BoE MPC member Catherine Mann said yesterday, “we already have very rapid increase in oil prices… In the U.K., that it becomes embedded by virtue of the institution mechanism of the price cap” on domestic energy bills.

“That embeddedness becomes a domestic inflationary problem that we have to deal with on the monetary policy stage,” she said.

“You only get inflation if businesses raise their prices. That’s where it comes from. It doesn’t come from wage settlements. It comes from businesses’ capacity to raise their prices in a systematic way and sustain demand,” she said.

New Zealand ANZ Business Confidence dropped to -38.1 in June, down from -32.0. Agriculture scored worse at -54.5, followed by construction at -42.3 and manufacturing at -41.4. Activity Outlook also dropped from 8.5 to 8.0.

ANZ noted: “The outlook for the economy is murky. As things stand, there is no reason for the economy to fall into a deep hole. Commodity prices are good, interest rates are at record lows, and the labour market is tight. But the economy is facing credit and cost headwinds and the global outlook is deteriorating. On the latter, for all that our commodity prices have been resilient, the risks are looking decidedly one-sided. Upside risks to growth appear few and far between and with the inflation outlook not consistent with the target midpoint we expect two more OCR cuts this year.”

Chicago Fed President Charles Evan said that is things “weren’t improving”, the 50bps rate hike in September is a “reasonable assessment”, but 75 bps “could also be ok”. He added “I doubt that more would be called for.”

“We wanted to get to neutral expeditiously. We want to get a little restrictive expeditiously,” Evans added. “We want to see if the real side effects are going to start coming back in line … or if we have a lot more ahead of us.”

ECB Governing Council member Ardo Hansson urged not to read too much in to the weaker than expected Q3 GDP figure (0.2% qoq released yesterday). He said, “these were preliminary numbers, maybe they were a bit slower than some expected.” And, “we have to wait and see what was behind this.” Also, he said “as there have been no significant, material change in one way or the other I would not make major conclusions” regarding monetary policy or economic outlook. He also emphasized the need to look at ECB’s own staff projections to be updated in December instead.

Separately, Daniele Nouy, chair of the Supervisory Board of the ECB, said that Eurozone has “reduced risks enough for the European Deposit Insurance Scheme to start.”. And it’s the right time to set it up and “consider some solidarity”. Nouy also added creating cross border consolidation in the banking said can be a solution to the top risks of low profitability. She said “such cross-border mergers would also create a few large European banks – let us call them `European champions’ – which could then successfully compete on the global stage.”

