Live Comments

Swiss CPI flat as imported prices drag

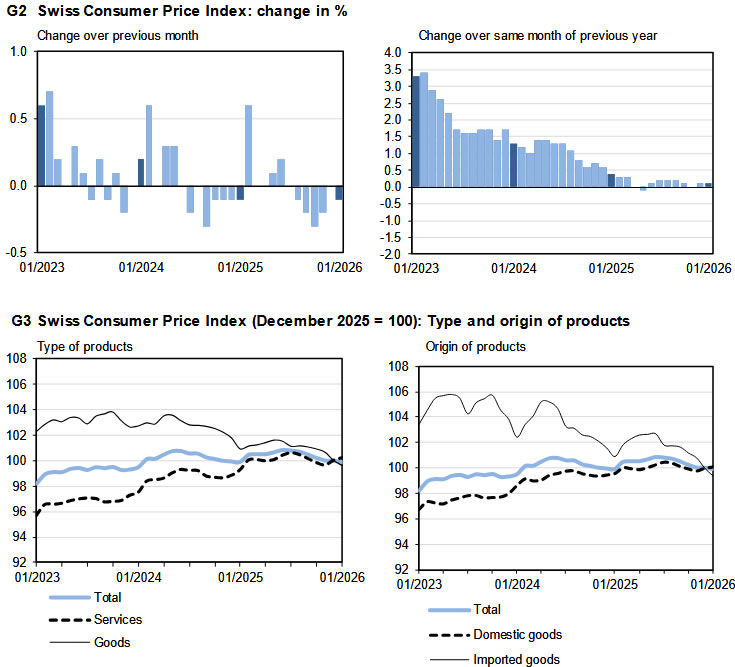

Switzerland’s consumer prices slipped -0.1% mom in January, undershooting expectations for a flat reading. The decline was largely driven by a -0.6% drop in imported product prices, while domestic prices edged up 0.1% on the month. Core CPI, which excludes fresh and seasonal products, energy and fuel, rose 0.1%, suggesting limited underlying pressure.

On an annual basis, headline inflation held steady at 0.1% yoy, in line with expectations. Core inflation was unchanged at 0.5%, with domestic product prices also steady at 0.5% from a year earlier. The data point to a subdued price environment, with limited momentum building in domestic costs.

Imported prices remained a key drag, falling -1.5% year-on-year compared with a -1.6% decline previously. The stronger Swiss Franc and softer external price dynamics continue to suppress imported inflation, keeping overall price growth well below levels seen elsewhere in Europe.

BoJ’s Tamura says inflation becoming “sticky,” sees scope to tighten

BoJ board member Naoki Tamura said in a speech that the wage–price cycle the Bank has been aiming to establish remains intact, with inflation increasingly driven by domestic factors rather than imported cost shocks. He argued that inflation is “becoming endogenous and sticky,” as higher labor costs replace raw material prices as the primary driver.

Tamura noted, as early as this spring the Bank could judge its price stability target achieved — provided wage growth in 2026 is confirmed to be consistent with the 2% goal for a third consecutive year. Such confirmation would mark a significant milestone in Japan’s long struggle to exit deflation.

He cautioned, however, that price developments warrant close attention as Yen resumes depreciation. Also, as firms continue to lift wages, there is strong potential for higher labor costs to be passed through across production, distribution and retail stages.

Tamura also there remains “considerable distance” to the neutral interest rate level, implying that even further rate hikes would leave financial conditions accommodative. The challenge, he said, is to avoid both a premature tightening that risks deflation and an environment of persistent inflation that exceeds what can be considered moderate — a balancing act that keeps normalization gradual.

Brutal risk shift ahead of US CPI: Yields sink, NASDAQ fails, USD/JPY under threat

