{kind=link}

Global markets are trading in mixed fashion, with risk appetite showing early signs of fatigue after a strong start to the year. US equity futures are sluggish, pointing to a flat open after both the DOW and S&P 500 closed at record highs yesterday. December ADP private payrolls from the US came in slightly weaker than expected, but the data generated little market reaction. That muted response reflects the broader interpretation that the labor market is cooling gradually rather than deteriorating sharply.

The combination of modest job growth and still-firm wage pressures fits neatly into the prevailing narrative. Hiring momentum has slowed, but companies are not shedding workers aggressively2. This “no hiring, no firing” pattern continues to dominate, with firms — particularly medium-sized businesses — still competing for talent. That dynamic helps explain why wage growth remains elevated despite softer headline job gains.

For policymakers, such conditions argue against any aggressive easing cycle. While the Fed may still deliver additional rate cuts later this year, the labor backdrop does little to justify a rapid or front-loaded move.

Still, Friday’s non-farm payrolls report remains the key event risk. Unlike ADP, NFP will provide a more comprehensive read on employment, wages, and participation, shaping expectations for the Fed’s next steps.

Elsewhere, precious metals are pulling back, with Gold and Silver retreating after touching record highs earlier in the week. The move appears to reflect profit-taking rather than a shift in fundamentals. The pullback extends the sideways consolidation that has been in place since late December. While geopolitics helped propel metals higher earlier in the week, momentum has faded for now.

In FX terms, Aussie remains the strongest performer for the week so far, followed by Kiwi, and then Yen. Loonie sits at the bottom, trailed by Swiss Franc and Euro. Dollar and Sterling are trading in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.61%. DAX is up 0.64%. CAC is up 0.01%. UK 10-year yield is down -0.077 at 4.410. Germany 10-year yield is down -0.046 at 2.799. Earlier in Asia, Nikkei fell -1.06%. Hong Kong HSI fell -0.94%. China Shanghai SSE rose 0.05%. Singapore Strait Times rose 0.16%. Japan 10-year JGB yield fell -0.009 to 2.121.

US ADP jobs rose 41k, wage pressures hold firm

US private-sector job recovered at the end of 2025, with ADP reporting a 41k rise in employment in December, but missed expectations of 50k. Hiring remained uneven, with goods-producing jobs slipping -3k, while service-providing roles rose 44k.

By company size, small businesses 9k jobs after November losses, while medium-sized firms added 34k. Large employers contributed just 2k. As ADP Chief Economist Nela Richardson noted, small establishments recovered into year-end even as large firms pulled back.

Wage dynamics remained firm. Pay growth for job-stayers was unchanged at 4.4% year-on-year, while job-changers saw an acceleration to 6.6% from 6.3%.

Eurozone inflation cools to 2.0% in December, services still main driver

Eurozone inflation edged lower in December, with flash data showing headline CPI slowing from 2.1% to 2.0% yoy, undershooting expectations of 2.1%. Core inflation also eased, with CPI excluding energy, food, alcohol and tobacco falling from 2.4% to 2.3%, below the 2.4% consensus forecast.

Services remained the dominant source of price pressure, posting an annual rate of 3.4%, down slightly from 3.5% in November. Food, alcohol and tobacco inflation ticked higher to 2.6%.

Non-energy industrial goods inflation eased further to 0.4%. Energy prices remained a strong disinflationary force, with prices falling -1.9% yoy after a smaller decline in November.

Japan PMI composite finalized at 51.1, but confidence and hiring hold up

Japan’s service sector lost some momentum at the end of 2025, with Services PMI finalized at 51.6 in December, down from 53.2 in November. Composite PMI eased to 51.1 from 52.0, marking a seven-month low.

According to S&P Global Market Intelligence Economics Associate Director Annabel Fiddes, services firms reported slower growth in activity and new orders, while manufacturing showed relative improvement. Despite softer demand signals, business confidence across Japan’s private sector remained firm, supporting a “solid and accelerated rise in employment”.

Cost pressures, however, remain a key challenge. Input prices rose at the fastest pace since April, driven by higher costs, prompting firms to lift selling prices at a solid rate. With demand conditions softening slightly, companies face a “difficult balance” between passing on higher costs to protect margins and maintaining competitiveness.

