{kind=link}

Yen once again took center stage, staging a broad-based rally that gathered pace through the Asian session. USD/JPY dived below 154, a sharp reversal from last week’s run toward 160 — a level widely perceived by markets as Japan’s informal line in the sand. The move gained traction as Japanese assets reacted in tandem. Nikkei opened sharply lower and finished the session down around -1.8%, reinforcing a classic domestic risk-aversion loop. Equity weakness in turn strengthened Yen further, lending durability to the rebound rather than leaving it vulnerable to quick retracement.

Momentum was reinforced by unusually direct political messaging over the weekend. Japanese Prime Minister Sanae Takaichi warned that authorities would take “all necessary measures” to counter speculative and highly abnormal market movements. While she did not specify whether she was referring to currency markets or bond yields, traders interpreted the comments as a clear signal that tolerance for renewed instability is limited.

As a result, caution has crept back into positioning. There is a growing sense that authorities could eventually step in if volatility resurfaces. Yet the irony is clear: as markets move in line with the government’s preference for a stronger Yen, the immediate risk of intervention diminishes rather than intensifies.

Politics remain an important undercurrent in Japan too. Takaichi is heading into a snap election in early February, seeking to solidify her mandate. Recent polling shows her approval has slipped modestly but remains elevated. A Nikkei survey released Monday showed support falling to 67% from 75% in December, while a Kyodo poll placed approval at 63%, down from 68%. A separate Mainichi survey painted a more cautious picture, showing approval dropping ten points to 57%. While still high by historical standards, the trend has attracted attention as the campaign approaches, particularly given the compressed political timetable.

The challenge for Takaichi lies in the gap between her personal popularity and that of her party. The LDP continues to poll near only 30% in several surveys, far below the prime minister’s own ratings. With the ruling coalition holding only a one-seat majority, the election is widely viewed as one of the most unpredictable in years.

Beyond Japan, Yen’s rally is unfolding against a backdrop of broad-based Dollar weakness. The greenback is under pressure across the board, with losses against Yen acting as a focal point but not the sole driver. Investors are increasingly uneasy about the direction of US policy and its implications for capital flows.

That unease goes beyond trade disputes. Markets are beginning to price the risk of capital friction alongside tariff conflict. When geopolitical tensions escalate, even allies become less inclined to hold each other’s debt, preferring hard currencies and perceived safe havens instead — a dynamic that has repeated itself throughout history.

This broader tone is clearly reflected in FX performance. Yen is currently the strongest major currency, followed closely by Swiss Franc, highlighting defensive positioning. Dollar sits at the bottom of the performance table, trailed by Loonie and Sterling, while Euro, Aussie and Kiwi occupy the middle ground.

In Asia, Nikkei fell -1.79%. Hong Kong HSI fell -0.00%. China Shanghai SSE fell -0.09%. Singapore Strait Times is down -0.60%. Japan 10-year JGB yield fell -0.027 to 2.237.