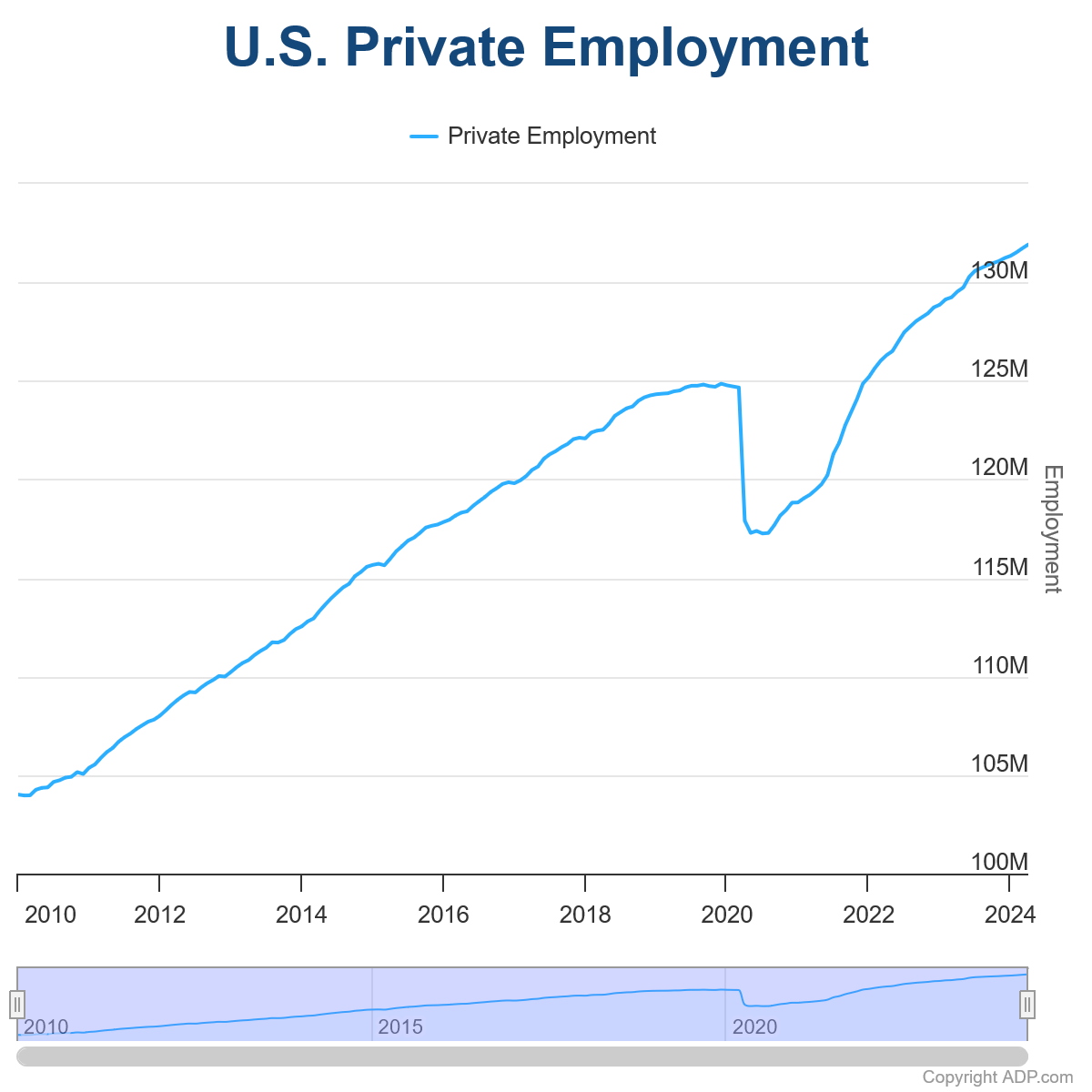

US ADP private employment grew 192k in April, above expectation of 180k. By sector, goods-producing jobs rose 47k, service-providing jobs rose 145k. By establishment size, small companies added 38k jobs, medium companies added 62k, large companies added 98k.

Year-over-year pay gains for job-stayers were little changed in April at 5%. Pay growth for job- changers fell from 10.1% in March to 9.3%.

“Hiring was broad-based in April,” said Nela Richardson, chief economist, ADP. “Only the information sector – telecommunications, media, and information technology – showed weakness, posting job losses and the smallest pace of pay gains since August 2021.”

