Dollar, Yen, and Swiss Franc emerge as the predominant winners as markets enter into US session, amidst a backdrop of mild risk-off sentiment. Nevertheless, momentum of these safe-haven currencies remains relatively tempered, holding off major range breakouts across the most traded currency pairs. Traders, particularly those focusing on Dollar, seem poised on the sidelines, awaiting tomorrow’s PCE inflation data from US. This upcoming release is anticipated to shed light on whether the disinflationary trend has stalled, as indicated by the latest CPI data.

Conversely, New Zealand Dollar languishes as the day’s most significant underperformer, following RBNZ’s decision to maintain interest rates unchanged. Australian Dollar trails closely, dampened by CPI reading that fell short of expectations, while Canadian Dollar also faces downward pressure. Euro and Sterling find themselves in mixed positions, though Euro slightly edges out with a modest advantage.

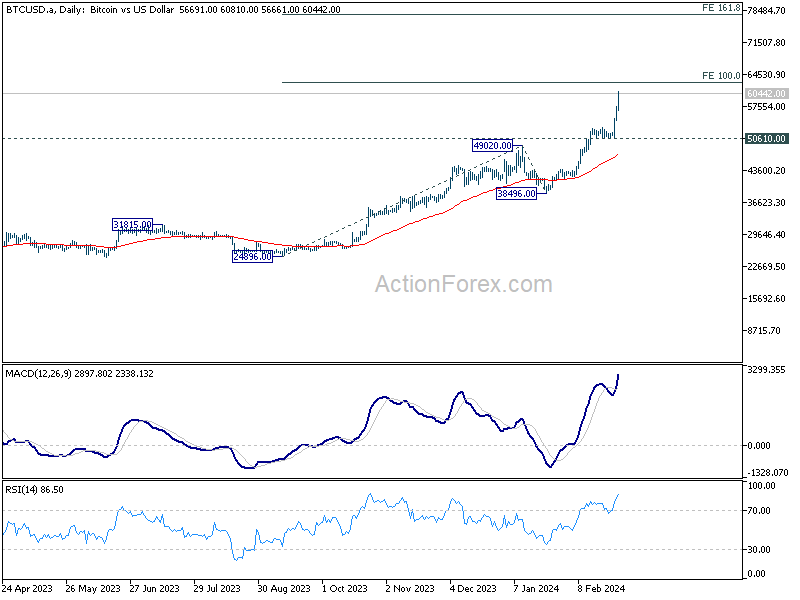

Technically, Bitcoin entered a phase of full upside acceleration this week, and breaks above 60k psychological level. Next target is 100% projection of 24896 to 49020 from 38496 at 62620. Decisive break there will pave the way to 68986 record high, or even further to 161.8% projection at 77528 next. In any case, outlook will now stay bullish as long as 50610 support holds.

In Europe, at the time of writing, FTSE is down -0.69%. DAX is up 0.23%. CAC is down -0.03%. UK 10-year yield is down -0.034 at 4.098. Germany 10-year yield is down -0.020 at 2.447. Earlier in Asia, Nikkei fell -0.08%. Hong Kong HSI fell -1.51%. China Shanghai SSE fell -1.91%. Singapore Strait Times fell -0.58%. Japan 10-year JGB yield rose 0.0022 to 0.698.

US goods trade deficit widens to USD -90.2B in Jan

US goods exports rose 0.2% mom to USD 170.42B in January. Goods imports rose 1.1% mom to USD 260.62B. Goods trade deficit widened to USD -90.2B, larger than expectation of -88.1B.

Wholesale inventories fell -0.1% mom to USD 896.8B. Retail inventories rose 0.5% mom to USD 804.8B.

ECB’s Kazimir on rate cut: June preferred, April a surprise, March a no go

In a Reuters interview, ECB Governing Council member Peter Kazimir emphasizd a cautious approach toward rate cuts. Kazimir explicitly stated, “There is no reason to rush a rate cut,” pinpointing June as his “preferred date”. “April would surprise me and March is a no go,” he added.

His comments reflect a strategic desire for a “smooth and steady cycle of policy easing,” contingent on a thorough assessment of the initial steps toward loosening monetary policy.

