Dollar remains under broad pressure midweek and is currently the weakest performer among major currencies. While dovish signals from Fed Vice Chair Michelle Bowman and Governor Christopher Waller cracked open the door for a July rate cut, that narrative has cooled. Several other Fed officials have voiced caution, pushing back on the idea of imminent easing, and markets have since trimmed the probability of a July move to below 20%.

Nonetheless, expectations for a September rate cut continue to gain momentum, with market pricing now showing an 85% chance, compared to around 65% a week ago. The key source of uncertainty remains the expiration of the 90-day reciprocal tariff truce with the US, set to end in early July. Without a breakthrough or de-escalation in trade talks, it’s hard to see the Fed moving as soon as July. September offers a more plausible window, and offers the Fed more flexibility to assess incoming data and policy developments.

EU–US trade tensions remain unresolved. European Commission Executive Vice-President Stephane Sejourne warned that Europe would need to “retaliate and rebalance” if the US insists on an asymmetrical deal similar to its pact with the UK. Though talks have reportedly accelerated, time is tight, and the risk of escalation still looms large over markets.

In currency markets, Swiss Franc leads as the strongest currency so far this week, followed by Sterling and Kiwi. Dollar remains at the bottom, trailed by the Loonie and Aussie. Yen and Euro are holding in the middle. There is a lack of unifying theme for now, except Dollar weakness.

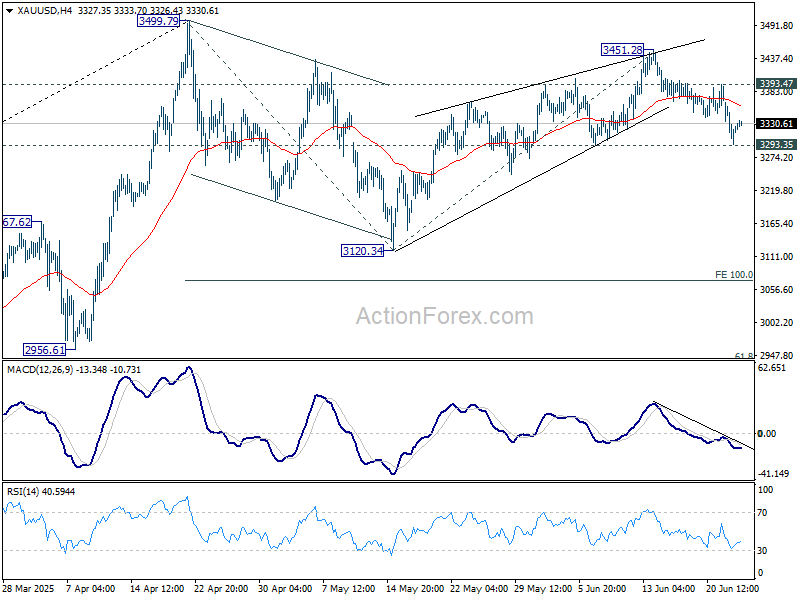

Technically, Gold recovered mildly after drawing support from 3293.35, but overall outlook is unchanged. Fall from 3451.28 is seen as the third leg of the corrective pattern from 3499.79 high. Firm break of 3293.35 support will solidify this case, and target 3120.34 support and possibly below.

In Asia, at the time of writing, Nikkei is up 0.31%. Hong Kong HSI is up 0.85%. China Shanghai SSE is up 0.45%. Singapore Strait Times is up 0.46%. Japan 10-year JGB yield is down -0.018 at 1.401. Overnight, DOW rose 1.19%. S&P 500 rose 1.11%. NASDAQ rose 1.43%. 10-year yield fell -0.027 to 4.293.

BoJ: Split emerges over of tariffs impact and rising domestic prices

BoJ’s Summary of Opinions from its June 16–17 meeting highlighted a growing divide among policymakers over the risks posed by US tariffs. While recent hard data for April and May “relatively solid”, several officials warned that the real effects of the tariffs have “yet to materialize”. One member emphasized the need to assess the impact carefully, as it would “certainly” weigh on bsusiness sentiment, while another described the economy as “somewhat stagnant.”

