{kind=link}

Canadian Dollar eased modestly in early US trading after the BoC left its policy rate unchanged at 2.25%, as markets had fully expected. While the decision itself carried no surprises, the statement struck a slightly cautious tone on growth, prompting a mild pullback in CAD after its recent period of outperformance.

Policymakers reiterated that the bank has entered a long pause, but also highlighted that uncertainty surrounding the growth outlook remains elevated. Q4 GDP is expected to be weak, and the anticipated recovery in 2026 could still be derailed by trade volatility, structural headwinds and the ongoing adjustments to supply chains.

Even so, the BoC made clear it is not preparing to adjust interest rates again soon. With inflation expected to hover near target and domestic slack offsetting cost pressures tied to trade reconfiguration, policymakers see little justification for further moves unless a drastic shock emerges. That message keeps the easing cycle firmly in the rear-view mirror.

Attention now shifts to the FOMC decision later today. A 25bps cut is fully priced and universally expected, making the headline move largely irrelevant for markets. Instead, traders will focus on how the Fed shapes expectations for 2026 through the dot plot, the vote split, the statement, and Chair Jerome Powell’s press conference. With so many variables, volatility is almost guaranteed.

Away from North American monetary policy, the IMF raised its forecast for China’s 2026 economic growth by 0.3 percentage points to 4.5%, citing stronger domestic stimulus and lower-than-expected tariff effects. However, the Fund also made clear that China must accelerate its transition toward consumption-led growth.

IMF Managing Director Kristalina Georgieva argued that China is now too large an economy to rely on export-driven expansion. “Continuing to depend on export-like growth risks furthering global trade tensions,” she said, adding that accelerating the shift toward domestic demand would be “beneficial for China” and for the global economy.

Her comments coincided with a stark warning from the European Union Chamber of Commerce in China. The group said European companies are accelerating diversification away from Chinese supply chains as Beijing’s self-reliance agenda and export controls deepen uncertainty. The EU trade imbalance with China has widened to 1:4 in container terms, from 1:2.7 in 2019, exacerbated by persistent deflation and Yuan depreciation.

EU Chamber President Jens Eskelund highlighted that China has now recorded 37 consecutive months of factory-gate deflation. “When we have this gap between deflation in China and inflation in Europe, that adds to the imbalance in currency,” he said.

For the week so far, Swiss Franc is currently the best performer, followed by Kiwi, and then Dollar. Yen is still the weakest, followed by Loonie, and then Aussie. EUro and Sterling are positioning in the middle.

In Europe, at the time of writing, FTSE is up 0.25%. DAX is down -0.52%. CAC is down -0.40%. 10-year yield is up 0.022 at 4.526. Germany 10-year yield is up 0.011 at 2.868. Earlier in Asia, Nikkei fell -0.10%. Hong Kong HSI rose 0.42%. China Shanghai SSE fell -0.23%. Singapore Strait Times fell -0.03%. Japan 10-year JGB yield fell -0.001 to 1.963.

BoC holds steady, points to weak Q4 GDP and balanced inflation outlook

The BoC kept the overnight rate unchanged at 2.25% today, in line with expectations. The most notable element of the statement was the Governing Council’s assessment that, if inflation and economic activity evolve broadly as projected in October, the current policy rate is “about the right level.” This marks a clear signal that the easing cycle has effectively ended and that the bank has entered a long period of steady policy barring major surprises.

The statement acknowledged mixed growth dynamics heading into year-end. The Bank expects final domestic demand to expand in Q4, but weakness in net exports will leave overall GDP “likely weak.” Growth is projected to firm in 2026, though policymakers warned that uncertainty remains elevated and that swings in trade flows could continue to create quarter-to-quarter volatility.

Employment has posted solid gains over the past three months and the unemployment rate declined to 6.5% in November. However, job markets in trade-sensitive sectors “remain weak,” and economy-wide hiring intentions are still “subdued”—reflecting the broader drag from structural trade reconfiguration.

Despite these pressures, BoC expects the ongoing economic slack to counterbalance cost increases associated with shifting trade patterns. As a result, CPI inflation is still anticipated to stay close to the 2% target, providing the BoC with scope to maintain a steady hand for the foreseeable future.

China CPI hits 21-month high, but weak demand keeps PPI in deep negative

China’s November inflation data paint a picture of an economy showing modest signs of surface-level improvement while still grappling with entrenched deflationary pressures.

CPI accelerated from 0.2% yoy to 0.7% yoy, matching expectations and marking a 21-month high. The gain was driven primarily by food prices, which rose 0.2% yoy after a -2.9% yoy drop in October. Core inflation held steady at 1.2% yoy, while energy prices slid -3.4% yoy—an even deeper decline than the prior month.

