In the post meeting press conference, BoJ Governor Haruhiko Kuroda said “domestic and overseas markets remain jittery but tensions have eased somewhat.” He pledged that “the BOJ will continue with measures that are exerting positive effects in the economy”.

“There is absolutely no need to change our 2% inflation target,” he said. “Given the pandemic, inflation is falling quite a lot in many countries. Prices may start falling in Japan as well. But that doesn’t mean Japan and western countries are discussing the need to change their inflation targets.”

On exchange rate, Kuroda reiterated that “currency rates should move in a way that reflects economic fundamentals.” He maintained the stance of “watching currency moves carefully from that perspective.”

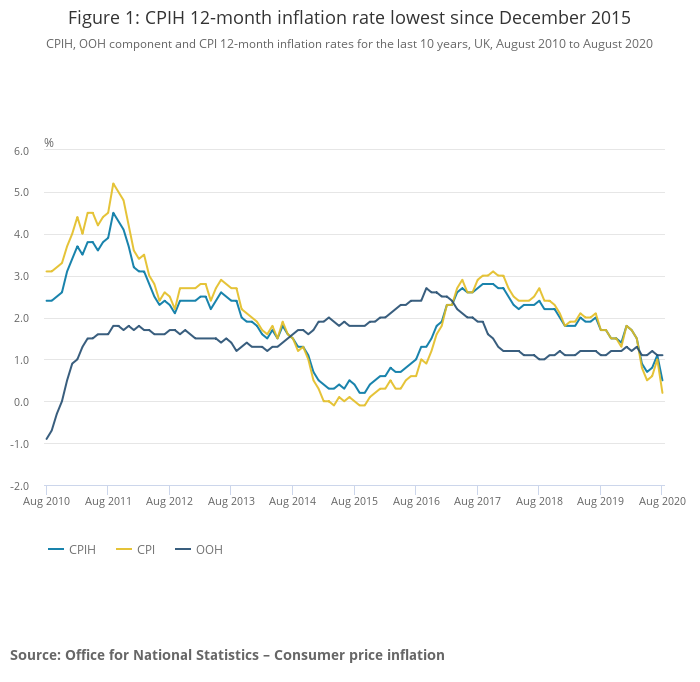

Eurozone CPI finalized at -0.2% in Aug, EU CPI at 0.4%

Eurozone CPI is finalized at -0.2% yoy in August, down from July’s 0.4% yoy. The highest contribution to the annual euro area inflation rate came from food, alcohol & tobacco (+0.33 percentage points, pp), followed by services (+0.30 pp), non-energy industrial goods (-0.03 pp) and energy (-0.77 pp).

EU CPI was finalized at 0.4% yoy, up from July’s 0.9% yoy. The lowest annual rates were registered in Cyprus (-2.9%), Greece (-2.3%) and Estonia (-1.3%). The highest annual rates were recorded in Hungary (4.0%), Poland (3.7%) and Czechia (3.5%). Compared with July, annual inflation fell in sixteen Member States, remained stable in five and rose in six.

Full release here.