{kind=link}

Yen rebounded broadly today, but the move appears driven more by pre-holiday profit-taking than a genuine shift in trend. Position squaring into year-end has offered temporary relief after recent weakness, yet price action lacks the conviction typically associated with durable reversals. There was also some support from stepped-up verbal intervention by Japanese officials. Authorities delivered their strongest warnings yet against excessive currency moves, helping to slow speculative pressure even if the impact remained short-lived.

Japanese Finance Minister Satsuki Katayama said the recent yen declines “absolutely do not reflect fundamentals,” adding that the government stands ready to take appropriate action against excessive moves. She suggested the scale of the Yen’s fall pointed to speculative behavior. Additionally, she referred to Japan’s September agreement with the U.S. on exchange-rate policy as a framework for possible intervention.

Yen sentiment also drew modest support from Prime Minister Sanae Takaichi, who emphasized that Japan’s national debt remains “still high.” She rejected irresponsible bond issuance or tax cuts, highlighting an effort to support growth without undermining confidence in Japan’s public finances or yen-denominated assets.

However, fiscal concerns remain a structural drag. Former BoJ policymaker Seiji Adachi argued bluntly that Yen weakness persists despite narrowing Japan–U.S. rate differentials, suggesting BOJ policy is no longer the main driver. Instead, he said investors are increasingly demanding a higher premium for Japan’s fiscal risk. Those concerns are already visible in rising Japanese government bond yields. Adachi warned it will be difficult to erase market doubts over Japan’s finances after proactive fiscal policies were so strongly emphasized, adding that higher bond yields could become the biggest risk to Japan’s economy next year.

Meanwhile, Dollar traded broadly lower, extending a soft year-end tone. Mixed U.S. data offered little support, with markets largely shrugging off the upward revision to Q3 GDP while focusing on sluggish October durable goods orders. Dollar is now on track for its weakest annual performance in eight years, and some see scope for further downside. Risks appear asymmetric, with attention increasingly centered on labor market health, while inflation concerns have been partially overshadowed. Additional uncertainty surrounds the prospect of a more politically influenced Fed following the replacement of Jerome Powell, which could tilt policy toward deeper easing. Still, that picture could shift early next year with December non-farm payrolls.

For now, Kiwi and Aussie lead gains alongside Yen, while Dollar sits at the bottom, followed by Euro and Sterling, with Swiss Franc and Loonie holding the middle ground.

In Europe, at the time of writing, FTSE is down -0.11%. DA is up 0.02%. CAC is down -0.31%. UK 10-year yield is down -0.06 at 4.532. Germany 10-year yield is down -0.018 at 2.882. Earlier in Asia, Nikkei rose 0.02%. Hong Kong HSI fell -0.11%. China Shanghai SSE rose 0.07%. Singapore Strait Times rose 0.62%. Japan 10-year JGB yield fell -0.041 to 2.040.

US durable goods fall -2.2% mom as transport orders drag

US durable goods orders fell -2.2% mom to USD 307.4B in October, undershooting expectations for a -1.5% decline. The weakness was driven largely by transportation equipment, which dropped -6.5% to USD 103.9B after two consecutive monthly increases.

Beneath the surface, underlying demand appeared more resilient. Orders excluding transportation rose 0.2% mom to USD 203.5B, in line with forecasts, suggesting steadier business investment outside volatile categories. Orders excluding defense declined -1.5% mom to USD 286.5B.

Canada GDP shrinks -0.3% mom as manufacturing drags, November looks firmer

Canada’s economy contracted in October, with real GDP falling by -0.3% mom, in line with expectations. The slowdown was broad-based, with 11 of 20 industrial sectors posting declines, highlighting ongoing softness across the economy.

Goods-producing industries were the main drag, falling -0.7% on the month as most components weakened. Manufacturing led the decline, reinforcing concerns that external demand and tighter financial conditions continue to weigh on Canada’s industrial base. Services-producing industries also slipped by -0.2%, partly reflecting labor stoppages that disrupted activity in several areas.

Looking ahead, early indications point to modest stabilization. Advance data suggest real GDP by industry rose 0.1% mom in November, supported by gains in educational services, construction, and transportation and warehousing. These were partly offset by renewed weakness in mining, quarrying, oil and gas extraction, and manufacturing.