Still, the board was not unanimous in its pessimism. Some members maintained that the damage from tariffs would be limited, pointing to robust wage growth and stable consumer inflation. One member even highlighted the influence of rice prices on “perceived inflation and inflation expectations”, urging close monitoring. Others noted that the domestic backdrop remains relatively firm, with wages rising and inflation slightly exceeding forecasts.

BoJ left its policy rate unchanged at 0.5% and decided to taper the pace of its bond holdings reduction more gradually starting next year.

BoJ’s Tamura: Will raise rates “without haste or delay” if outlook justifies It

BOJ board member Naoki Tamura said today that the central bank must remain prepared to adjust its policy rate “in a timely and appropriate manner” based on evolving data, even in the face of ongoing uncertainties. While real interest rates remain low, Tamura emphasized that rate hikes would be guided by evidence of sustained improvements in activity and inflation, stressing the need for being “without haste or delay”.

Tamura added that uncertainty is a constant in policy-making, but that should not paralyze decision-making. If the risks to inflation shift meaningfully to the upside or the likelihood of hitting the 2% target increases, the BoJ should be ready to “act decisively.”

Australia CPI slows to 2.1% yoy in May, weakest since October 2024

Australia’s monthly CPI eased more than expected in May, dropping from 2.4% yoy to 2.1% yoy, the lowest level since October 2024 and below forecasts of 2.4% yoy.

Underlying inflation also softened, with trimmed mean CPI falling from 2.8% yoy to 2.4% yoy, reinforcing signs that underlying price pressures are easing across the economy. Excluding volatile items and holiday travel, inflation ticked down slightly to 2.7% yoy from 2.8% yoy.

The largest annual price increases came from food and non-alcoholic beverages (+2.9%), housing (+2.0%), and alcohol and tobacco (+5.9%).

The overall print strengthens the case for additional RBA rate cuts in the second half of the year, particularly as disinflation broadens.

Fed’s Barr: Tariffs to push inflation higher, but policy can wait

Fed Governor Michael Barr warned that the recent wave of tariffs is likely to drive inflation higher, citing the potential “Higher short-term inflation expectations, supply chain adjustments, and second-round effects”. Speaking overnight, Barr acknowledged that this could add to inflation persistence even as the broader economy slows and unemployment, currently at 4.2%, edges higher.

Despite these headwinds, Barr said the Fed is in a good position to “wait and see” how economic conditions evolve before adjusting policy. He noted the “considerable uncertainty about tariff policies and their effects,” stressing that monetary policy requires balancing “tradeoffs” between supporting growth and containing inflation.

Fed’s Williams sees growth slowing to 1%, tariffs to push inflation to 3%

New York Fed President John Williams warned overnight that the combination of policy uncertainty, restrictive trade measures, and declining immigration will drag significantly on the US economy this year. He projects growth will decelerate to just 1%, with unemployment rising to 4.5% by the end of 2025. Williams also anticipates a near-term spike in inflation to 3%, driven by tariffs, though he expects that to slowly subside back toward 2% over the next two years.

While Williams described the hard economic data as still solid, he acknowledged a growing disconnect with softer indicators that point to rising concerns among consumers and businesses. Nonetheless, he welcomed signs that inflation expectations remain anchored despite recent price shocks.

Looking ahead, Williams emphasized that monetary policy will be guided by data due “over the next few months,” which will inform whether and when Fed should adjust interest rates. Though he reiterated that “interest rates eventually need to get back to more normal levels”, his comments suggest a wait-and-see approach remains the most likely course for now.

Fed’s Kashkari: Staying patient amid tariff uncertainty, sees strong economy

Minneapolis Fed President Neel Kashkari reiterated Fed’s cautious stance overnight, emphasizing that policymakers remain in “wait and see mode” as they monitor the economic fallout from tariff policy. He noted that while officials are hesitant to make any “dramatic changes” to the policy outlook just yet, their priority is to gain clarity on how tariffs will impact inflation and broader growth dynamics.

Kashkari struck a generally optimistic tone on the domestic economy, saying the fundamentals remain “quite strong” and that inflation appears to be trending back toward the 2% target. He pointed to recent data suggesting underlying inflation is running near 2.5%, which—while still above target—is showing a welcome moderation.

However, the lingering uncertainty around tariffs continues to cloud the outlook. Kashkari warned that “nervousness” around trade is leading some firms to pause investment and may amplify inflation risks. While ongoing negotiations offer a path forward, he made clear that “ultimately we need to see what actually happens and then adjust our analysis of the economy.”

