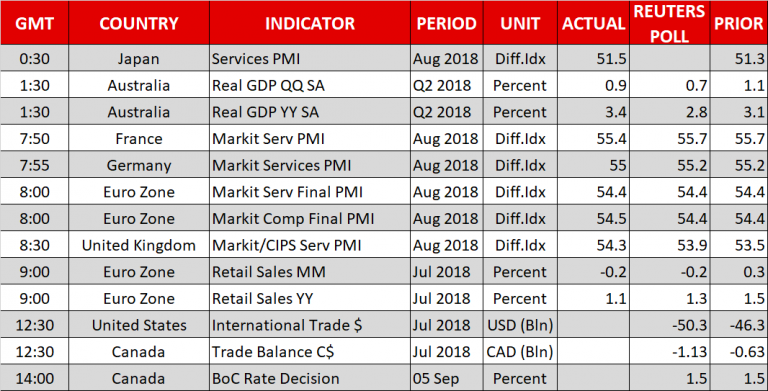

Here are the latest developments in global markets:

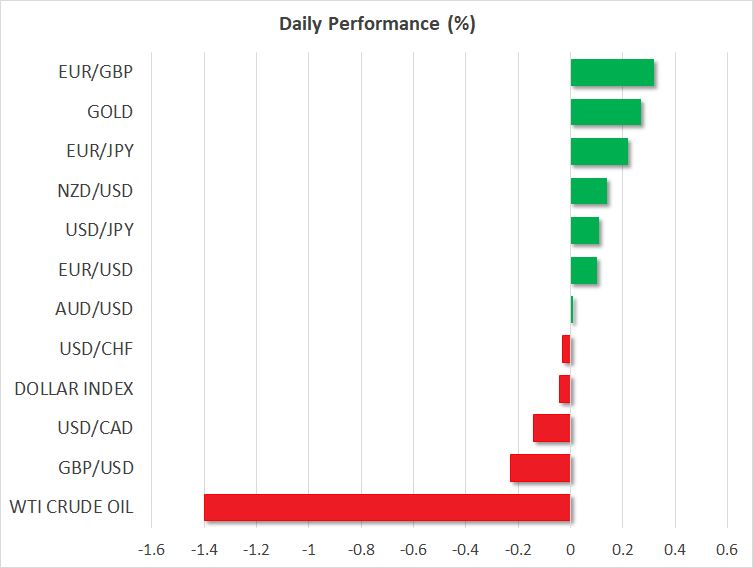

FOREX: The US dollar was moving sideways versus a basket of six major currencies on Wednesday as worries remain that the US President Donald Trump may soon restart a trade war with Beijing by imposing tariffs on more Chinese imports as early as tomorrow. Dollar/yen edged up by 0.12% but remained below its intraday high of 111.71. Turning to the euro area, the final German Markit services PMIfor the month of August was revised down to 55.0 compared to the 55.2 in the preliminary estimate, while the Eurozone Markit composite PMI finalized at 54.4 as expected in the same month. Meanwhile, retail sales in the euro area increased by 1.1% y/y in July from 1.2% previously, matching expectations. After the data, euro/dollar was trading lower by 0.11 %. Pound/dollar fell by 0.30% despite better-than-expected Markit/CIPS UK services PMI data; the index improved by 0.8 points to 54.3, compared to the expected 53.9. The antipodean currencies were mixed today, with aussie/dollar being flat and kiwi/dollar up by 0.11%. Dollar/loonie inched down to 1.3176 (-0.08%) after piercing slightly above the 1.3200 level on Tuesday. The BoC rate decision could bring further volatility to the loonie later today.

STOCKS: Investors were in a cautious mood in the European stock markets, driving equity indices lower on Wednesday except for the Italian FTSE MIB, which managed to surge by 1.0% at 1100 GMT; the upside move followed news by Italy’s deputy PM that the budget will be “courageous”. The pan-European STOXX 600 dived by 0.68% to its lowest since July and the blue-chip Euro STOXX 50 was down by 0.82%, hitting a 5-month trough. The German DAX 30 dropped by 0.61%, the UK’s FTSE 100 moved down by 0.33% and the Spanish IBEX 35 eased by 0.07%. The French CAC 40 was the worst performer, losing 0.95%. Futures tracking US stock indices were all in the red, pointing to a negative open.