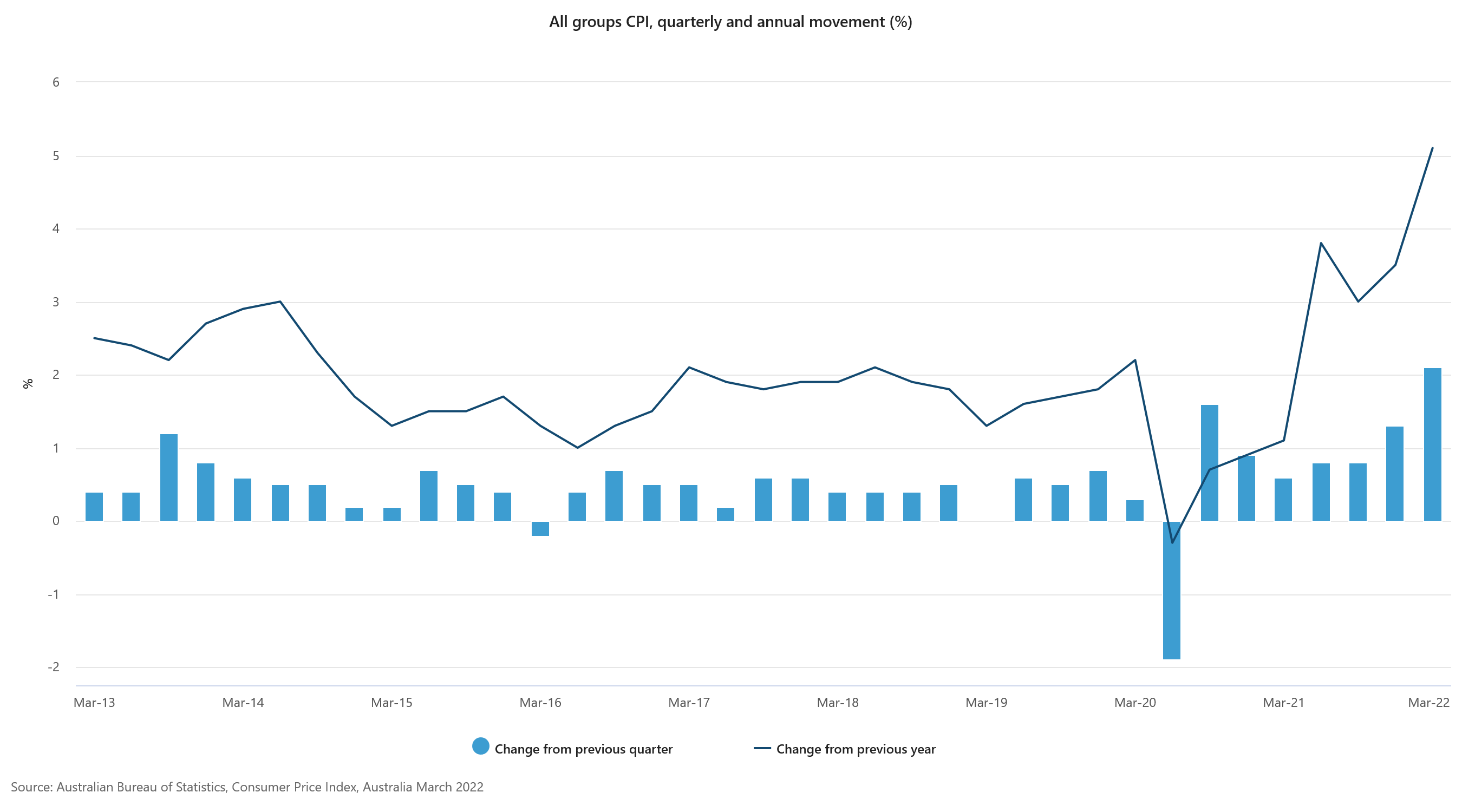

Australia CPI rose 2.1% qoq in Q1, accelerated from Q3’s 1.3% qoq, above expectation of 1.7% qoq. For the 12-month period, CPI accelerated to 5.1% yoy, up from 3.5% yoy, above expectation of 4.6% yoy. RBA trimmed mean CPI also accelerated from 2.6% yoy to 3.7% yoy, above expectation of 3.4% yoy.

Head of Prices Statistics at the ABS, Michelle Marquardt, said “The CPI recorded its largest quarterly and annual rises since the introduction of the goods and services tax (GST) (in 2000)”

“Strong demand combined with material and labour supply disruptions throughout the year resulted in the highest annual inflation for new dwellings since the introduction of the GST. Annual price inflation for automotive fuel was the highest since the 1990 Iraqi invasion of Kuwait.”

Marquardt said: “Annual trimmed mean inflation was the highest since 2009. This reflected the broad-based nature of price rises, as the impacts of supply disruptions, rising shipping costs and other global and domestic inflationary factors flowed through the economy.”

