Central bank meetings and the US jobs report will kick off the final month of 2019 next week, energising the markets as many traders return from the Thanksgiving break in the United States. The nonfarm payrolls report will of course be the main highlight as a positive print there could further add to the improving picture for the US economy, fuelling the dollar. But the ISM manufacturing and non-manufacturing PMIs will also be key in directing the greenback in the coming days. Elsewhere, both the Reserve Bank of Australia and the Bank of Canada are expected to stand pat. GDP figures out of Australia will also be watched, making it a busy week for aussie traders. Meanwhile, in commodities, major oil producers will be meeting in Vienna to decide what output quotas to set.

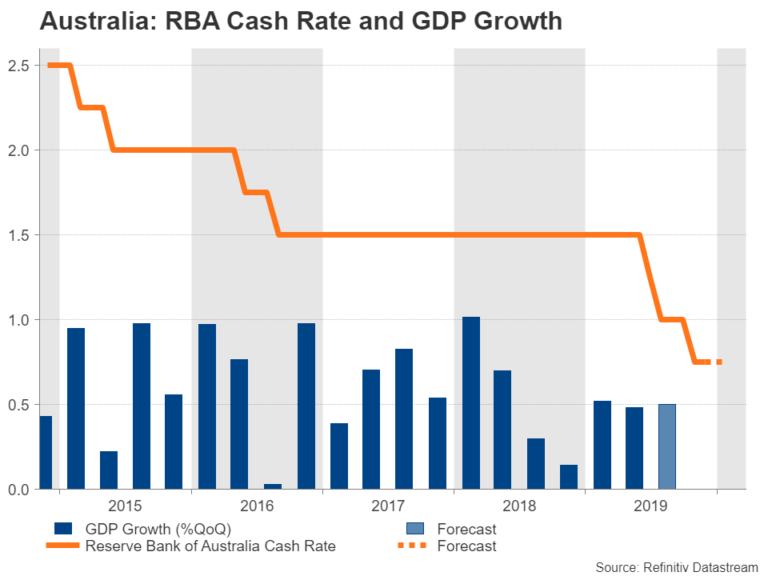

RBA meeting and Q3 GDP in focus for aussie

The risk-sensitive Australian dollar has been unable to capitalize on the trade deal optimism as the Australian economy appears too caught up in the US-China trade dispute for the outlook to brighten anytime soon. Talk of quantitative easing isn’t helping the aussie either even though RBA Governor Philip Lowe has suggested the country is “a fair way from it”. Lowe will get another chance to set the record straight next week when the RBA meets on Tuesday for its final gathering of the year.

Interest rate futures currently point to a 90% probability that the cash rate will be kept at 0.75% in December, but investors are in no doubt the RBA will ease again next year. The question is how soon will the next cut arrive? The clues will lie not only in the RBA’s policy statement but also in a batch of Q3 data due from Australia next week.

Third quarter numbers on business inventories, next exports contribution and Gross Domestic Product (GDP) are released on Monday, Tuesday and Wednesday, respectively. GDP is forecast to have expanded by 0.5% quarter-on-quarter in the three months to September, the same pace as in the second quarter.

In addition, October data on building approvals (Monday) and retail sales (Thursday) will be monitored, as well as the Caixin/IHS Markit manufacturing PMI out of China on Monday.

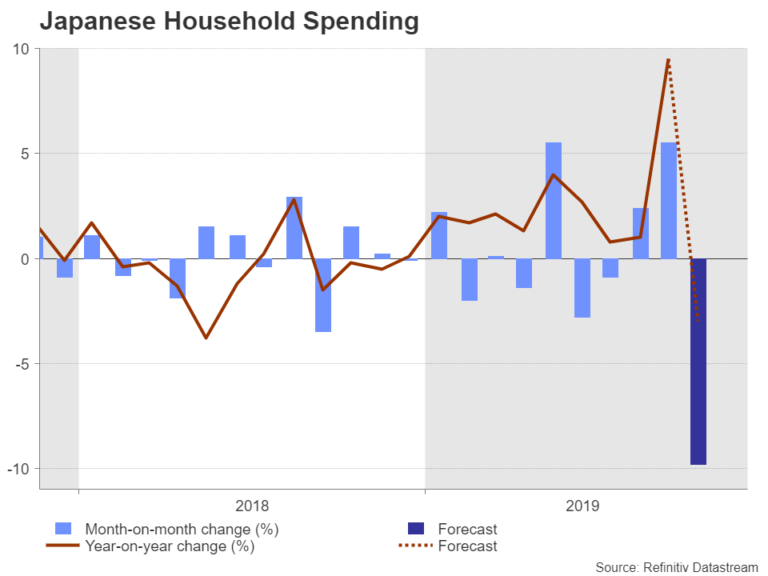

Japanese household spending likely slumped in October

After Japan’s worse-than-expected retail sales figures for October this week, all eyes will be on household spending numbers next Friday, which should provide a broader look at how consumption held up following the sales tax hike on October 1. Household spending is expected to have plunged by 9.8% month-on-month in October – somewhat better than the 14% drop recorded in April 2014 when the sales tax last went up.