COMMODITIES: Oil prices edged sharply lower today as a tropical storm hitting the US Gulf coast weakened. West Texas Intermediate (WTI) crude lost all the gains that it posted yesterday and dropped by 1.35% to $68.93/barrel. Brent oil retreated by 1.06% to $77.34 following the bounce off the highest level since May. In related news, Saudi Arabia said that it wants crude prices to stay between $70 and $80 per barrel, while OPEC’s General Secretary Mohammad Barkindo expressed the view that world oil demand will hit 100 million barrels per day “much sooner” than previously expected. Gold rose by 0.32% to $1,194.8/ounce.

Day ahead: Trade data out of the US and Canada eyed; BoC rate decision in the forefront

The US and Canada will see the release of trade data later on Wednesday as unresolved NAFTA negotiations between the countries resume today in Washington, a few days after the US president suggested to leave Canada out of the pact if the deal is not “fair” for the US. The talks will also come at a time when Bank of Canada (BoC) policymakers gather to decide on interest rates, with investors waiting eagerly to hear whether the BoC will keep its data-dependent approach under a riskier trade environment.

At 1230 GMT, the Bureau of Economic Analysis is expected to say that despite narrowing for the past three months, the US international trade deficit widened to $50.3 billion in July from $46.3bn in the previous month, reaching the highest since February. Investors, however, will likely be more interested to see whether the trade deficit was skewed on the Chinese or Canadian side as Washington continues to attack China and Canada.

At the same time in Canada, though, trade terms are also anticipated to deteriorate in July, with the deficit projected to come wider at C$1.13bn after reaching 1-year lows at C$0.63bn in June. Still, traders could wait for the BoC rate announcement later at 1400 GMT before taking a position on the loonie. Forecasts are for policymakers to hold borrowing costs unchanged at 1.50% with the probability for such an outcome currently standing at 82% according to overnight index swaps. Given that the NAFTA disagreements have fired up again, the central bank would prefer to sit on the sidelines for now despite inflation hitting 3.0% in July, the upper limit of its 1-3.0% price target.

Yet it could message that the next rate hike could come as soon as next month while flagging that the rate path will remain dependent on economic data to ensure that higher rates are manageable by high-indebted households. Note that household debt to disposable income ratio fell to the lowest in two years in the first quarter after new mortgage restrictions took effect in January. Should the rate statement sound more optimistic than analysts think, the loonie could recoup previous losses. On the other hand, if the BoC casts doubts on rate increases in coming months, the currency could lose ground. No press conference will follow by Governor Stephen Poloz after the completion of the meeting.

Elsewhere, Australian trade stats will come under review on Thursday at 0130 GMT, while Switzerland will publish GDP growth readings for the second quarter at 0545 GMT. In Sweden, the Riksbank is projected to hold rates steady at 0730 GMT and give a guideline on future rate hikes tomorrow.

Brexit will remain under the spotlight. Yesterday the Bank of England Chief, Mark Carney, said during his testimony in Parliament that he will extend his term beyond June 2019 to assist the British economy after its exit from the EU. Recall that the Treasury Committee has asked Carney to stay in his post until 2020.

Trade developments could make headlines during the day ahead of a crucial tariff deadline on Thursday; the US is scheduled to impose tariffs on $200 billion Chinese imports, while China could retaliate by unleashing tariffs on $60 billion US products.

In equities, executives from Facebook and Twitter, as well as Google’s top lawyer will be testifying before Congress on Wednesday on Russia meddling in the 2016 US presidential election.

In energy markets, weekly API data on US crude stocks are due at 2030 GMT.

In terms of public appearances, the dove Federal Reserve Bank of Minneapolis President, Neel Kashkari (FOMC member) will be speaking in Bozeman, Montana at 0800 GMT, while at 2230 GMT, the Atlanta Fed president, Raphael Bostic (FOMC member) will be commenting on monetary policy before a fireside chat of the Chicago Council on Global Affairs.

{kind=link}