Yen recovered modestly after BoJ held interest rates steady at 0.50%, in line with expectations. The decision came with no change to the existing bond taper plan, but with a new framework to gradually reduce bond purchases starting in fiscal 2026. Markets interpreted the move as largely symbolic for now, since implementation begins next year. Overall, reaction was subdued, with most major currencies trading within last week’s ranges.

BoJ’s decision to phase in bond tapering follows a spike in yields on super-long Japanese government bonds last month, which has increased fiscal strain. Finance Minister Katsunobu Kato warned that sustained high rates could worsen Japan’s fiscal health. BoJ Governor Ueda acknowledged waning demand for long-dated bonds and noted that yield volatility in those maturities risks bleeding into shorter-term rates with broader economic consequences.

Still, Yen’s rebound was limited as the market continues to price in a long period of policy inertia. Underlying inflation remains sluggish and economic growth is projected to moderate in the near term. With medium-term inflation expected to rise only gradually, the BoJ is sticking to a cautious path while monitoring global developments—especially on the trade front.

Trade diplomacy produced mixed results at the G7. The US and UK reached a new deal that preserves favorable tariff treatment for British autos and eliminates duties on aerospace exports, but left the steel and aluminum issue unresolved. The deal averts higher tariffs scheduled for next month, but Britain must meet new security conditions to keep its metals industry exempt. Prime Minister Starmer secured some concessions, but the agreement remains partial.

By contrast, Japan came away empty-handed from its bilateral session with the US Prime Minister Ishiba admitted to reporters that significant gaps remain, particularly on auto tariffs. The 25% levy on Japanese vehicles, along with other reciprocal tariffs, remains paused until July 9—but time is running out. Without a deal, Japan faces renewed headwinds just as its economy shows signs of softening.

Meanwhile, Canada and the US have committed to finalizing a comprehensive economic and security agreement within 30 days. While no details were released, both sides characterized the talks as constructive. These incremental steps highlight the fragmented state of global trade realignment as countries seek partial wins amid broader tensions.

In the forex market, Aussie and Kiwi outperform, while Euro follow with mild gains. Dollar, Swiss Franc, Yen and remain softer, with most pairs and crosses trapped inside last week’s ranges.

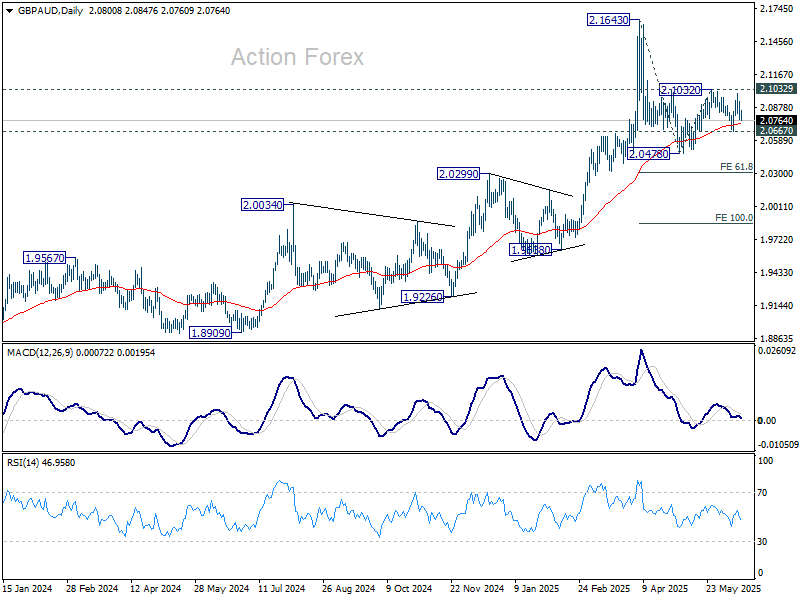

Technically, GBP/AUD was rejected by 2.1032 resistance again and focus is back on 2.0667 support. Firm break there will argue that the correction from 2.1643 is resuming with another down leg through 2.0478 support to 61.8% projection of 2.1643 to 2.0478 from 2.1032 at 2.0312. Nevertheless, break of 2.1032 will extend the rebound from 2.0478 to retest 2.1643 high.

In Asia, at the time of writing, Nikkei is up 0.46%. Hong Kong HSI is down -0.32%. China Shanghai SSE is down -0.08%. Singapore Strait Times is up 0.36%. Japan 10-year JGB yield is up 0.026 at 1.48. Overnight, DOW rose 0.75%. S&P 500 rose 0.94%. NASDAQ rose 1.52%. 10-year yield rose 0.028 to 4.452.

Looking ahead, Germany ZEW economic sentiment is the main feature in European session. Later in the day, US retail sales will take center stage. Import prices, industrial production and capactity utilization, business inventories, and NAHB housing index will also be released.

