{kind=link}

Yen rallied broadly during the Asian session as weaker-than-expected Chinese data undermined regional risk sentiment. Retail sales disappointed sharply, reinforcing doubts about the strength of China’s domestic recovery and prompting a defensive tilt across FX markets.

Hopes that poor data would trigger fresh stimulus from Beijing failed to gain traction. Instead, markets appear increasingly focused on the limits of short-term policy support in the absence of deeper structural reform. The concern is that quick fixes can no longer offset entrenched weaknesses in confidence and balance sheets.

That view was echoed by the International Monetary Fund last week, which urged China to accelerate structural reforms and address the prolonged property slump. With around 70% of household wealth tied to real estate, the housing downturn continues to weigh heavily on consumption and broader economic momentum.

The IMF also cautioned that China’s size limits its ability to drive growth through exports alone. Continued reliance on export-led expansion risks exacerbating global trade tensions, particularly as tariff pressures remain in place. These warnings have reinforced investor skepticism toward cyclical and China-sensitive assets.

Yen has also drawn support from Japan’s domestic backdrop. Tankan survey data showed improving manufacturing sentiment, resilient capital expenditure plans, and inflation expectations stabilizing slightly above the BoJ’s 2% target, strengthening expectations for a rate hike later this week.

Although Japan’s economy contracted in the third quarter as exports faltered under U.S. tariffs, momentum appears to be turning. Exports and factory output have shown signs of recovery, supporting expectations that growth will rebound in the current quarter and allowing the BoJ to continue normalization cautiously.

For now, Yen leads FX gains, followed by Loonie and Dollar. Kiwi underperforms after weak services data, with Aussie and Sterling also lagging. Euro and Swiss Franc sit mid-pack.

Looking ahead, markets face a packed calendar with BoE, ECB, and BoJ decisions, but US CPI and labor data are likely to be the decisive drivers as markets approach year-end.

In Asia, Nikkei fell -1.18%. Hong Kong HSI is down -1.17%. China Shanghai SSE is down -0.35%. Singapore Strait Times is down -0.11%. Japan 10-year JGB yield rose 0.002 to 1.957.

Japan Tankan: Manufacturing sentiment improves as firms absorb tariff impact

Japan’s Q4 Tankan survey delivered a broadly supportive signal for the economy, reinforcing expectations that the BoJ will proceed with rate normalization. The large manufacturing index rose from 14 to 15, in line with expectations, marking a third consecutive quarterly improvement and the strongest reading since December 2021. The result suggests manufacturers have so far weathered the impact from higher U.S. tariffs better than feared.

Sentiment among non-manufacturers was less impressive, with the index unchanged at 34, falling short of expectations for a modest uptick. Even so, the divergence does not point to a meaningful deterioration in overall conditions, as services confidence remains elevated relative to historical norms.

Capital spending intentions added to the constructive tone. Large firms now plan to increase investment by 12.6% in the current fiscal year ending March 2026, slightly above market expectations of 12.0%.

The survey also indicated firms expect inflation to average 2.4% across one-, three-, and five-year horizons, suggesting expectations are stabilizing around the BoJ’s 2% target.

With tariff uncertainty easing and manufacturing sentiment holding firm, the survey supports the dominant market view that BoJ is positioned to raise rates in December, even as the pace of tightening beyond that remains gradual.

China data disappoints as consumption and investment weaken further

China’s November activity data delivered a broadly weaker-than-expected picture. Industrial production rose 4.8% yoy, missing expectations for 5.0% growth and marking the weakest pace since August 2024.

The sharper disappointment came from consumption. Retail sales rose just 1.3% yoy, far below expectations of 2.9% and slowing markedly from October’s 2.9% pace. It was also the weakest reading since December 2022.

Investment conditions also deteriorated. Year-to-date fixed asset investment fell -2.6%, deeper than expected -2.3% and the sharpest contraction since the pandemic in 2020. The drag from property intensified, with real estate investment down -15.9% in the first eleven months of the year, extending the slump seen earlier and reinforcing the view that the property sector remains a central constraint on China’s recovery.

RBNZ’s Breman sees OCR holding at 2.25% if outlook unfolds as expected

RBNZ Governor Anna Breman signaled in media interviews today that the bar for further near-term easing remains high. While the forward path published in the November Monetary Policy Statement allows for a small probability of another rate cut, Breman stressed “if economic conditions evolve as expected the OCR is likely to remain at its current level of 2.25 per cent for some time.”

Looking ahead to the next OCR decision in February, Breman said the central bank will continue to assess incoming data, financial conditions, and global developments, with a particular focus on implications for New Zealand’s economic outlook and its medium-term inflation objective.