Kazimir highlighted the rapid disinflation observed at the “headline level”, albeit with remaining uncertainties around core inflation “because wage developments remain unclear.” The upcoming collective bargaining deals are deemed pivotal in clarifying this outlook.

Market forecasts now anticipating a 90bps reduction in interest rates by the year’s end, starting in June. Kazimir acknowledged this revised market sentiment as “more realistic.”

Eurozone economic sentiment falls to 95.4 in Feb, EU down to 95.4

Eurozone Economic Sentiment Indicator fell from 96.1 to 95.4 in February. Employment Expectations Indicator rose from 102.3 to 102.5. Economic Uncertainty Indicator fell from 21.3 to 20.1.

Eurozone industry confidence fell from -9.3 to -9.5. Services confidence fell from 8.4 to 6.0. Consumer confidence rose from -16.1 to -15.5 Retail trade confidence fell from -5.6 to -6.7. Construction confidence fell from -4.6 to -5.4.

EU Economic Sentiment Indicator fell from 95.8 to 95.4. Amongst the largest EU economies, the ESI deteriorated markedly in Italy (-1.6) and slightly in Germany (-0.6) and Poland (-0.5), while it improved strongly in the Netherlands (+1.7) and remained broadly stable in France (-0.3) and Spain (-0.2).

RBNZ keeps OCR at 5.50%, door still open for another hike

RBNZ decided to hold Official Cash Rate unchanged at 5.50%. The central bank expressed its confidence that the current OCR level is effectively restraining demand. However, it underscored the need for a “sustained decline in capacity pressures” to ensure that inflation re-aligns with 1 to 3% target range. This necessitates maintaining OCR “at a restrictive level for a sustained period of time”.

The updated economic forecasts in the MPS projects that CPI inflation will return to the target band by Q3 this year, then falls further to 2% midpoint by Q4 2025. These projections indicate a “slightly lower” inflation rate over the forecast period compared to previous estimates made in November.

Regarding future movements, the central bank anticipates OCR path to echo the trajectory outlined in the November MPS. It suggests OCR could peak at 5.6% in Q2 this year, leaving room for a marginal possibility of another rate hike.

Absent further increases, interest rate reductions are expected to commence in the Q2 2025, with OCR gradually decreasing to 3.2% by Q1 of 2027.

Australia monthly CPI unchanged at 3.4% in Jan, trimmed mean CPI down to 3.8%

Australia monthly CPI was unchanged at 3.4% yoy in January, below expectation of a rise to 3.6% yoy. CPI excluding volatile items and holiday travel slowed from 4.2% yoy to 4.1% yoy. Trimmed mean CPI also slowed from 4.0% yoy to 3.8% yoy.

The detailed breakdown reveals that the main inflationary pressures came from specific sectors: Housing costs rose by 4.6%, food and non-alcoholic beverages by 4.4%, alcohol and tobacco by a significant 6.7%, and insurance and financial services saw the highest increase at 8.2%.

These increases were somewhat mitigated by a decrease in the recreation and culture sector, notably a -1.7% drop, primarily driven by a -7.1% fall in Holiday travel and accommodation, which provided a counterbalance to the overall annual inflation rate.