Australia CPI cools more than expected to 3.4%, easing near-term pressure on RBA

Australia’s inflation cooled more than expected in November, offering some relief after months of intensifying price pressure. Headline CPI slowed from 3.8% yoy to 3.4%, undershooting expectations of 3.6%. Trimmed mean inflation eased modestly from 3.3% yoy to 3.2%, pointing to a gradual moderation in underlying pressures.

The slowdown was broad-based. Annual goods inflation fell to 3.3% yoy from 3.8%, driven largely by a sharp deceleration in electricity prices, which rose 19.7% over the year compared with 37.1% previously. Services inflation also eased, slowing to 3.6% yoy from 3.9%, helped by a pullback in domestic holiday travel costs after October’s school-holiday and major sporting-event surge.

Despite the moderation, price pressures remain elevated in key areas. Housing inflation stayed firm at 5.2% yoy, while rents and medical services continued to rise at a solid pace. The data ease immediate pressure on the RBA for rate hike. But with inflation still well above target range, policymakers are likely to remain cautious about declaring victory too early.

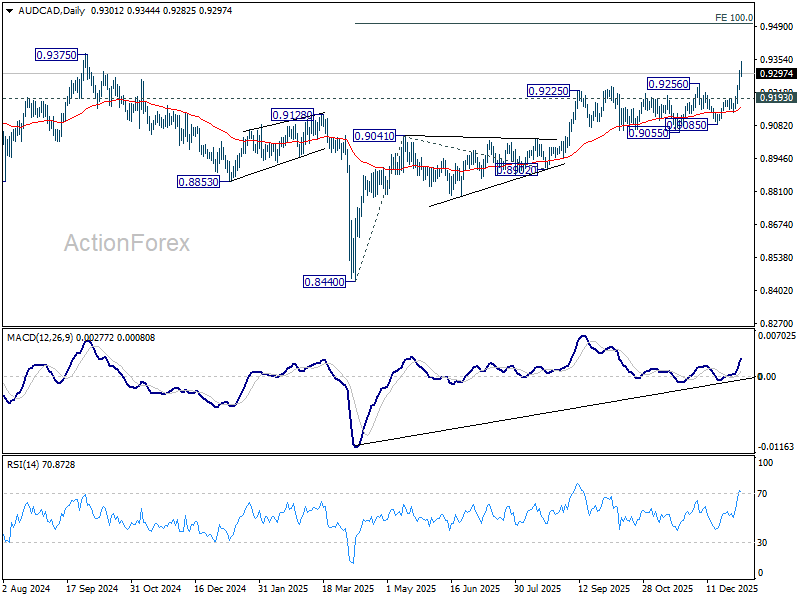

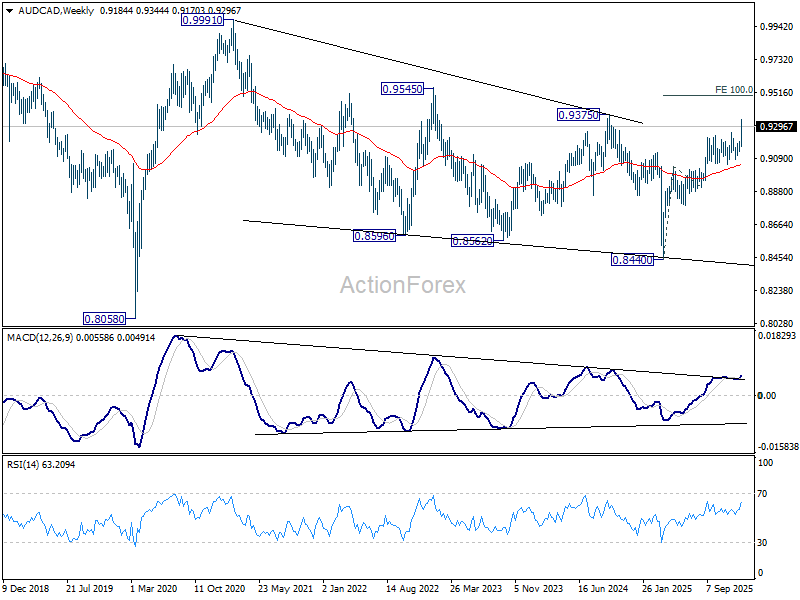

AUD/CAD Medium-Term Parity Case Builds on Metal Boom and RBA Outlook

Australian Dollar has taken a clear leadership role among commodity currencies as the new year starts, outperforming peers as powerful tailwinds from metals markets combine with resilient domestic rate expectations.

