Wednesday brought a lull in FX volatility as Dollar’s selloff eased, though it remained broadly under pressure for the week. The geopolitical backdrop is calmer, with the Israel-Iran ceasefire appearing stable for now. Trade talks seemed to be on hold, and with no major data releases on deck, markets are drifting into the second half of the week awaiting fresh signals.

Fed Chair Jerome Powell’s second day of testimony will garner attention, but few expect new revelations. His message Tuesday emphasized policy caution amid tariff uncertainty, and reiterated that inflation must remain anchored to support labor market strength. The path of interest rates remains clouded by unanswered questions on how deeply and persistently tariffs will feed into prices.

Following dovish signals from Vice Chair Bowman and Governor Waller, markets briefly speculated on a possible July rate cut. But a series of pushbacks from other Fed officials has brought expectations back to earth. The probability of a July cut has cooled to around 20%, with traders now placing 85% odds on a move in September—still contingent on upcoming data, particularly next week’s June non-farm payrolls.

Currency markets reflect this recalibration. Dollar remains weak but has edged off its lows, now the second-worst performer of the week after Loonie. Yen is not far behind as the third worst. Swiss Franc continues to lead, followed by the Pound and Kiwi. Euro and Aussie are holding in the middle of the pack.

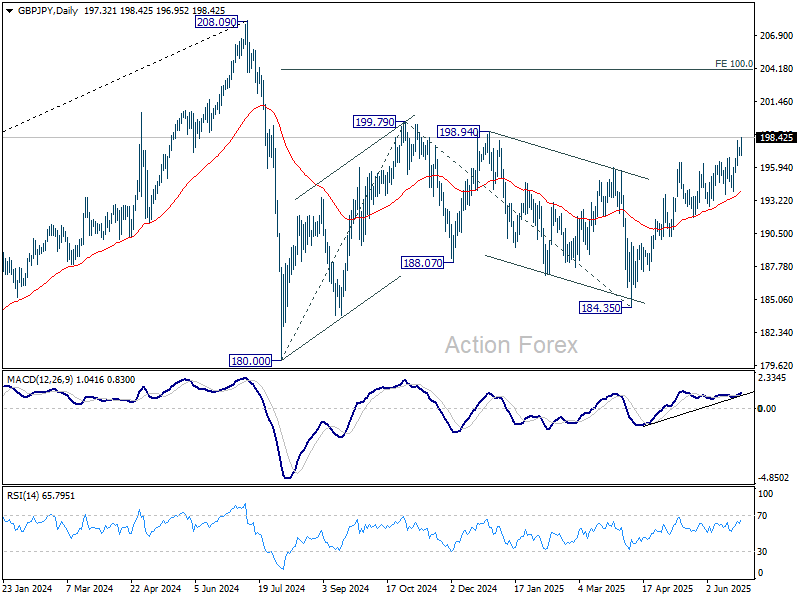

Technically, GBP/JPY’s rally is advancing today. Looking a D MACD, recent rise from 184.35 is accelerating slightly. Focus now turns to 199.79 resistance. Firm break there will resume the rise from 180.00, and target 100% projection of 180.00 to 199.79 from 184.35 at 204.14.

In Europe, at the time of writing, FTSE is down -0.09%. DAX is down -0.49%. CAC is down -0.47%. UK 10-year yield is up 0.015 at 4.494. Germany 10-year yield is up 0.031 at 2.578. Earlier in Asia, Nikkei rose 0.39%. Hong Kong HSI rose 1.23%. China Shanghai SSE rose 1.04%. Singapore Strait Times rose 0.56%. Japan 10-year JGB yield fell -0.015 to 1.405.

BoJ: Split emerges over of tariffs impact and rising domestic prices

BoJ’s Summary of Opinions from its June 16–17 meeting highlighted a growing divide among policymakers over the risks posed by US tariffs. While recent hard data for April and May “relatively solid”, several officials warned that the real effects of the tariffs have “yet to materialize”. One member emphasized the need to assess the impact carefully, as it would “certainly” weigh on business sentiment, while another described the economy as “somewhat stagnant.”

