European markets are finishing on a strong note as trade optimism grows as the US-China will resume talks for the first time since May 10th and after the ECB adjusted their forward guidance, highlighting that several members discussed the possibility of future interest rate cuts if conditions in the eurozone deteriorated. US futures are also modestly higher ahead of a highly anticipated non-farm payroll report, which is expected to show 175,000 jobs were created in May. Fed rate cut bets could get a boost if we see a big miss with today’s job number, with the June meeting possibly becoming a live meeting. Analysts are waiting to see if the ADP private payroll report, which showed the lowest creation of private sector jobs since March 2010, was the first crack being showed in the strongest part of the US economy, the labor market.

European stocks are green across the board with the CAC 40 leading the way higher with a 1.2% gain, Euro Stoxx 50 is up 0.9%, while the DAX is 0.6% stronger. Both the Dow and S&P futures are up 0.3% in early trade. Gold’s rally is taking a breather, with prices easing 0.2%, while oil benefited from the risk-on tone and positive comments from the Saudi oil minister.

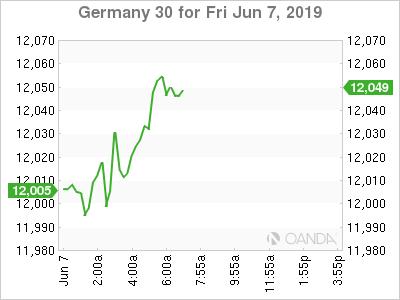

- DAX – ECB driven gains limited by very weak numbers out of Germany

- Trade – Mnuchin and Yi Gang aim to return constructive talks this weekend at G20

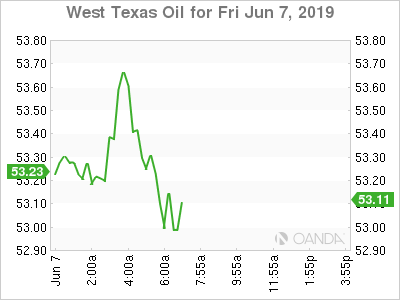

- Oil – Saudis remain confident cuts will be extended

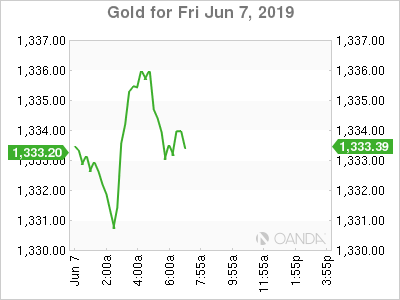

- Gold – Shines bright on trade and falling dollar expectations

DAX

The DAX is benefitting from the European Central Bank (ECB) policy decision that delivered a dovish bias that saw the bank focus more on the global picture and not so much to the eurozone rebound that occurred in Q1. Today’s gains from the DAX are slightly underperforming their neighbors as German data on industrial production and exports plunged in April. It appears German factories are no longer benefiting from Brexit stockpiling and industrial production fell to the a near four year low, prompting many to believe first quarter momentum did not carry over. With external risks rising in the eurozone, German manufacturing remains exposed to possible further weakness on Brexit risk and the impending US-Europe tariff battle. If the second quarter continues to disappoint, easing will easily be back on the ECB’s radar.

Bund yields are slightly higher today by 0.6 basis points to -0.235%, but that could be temporary if the markets begin to price in further rate cuts to stimulate domestic demand.

Trade

Markets are beginning to price in optimism that the US-China trade war will see officials resume constructive talks, while the battle in the Americas will see Mexico get hit with tariffs, but it could be short-lived as progress appears to be headed in the right direction.

Overnight, PBOC Governor Yi Gang reminded markets that China has ample policy tools if we continue to see trade tensions escalate. China has been active already in stimulating the economy and Yi Gang noted, “We have plenty of room in interest rates, we have plenty of room in required reserve ratio rate.” This weekend, he will hold talks with Secretary Mnuchin at the G20 finance minister meeting, a resumption of talks since May 10th, the day President Trump rose tariffs on $200 billion in Chinese goods to 25%.

Beijing and Washington’s extended break provided a blow to sentiment that may not easily be repaired even if we do see further progress this weekend. Markets will only be convinced if we hear constructive comments from both Xi and Trump. With a potential onslaught of fresh easing coming from most of the advanced economies central banks, we could see a trade deal be the catalyst needed to help take global equities back to their 2018 highs.

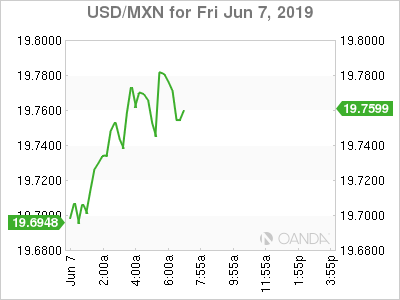

The Mexico and US are making progress with their talks, but might not see enough progress for Mexican goods to avoid the first round of tariffs on June 10th. Vice President Pence stated that the US will impose 5% tariffs on Mexico on Monday as planned. Mexican officials continue to highlight the progress that has been made and markets are starting to believe a sustainable deal is nearing. The Mexican peso is slightly softer against the dollar this morning.

Oil

Crude prices were supported by a united stance from the Russian and Saudi oil ministers, and by the overall optimisitc tone that is embracing risk assets. The energy ministers suggested the oil production cuts are likely to be continued, but that it is not a done deal. Saudi energy minister Al-Falih said he was sure the OPEC + production cuts would be extended and that the need to calibrate and not deepen cuts. Novak noted the contaminate crisis that clogged its main export route was almost fixed and that Poland will get crude shortly. Russia was the first country to suggest moving the OPEC and allies meeting and a date has still yet to be agreed upon. Novak stated that most countries agree on July 2nd to 4th.

West Texas Intermediate crude found major support from the $50.00 a barrel level and could see further bullish momentum if we see something constructive out of the G20 talks this weekend. If the Fed cuts rates sooner than later, that could provide dollar weakness which should be supportive for crude prices. The main driver for higher oil will remain on a pickup in global demand and that would likely stem from positive progress on all trade wars.

Gold

Gold prices are poised for their best weekly performance in six months as trade wars have dealt a strong blow to global growth and further easing appears to be on the way from all the major central banks. The yellow metal is poised for another major move higher if we see further dollar weakness. Fed cut rate bets have been on an upward trajectory and that could be confirmed if we see the strongest part of the US economy, the labor market show signs of weakness.

{kind=link}