet assert with confidence that inflation will sustainably and stably achieve its 2% target.

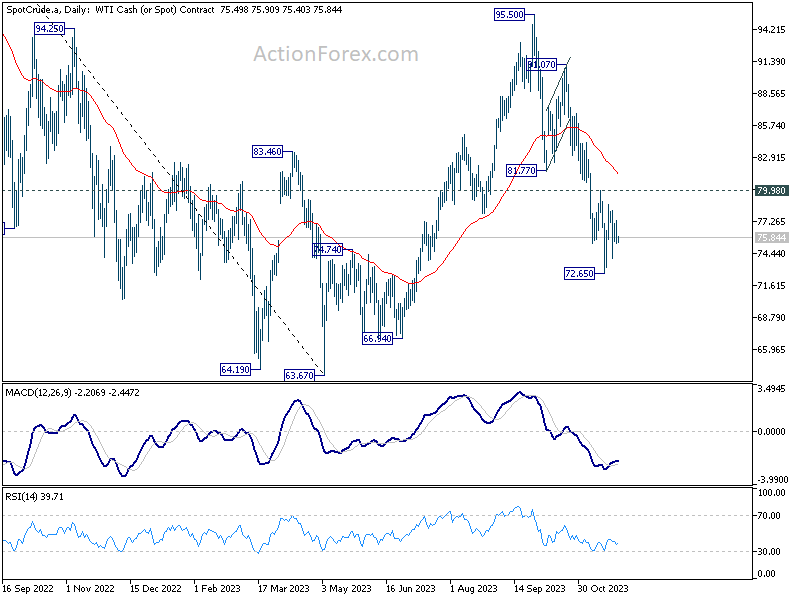

WTI oil staying near-term bearish, anticipating delayed OPEC+ decisions

In the current oil market, stability reigns as prices stay in the near-term range, with all eyes on the impending delayed OPEC+ meeting scheduled for Thursday. There’s growing consensus, as per news reports in the past two days, that a compromise on 2024 output levels is within reach. However, it seems the most probable outcome will just be continuation of existing production cuts, rather than any new, drastic changes.

This outlook, predominantly unaltered barring any unexpected deepening of cuts, steers towards bearish sentiment for oil prices in the near term. A key factor influencing this view is rising inventory levels in US. Concurrently, economic growth in China, a major player in global oil demand, remains tepid. While there have been some positive signs in China, they are not robust enough to shift the demand dynamics significantly.

Another critical element in this equation is Saudi Arabia’s decision regarding its additional voluntary cut of 1 million barrels per day, which is nearing its expiry at the end of December.

From a technical standpoint, near term outlook in WTI crude oil stays bearish with 79.98 resistance holds. Current fall from 95.50 if expected to extend through 72.56 to 63.37/66.94 support zone. But strong support would likely be seen to to bring rebound. Overall, range trading should continue for the medium term above 63.67, barring another significant developments.

Focus Shifts to RBNZ, Inflation Reports from US, Eurozone, Australia, and China PMIs

RBNZ is widely expected to hold the Official Cash Rate steady at 5.50% on Wednesday. Accompanying this decision will be the quarterly Monetary Policy Statement, which will include new economic forecasts. Despite some speculation about potential rate cuts in 2024, RBNZ’s projections may not strongly reflect this, especially considering the recent resurgence in energy prices. This could imply that the RBNZ may either need to hike rates further or maintain the current levels for an extended period, with the latter seeming more likely. In terms of central bank activities, Fed is also set to release its Beige Book economic report, offering insights into the economic conditions across various regions.

On the data front, key inflation figures are due from several major economies. US will release its PCE and core PCE price indexes, while Eurozone will publish its CPI flash data. Australia’s monthly CPI data is also awaited. These inflation reports are crucial for central banks like Fed and ECB, as they could influence the timing and pace of upcoming rate cuts and pace of policy loosening next year. Although Australia’s more critical quarterly CPI data will come in January, the upcoming monthly figures will still play a role in shaping market expectations regarding RBA’s next moves.

Canada’s employment data is another significant release that could impact the forex markets. Particularly, following a strong market response to Canada’s recent robust retail sales data, another set of positive employment figures could potentially trigger a notably rally in Loonie.

Lastly, economic indicators from China, including the official and Caixin PMI reports, will be closely watched. These reports are vital in supporting the recent rally in commodity prices, as they provide insights into the Chinese economy’s health, a major player in global commodity demand.

Here are some highlights for the week:

- Monday: Japan corporate service price index; US new home sales.

- Tuesday: Australia retail sales; Germany Gfk consumer climate; Eurozone M3 money supply; US house price index, consumer confidence.

- Wednesday: Australia CPI; RBNZ rate decision; Germany CPI flash; UK M4 money supply, mortgage approvals; Canada current account; US GDP revision, goods trade balance, Fed’s Beige Book report.