SNB Board member Andrea Maechler said yesterday that “we are still in a territory where the Swiss franc is high.” “The reality is, we continue to have a safe-haven currency,” she said. “Uncertainties remain high, largely because of the COVID crisis which continues to be there.”

“You’ve seen recently there has been quite an appreciation of the Swiss franc,” Maechler said. “Now if you look at the real exchange rate, it’s still higher than 2015. It is something that we do continue to monitor, and we will continue to do so.”

Maechler reiterated that it’s necessary for the central bank to intervene in the markets.

BoE Chief Economist Andy Haldane said two paths are possible for the economy in H2. “One involves a negative feedback loop from higher unemployment to lower spending, the other a positive feedback loop from higher spending to lower unemployment.”

The first poses a downside risk to the outlook, the second an upside risk. “As things stand, it is unclear which of these scenarios, or feedback loops, will prove the more potent,” he added.

Haldane also said risks to the economy remain “considerable and two-sided”. “Of these risks, the most important to avoid is a repeat of the high and long-duration unemployment rates of the 1980s, especially among young people.”

ifo Institute forecasts German economy to grow 2.6% in 2018, then slow to 2.1% in 2019. It’s head of f Economic Forecasting Timo Wollmershaeuser noted that the calculations “confirm figures from our December forecast.: However, “underlying forces have shifted somewhat.”

In particular, forecast for household consumption expenditure was scaled by by 0.5% in 2018, because of lower than expected spending back in 2H 2017. Government spending forecast was raised by 0.5% in 2018, as new government policy will provide a stimulus. Export growth was revised up by 0.5% in 2018, thanks to upturn in Eurozone economy and US tax cuts.

Regarding risks, “the debate over the introduction and/or increase in tariffs on transatlantic trade and the appreciation of the euro are weakening sentiment among German companies.” Also, the new coalition government is “disappointing in terms of reforming the tax and social security system.” In particular, Wollmershaeuser said that was no response to US, France and UK tax cuts.

China’s Central Bank, PBoC, issued a statement in its website regarding Governor Yi Gang’s response to China Securities Journal regarding recent decline in the Yuan.

Yi acknowledged the fluctuation in the exchange rate and said the central bank is “pay closing attention”. He attributed to the decline of Chinese Yuan to strength of the US Dollar, external uncertainties and some procyclical behaviors.

He also noted that the “managed floating exchange rate system” is based on market supply and demand. And “practice over the years has proven that this system must be effective and must be adhered to”.

At the same time, China is committed to deepen the reform of exchange rate marketization and use sufficient policy tools to ” maintain the basic stability of the RMB exchange rate at a reasonable and balanced level.”

German ZEW Economic Sentiment dropped to -24.5 in July, down from -21.1 and missed expectation of -22. Current Situation Index dropped to -1.1, down from 7.8 and missed expectation of 5. Eurozone ZEW economic sentiment dropped slightly to -20.3, down from -20.3 and beat expectation of -20.9. Eurozone Current Situation index dropped -6.9 to -10.6.

ZEW President Achim Wambach said: “Continued negative trend in incoming orders in the German industry is likely to have reinforced the financial market experts’ pessimistic sentiment. A lasting containment of the factors that are causing uncertainty in the export-oriented sectors of the German economy is currently not in sight. The Iran conflict seems to be intensifying and the ongoing trade dispute between the USA and China is a burden not only to Chinese economic development. Furthermore, no discernible progress has been made in the negotiations as to what Brexit will look like.”

Entering into European session, Australian Dollar is the weakest one for today. RBA revealed new economic projections that indicate slow rise in inflation and unemployment rate. Also, it reiterated the stance that the chance for a hike or cut next is evenly balanced. Canadian Dollar is the second weakest as WTI crude oil dips below 52.5. The Loonie will look into job data to be released later today. Sterling’s post BoE rebound lost steam and is now the third weakest.

