Dollar pares back some gains in Asian session today after yesterday’s yield driven rally. 10 year yield hit as high as 2.990 during regular trading hour before closing at 2.973, up 0.022. However, that was below open at 2.975 and thus, showed a bit of hesitation ahead of 3% handle. US stocks closed mixed, with DOW down -0.06%, S&P 500 up 0.01% and NASDAQ down -0.25%. Weaker Yen helped lifted Nikkei as it’s trading up 0.76% at the time of writing. China SSE is also recovery and is up 2% while Hong Kong HSI is up 1%.

In the currency markets, New Zealand Dollar is so far the weakest one for the week as selloff extends today. Yen is not much better as it’s closely following as the second weakest. On the other hand, Swiss Franc is the second strongest one, as helped by EUR/CHF’s rejection from 1.2 handle. But the Franc is losing momentum in Asian session as it turned mixed. We might see EUR/CHF revisit 1.2 again pretty soon.

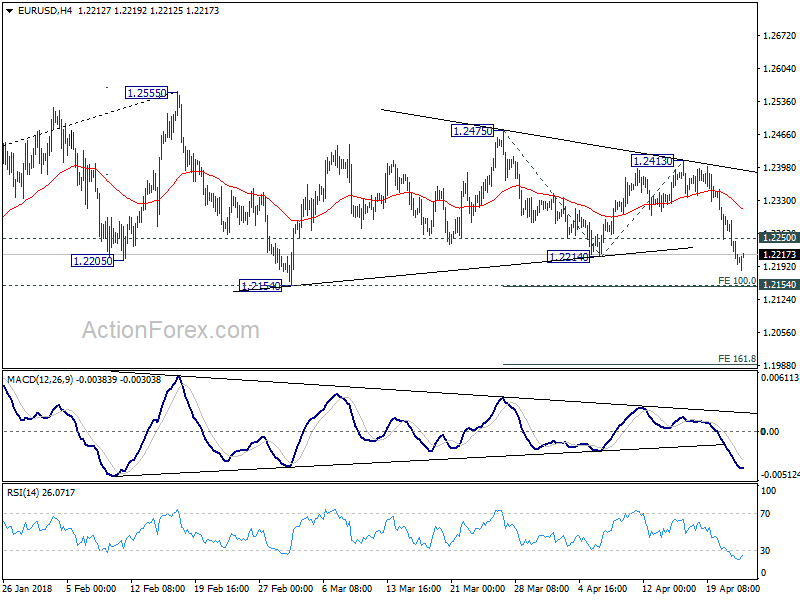

Technically, EUR/USD’s break of 1.2214 support now revived the case of medium term trend reversal. That also helped lifted Dollar index to 91, with medium term trend line resistance taken out. The firm break of 108 resistance in USD/JPY and 1.2814 in USD/CAD also aligned Dollar’s near term bullish outlook with others. Yen would be a focus today as USD/JPY’s yield drive rally might take other Yen crosses higher. In particular, EUR/JPY is having last week’s high of 133.08 in sight.

Aussie spiked lower CPI, but quickly recovered

Australia CPI was unchanged at 1.9% yoy in Q1, below expectation of 2.0%. RBA trimmed mean CPI rose to 1.9% yoy, up from 1.8% yoy and beat expectation of 1.8% yoy. RBA weighted median CPI was unchanged at 2.0% yoy, beat expectation of 1.9% yoy. The Australian Bureau of Statistics noted in the release that “while the annual CPI rose 1.9 per cent, most East Coast cities have continued to experience annual inflation above 2.0 per cent, due in part to the strength in prices related to Housing and Food. Softer economic conditions in Darwin and Perth have resulted in annual inflation remaining subdued at 1.1 and 0.9 per cent respectively.”

AUD/USD spiked lower to 0.7576 after the release but quickly recovered. Firstly, the decline is a bit stretched after AUD/USD fell for three days. Secondly, the CPI data just affirmed the case that RBA is in no rush to raise interest rate.

German Ifo expected to drop in April

German Ifo business climate will be a major focus for today. The headline Business climate index is expected to drop from 103.2 to 102.8 in April. Expectation index is expected to drop from 100.1 to 99.5 while current assessment index is expected to drop to from 106.5 to 106.0. Eurozone PMIs released yesterday were indeed quite solid. While they still indicate slight slowdown from stellar growth in Q4, the dip might not be as deep as some expected. And Eurozone could quickly regain momentum again in Q2. But after all, we’re not expecting the data to chance ECB’s cautious stance. More on ECB in ECB Preview: Caution over Recent Slowdown Won’t Affect QE Schedule

Elsewhere

Swiss trade balance and UK public sector net borrowing will be featured in European session. US will release house price indices, new home sales and consumer confidence later in the day.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2173; (P) 1.2231 (R1) 1.2265; More….

