U.S. Review

Was April the Bottom?

- Data this week continued to suggest the U.S. economy hit rock bottom in April. Still, it is a long road to recovery and the pickup in economic activity will be gradual.

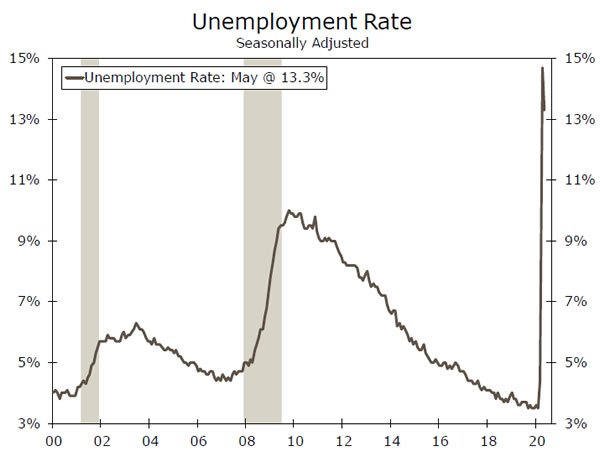

- In what was a surprising jobs report, the U.S. labor market added 2.5 million jobs in May and the unemployment rate fell to 13.3%. The bottom line: hiring started to pick-up earlier than expected as states began to loosen restrictions in May.

- Survey evidence from the ISM further supports the notion that economic activity has bottomed, as does mobility data, though they exemplify just how gradual the rebound may be.

Was April the Bottom?

The U.S. labor market added 2.5 million jobs in May. As you can probably gather, this was to the surprise of most analysts. The consensus forecast estimate was for a loss of 7.5 million jobs and not one forecaster expected an increase. So what happened?

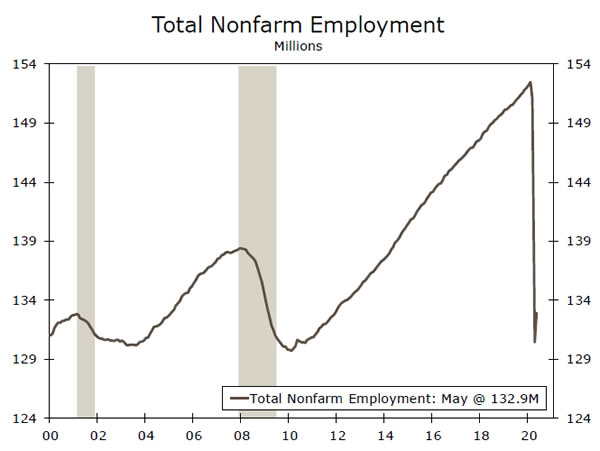

At a high level, the May employment report suggests the reopening of many parts of the economy led to an immediate pickup in hiring, or more likely re-hiring. The lifting of lockdowns has had a positive impact on the labor market earlier than expected, and after shedding a total 22 million jobs in March and April, businesses started to rehire in the midst of re-opening.

This was true of most sectors, as a majority of major industries added jobs, with the exception of government, which shed 585K positions, mostly due to education cuts. The most pronounced gain came in the hardest hit leisure & hospitality sector, which added over 1.2 million jobs.