Yen and Swiss Franc are strong on risk aversion. Investors are apparently troubled by news that Trump is not going to meet Chinese Xi to seal the trade deal this month. New Zealand Dollar is also strong today but it’s just recovering yesterday’s steep post-job data selloff. Dollar is mixed for now.

For the week, Dollar is overwhelmingly the strongest one, trading above prior week’s high against all but Yen. Yen is the second strongest, followed by Swiss Franc. Falling global treasury yields and mild risk aversion are support these two safe-haven currencies. Commodity currencies are weakest, led by Australian Dollar.

In Asia:

Nikkei closed down -2.01%.

Hong Kong HSI is back from holiday and is down -0.22%.

China is still on holiday.

Singapore Strait Times is down -0.10%.

Japan 10-year JGB yield is down -0.0227 at -0.031.

Overnight:

DOW dropped -0.87%.

S&P 500 dropped -0.94%.

NASDAQ dropped -1.18%.

10-year yield dropped -0.050 to 2.652, back below 2.7% handle.

30-year yield dropped -0.045 to 2.993, lost 3.0% handle.

UK Prime Minister Boris Johnson’s effort to end Brexit drama failed, at least for now, after suffering humiliating defeat in the House of Commons today. MPs passed an amendment tabled by former Conservatives Minister Oliver Letwin by 322 to 306. Under the amendment, the so-called Benn act was trigger that forces Johnson to seek Brexit extension through January 31, 2020. And, the meaningful vote on the Brexit deal wouldn’t be held today. Johnson said immediate that he will not negotiate a further delay with the EU. But in doing so, he could in the end face being held in contempt of court.

Meanwhile, Europe Commission spokesperson quickly said “The European commission takes note of the vote in the House of Commons today on the so-called Letwin amendment meaning that the withdrawal agreement itself was not put to vote today. It will be for the UK government to inform us about the next steps as soon as possible.”

The Pound, and other European majors, might suffer some setback as the week opens. But Johnson is generally expected to concede and seek a delay. And EU is not expected to reject it despite all the hassles. Thus, any setback could be temporary. And the guesses on whether Johnson would get enough votes for his deal would continue.

Lira has a quick dip in early US session while Yen crosses recover in general. The trigger is a social media report that American pastor Andrew Brunson, will be released from house arrest by August 15.

The U.S. Embassy in Ankara, Turkey, quickly comes out and denies that it released related statement.

While the rumor is denied, the reactions in the markets argue that traders are ready to take any positive news to close out their positions. The worst of Turkish crisis might be temporarily over.