EUR/USD drops to as low as 1.2184 so far and the break of 1.2214 support revived the case of medium term reversal. Intraday bias remains on the downside for 1.2514 support first. Decisive break there will confirm the bearish case and target 161.8% projection of 1.2475 to 1.2214 from 1.2413 at 1.1991. On the upside, 1.2250 minor resistance will turn bias neutral first. But risk will now stay on the downside as long as 1.2413 resistance holds.

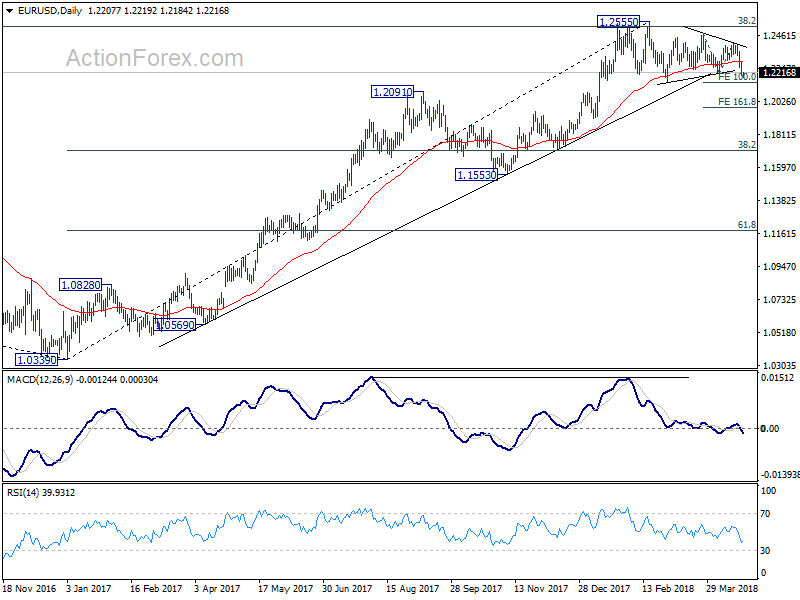

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Firm break of 1.2154 support will confirm rejection by this fibonacci level. And in that case, a medium term top is at least formed at 1.2555. EUR/USD should then head back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. We’ll look at the structure and momentum of such decline before decision if it’s an impulsive or corrective move.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Y/Y Mar | 0.50% | 0.50% | 0.60% | 0.70% |

| 1:30 | AUD | CPI Q/Q Q1 | 0.40% | 0.50% | 0.60% | |

| 1:30 | AUD | CPI Y/Y Q1 | 1.90% | 2.00% | 1.90% | |

| 1:30 | AUD | CPI RBA Trimmed Mean Q/Q Q1 | 0.50% | 0.50% | 0.40% | |

| 1:30 | AUD | CPI RBA Trimmed Mean Y/Y Q1 | 1.90% | 1.80% | 1.80% | |

| 1:30 | AUD | CPI RBA Weighted Median Q/Q Q1 | 0.50% | 0.50% | 0.40% | 0.50% |

| 1:30 | AUD | CPI RBA Weighted Median Y/Y Q1 | 2.00% | 1.90% | 2.00% | |

| 6:00 | CHF | Trade Balance (CHF) Mar | 3.23B | 3.14B | ||

| 8:00 | EUR | German IFO Business Climate Apr | 102.8 | 103.2 | ||

| 8:00 | EUR | German IFO Expectations Apr | 99.5 | 100.1 | ||

| 8:00 | EUR | German IFO Current Assessment Apr | 106 | 106.5 | ||

| 8:30 | GBP | Public Sector Net Borrowing (GBP) Mar | 1.1B | -0.3B | ||

| 10:00 | GBP | CBI Trends Total Orders Apr | 4 | 4 | ||

| 13:00 | USD | House Price Index M/M Feb | 0.60% | 0.80% | ||

| 13:00 | USD | S&P/Case-Shiller Composite-20 Y/Y Feb | 6.30% | 6.40% | ||

| 14:00 | USD | New Home Sales Mar | 625K | 618K | ||

| 14:00 | USD | Consumer Confidence Index Apr | 126 | 127.7 |

{kind=link}