Reactions to US withdrawal from the Iran nuclear deal were centered in oil and yield. Stocks had a rather quiet day yesterday with DOW ended up 0.01%, S&P 500 down -0.03% and NASDAQ up 0.02%. At the time of writing, Nikkei is down -0.35%. Meanwhile, after a volatile ride, WTI crude oil is back above 70 hand, trading at 70.6, and it could probably have a take on this week’s high at 70.84 later today. Rebound in oil price also lifted 10 year yield which is back at 2.99, comparing to last week’s low at 2.91. Gold continues to gyrate in tight range around 1310.

In the currency markets, strength in oil also helps lift Canadian Dollar broadly higher today. And yield support Dollar as the second strongest for today and pushed yes lower as the weakest one. Though, for the week, Sterling remains the strongest one, as it’s in recovery mode ahead of BoE rate decision. Dollar is actually the real deal as it’s trading above last week’s high against all but Yen and Sterling. Canadian Dollar, despite today’s recovery, is the third weakest, after Aussie and Euro.

Technically, EUR/CHF’s break of 1.1888 minor support yesterday finally confirmed the rejection by 1.2 handle. The pull back will likely extend lower today for 1.18 handle. The point to watch is whether such pull back in EUR/CHF will lift the Swiss Franc elsewhere, or it would pressure Euro against others.

UK, Germany and France urged US not to obstructs Iran deal implementation after withdrawal

US President Donald Trump announced to withdraw from the Iran nuclear deal overnight and blamed that as a “horrible one-sided deal that should have never, ever been made.” And, he would reimpose the US economic sanctions on Iran. UK, Germany and France issued a joint statement in response to the decision. The three countries pledged their “continuing commitment” to the JCPoA Iran deal. And they urged the US to “avoid taking action which obstructs its full implementation by all other parties to the deal”.

Japan, South Korea and China in first trilateral talk since 2015

Japanese Prime Minister Shinzo Abe, South Korean President Moon Jae-in and Chinese Premier Li Keqiang are meeting in Tokyo today for the first trilateral summit since 2015. As the host of the meeting, Abe said that “for our three nations, building future-oriented cooperative relations is extremely important for the region as a whole.” And he urged the three nations to “stay in close touch with international society and demand that North Korea take concrete moves” on denuclearization.

China’s Li expressed the willingness to “work with Japan and South Korea to jointly maintain regional stability and push forward the development of the three countries.” Separately, China is set to sign a currency swap agreement with Japan, and grant the country a quota of Renminbi Qualified Foreign Institutional Investors (RQFII) for investments.

On the data front

UK BRC retail sales monitor dropped -4.2% yoy in April. Japan labor cash earnings rose 2.1% yoy in March. Main focus will be on PPI inflation data from the US later today.

