{kind=link}

Dollar found modest support in early US trading, managing a mild recovery as markets position cautiously ahead of the Federal Reserve’s rate decision. The move looked more like a pause in selling than a decisive shift in sentiment, with traders reluctant to press positions before policy clarity.

Some stabilization came after comments from US Treasury Secretary Scott Bessent, who reiterated that the US maintains a “strong Dollar policy.” The remarks helped temper immediate nervousness, but failed to materially change the broader tone. That is largely because Bessent’s message stands in clear contrast to President Donald Trump’s comments a day earlier. Trump said Dollar was “doing great” despite sliding more than 10% over the past year, effectively signaling comfort with continued weakness.

As a result, markets have interpreted Bessent’s remarks as an attempt to smooth volatility rather than to reverse the White House’s permissive stance. The comments were seen as damage control, not a policy pivot. Technically, Bessent’s assertion is not entirely inaccurate. With the Dollar Index still hovering around 96, the currency remains well above its cycle lows near 70 seen during the 2008 financial crisis.

But that historical context has done little to inspire fresh Dollar demand. Traders appear fully adept at filtering political rhetoric. Rather than betting on verbal assurances, markets are focused on policy actions and institutional signals, leaving Bessent’s comments with limited traction.

Attention now turns to the Fed. Rates are widely expected to be held at 3.50–3.75%, making the decision itself largely a non-event. The real focus will be on the statement language and Jerome Powell’s press conference. The base case remains an easing bias framed within a wait-and-see stance. The Fed’s latest dot plot points to one rate cut this year, making a cautious tilt toward easing a logical extension of current guidance.

Still, a more non-committal tone cannot be ruled out. Solid pockets of economic data, still-elevated inflation, and renewed trade threats involving Europe and Canada give policymakers reason to retain flexibility rather than pre-commit.

That nuance matters politically. Even a straightforward hold is likely to draw renewed criticism from Trump. Any shift toward a more neutral or less dovish bias would almost certainly provoke sharper attacks, further testing perceptions of Fed independence. Against that backdrop, outcomes and market reactions remain highly fluid.

In FX performance terms, the picture remains unfavorable for Dollar. For the week so far, it is the worst-performing major, followed by Sterling and Euro. Yen leads, followed by Aussie and Kiwi. Loonie sits mid-pack after the BoC held rates and maintained a neutral stance. Swiss Franc has drifted back toward the middle as risk sentiment modestly improves.

BoC holds at 2.25%, US trade risk as key source of vulnerability

The BoC left its policy rate unchanged at 2.25%, in line with expectations, and reiterated a neutral bias. The Governing Council said the current setting “remains appropriate,” conditional on the economy evolving broadly in line with its outlook.

The Bank judged that the outlook for both the global and Canadian economies is little changed from the October MPR. However, it cautioned that the balance of risks remains tilted by external factors, particularly “unpredictable US trade policies and geopolitical risks.”

Near-term growth is expected to remain “modest”. Growth forecasts were left broadly unchanged, with GDP expected to expand 1.1% in 2026 and 1.5% in 2027. A major source of uncertainty remains the upcoming review of the Canada-US-Mexico Agreement, which could materially affect trade flows and investment decisions. On inflation, the BoC expects price growth to stay close to its 2% target over the projection horizon.

Australia CPI surges to 3.6% in Q4, 3.8% in December

Australia’s Q4 CPI showed little relief for RBA where it matters most for policy. Headline inflation rose 0.6% qoq, slightly below expectations of 0.7% and slowing sharply from the prior quarter’s 1.3% gain. However, on an annual basis, CPI accelerated from 3.2% yoy to 3.6% yoy, matching forecasts and keeping inflation well above the RBA’s target band.

The more important signal came from underlying inflation. Trimmed mean CPI rose 0.9% qoq, easing marginally from 1.0% previously but beating expectations of 0.8%. Annual trimmed mean inflation climbed from 3.0% yoy to 3.4% yoy, above the expected 3.2%, reinforcing concerns that price pressures remain persistent.

December’s monthly details added to that unease. Headline CPI jumped 1.0% mom, lifting the annual rate from 3.5% yoy to 3.8%, both above expectations. Trimmed mean CPI rose a more modest 0.2% mom, but annual core inflation still edged up from 3.2% yoy to 3.3% yoy.

Price pressures remain broad in December. Goods inflation accelerated from 3.2% yoy to 3.4%, driven largely by a 21.5% surge in electricity prices. Services inflation climbed from 3.6% yoy to 4.1%, led by domestic travel and accommodation and rising rents.

Markets are now firming up their expectation that RBA will return to rate hike in February.

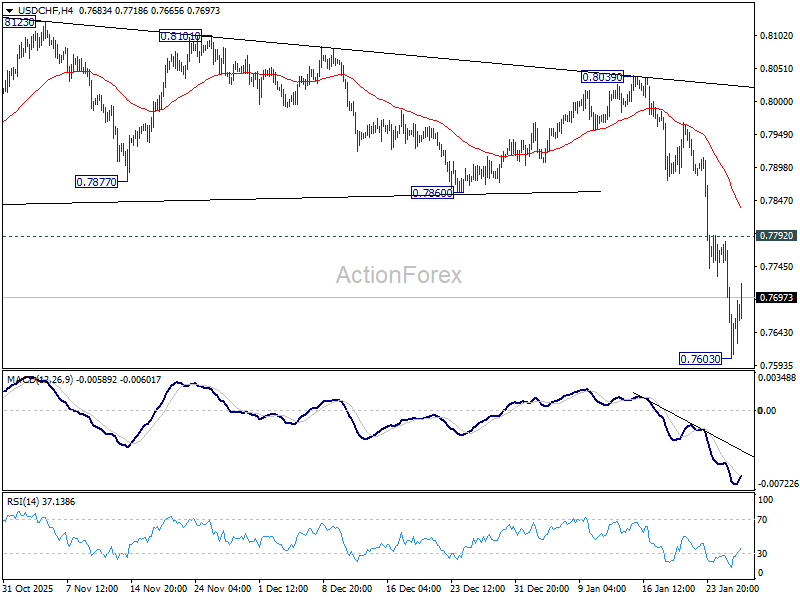

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7550; (P) 0.7667; (R1) 0.7730; More….

A temporary low is formed at 0.7603 in USD/CHF with current recovery and intraday bias is turned neutral first. Outlook will stay bearish as long as 0.7792 resistance holds Break of 0.7603 will resume the larger down trend to 0.7382 projection level next. However, firm break of 0.7792 will turn bias back to the upside, for stronger rebound to 0.7860 support turned resistance.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress and resuming. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8184) holds.