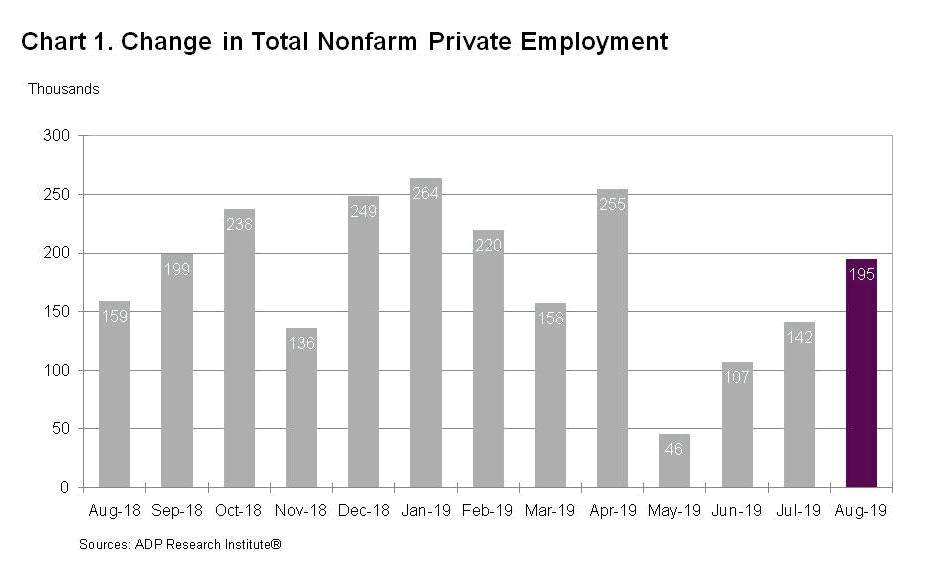

ADP report showed 195k growth in private sector jobs in August, well above expectation of 140k. Jobs in goods-producing sector grew 11k while jobs in service-providing sectors grew 184k. Small businesses added 66k, medium business added 77k, large businesses added 52k.

“In August we saw a rebound in private-sector employment,” said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. “This is the first time in the last 12 months that we have seen balanced job growth across small, medium and large-sized companies.”

Mark Zandi, chief economist of Moody’s Analytics, said, “Businesses are holding firm on their payrolls despite the slowing economy. Hiring has moderated, but layoffs remain low. As long as this continues recession will remain at bay.”

Good morning. I’m pleased to be here with you to discuss today’s policy announcement and the Bank of Canada’s Monetary Policy Report (MPR). I am especially pleased to have Senior Deputy Governor Carolyn Rogers here for her first press conference. She has joined the Governing Council at an important time.

Our message today is threefold.

First, the emergency monetary measures needed to support the economy through the pandemic are no longer required and they have ended.

Second, interest rates will need to increase to control inflation. Canadians should expect a rising path for interest rates.

Third, while reopening our economy after repeated waves of the COVID-19 pandemic is complicated, Canadians can be confident that the Bank of Canada will control inflation. We are committed to bringing inflation back to target.

Let me take each of these in turn.

The Bank’s response to the pandemic has been forceful. Throughout, our actions have been guided by our mandate. We have been resolute and deliberate, communicating clearly with Canadians on our extraordinary measures to support the economy and on the conditions for their exit. When we introduced emergency liquidity measures to support core funding markets, we said they would end when market functioning was restored. And they did. When we launched quantitative easing (QE), we said it would continue until the recovery was well underway. As the recovery progressed, we began tapering QE and ended it in October. Today marks the final step in exiting from emergency policies. We said exceptional forward guidance would continue until economic slack was absorbed. With the strength of the recovery through the second half of 2021, the Governing Council now judges this condition has been met. As such, we are removing our commitment to hold our policy rate at its floor of 0.25%.

Second, we want to clearly signal that we expect interest rates will need to increase. A lot of factors are contributing to the uncomfortably high inflation we are experiencing today, and many of them are global and reflect the unique circumstances of the pandemic. As the pandemic fades, conditions will normalize, and inflation will come down. However, with Canadian labour markets tightening and evidence of capacity pressures increasing, the Governing Council expects higher interest rates will be needed to bring inflation back to the 2% target.

Finally, Canadians can be assured that the Bank of Canada will control inflation. Prices for many goods and services are rising quickly, and this is making it harder for Canadians to make ends meet—particularly those with low incomes. Prices for food, gasoline and housing have all risen faster than usual. We expect inflation will remain close to 5% through the first half of 2022 and then move lower. There is some uncertainty about how quickly inflation will come down because we’ve never experienced a pandemic like this before. But Canadians can be assured that we will use our monetary policy tools to control inflation.

Let me turn to the economic outlook that we’ve outlined in our MPR.

Globally, the pandemic recovery is strong but uneven and continues to be marked by supply chain disruptions. Robust demand for goods combined with these supply problems and higher energy prices have pushed up global inflation. With this rise in inflation, expectations that monetary stimulus will be reduced have been pulled forward and financial conditions have tightened from very accommodative levels.

In Canada, growth in the second half of 2021 was even stronger than we had projected, and a wide range of measures now suggest economic slack is absorbed. With the rapid spread of the Omicron variant, first-quarter growth is likely to be modest, but we expect the impact on our economy to be less severe than previous waves. We forecast annual growth in economic activity will be 4% this year and about 3½% in 2023 as consumer spending on services rebounds and business investment and exports show solid growth.