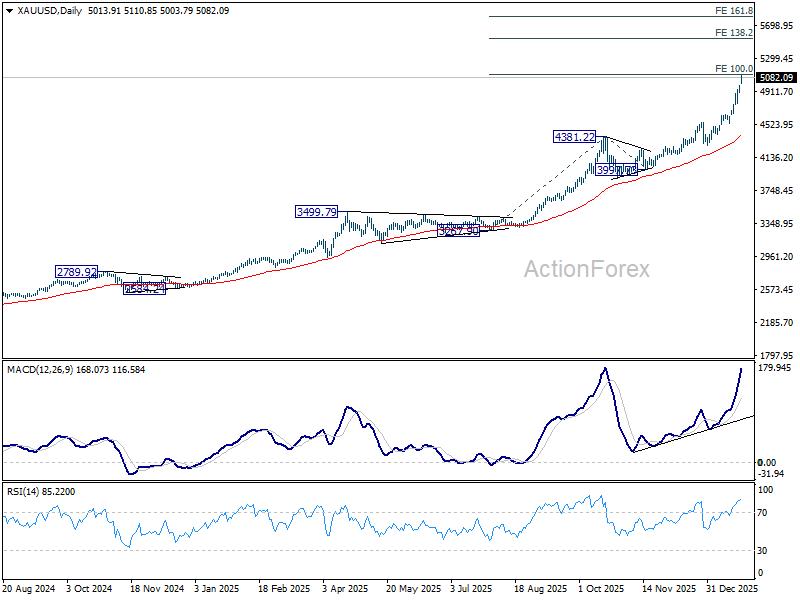

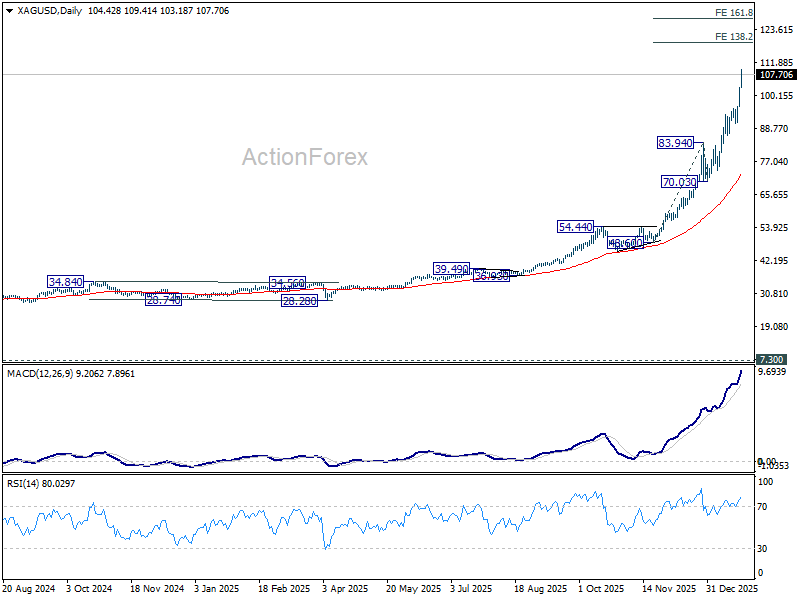

Metals mania continues as gold eyes 5,500, silver targets 118

Safe-haven flows have poured into precious metals again as global risk sentiment deteriorated at the start of the week, driving Gold to a fresh all-time high above 5,100 an ounce and sending Silver decisively through the 100 mark. The move reflects widespread investor anxiety amid escalating geopolitical and trade tensions, including renewed tariff threats and broad policy uncertainty that have weakened confidence in traditional risk assets and more importantly, Dollar.

The latest trigger has been a sharp escalation in tensions between the US and Canada. US President Donald Trump warned over the weekend that Canada could face 100% tariffs on its exports if Ottawa proceeds with trade agreement that he believes would allow China to flood the US market. Treasury Secretary Scott Bessent amplified the message on Sunday, warning that the US could not allow Canada to function as a backdoor for Chinese goods. The hardline comments land against a broader backdrop of tariff disputes and market skepticism about predictable policy direction.

Although Canada’s leadership quickly sought to dial down tensions, markets remained unsettled. Prime Minister Mark Carney sought to ease immediate fears, emphasizing its commitment to existing obligations under the United States–Mexico–Canada Agreement and clarifying that recent tariff reductions with China do not constitute a comprehensive free trade pact. Despite the diplomatic pushback, markets remain sensitive to even the threat of wider trade escalation, amplifying safe-haven bid dynamics.

In the background, underlying both rallies in Gold and Silver is a broader deterioration in risk appetite, with concerns spanning not just North American trade friction but also lingering uncertainty over NATO relations, Greenland disputes, and Middle East flashpoints. Markets are pricing this backdrop as a structural premium for haven assets rather than transient headline shocks.

Technically, Gold has already met 100% projection of 3267.90 to 4,381.22 from 3,997.73 at 5,111.05 and momentum still looks strong in both 4H and D MACD. There is no sign of topping yet. Sustained trading above 5,111.05 will pave the way to 138.2% projection at 5,536.33 next. On the downside, break of 4,899.23 support will indicate short term topping, and bring consolidations first.