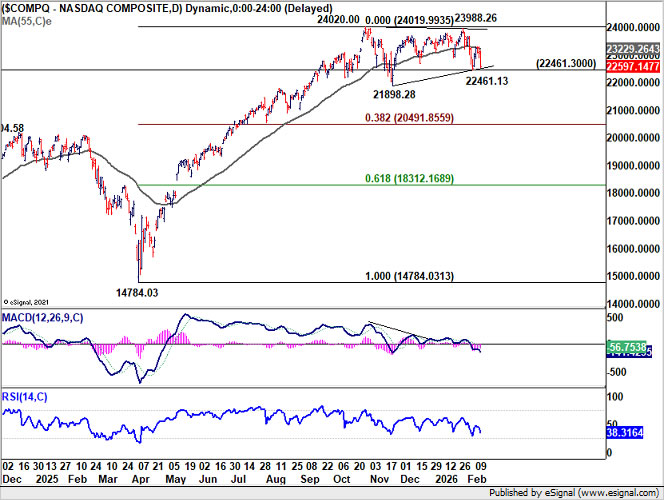

US equities staged a sharp reversal overnight, closing decisively lower with NASDAQ leading losses at -2%. DOW fell -1.3%, slipping back below the 50,000 mark after managing to hold it for four sessions only. Treasury markets reinforced the risk-off signal as 10-year yield took another leg lower and is now on the verge of breaking below 4.1% handle.

January CPI is due, but its influence may be limited. The strong non-farm payrolls report has effectively removed urgency for a March Fed move and supports a pause at least through June. Unless inflation delivers a major shock, markets would revert to broader risk dynamics once the event passes.

The catalyst behind the equity selloff is once again AI disruption anxiety. Software stocks, which have been under persistent pressure this year, extended losses sharply. More concerning is that the negative tone is spreading beyond technology. Financials came under pressure amid fears that AI could disrupt wealth management and advisory services. Industrials and logistics stocks also saw heavy selling on concerns that AI-driven efficiency gains in freight and supply chains could erode traditional revenue models. Even real estate came under scrutiny on speculation that higher unemployment or automation could dampen demand for office space.

Technically, NASDAQ’s rejection at the 55 D EMA (now at 23,229), is a clear near-term bearish signal. Immediate focus now turns to 22,461 support. Firm break there would open the door through 21,898 support towards 38.2% retracement of 14,784.03 to 24,020.00 at 20,419.85.

Meanwhile, 10-year yield’s close below 4.108 solidifies the view that the rebound from 3.947 3.947 has completed as a corrective move to 4.311. As long as 55 D EMA (now at 4.178) caps upside, downside risk dominates. Sustained trading below 4.100 would send yield further to 4.000 psychological level and potentially retest the October low near 3.947.

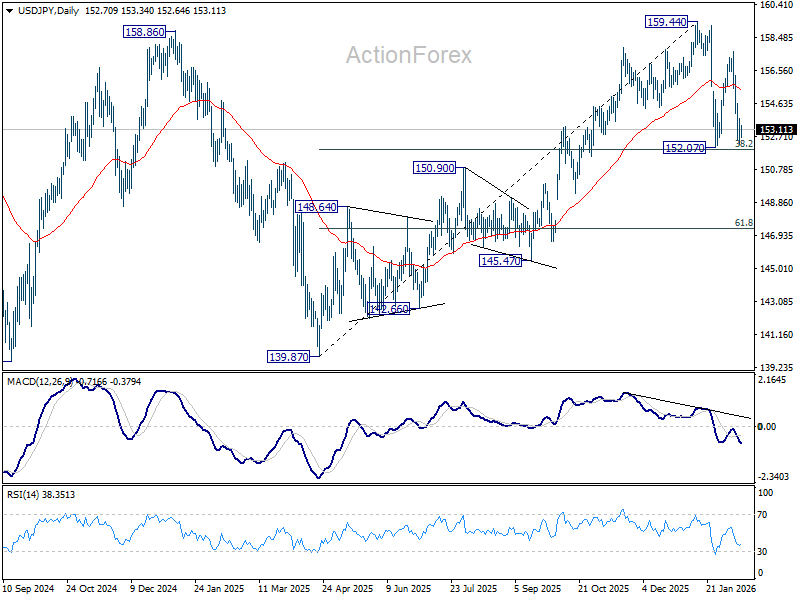

USD/JPY remains marginally above 38.2% retracement of 139.87 to 159.44 at 151.96, leaving the pattern from 159.44 technically seen as a consolidation within the broader uptrend from 139.87. As long as this level holds, the structural bias cannot be deemed decisively bearish.

That said, extended weakness in US equities and further decline in Treasury yields would likely intensify downside pressure on USD/JPY. A clear break below 151.96 would mark a significant technical shift towards bearish trend reversal. Deeper fall would then likely be seen to 61.8% retracement at 147.34, and possibly below.