CPI inflation is currently well above our target range and core measures have edged up. Global supply chain disruptions, weather-related increases in agricultural prices and high energy prices have put upward pressure on inflation in Canada, and that is expected to continue in the months ahead. These pressures should ease in the second half of 2022, and inflation should decline relatively quickly to around 3% by year end. Further out, we expect demand will moderate and supply will increase as productivity improves. This will ease price pressures and bring inflation gradually back close to the 2% target over 2023 and 2024.

Let me now say a few words about the Governing Council’s deliberations.

Of course, we discussed the impact of Omicron. Renewed restrictions and household caution about this highly infectious variant have temporarily slowed economic activity. Once again, high-contact services sectors have been hardest hit. But with many more Canadians getting infected in this wave, worker absences have been more widespread. Our high rates of vaccination and adaptability to restrictions should limit the downside economic risks of this wave.

The Governing Council also spent considerable time assessing the overall balance of demand and supply in the economy. In October, we projected the output gap would close sometime in the middle quarters of this year. While measuring the output gap is always uncertain and pandemic-related distortions make assessing supply more complicated, a broad range of indicators clearly suggest economic slack has been absorbed more quickly than expected. Employment is above pre-pandemic levels, businesses are having a hard time filling job openings, and wage increases are picking up. Unevenness across sectors remains, but taking all the evidence together, the Governing Council judges the economy is now operating close to its capacity.

We debated the most likely path for inflation. The resolution of global supply bottlenecks has important implications for inflation in Canada. There is some evidence that supply disruptions may have peaked, but the spread of Omicron is a new wildcard that could further disrupt global supply chains. We also considered the potential for some reversal of the large price increases for goods. This would pull inflation down more quickly than we forecast. Overall, we judged the risks around our inflation projection are reasonably balanced.

We also assessed more domestic sources of inflationary pressures. While global goods price inflation is expected to ease, the tightness in Canadian labour markets, rising house prices and evident capacity pressures suggest that if demand continues to grow faster than supply this will put upward pressure on inflation.

We noted that measures of inflation expectations are broadly in line with our own forecast, with longer-term expectations remaining well anchored on the 2% target. We agreed it is paramount to ensure that higher near-term inflation expectations don’t migrate into higher long-term expectations and become embedded in ongoing inflation.

Putting all this together, we concluded that, consistent with our forecast, a rising path for interest rates will be required to moderate spending growth and bring inflation back to target.

Of course, we discussed when to begin increasing our policy interest rate. Our approach to monetary policy throughout the pandemic has been deliberate, and we were mindful that the rapid spread of Omicron will dampen spending in the first quarter. So we decided to keep our policy rate unchanged today, remove our commitment to hold it at its floor, and signal that rates can be expected to increase going forward. As we indicated in our press release this morning, the timing and pace of those increases will be guided by the Bank’s commitment to achieving the 2% inflation target.

We take our communication with Canadians very seriously. For almost two years now we have told Canadians we would keep our policy rate pinned at its floor until economic slack is absorbed. With slack absorbed more quickly than expected, it is time to remove our extraordinary forward guidance. This ends our emergency policy setting and signals that interest rates will now be on a rising path. This is a significant shift in monetary policy, and we judged that it is appropriate to move forward in a deliberate series of steps.

Let me say a final word about another important monetary policy tool—our balance sheet. The Bank will keep the holdings of Government of Canada bonds on our balance sheet roughly constant at least until we begin to raise the policy interest rate. At that time, we will consider exiting the reinvestment phase and reducing the size of our balance sheet by allowing maturing Government of Canada bonds to roll off. As we have done in the past, before implementing changes to our balance sheet management, we will provide more information on our plans.

With that, Senior Deputy Governor Rogers and I will be happy to take your questions.