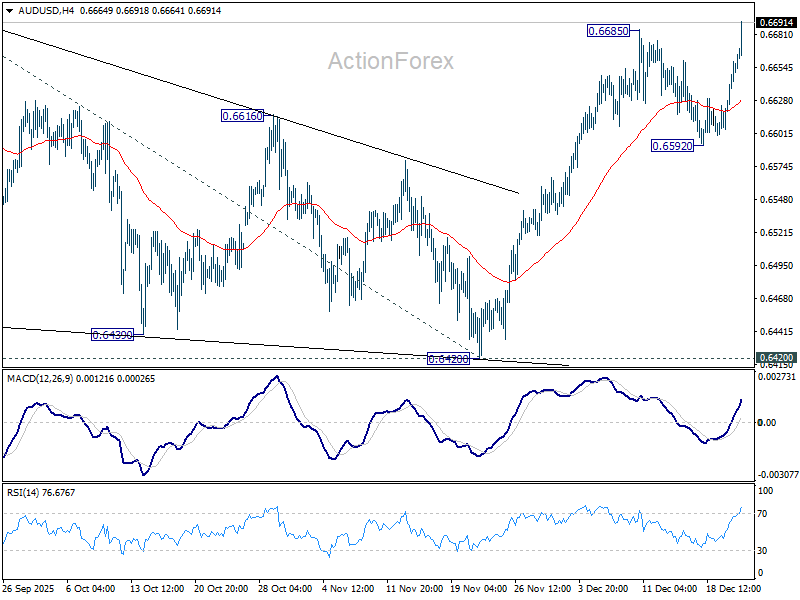

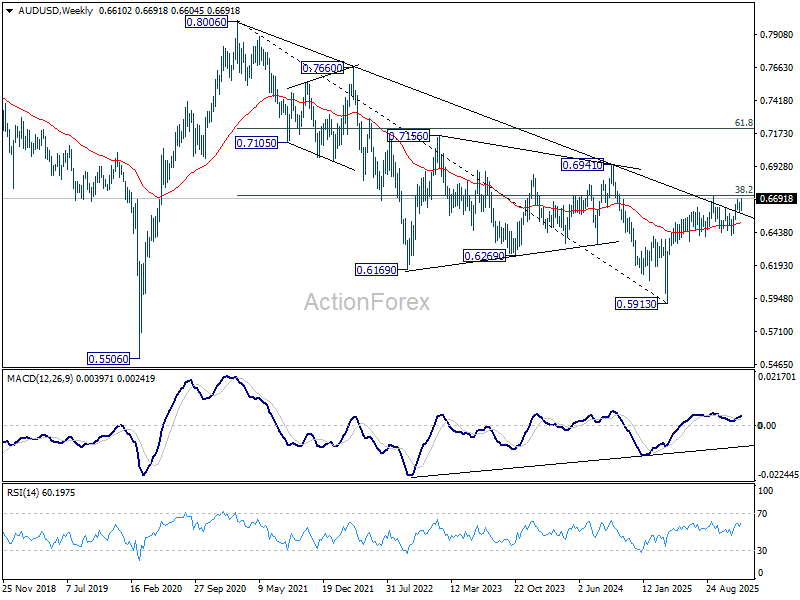

RBA minutes confirms 2026 hike risk, AUD/USD presses 0.67, eyes 0.72 next year

Australian Dollar surged broadly after minutes from the December policy meeting confirmed that the RBA had actively discussed the possibility of a rate hike in 2026. While officials stressed that such an outcome is far from assured, the acknowledgment alone was enough to reprice expectations and trigger a sharp AUD bid.

According to the minutes, board members debated whether a rise in the cash rate might need to be considered sometime next year following a recent pickup in inflation. Policymakers agreed that risks to inflation had tilted to the upside, but emphasized that it would take “a little longer” to judge whether price pressures would prove persistent rather than temporary.

The discussion also revealed internal disagreement over whether financial conditions remain sufficiently restrictive. Some members pointed to aggressive bank lending and ongoing strength in housing prices as signs that conditions may no longer be tight enough to restrain inflation effectively, adding weight to the upside risk narrative.

At the same time, the board agreed that labor market conditions remain somewhat tight, with the economy likely still operating in excess demand. Elevated capacity utilization was also flagged as evidence of ongoing supply constraints, reinforcing concern that inflation could prove more stubborn than previously assumed.