Breman also reiterated that monetary policy is not on a preset course, highlighting the MPC’s regular meeting schedule as a reflection of that flexibility.

NZ BNZ service falls to 46.9, recovery hopes dented

New Zealand’s services sector slipped deeper into contraction in November, reinforcing signs that domestic demand remains fragile. BusinessNZ Performance of Services Index fell from 48.4 to 46.9, marking the lowest level of activity since May and sitting well below the survey’s long-run average of 52.8. All five sub-indices remained in contraction territory, underlining the broad-based nature of the slowdown.

Activity and sales saw the sharpest deterioration, dropping from 48.4 to 45.8, while employment also weakened from 48.6 to 46.4. New orders edged marginally higher from 49.2 to 49.3, offering little evidence of an imminent turnaround in demand.

BusinessNZ Chief Executive Katherine Rich said the November reading “put to bed” any immediate hope that the sector was moving toward expansion. While the proportion of negative comments eased slightly from recent months, businesses continued to cite a weak economic backdrop, low consumer confidence, high living costs, inflation, interest rates, and reduced spending as the dominant constraints on activity.

Final busy week before holidays puts NFP, CPI, BoE and BoJ in Focus

It is another event-packed week ahead before year-end holidays thin liquidity and mute follow-through. Three major central banks—BoE, ECB, and BoJ—will deliver policy decisions. But heavy-weight US data releases are expected to dominate price action and determine whether recent Dollar weakness turns from hesitation into conviction.

November US CPI and non-farm payrolls will be crucial in shaping expectations for the length of the Fed’s pause into early 2026. After last week’s risk-management cut, markets are largely priced for a January hold, while odds of a March move remain near 50%.

Fed Chair Jerome Powell has made it clear that policy focus has shifted toward employment rather than inflation. Tariff-related price pressures are increasingly viewed as transitory, reducing urgency to respond to short-term inflation noise. As a result, labor market data is likely to carry more weight than CPI in determining near-term Dollar direction, especially if hiring c shows further renewed deterioration.

In the UK, BoE is widely expected to deliver a 25bps rate cut to 3.75% on Thursday. Market concerns around the Autumn Budget have faded without disruption, while recent data suggests inflation has peaked lower than previously feared. The policy decision itself is well priced, leaving attention firmly on what comes next.

That BoE outlook remains uncertain. A recent Reuters poll shows no clear consensus on the 2026 rate path. Around two-thirds of economists expect a follow-up cut to 3.50% by end-March, while median forecasts see rates bottoming at 3.25% in Q3, implying two additional cuts next year. Voting patterns and Governor Andrew Bailey’s press conference will be scrutinized, though both are likely to highlight internal MPC splits rather than provide firm guidance.

ECB policy looks far more settled. Officials have been explicit that they are comfortable with the Deposit rate at 2.00%, with the bar for any move set high for the foreseeable future. According to Reuters polling, roughly 80% of economists expect rates to remain unchanged through mid-2026, with nearly three-quarters holding that view through year-end.

Speculation that the ECB’s next move could be a hike continues to circulate, but it remains premature. Markets and President Christine Lagarde are unlikely to entertain such discussions seriously . Instead, attention will fall on updated economic projections and sentiment indicators such as German ZEW and Ifo surveys.

In Japan, BoJ is now expected to raise rates by 25bps to 0.75%, following increasingly explicit signals from officials that normalization should resume. Governor Kazuo Ueda’s recent meeting with Prime Minister Sanae Takaichi is seen as political clearance for the move, reducing uncertainty around timing.

Even so, tightening beyond this week is expected to be slow and conditional. Future hikes will depend heavily on the outcome of next year’s Shunto wage negotiations, which appear constructive but not yet decisive. A Reuters poll shows just over two-thirds of economists expect rates to reach at least 1.00% by next September, while only a minority see 1.25% by end-2026. Japan’s Tankan survey and national CPI will help frame expectations.

Elsewhere, Canada CPI and retail sales will be watched for any challenge to BoC’s extended pause narrative, while New Zealand GDP will help gauge whether recent stabilization is evolving into a firmer recovery. PMI readings from major economies will provide timely growth signals, but unless they deliver clear surprises, they are likely to reinforce rather than redefine the week’s dominant US-driven themes.

Here are some highlights for the week:

- Monday: New Zealand BNZ services; Japan Tankan survey; China industrial production, retail sales, fixed asset investment; Swiss PPI, SECO economic forecasts; Eurozone industrial production; Canada CPI, manufacturing sales; US Empire state manufacturing.