Wage growth figures will also be published on the same day. Total cash earnings growth turned positive in September, having declined for most of the year. A further pick up in wage growth in October could ease concerns about a sustained drop in consumption if the household spending data is dismal.

Ahead of Friday’s releases, the third quarter estimate for capital expenditure will be watched on Monday, which is usually a good indicator as to whether the initial GDP growth reading is prone to a revision. However, unless there is a shockingly big decline in household consumption, next week’s data is unlikely to stir much of a reaction in the yen, as the Bank of Japan has set the bar high for further monetary easing.

Final PMIs to be European highlight

It will be a relatively quiet week in the Eurozone and the United Kingdom, with the main attraction being IHS Markit’s final PMI prints as well as German industrial orders and output numbers. The final manufacturing PMI is up first on Monday, with the services PMI coming up on Wednesday. The UK will also get the construction PMI, due on Tuesday.

Both the euro and the pound came under pressure from last week’s flash releases for November, which showed unexpected weakness in the services sector. The two currencies therefore stand to make some gains if there’s any upward revisions to the final readings, particularly in the services PMIs.

Perhaps of more significance for the euro though, are German industrial indicators for October. Any sign that the manufacturing downturn in Europe’s largest economy is bottoming out could help lift the single currency out of the doldrums. Industrial orders are due on Thursday, while industrial output is out on Friday. Other data worth observing are revised Eurozone GDP estimates for the third quarter and October retail sales figures on Thursday.

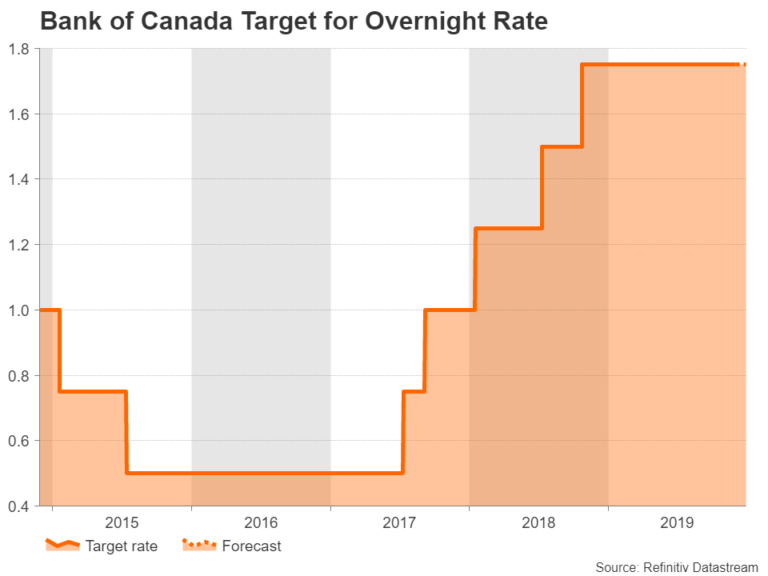

Bank of Canada expected to hold rates steady

Market odds of a December rate cut by the Bank of Canada shot up after Governor Stephen Poloz revealed that the Governing Council discussed the merits of an insurance cut at their October 30 meeting. However, those expectations quickly reversed after Poloz changed his tune three weeks later, sounding a more neutral tone.

Investors currently see less than a 5% chance of a rate cut on Wednesday when the BoC holds its last policy meeting of the year. A rate cut in 2020 is also not looking as certain as it did just a few weeks ago. Nevertheless, Poloz will likely reiterate at the meeting that the risks remain tilted to the downside as the trade war rumbles on.

Unusually, however, those shifting expectations have not been reflected in the dollar/loonie pair, with the Canadian dollar maintaining its post-October meeting losses as US data since then has been dollar supportive, while Canadian indicators have been on the weak side, pressuring the loonie.

If Poloz fails to clarify the BoC’s stance, traders may be able to take their cues from Canada’s employment report for November on Friday.

