{kind=link}

Dollar extended its rebound today, though upside momentum remains restrained. Price action suggests markets are still digesting recent shifts in policy expectations rather than embracing a full risk-off move. Attention remains on the implications of Kevin Warsh being lined up as the next chair of the Fed. While Fed rate cut probabilities have barely shifted, repricing has been far more visible in higher-beta assets, notably precious metals and cryptocurrencies.

Equities have so far been more resilient, but the tone is softening. US stock futures are slightly heavier, with NASDAQ underperforming. The move has been exacerbated by weakness in Nvidia, whose shares slipped in premarket trading after reports cast doubt on a proposed USD 100 billion investment linked to OpenAI. Nvidia’s drag on tech sentiment has added to concerns that risk repricing could broaden. If equity weakness starts to align more closely with the sharp selloff already seen in crypto over the past two sessions, markets may begin to reassess overall risk appetite more forcefully.

For now, it remains unclear how tightly the recent cryptocurrency slump will correlate with tech stocks and broader sentiment. The disconnect suggests investors are selectively reducing exposure rather than exiting risk wholesale.

Looking ahead, the RBA rate decision is the next major focal point. A 25bp hike to 3.85% is well priced and unlikely to surprise. The real question lies in forward guidance. Markets are pricing roughly 55bp of tightening by year-end, implying at least one additional hike. Whether the RBA signals a return to a tightening cycle or frames the move as a one-off adjustment will be critical.

AUD/USD has already shown signs of hesitation after breaching the 0.7000 mark last week. The next directional move will hinge on both global risk sentiment and how convincingly the RBA leans toward further tightening.

For now, Dollar leads performance on the day, followed by Sterling and Euro. Swiss franc lags, trailed by Loonie and Kiwi. Aussie and Yen are trading near the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.63%. DAX is up 0.74%. CAC is up 0.60%. UK 10-year yield is down -0.024 at 4.506. Germany 10-year yield is up 0.011 at 2.858. Earlier in Asia, Nikkei fell -1.25%. Hong Kong HSI fell -2.23%. China Shanghai SSE fell -2.48%. Singapore Strait Times fell -0.26%. Japan 10-year JGB yield fell -0.013 to 2.238.

UK PMI manufacturing finalized at 17-month high, inflation risks return

UK PMI Manufacturing was finalized at 51.8 in January, up from December’s 50.6 and marking a 17-month high. The reading signals a solid start to 2026 for the sector, showing resilience despite a challenging backdrop of geopolitical tension and trade uncertainty.

According to Rob Dobson of S&P Global Market Intelligence, growth momentum improved notably. Output and order books expanded at a faster pace, while new export business rose for the first time in four years, led by demand from Europe, China, and the US. Business confidence also rebounded, reaching its highest level since before the 2024 Autumn Budget, as firms focused on opportunities ahead rather than near-term policy and geopolitical risks.

The labor market picture showed tentative stabilization. Although hiring remained weak, the pace of job cuts slowed to its mildest in 15 months. That said, inflation pressures are resurfacing, with higher Minimum Wage and employer National Insurance costs feeding through supply chains alongside rising metals prices, posing a potential constraint on margins in coming months.

Eurozone PMI manufacturing finalized at 49.5, recovery momentum at snail’s pace

Eurozone PMI Manufacturing was finalized at 49.5 in January, up from December’s 48.8. According to Cyrus de la Rubia of Hamburg Commercial Bank, progress remains at a “snail’s pace”. Order intakes continued to fall, albeit at a less severe pace than late last year, while sentiment twelve months ahead improved slightly, suggesting firms are cautiously more optimistic about future production.

The regional picture remains highly uneven. Greece led with a PMI of 54.2, a five-month high, while France surprised on the upside at 51.2 (a 43-month high). Germany showed tentative stabilization, with contraction easing to a three-month high of 49.1. In contrast, Italy (48.1)remained firmly in contraction, Austria (47.2) deteriorated sharply, and Spain (49.2) slipped into its second consecutive month of decline after previously outperforming peers.

Cost pressures also re-emerged as a key theme. Input price inflation rose noticeably, driven in part by a sharp increase in natural gas prices and firmer oil costs. At the same time, higher prices for industrial metals may reflect strengthening global demand rather than pure supply stress.