On a monthly basis, CPI fell -0.1% mom after October’s 0.2% mom increase, contrary to expectations for another rise.

PPI slipped from –2.1% yoy to –2.2% yoy, extending China’s factory-gate deflation streak into a fourth year. Manufacturers continue to cut prices aggressively to clear excess supply, a sign that domestic and external demand remain too weak to absorb output.

Coal mining prices tumbled -11.8% yoy, while the oil and gas extraction sector saw a -10.3% yoy decline—deep drops that suggest little improvement in industrial profitability.

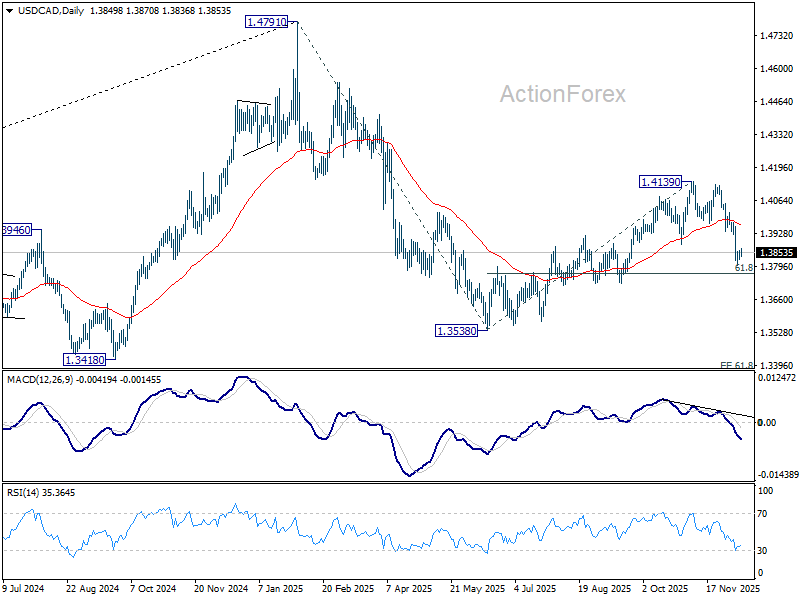

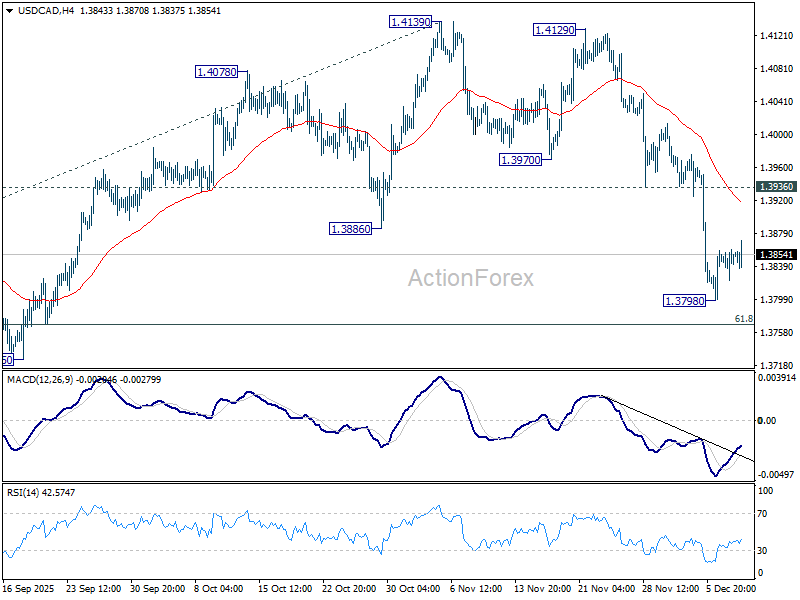

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3826; (P) 1.3844; (R1) 1.3863; More…

USD/CAD recovers mildly in early US session but outlook is unchanged. Intraday bias stays neutral and more consolidations could be seen. Upside of recovery should be limited below 1.3936 support turned resistance. On the downside, break of 1.3798 will resume the fall from 1.4139 to 61.8% retracement of 1.3538 to 1.4139 at 1.3768. Firm break there will argue that whole decline form 1.4791 might be ready to resume through 1.3538 low.

In the bigger picture, current development suggests that price actions from 1.4791 is developing into a deeper, larger scale correction. In the less bearish case, it’s just correcting the rise from 1.2005 (2021 low). But even so, break of 1.3538 will pave the way to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. This will remain the favored case as long as 1.4139 resistance holds, in case of rebound.