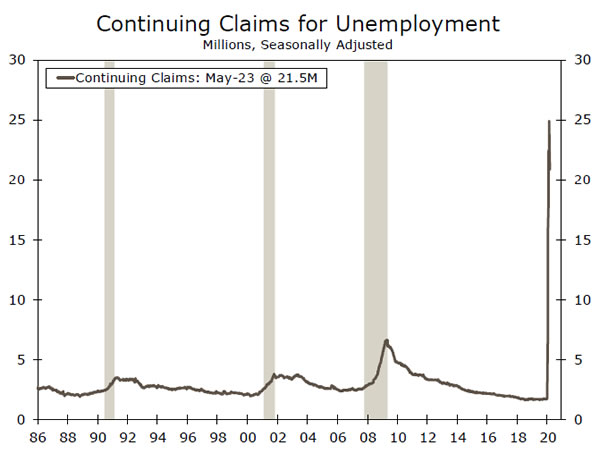

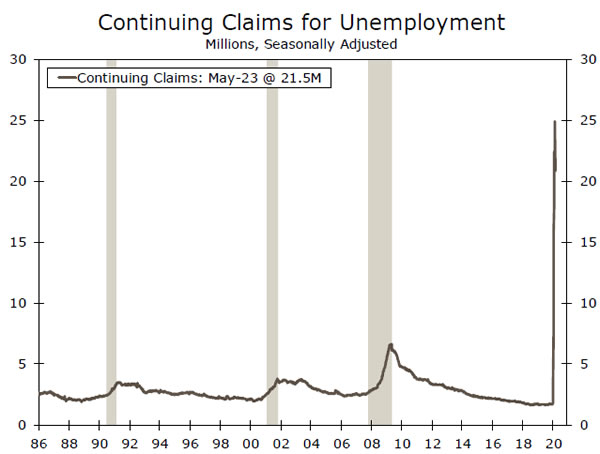

The May jobs report is an encouraging signal regarding the economic rebound. But, despite the better-than-expected outcome, it’s important not to overlook the fact that there were still 21 million people unemployed in May. The total level of employment is thus nearly 13% below its February pre-virus peak. This is relatively consistent with estimates of people continuing to file unemployment claims, which as of May 23, totaled 21.5 million Americans (plus an additional 10 million or so receiving PUA benefits). As workers get called back to work or begin to find new positions, this number will move lower, making continuing claims a key indicator to watch as we assess the extent of the rebound in the labor market.

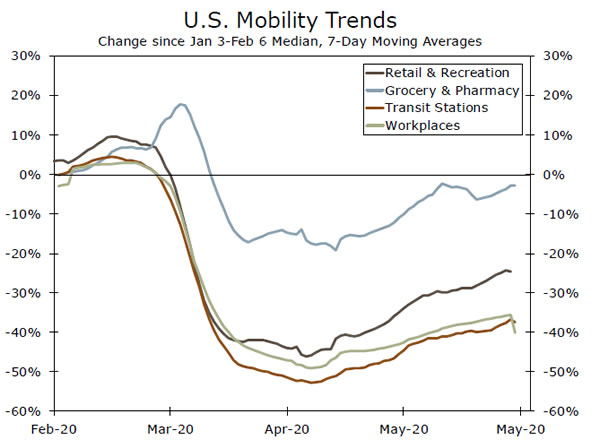

Outside the labor market, additional data this week continued to suggest the U.S. economy hit rock bottom in April. With states continuing to gradually re-open, high frequency mobility data have shown a decent uptick in movement, though levels remain wellbelow pre-virus norms. Further, the latest Institute for Supply Management (ISM) manufacturing and non-manufacturing indices suggested that while activity is still contracting, more firms reported a pick-up in activity relative to April. More plainly, change in activity was still bad in May, but less bad than in April. For more on the ISM indices, please see Topic of the Week on Page 7.

With activity still restrained, policymakers continue to adapt and adjust their tools as necessary. The Fed announced an expansion of its Municipal Liquidity Facility on Wednesday, now allowing every state to have at least two cities or counties eligible for the program no matter its population. It also now allows issuers such as public transit, airports, toll facilities and utilities to directly use the facility. Further, the Senate voted unanimously to loosen the rules for the Paycheck Protection Program, now allowing businesses 24 weeks to use the funds (up from eight weeks previously) and requiring only 60% of the loan (75% previously) be used for payroll to qualify for forgiveness. These policy actions should better assist the economy through the crisis.

Overall, economic activity should continue to pick-up as more states loosen lockdowns in coming weeks, meaning employment also looks set to continue to rebound. But, the resurgence of activity will likely be gradual and we do not expect the labor market to return anywhere near its pre-virus position for quite some time.

U.S. Outlook

NFIB • Tuesday

All things considered, the NFIB Small Business Optimism Index has held up relatively well. Two months into what on paper is a cataclysmic event, the headline index is still at levels seen in 2012 and 2013. After falling from 104.5 in February to 96.4 and 90.9 in March and April, consensus expects the index to rise to 92.0 in May. We will be watching hiring plans (the 21% of firms planning to increase staffing in February fell to just 1% in April) and selling prices (down to -18% in April from 11% expecting to raise prices in February).