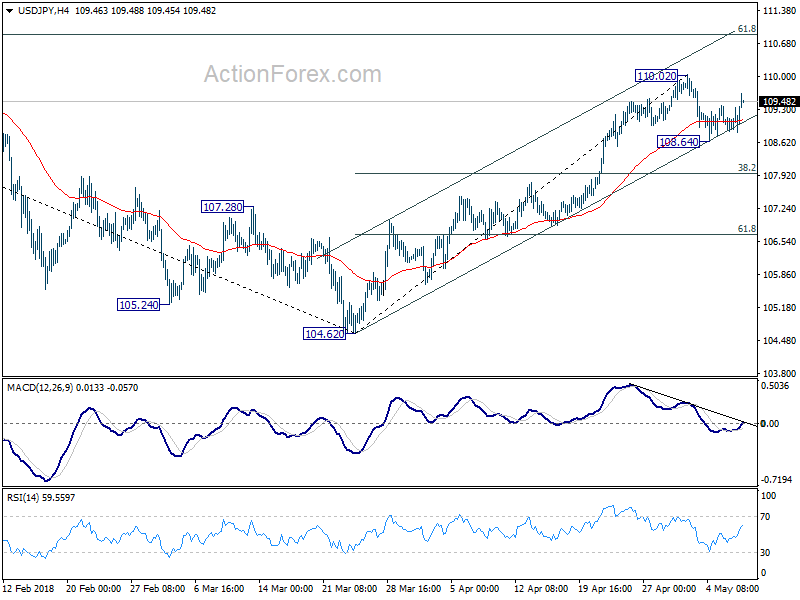

USD/JPY Daily Outlook

Daily Pivots: (S1) 108.85; (P) 109.10; (R1) 109.38; More…

USD/JPY recovers to as high as 109.63 so far as it’s continuing to draw support from near term channel. Nonetheless, upside is limited below 110.02 short term top so far. Thus, intraday bias remains neutral and more consolidation would be seen. On the downside, below 108.64 will bring deeper pull back. But downside should be contained by 38.2% retracement of 104.62 to 110.02 at 107.95 to bring rebound. On the upside, break of 110.02 will resume the rise from 104.62 to 61.8% retracement of 114.73 to 104.62 at 110.86 next.

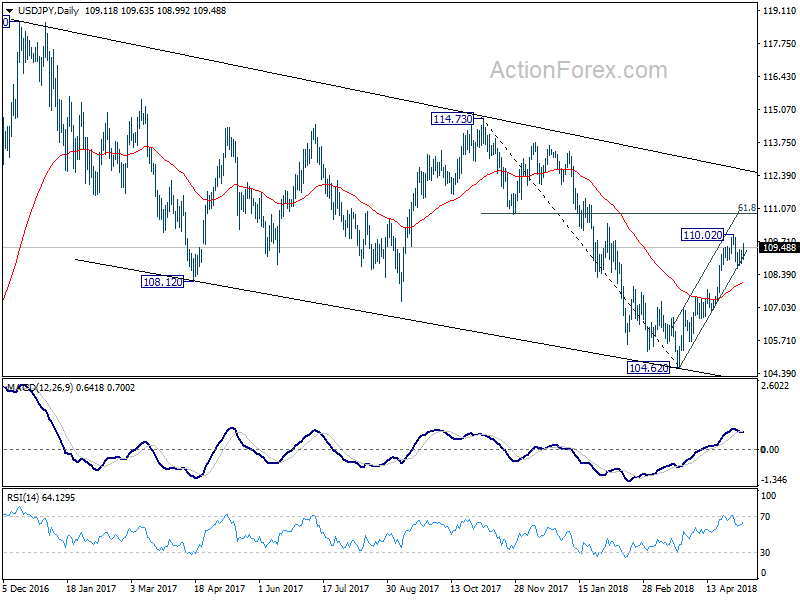

In the bigger picture, corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Rise from 104.62 is possibly resuming the up trend from 98.97 (2016 low). This will be the preferred case as long as 55 day EMA (now at 107.95) holds. Decisive break of 114.73 resistance will confirm our view and target 118.65 and above. However, sustained break of 55 day EMA will dampen this bullish view and turn focus back to 104.62 low instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Retail Sales Monitor Y/Y Apr | -4.20% | -0.80% | 1.40% | |

| 0:00 | JPY | Labor Cash Earnings Y/Y Mar | 2.10% | 1.00% | 1.30% | 1.00% |

| 5:00 | JPY | Leading Index CI Mar P | 105.1 | 106 | ||

| 12:30 | CAD | Building Permits M/M Mar | -2.60% | |||

| 12:30 | USD | PPI M/M Apr | 0.20% | 0.30% | ||

| 12:30 | USD | PPI Y/Y Apr | 2.80% | 3.00% | ||

| 12:30 | USD | PPI Core M/M Apr | 0.20% | 0.30% | ||

| 12:30 | USD | PPI Core Y/Y Apr | 2.40% | 2.70% | ||

| 14:00 | USD | Wholesale Inventories M/M Mar F | 0.60% | 0.50% | ||

| 14:30 | USD | Crude Oil Inventories | 6.2M | |||

| 21:00 | NZD | RBNZ Official Cash Rate | 1.75% | 1.75% |

{kind=link}