Iron ore prices surged to their highest level since February, driven by optimism over Chinese macro support and seasonal restocking ahead of the Lunar New Year. That confidence was underlined by fresh guidance from the PBoC which said it will deploy interest-rate cuts, reserve-requirement reductions and other tools in a flexible and efficient manner to maintain ample liquidity and support credit growth.

Policymakers also pledged to step up counter-cyclical and cross-cyclical adjustments, boost domestic demand and manage financial risks, signaling a determination to stabilize growth early in the new five-year planning cycle. For commodity exporters, the message has been unambiguously supportive.

Also, Copper has delivered an additional boost, pushing to a fresh series of record highs. The rally has been driven by supply-side disruptions and deepening concerns over medium-term availability rather than short-term speculative flows.

Production setbacks at several major mines, including Freeport‑McMoRan’s Grasberg operation, have tightened global supply. At the same time, demand expectations continue to rise due to Copper’s critical role in construction, energy transition, artificial intelligence data centers and defense industries.

Back home, November CPI data in Australia surprised to the downside, reducing pressure for an immediate February rate hike by the RBA. Even so, the broader policy outlook remains tilted toward tightening rather than easing.

Underlying inflation pressures are easing only slowly, particularly in services, keeping policymakers cautious. Markets still expect rates to remain on hold in February but see a high likelihood of a hike by June and another before the end of the year.

That policy-commodity mix has translated directly into Aussie strength. Technically, AUD/CAD has broken decisively above 0.9256 resistance, confirming resumption of the uptrend from 0.8440 (2025 low). Next upside target stands at 100% projection of 0.8440 to 0.9041 from 0.8902 at 0.9503.

More importantly, the upside breakout strengthens the case that the entire corrective decline from the 0.9991 (2021 high) ended at 0.8440. Medium-term focus now shifts to 0.9545, where decisive break would argue that the longer-term rise from the 2020 low at 0.8058 is ready to resume toward parity.

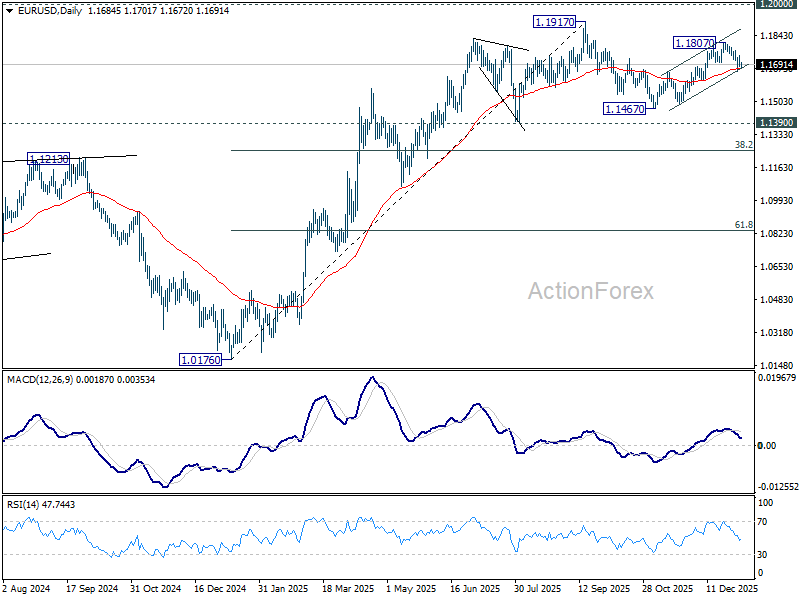

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1667; (P) 1.1705; (R1) 1.1726; More….

EUR/USD is still bounded in tight range above 1.1658 and intraday bias stays neutral. Rise from 1.1467 could still be in progress. Firm break of 1.1807 resistance will resume the rally to retest 1.1917 high. However, break of 1.1658 support will target 1.1467, as corrective pattern from 1.1917 has started the third leg.

In the bigger picture, as long as 55 W EMA (now at 1.1408) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.