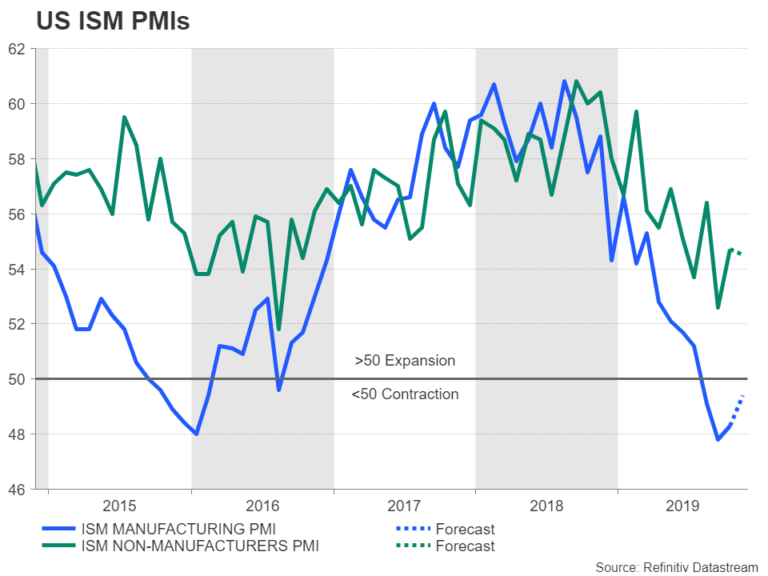

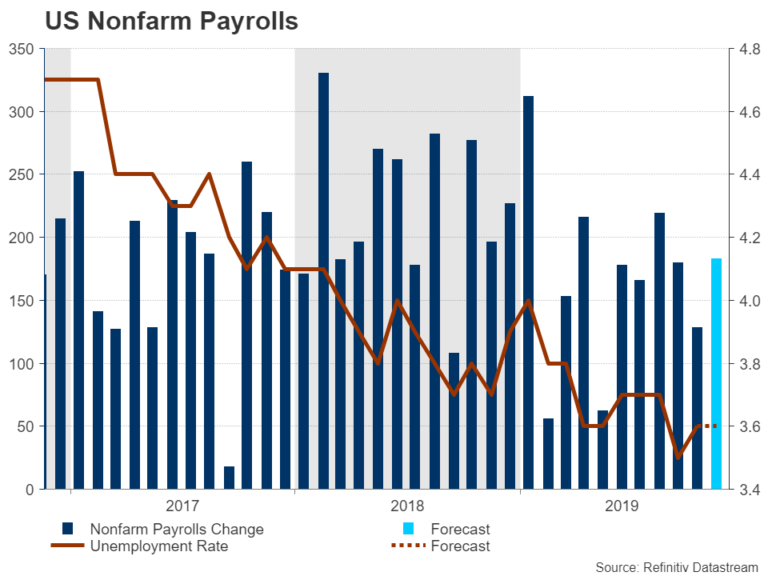

More dollar upside from NFP?

The US dollar has been crawling higher over the past week as positive trade headlines and encouraging economic pointers from the US have delivered a double boost for the currency. The run of upbeat releases could continue next week with the ISM PMIs and the all-important jobs report.

The ISM manufacturing PMI is out on Monday and is forecast to rise from 48.3 to 49.4 in November, which would confirm other recent data suggesting that the sector may be starting to recover. The ADP private employment survey on Wednesday should provide a clue as to what to anticipate from Friday’s government report. More importantly on Wednesday, the ISM non-manufacturing PMI will be viewed closely. The ISM’s composite index, which measures services and other non-manufacturing activity, is forecast to ease slightly to 54.5 in November after jumping to 54.7 in the prior month.

More data will follow on Thursday with October trade numbers and factory orders, but the market focus will really be on Friday’s nonfarm payrolls report. The headline NFP figure for November is expected at 183k, an improvement on the previous month’s gain of 128k jobs. No change is forecast in the unemployment rate of 3.6%, while average earnings are projected to have risen by 0.3% m/m, accelerating slightly from the prior month. Last but not least, the University of Michigan’s preliminary consumer sentiment survey will also be doing the rounds on Friday.

If next week’s numbers are broadly positive, the dollar is likely to extend its gains, though the bulls may struggle to overcome key resistance points its facing versus the euro and the yen at 1.10 per euro and 109.60 yen respectively.

OPEC+ meeting a downside risk for oil prices

OPEC, Russia and other major producers are scheduled to meet next Thursday and Friday to decide whether to extend the current output cap deal beyond March 2020. The consensus view is that the OPEC-led alliance will agree to extend the deal until June, though a longer extension until the end of 2020 is possible.

Saudi Arabia has been calling for even deeper cuts as it tries to boost prices ahead of the initial public offering of the state-owned oil giant Saudi Aramco. However, others like Russia are against further production cuts.

That’s not to say a surprise announcement of bigger cuts to the existing quotas should be discounted, but most reports suggest there isn’t enough support for tighter output restrictions. And with many industry analysts predicting a supply glut in the early parts of 2020, it’s looking unlikely that oil prices will be able to extend their bullish phase into next year.

{kind=link}