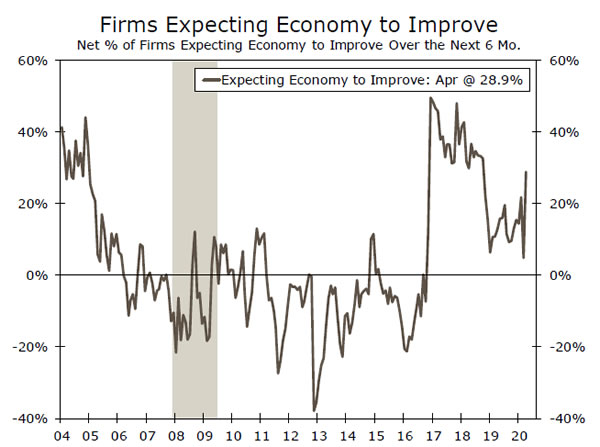

The index is holding up because owners are looking ahead to a better future—the net percentage of firms expecting the economy to improve over the next six months surged to 29% in April from 5%. This outcome is contingent on the PPP’s effectiveness as well as the virus not forcing another round of shutdowns. This also seems to be the outcome expected by the stock market, up 40% from its bottom.

Previous: 90.9 Consensus: 92.0

CPI • Wednesday

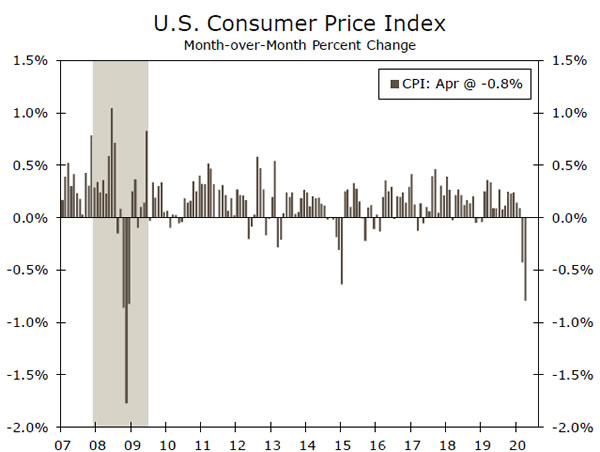

Inflation is difficult to measure in the best of times, but in March and April, it was difficult to even define conceptually. The CPI fell 0.8% in April, the largest deflationary reading since the Great Recession, but this is fairly misleading. The price index was dragged down by declines in the prices of gasoline (-21%), airfare (-15%), car rentals (-17%), hotels (-7%) and apparel (-5%). But these are all things that consumers, for the most part, were not consuming. Most of them couldn’t; there was nowhere to go. On the other hand, grocery prices rose 2.6%, rents rose 0.2% and medical care services prices rose 0.5%, meaning that experienced inflation was something different than what the BLS reported.

May will be affected by similar quirks. We expect the CPI remained unchanged on the month. Looking ahead, inflationary pressure will be muted as the economy struggles to close the output gap.

Previous: -0.8% Wells Fargo: 0.0% Consensus: 0.0% (Month-over-Month)

Initial Jobless Claims • Thursday

Over the past 11 weeks, 42.6 million initial jobless claims have been filed, meaning that nearly 28% of all people employed in February lost their job, at least temporarily. The 1.9 million reported the week ended May 30 was the ninth straight decline, but more than two months after America shutdown it remains staggeringly high. Most states have likely worked through technical backlogs, which means that layoffs have clearly spread well beyond the directly affected industries.

Last week, we were excited to see that continuing claims fell, indicating that gross hiring had picked up enough to pull down the number of people receiving benefits. There was no such consolation this week, as they rose again to 21.5 million. The numbers out of California are volatile, but even excluding the largest state, the continuing claims numbers are not really falling, despite most of the country now being “open” again.

Previous: 1.9M Consensus: 1.6M

Global Review

Trio of Central Bank Meetings Dominate the Week

- There was a trio of key central bank meetings this week, with the Reserve Bank of Australia (RBA) kicking the week off. As expected, the RBA maintained its main policy rate and target for the three-year sovereign bond yield.

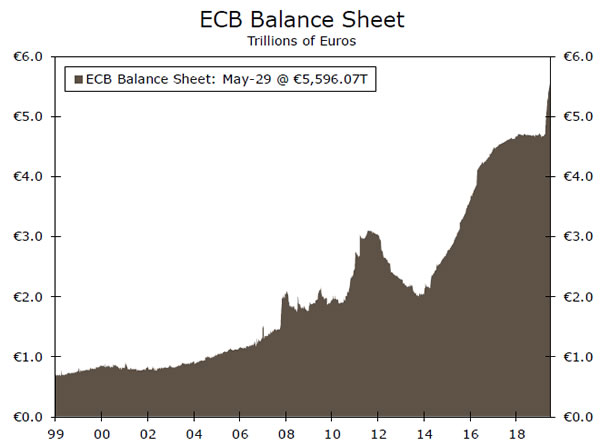

- The European Central Bank increased the Pandemic Emergency Purchase Program by €600 billion, extended the timeline for purchases to June 2021 and announced maturing holdings would be reinvested until at least the end of 2022.