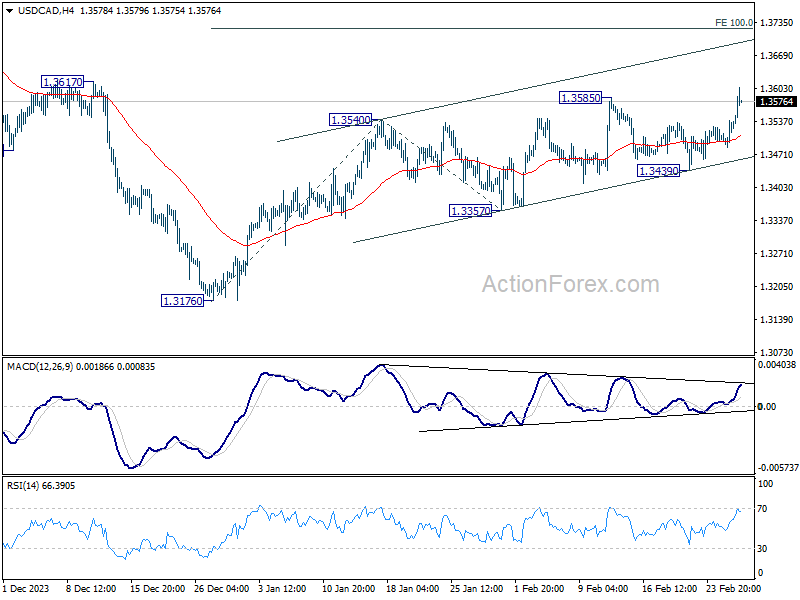

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3496; (P) 1.3518; (R1) 1.3550; More…

USD/CAD’s rally from 1.3176 is resuming today by breaking 1.3585 resistance. Intraday bias is back on the upside for 100% projection of 1.3761 to 1.3540 from 1.3357 at 1.3721 next. For now, near term outlook will stay bullish as long as 1.3439 support holds, in case of retreat.

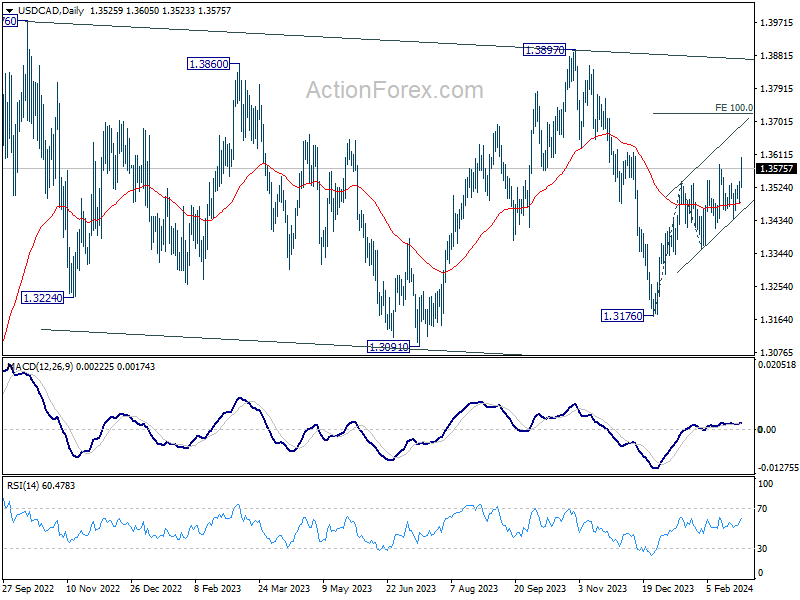

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Jan | 3.40% | 3.60% | 3.40% | |

| 00:30 | AUD | Construction Work Done Q4 | 0.70% | 0.80% | 1.30% | |

| 01:00 | NZD | RBNZ Interest Rate Decision | 5.50% | 5.50% | 5.50% | |

| 09:00 | CHF | Credit Suisse Economic Expectations Feb | 10.2 | -19.5 | ||

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Feb | 95.4 | 96.6 | 96.2 | 96.1 |

| 10:00 | EUR | Eurozone Industrial Confidence Feb | -9.5 | -9.2 | -9.4 | -9.3 |

| 10:00 | EUR | Eurozone Services Sentiment Feb | 6 | 9 | 8.8 | 8.4 |

| 10:00 | EUR | Eurozone Consumer Confidence Feb F | -15.5 | -15.5 | -15.5 | |

| 13:30 | CAD | Current Account Q4 | -1.6B | -1.9B | -3.22B | -4.7B |

| 13:30 | USD | GDP Annualized Q4 P | 3.20% | 3.30% | 3.30% | |

| 13:30 | USD | GDP Price Index Q4 P | 1.60% | 1.50% | 1.50% | |

| 13:30 | USD | Goods Trade Balance (USD) Jan P | -90.2B | -88.1B | -87.9B | |

| 13:30 | USD | Wholesale Inventories Jan P | 0.20% | 0.40% | ||

| 15:30 | USD | Crude Oil Inventories | 3.1M | 3.5M |

{kind=link}