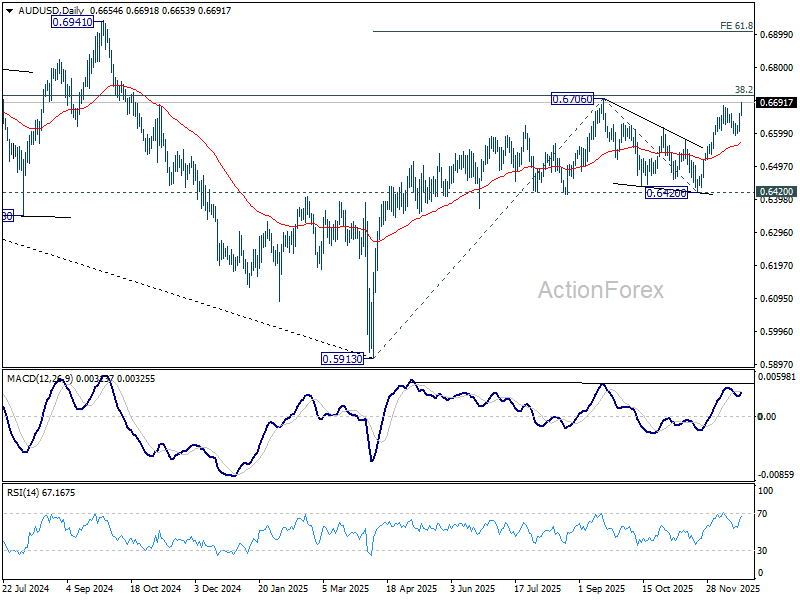

Markets reacted by pushing AUD higher across the board, with AUD/USD extending its rebound from 0.6420. Immediate focus has now shifted to a critical cluster resistance zone around 0.6706–0.6713, which includes 38.2% retracement of 0.8006 to 0.5913 at 0.6713.

Decisive break above this 0.6716/13 zone would mark a significant technical development. It would strengthen the case that AUD/USD is already reversing the entire downtrend from the 2021 high at 0.8006.

In that scenario, the next near-term target comes in at 61.8% projection of 0.5913 to 0.6706 from 0.6420 at 0.6910.

Beyond the near term, confirmation of a broader trend reversal would open scope for a move toward to 61.8% retracement of 0.8006 to 0.5913 at 0.7206 and above next year.

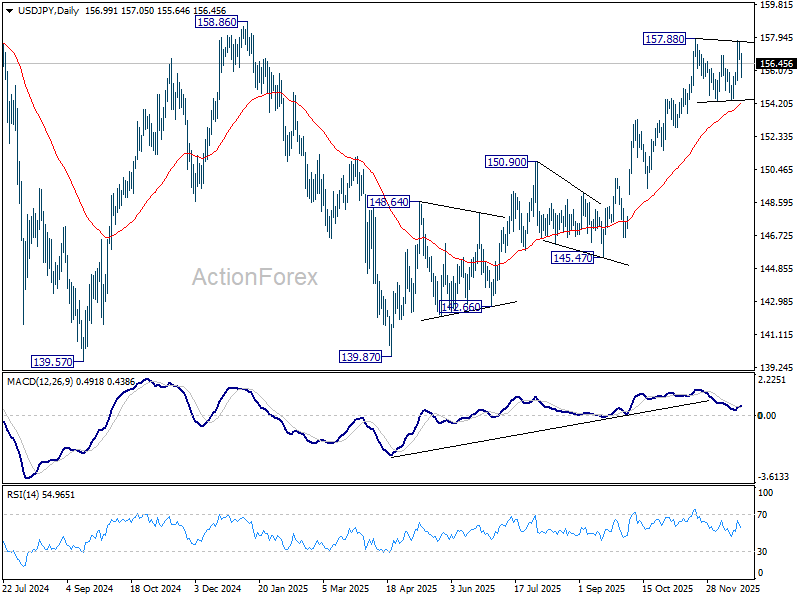

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.59; (P) 157.15; (R1) 157.59; More…

USD/JPY’s sharp decline today suggests rejection by 157.88 resistance, and intraday bias is turned neutral. Consolidations from 1.5788 is extending with another downleg. But further rally is expected as long as 154.33 support holds. Firm break of 158.85 key structural resistance will be an important medium term bullish sign. Next target will be 161.94 high. However, decisive break of 154.38 will turn bias to the downside for deeper correction.

In the bigger picture, corrective pattern from 161.94 (2024 high) could have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.