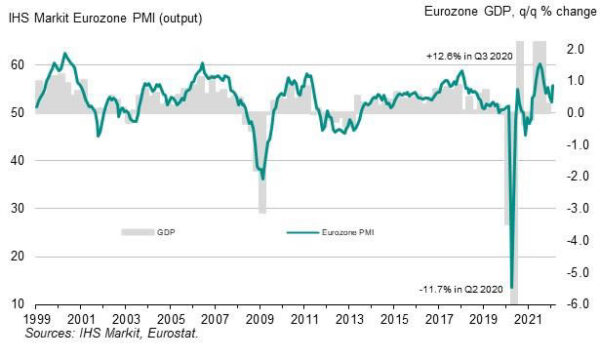

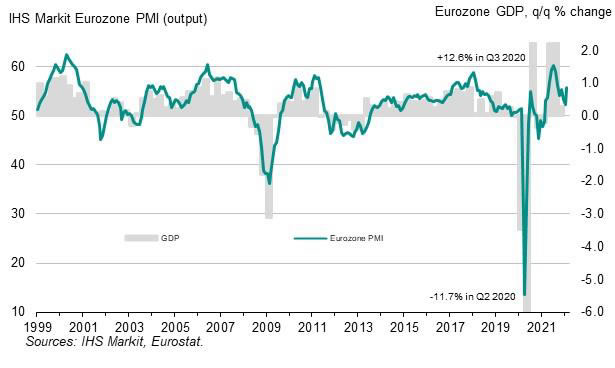

Eurozone PMI Manufacturing dipped slightly from 58.7 to 58.4 in February, below expectation of 58.7. PMI Services, on the other hand, jumped from 51.1. to 55.8, above expectation of 51.7. PMI Composite rose from 52.3 to 55.8, a 5-month high.

Chris Williamson, Chief Business Economist at IHS Markit said:

“The eurozone economy regained momentum in February as an easing of virus-fighting restrictions led to renewed demand for many consumer services, such as travel, tourism and recreation, and helped alleviate supply bottlenecks. Business optimism in the outlook has likewise improved as companies look to the further reopening of the economy, encouraging increased hiring.

“However, although easing, supply constraints remain widespread and continue to cause rising backlogs of work. As such, demand has again outstripped supply, handing pricing power to producers and service providers. At the same time, soaring energy costs and rising wages have added to inflationary pressures, resulting in the largest rise in selling prices yet recorded in a quarter of a century of survey data history.

“The strength of the rebound in business activity signalled by the PMI provides welcome evidence that the economy has so far shown encouraging resilience in the face of the Omicron wave, but the intensification of inflationary pressures will add to speculation of an increasing hawkish stance at the ECB.”

Full release here.

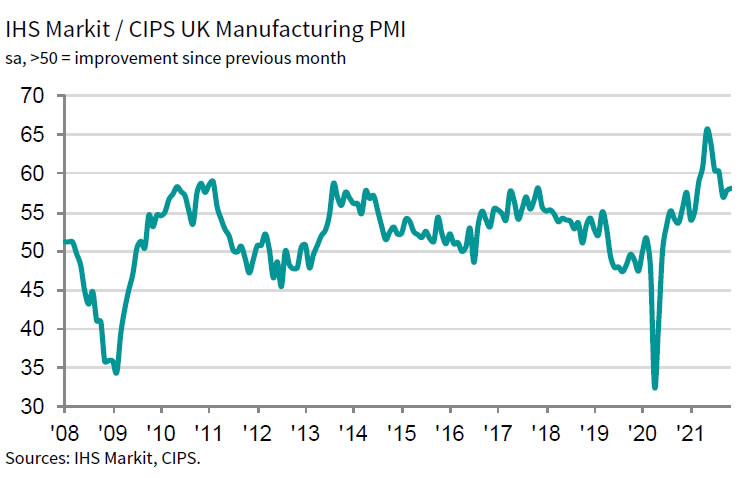

UK PMI manufacturing finalized at 45.3 in Dec, took a further turn for the worse

UK PMI Manufacturing was finalized at 45.3 in December, down from 46.5 in November, a 31-month low. S&P Global noted that production and new orders fell at faster rates, leading to accelerated job losses. Selling price and input cost inflation eased.

Rob Dobson, Director at S&P Global Market Intelligence, said: “The UK manufacturing downturn took a further turn for the worse at the end of the year. Output contracted at one of the quickest rates during the past 14 years, as new order inflows weakened and supply chain issues continued to bite. The decline in new business was worryingly steep, as weak domestic demand was accompanied by a further marked drop in new orders from overseas.

Full release here.