- Thursday: Japan industrial production, retail sales, consumer confidence, housing starts; New Zealand ANZ business confidence; China official PMIs; Germany retail sales; Swiss KOF economic barometer, retail sales; Eurozone unemployment rate, CPI flash; US personal income an spending, PCE price index, Chicago PMI, pending home sales.

- Friday: Japan unemployment rate, capital spending, PMI manufacturing final; China Caixin PMI manufacturing; Swiss GDP, PMI manufacturing; Eurozone PMI manufacturing final; UK PMI manufacturing final; Canada employment; US ISM manufacturing.

USD/JPY Daily Outlook

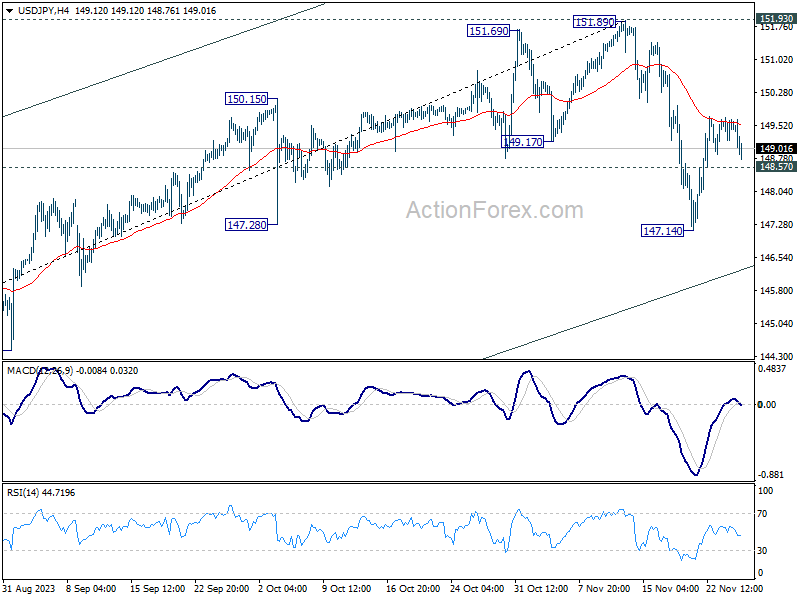

Daily Pivots: (S1) 149.19; (P) 149.45; (R1) 149.70; More…

USD/JPY dips notably today but stays above 148.57 minor support. Intraday bias remains neutral at this point. Risk stays on the downside as long as 55 4H EMA (now at 149.55) holds. Break of 148.57 minor support will turn bias to the downside the resume the fall from 151.89 through 147.14 support. However sustained break of 55 4H EMA will revive near term bullishness, and target a retest on 151.89/93 resistance zone

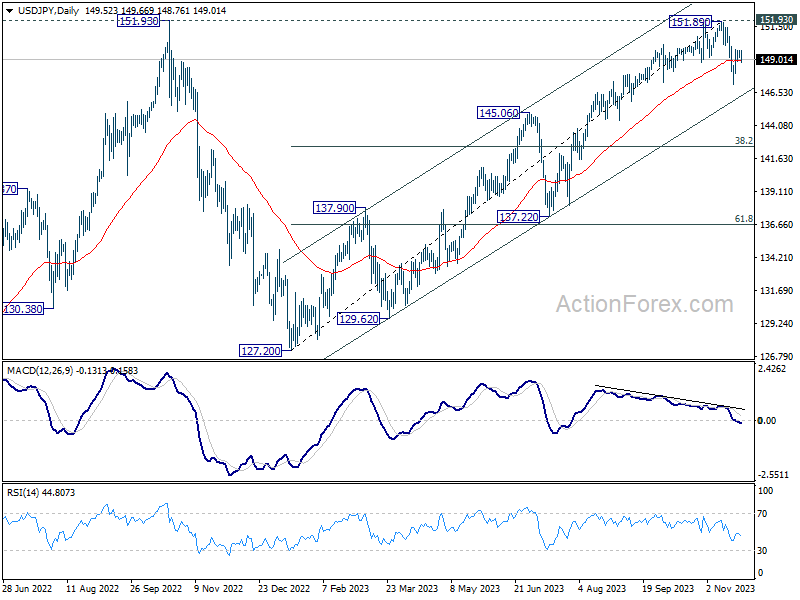

In the bigger picture, rise from 127.20 (2023 low) is seen as the second leg of the pattern from 151.93 (2022 high). Decisive break of 145.06 resistance turned support will confirm that this second leg has completed, after rejection by 151.93. Deeper fall would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. Nevertheless strong bounce from 145.06 will retain medium term bullishness for another test on 151.93 at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Oct | 2.30% | 2.10% | 2.10% | |

| 15:00 | USD | New Home Sales M/M Oct | 725K | 759K |

{kind=link}