US initial jobless claims dropped -3k to 213k in the week ending January 12, slightly below expectation of 218k. Four week moving average of initial claims dropped -1k to 220.75k.

Continuing claims rose 18k to 1.737M in the week ending January 5. Four-week moving average of continuing claims rose 8k to 1.7285M.

Strong buying emerges in GBP as it surges across the board just now. In particular GBP/USD has taken out last week’s high at 1.4295 and is on track to 1.4345 resistance (2018 high).

Looking at GBP action bias table, bullishness in the GBP is consistently against all other major currency In particular, GBPUSD is on upside bias across time frame.

The GBPUSD D action bias chart also supports that’ it’s heading to 1.4345 and above.

Canadian Foreign Minister Chrystia Freeland U.S. Trade Representative Robert Lighthizer and Mexican Economy Minister Ildefonso Guajardo started intensive NAFTA talks in Washington yesterday.

Freeland sounded upbeat as she said there were “good progress” made on the “rules of origin in our conversations with the U.S., with Mexico, and in our trilateral conversation.” But she declined to comment on whether there would be a deal within the next three weeks, as the US is pushing for.

Freeland just noted that “our commitment is to get a really good win-win-win outcome as quickly as possible and…we’ll work as long as it takes to get a great deal”.

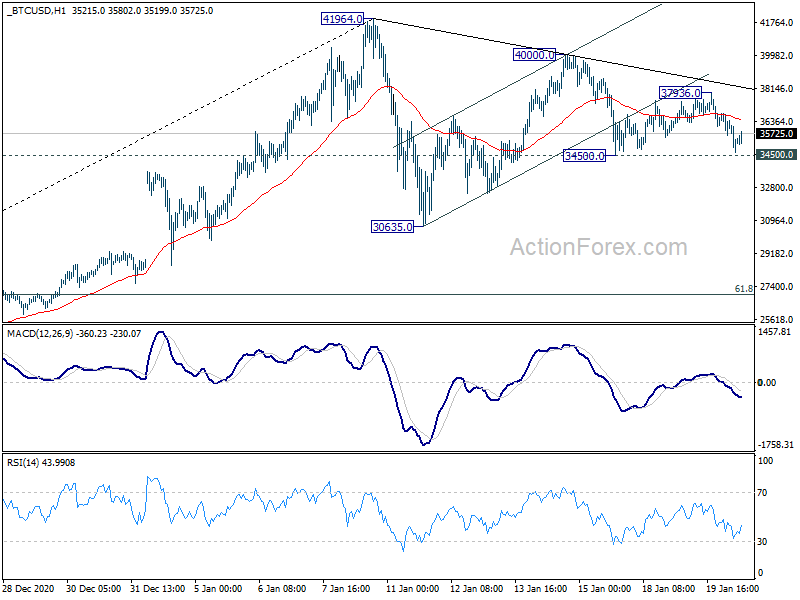

We’re holding on to the view that bitcoin’s price actions from 40000 represents the third leg of the corrective pattern from 41964.0. This is affirmed by the fact that corrective recovery from 34500 to 37936 was limit by the channel support turned resistance. Focus is now back on 34500 support. Break there will further confirm our view and target 30635 support next. Still, even in this case, we’re not expecting and firm break of 30k handle. Meanwhile, break of 37936 resistance will dampen this view and bring strong rebound, probably through 40000 to retest 41964 high.

BoE Mann: Embedded inflation becomes a domestic problem

BoE MPC member Catherine Mann said yesterday, “we already have very rapid increase in oil prices… In the U.K., that it becomes embedded by virtue of the institution mechanism of the price cap” on domestic energy bills.

“That embeddedness becomes a domestic inflationary problem that we have to deal with on the monetary policy stage,” she said.

“You only get inflation if businesses raise their prices. That’s where it comes from. It doesn’t come from wage settlements. It comes from businesses’ capacity to raise their prices in a systematic way and sustain demand,” she said.