BoJ maintains policy, expects gradual rebound in inflation after near term weakness

BoJ kept its short-term interest rate unchanged at 0.5% in a unanimous decision today, while sticking with its current bond tapering program through March 2026. Looking further out, the central bank introduced a new bond purchase schedule for fiscal 2026, planning to reduce monthly purchases by JPY 200B each quarter, bringing the total to JPY 2T per month by March 2027.

In its statement, the BoJ downgraded its growth outlook, noting that Japan’s economy is “likely to moderate” in the near term as overseas economies slow and domestic corporate profits weaken. While accommodative financial conditions should provide some support, the central bank only expects a modest recovery later as global growth returns.

On inflation, the impact from food and import price increases is “expected to wane”, while underlying CPI is likely to remain “sluggish” due to a slowing economy. However, the bank anticipates that inflation will gradually pick up over time, supported by rising medium- to long-term inflation expectations and a growing “sense of labor shortage” as the economy recovers.

BoJ also acknowledged “extremely uncertain” outlook around the global trade and policy environment, warning of spillovers to Japan’s financial markets and inflation outlook. The statement emphasized the need to closely monitor foreign exchange developments and their broader implications.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 195.58; (P) 196.13; (R1) 197.14; More…

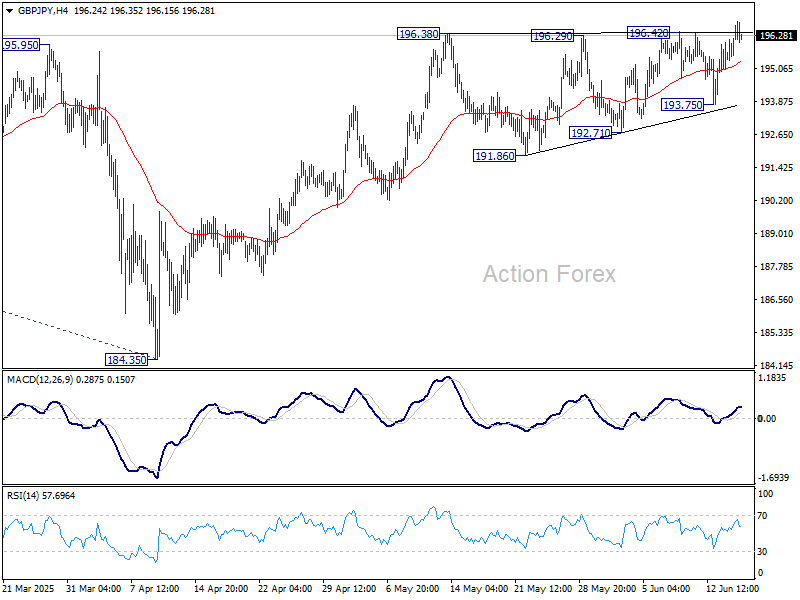

GBP/JPY retreated mildly after edging higher to 196.83. Yet, the breach of 196.42 resistance argues that rise recent rally is resuming. Intraday bias is mildly on the upside for 199.79 resistance first. Firm break there will target 100% projection of 180.00 to 199.79 from 184.35 at 204.14. For now, outlook will stay cautiously bullish as long as 193.75 support holds, in case of retreat.

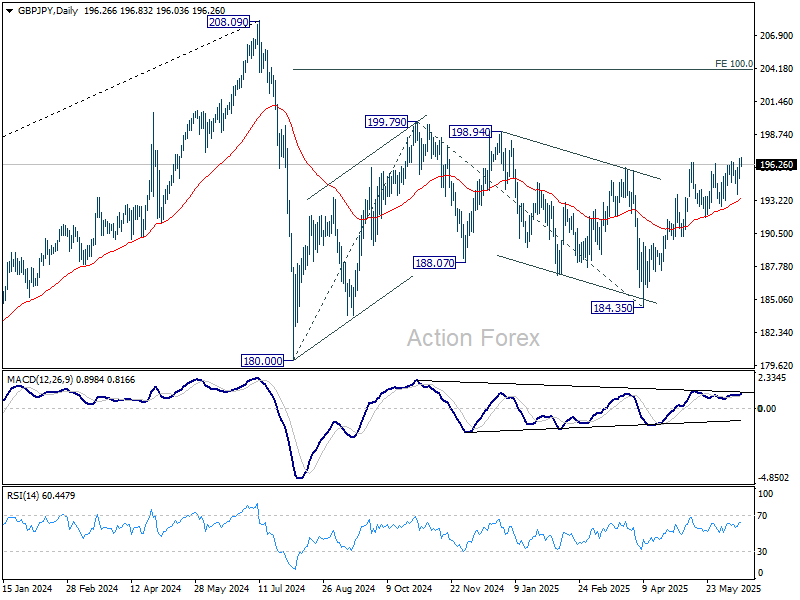

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

{kind=link}