Fed’s Schmid backs wait-and-see stance amid uncertainty

Speaking overnight, Kansas City Fed President Jeff Schmid called Fed’s “wait-and-see” stance appropriate, especially given that inflation remains above target and the effects of rising tariffs are still filtering through the economy. “The resilience of the economy gives us the time to observe how prices and the economy develop,” he added

Schmid noted that business contacts “almost uniformly” expect tariffs to drive prices higher and weigh on activity, putting Fed’s inflation and employment mandates at odds. But “there is far less clarity on when and by how much,” said Schmid, who argued there’s little justification for near-term rate adjustments until the economic picture becomes clearer.

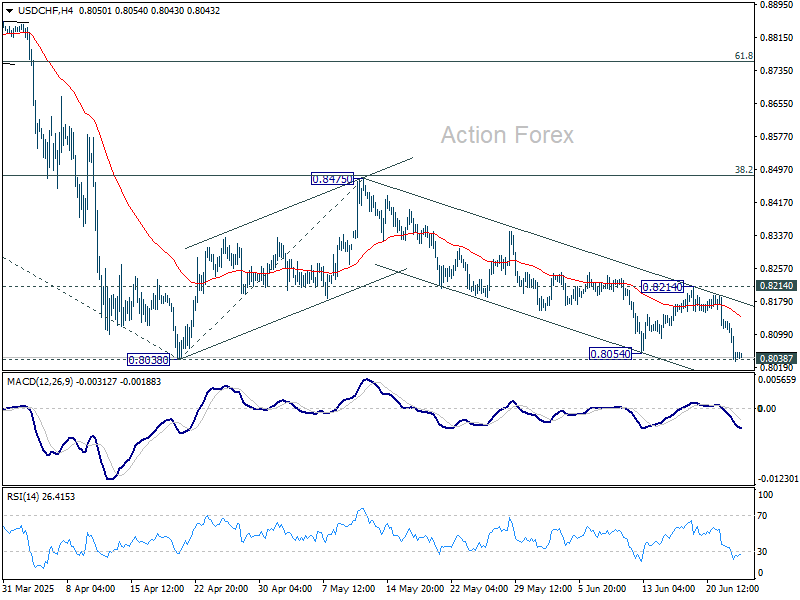

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8013; (P) 0.8074; (R1) 0.8114; More….

Immediate focus is now on 0.8038 low as fall from 0.8475 extends. Firm break there will confirm larger down trend resumption. Next target is 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757. For now, risk will stay on the downside as long as 0.8214 resistance holds, in case of recovery.

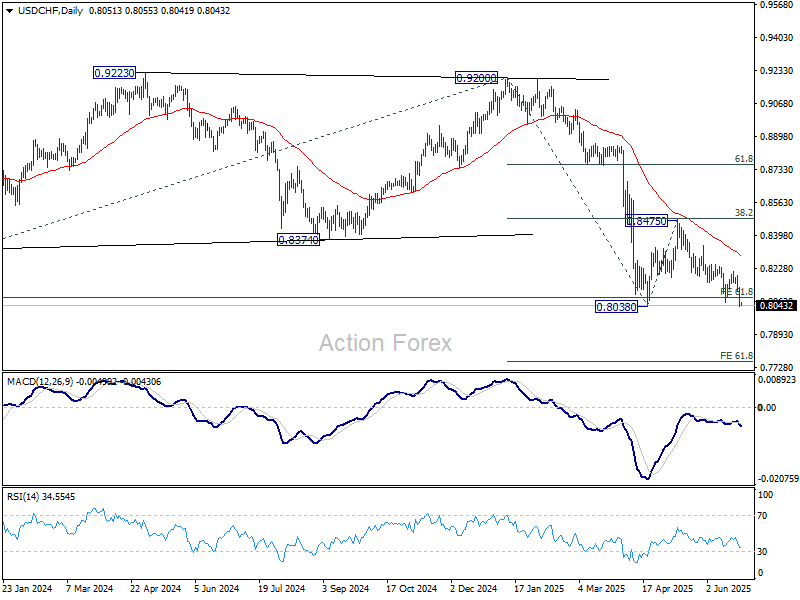

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8640) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

{kind=link}