- Tuesday: Australia PMIs, Westpac consumer confidence; UK employment PMIs; Eurozone PMIs, trade balance, Germany ZEW economic sentiment; US non-farm payrolls, retail sales, PMIs.

- Wednesday: Japan trade balance; UK CPI, PPI; Germany Ifo business climate; Eurozone CPI final.

- Thursday: New Zealand GDP; Swiss trade balance; BoE rate decision; ECB rate decision; US CPI, jobless claims, Philly Fed survey.

- Friday: New Zealand trade balance, ANZ business confidence; Japan CPI, BoJ rate decision; Germany Gfk consumer sentiment, PPI; UK retail sales; Canada retail sales; US existing home sales.

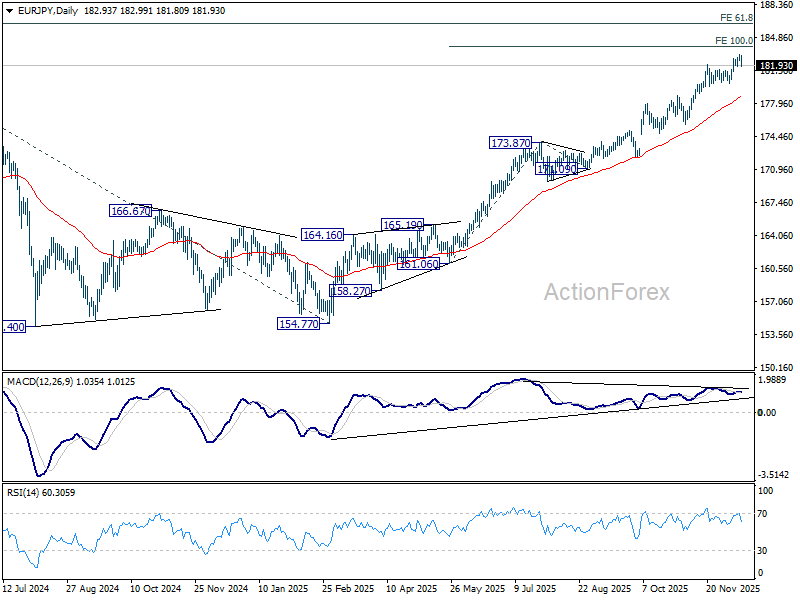

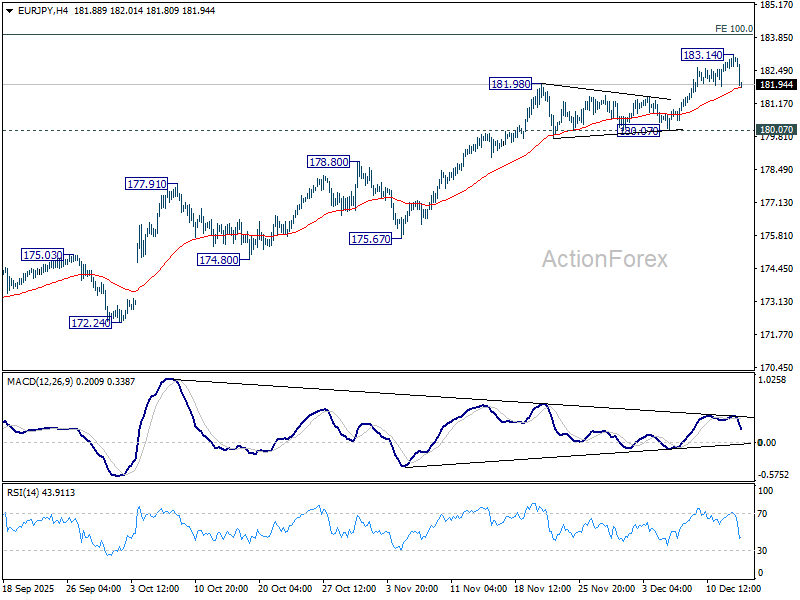

EUR/JPY Daily Outlook

Daily Pivots: (S1) 182.60; (P) 182.88; (R1) 183.23; More…

Intraday bias in EUR/JPY is turned neutral with current steep retreat and some consolidations would be seen below 187.14. Further rally remains in favor. But considering bearish divergence condition in both 4H and D MACD, upside should be limited 100% projection of 161.06 to 173.87 from 171.09 at 183.90, at least on first attempt. Meanwhile, firm break of 180.07 will confirm short term topping, and bring deeper correction to 55 D EMA (now at 178.59).

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, considering bearish divergence condition in D MACD, upside should be capped by 186.31 on first attempt. Outlook will continue to stay bullish as long as 55 W EMA (now at 170.73) holds, even in case of deep pullback.