Japan PMI manufacturing finalized at 51.5, growth returns, inflation a risk

Japan’s manufacturing sector returned to expansion in January, with PMI Manufacturing finalized at 51.5. This marks the first improvement in operating conditions since mid-2025 and represents the strongest rate of growth since August 2022, offering early evidence of a cyclical recovery taking hold.

The details were encouraging. S&P Global Market Intelligence noted that output and new orders recorded their sharpest increases in almost four years, while export demand rose for the first time since 2022. Employment growth also accelerated to its fastest pace since September 2022, suggesting the sector is “gearing up for further increases in output in the months ahead.”

That said, cost pressures are resurfacing as a potential constraint. Input price inflation climbed to a near one-year high, driven in part by the weaker yen, and firms passed some of those costs on to customers. Whether these price pressures intensify will be key in assessing how durable the recovery proves to be.

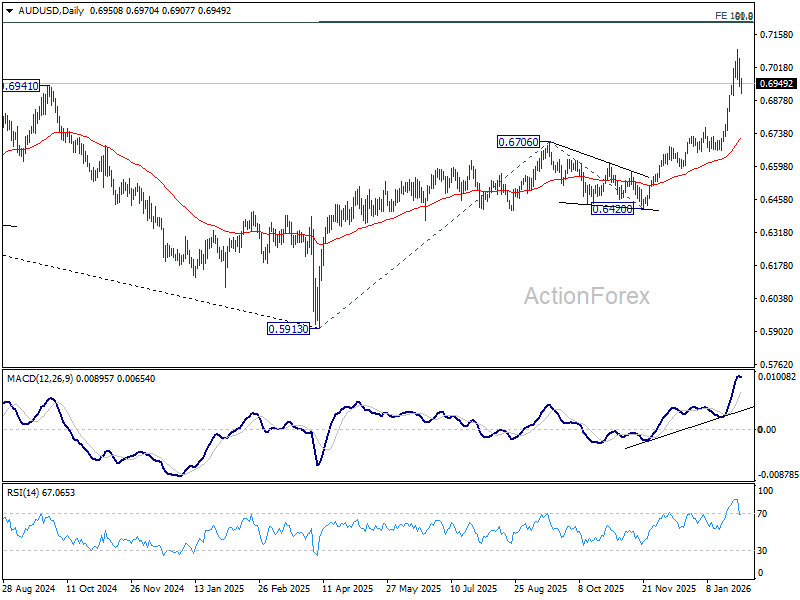

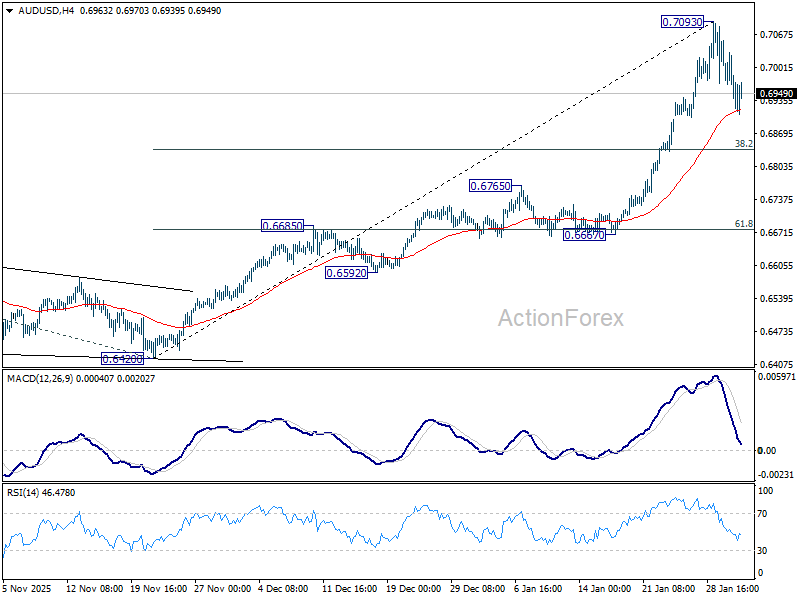

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6917; (P) 0.6986; (R1) 0.7033; More...

Intraday bias in AUD/USD remains neutral as consolidations continue. Risk will stay on the upside as long as 55 4H EMA (now at 0.6916) holds. Above 0.7093 will extend larger up trend to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213 next. Nevertheless, sustained break of 55 4H EMA will confirm short term topping, and bring lengthier consolidations before rally resumption. Deeper pullback would then be seen to 38.2% retracement of 0.6420 to 0.7093 at 0.6836.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.