Silver’s parabolic rise continues today without any hesitation above 100 psychological level. Near term outlook will stay bullish as long as 99.34 support holds. Next target is 138.2% projection of 48.60 to 83.94 from 70.03 at 118.86. On the downside, break of 99.34 will indicate short term topping and bring consolidations first.

Fed and BoC hold expected, while Australia CPI raises stakes

The week ahead places central banks back at the center of market attention, with the Fed and BoC emerging as the dual policy risks. Both are widely expected to keep interest rates unchanged, but neither meeting is likely to be treated as routine, given heightened political and trade uncertainty shaping global macro expectations.

The Fed is expected to hold rates steady at 3.50–3.75% at Wednesday’s decision, an outcome that is firmly priced in. Fed funds futures imply roughly 96% probability of no change. Economists show unanimity: all 100 respondents in the latest Reuters poll forecast a hold. Beyond the meeting itself, markets are aligned around a prolonged pause. Futures pricing assigns only about a 15% chance of a March rate cut, while 58% of economists surveyed expect policy to remain unchanged throughout the first quarter. The Fed, for now, appears set to sit tight as it assesses incoming data.

Nevertheless, that confidence fades further out the curve. By the end of June, futures price roughly a 60% chance of one rate cut, reflecting a more divided outlook on growth and inflation as the year progresses. Economic developments remain a wild card, particularly given the erratic policy environment from Washington since the start of the year. Shifting trade threats and diplomatic tension complicate forecasts for both activity and inflation.

Leadership in Fed uncertainty adds to the mix. The question of who replaces Jerome Powell as Fed chair has real policy implications, with successors like Kevin Warsh and Kevin Hassett offering contrasting approaches. A more dovish tilt under Hassett would mark a meaningful shift in tone.

For now, the base case remains intact: at least one rate cut later this year, but with timing highly conditional. Markets are increasingly wary of extrapolating too far ahead in an environment where political risk can override macro signals.

In Canada, the policy outlook appears a little bit more settled. The BoC is expected to hold rates at 2.25%, as its easing cycle has effectively run its course. In a recent Reuters poll, all 35 economists surveyed expected a hold this month, while nearly three-quarters forecast rates to remain unchanged through 2026, highlighting confidence in a prolonged pause.

That said, trade risks loom large. As long as Canada maintains preferential access to US markets—either through agreements or prolonged negotiations—the BoC can afford patience. But the balance of risks still leans dovish. Should tariffs expand to a broader range of industries, growth would likely weaken, forcing the BoC into additional rate cuts despite its current inclination to stay on hold.

Also, markets are approaching Australia’s CPI release with heightened sensitivity, as the data now sits at the center of the debate over whether the RBA can afford continued restraint. The past two months have seen a dramatic turnaround in expectations, with rate-cut assumptions replaced by a credible risk that policy may need to tighten further, and sooner.

The latest catalyst came from December’s strong employment report, which reinforced concerns that domestic demand and wage pressures remain inconsistent with a smooth return of inflation to target. While the RBA’s base case remains one of patience, officials have made clear they are unwilling to tolerate a renewed inflation drift, particularly if it threatens to entrench expectations.

The focus this time will particularly be on trimmed mean CPI, where any upside surprise would be especially problematic for policymakers. A further move away from the top of the target band would significantly raise the odds of pre-emptive tightening, forcing the RBA to act earlier than intended to preserve credibility.

Also, markets will closely watch US consumer confidence, Germany’s Ifo survey, Eurozone GDP, and Canada’s GDP.

Here are some highlights for the week:

- Monday: Germany Ifo business climate; US durable goods orders.

- Tuesday: Japan corporate services prices; Australia NAB business confidence; US house price index, consumer confidence.

- Wednesday: Japan BoJ minutes; Australia CPI; Germany Gfk consumer sentiment; BoC rate decision; Fed rate decision.

- Thursday: New Zealand trade balance, ANZ business confidence; Canada trade balance; US jobless claims, trade balance, factory orders.