Still, the board was not unanimous in its pessimism. Some members maintained that the damage from tariffs would be limited, pointing to robust wage growth and stable consumer inflation. One member even highlighted the influence of rice prices on “perceived inflation and inflation expectations”, urging close monitoring. Others noted that the domestic backdrop remains relatively firm, with wages rising and inflation slightly exceeding forecasts.

BoJ left its policy rate unchanged at 0.5% and decided to taper the pace of its bond holdings reduction more gradually starting next year.

BoJ’s Tamura: Will raise rates “without haste or delay” if outlook justifies It

BOJ board member Naoki Tamura said today that the central bank must remain prepared to adjust its policy rate “in a timely and appropriate manner” based on evolving data, even in the face of ongoing uncertainties. While real interest rates remain low, Tamura emphasized that rate hikes would be guided by evidence of sustained improvements in activity and inflation, stressing the need for being “without haste or delay”.

Tamura added that uncertainty is a constant in policy-making, but that should not paralyze decision-making. If the risks to inflation shift meaningfully to the upside or the likelihood of hitting the 2% target increases, the BoJ should be ready to “act decisively.”

Australia CPI slows to 2.1% yoy in May, weakest since October 2024

Australia’s monthly CPI eased more than expected in May, dropping from 2.4% yoy to 2.1% yoy, the lowest level since October 2024 and below forecasts of 2.4% yoy.

Underlying inflation also softened, with trimmed mean CPI falling from 2.8% yoy to 2.4% yoy, reinforcing signs that underlying price pressures are easing across the economy. Excluding volatile items and holiday travel, inflation ticked down slightly to 2.7% yoy from 2.8% yoy.

The largest annual price increases came from food and non-alcoholic beverages (+2.9%), housing (+2.0%), and alcohol and tobacco (+5.9%).

The overall print strengthens the case for additional RBA rate cuts in the second half of the year, particularly as disinflation broadens.

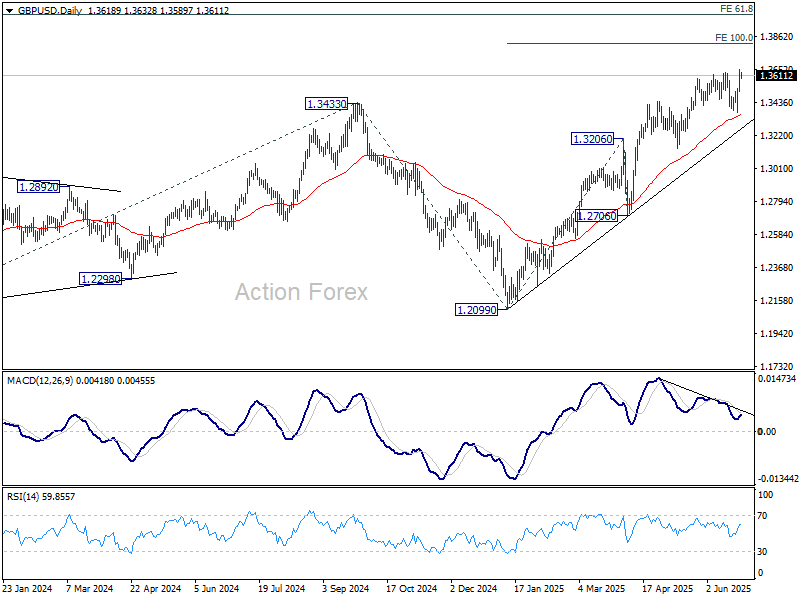

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3524; (P) 1.3586; (R1) 1.3678; More…

Intraday bias in GBP/USD stays on the upside despite today’s slight retreat. Rally from 1.2099 is resuming, and should target 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813. Outlook will now stay bullish as long as 1.3369 support holds, even in case of deeper pullback.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2948) holds, even in case of deep pullback.

{kind=link}