China Ministry of Commerce announced to start to impose 25% retaliatory tariffs on USD 16B in US goods starting August 23, “in parallel with the US. The MOFCOM condemned that the US “once again overrides international law: as a very unreasonable practice. And Chin’s countermeasures were to safeguard its own “legitimate rights and interest and global multilateral trading system”.

Full short statement in simplified Chinese.

This is in response to US Trade Representative’s announcement yesterday, to start to collect 25% tariffs on USD 16B of Chinese imports starting August 23. The announced lists contains 279 of the original 284 tariff lines that were proposed back on June 15.

As a recap, this is the second tranche of tariffs as part of the Section 301 intellectual property investigations. The first tranche of 25% tariffs on USD 34B of Chinese goods already took effect on July 6. The upcoming 25% tariffs on USD 200B in Chinese goods are work in progress.

RBA Lowe said economy reached a gentle turning point, but growth forecasts revised down

In the “Opening Statement to the House of Representatives Standing Committee on Economics“, RBA Governor Philip Lowe said “there are signs the economy may have reached a gentle turning point”. The economic outlook is supported by lower interest rates, tax cuts, weaker exchange rate, stabilization of housing markets, improvement in resources sector and infrastructure spending. Thus, “consistent with this, we are expecting the quarterly GDP growth outcomes to strengthen gradually after a run of disappointing numbers,” Lowe said.

Though, for now, Lowe reiterated that “It is reasonable to expect an extended period of low rates will be needed to achieve the Board’s employment and inflation objectives,.” And, at the Q&A session, Lowe also noted that “it’s possible we end up at the zero lower bound” on interest rates. He added “it’s unlikely but it is possible” and RBA is “prepared to do unconventional things if circumstances warranted.”.