- Friday: Japan Tokyo CPI, retail sales, industrial production, unemployment rate; Australia PPI; Germany CPI flash, unemployment, GDP; Swiss KOF economic barometer; Eurozone GDP, unemployment rate; Canada GDP; US PPI, Chicago PMI.

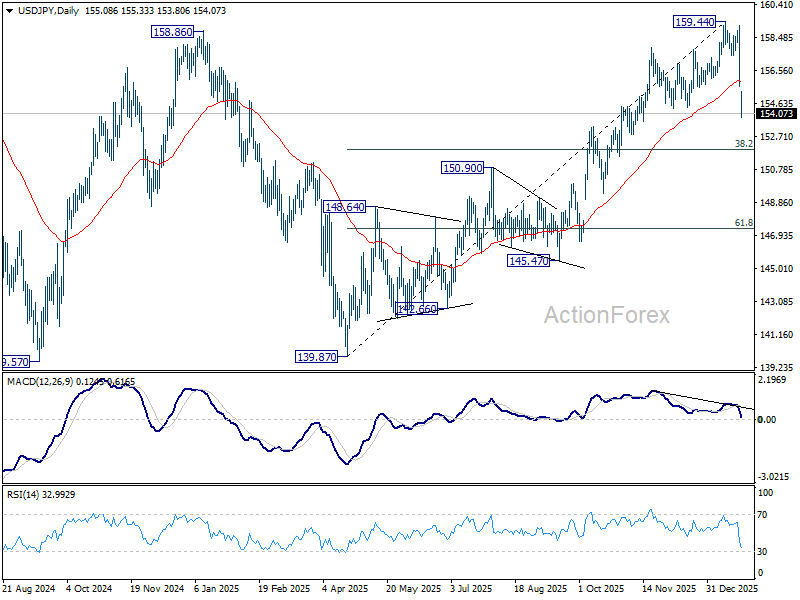

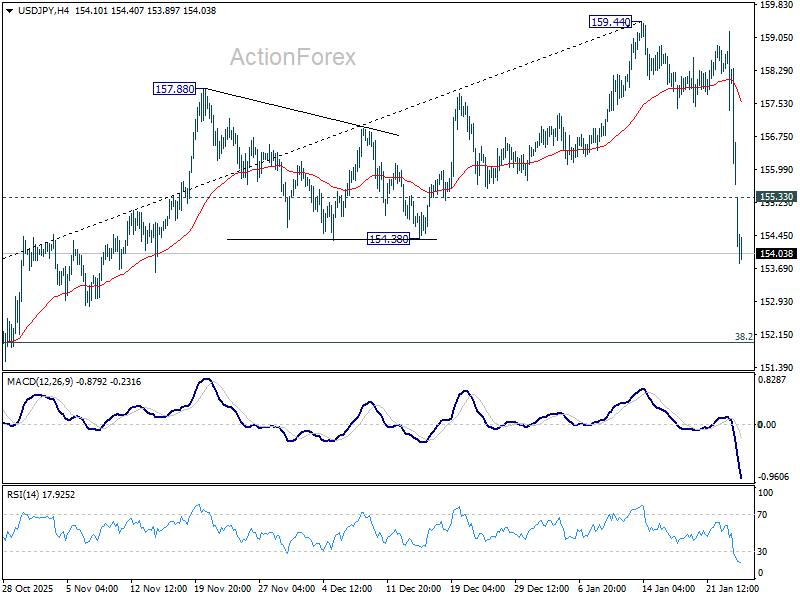

USD/JPY Daily Outlook

Daily Pivots: (S1) 154.48; (P) 156.86; (R1) 158.09; More…

USD/JPY gaps lower today and fall from 159.44 accelerates. Intraday bias stays on the downside for 38.2% retracement of 139.87 to 159.44 at 151.96. Strong support should be seen there to bring rebound, at least on first attempt. On the upside above 155.33 minor resistance will turn intraday bias neutral and bring consolidations first. However, decisive break of 151.96 will argue that fall from 159.44 is not a correction, be reversing whole rise from 139.87. Deeper decline would then be seen to 61.8% retracement at 147.34.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.35) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.