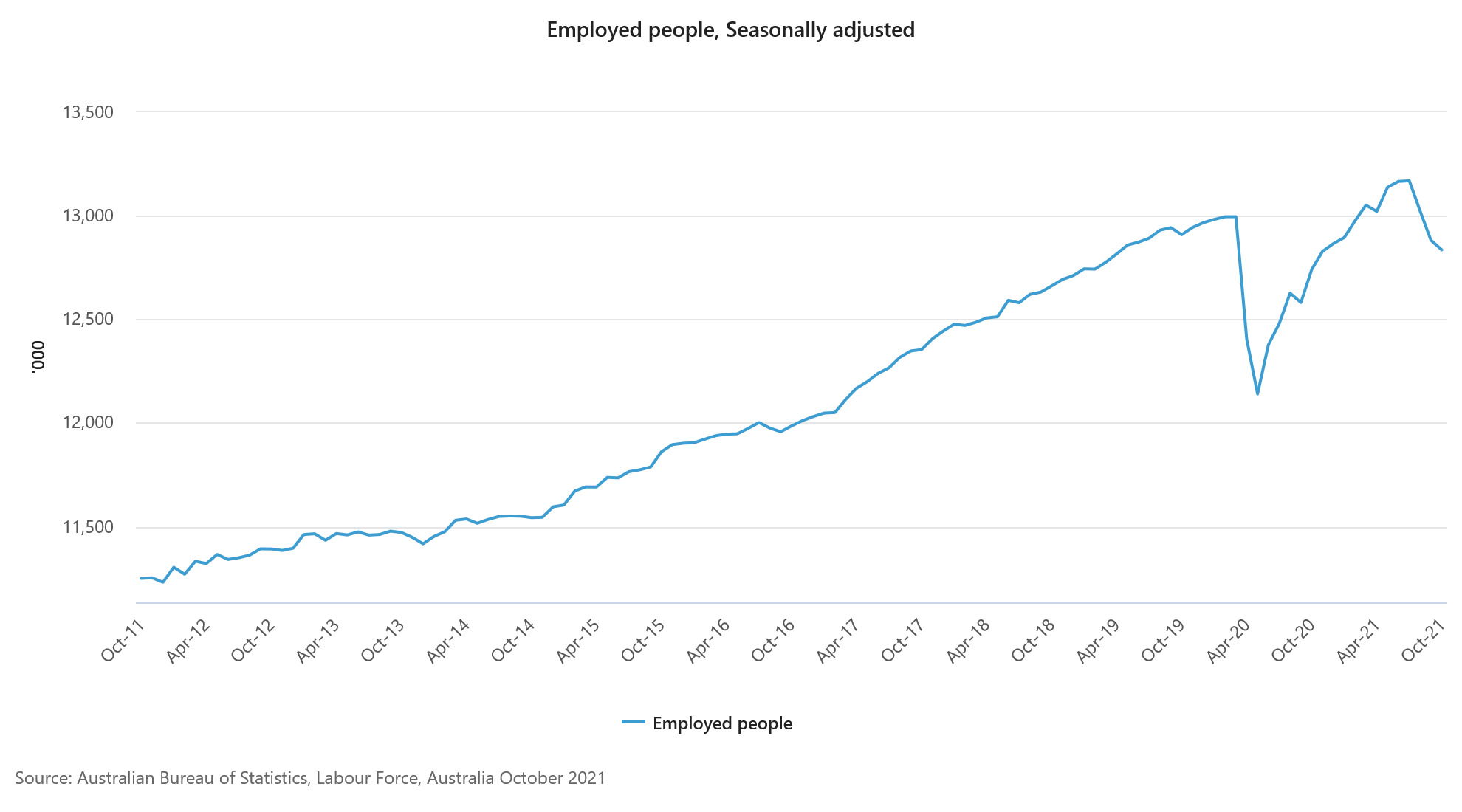

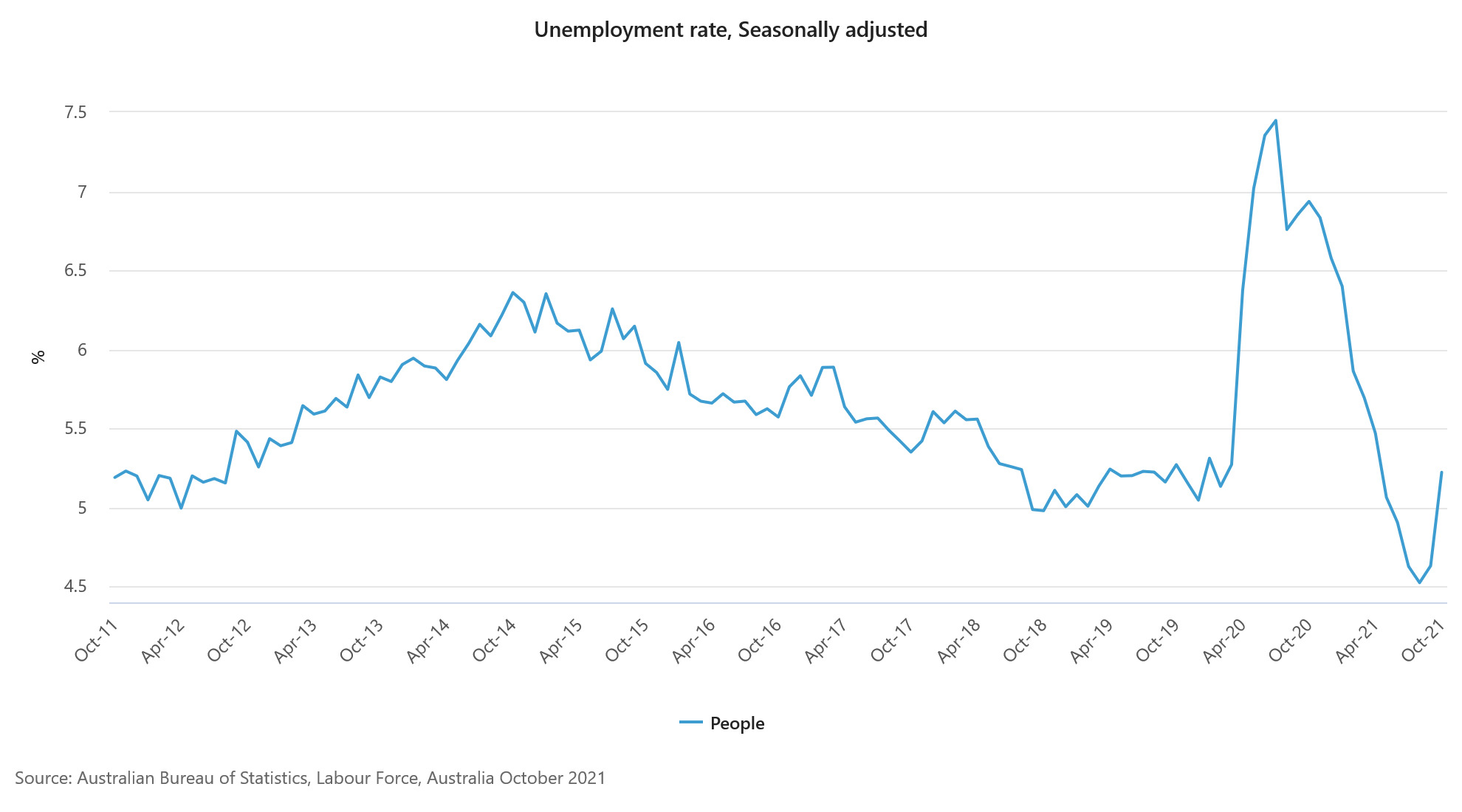

In the new economic forecasts, 2019 year end growth was revised down from 2.75% to 2.50%. 2020 year-end growth was unchanged at 2020%. 2021 year-end growth was expected to pick up to 3.00%. Unemployment rate forecasts for 2019 and 2002 year-end were revised up from 5.00% to 5.25%. Unemployment was expected to drop to 5.00% in 2021 year end. Headline CPI forecasts were also revised down from 2.00% to 1.75% at both 2019 and 2020 year-end, before picking up to 2.00% at 2021 year-end.