- The Bank of Canada left its main policy rate unchanged and modestly scaled back some provisions aimed at providing liquidity in financial markets.

Trio of Central Bank Meetings Dominate the Week

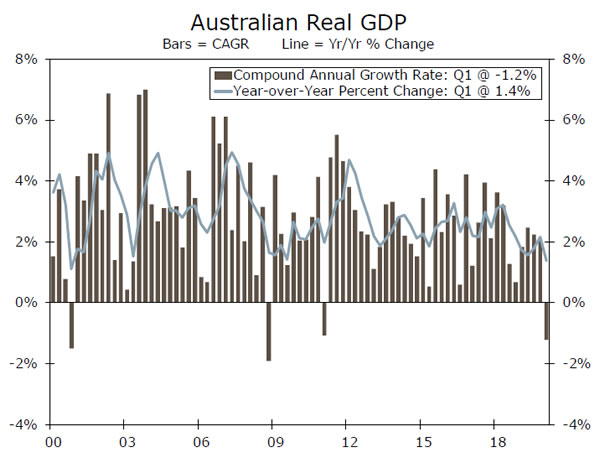

There was a trio of key central bank meetings this week, with the Reserve Bank of Australia (RBA) kicking the week off. As expected, the RBA left monetary policy unchanged, maintaining its main policy rate and target for the three-year sovereign bond yield. The statement noted that “it is possible that the depth of the downturn will be less than earlier expected” citing a significant decline in new infections and a lifting of some restrictions earlier than expected. Another source of upside risk for the Australian economy is the steadily improving economic outlook in China.

That said, better than expected in relative terms is likely to still be quite bad on an absolute basis. Q1 real GDP growth was -0.3% (not annualized) in Q1, and data released Wednesday showed retail sales declining 17.7% month-over-month in April. Total hours worked declined 9% in the month, and nearly 600,000 people lost their jobs. Barring a complete miracle turnaround in June, Australia is likely in its first recession since the early 1990s.

Unlike the RBA, the European Central Bank (ECB) did make a few changes to monetary policy at its meeting this week. Specifically, the ECB increased the Pandemic Emergency Purchase Program (PEPP) by €600 billion, raising the total size of the program to €1.35 trillion. The timeline for the PEPP was extended to June 2021 from December 2021, and maturing PEPP holdings would be reinvested until at least the end of 2022, and longer if necessary. This was a more dovish announcement than we expected, both in terms of the size of the expansion of the program and in the reinvestment guidance. Preliminary data for May suggest the Eurozone economy is starting to bounce back as re-openings across the region progress, but economic activity remains significantly depressed and remains a long way from normal.

Rounding out the week was the Bank of Canada, which left its main policy rate unchanged and modestly scaled back some provisions aimed at providing liquidity in financial markets. The BoC’s programs for purchasing federal, provincial and corporate debt remained at their previous frequency and scope. Like the RBA, the BoC noted in its statement that the Canadian economy appears to have avoided the most severe scenario presented in its April outlook.

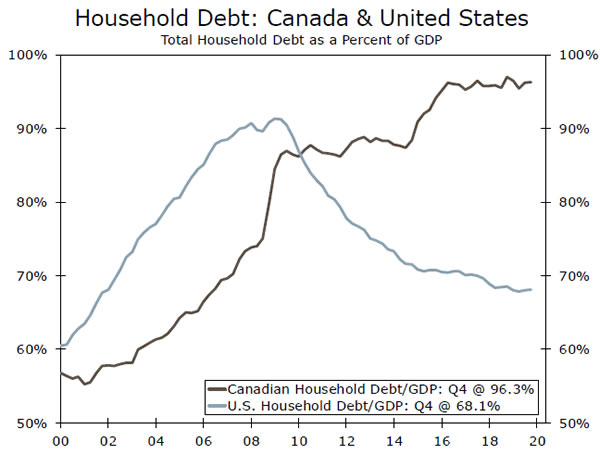

But also like the RBA, Canada’s economy continues to suffer from the double hit from measures adopted to fight COVID-19 and low commodity prices. After a 2.0 million decline in payrolls in April, the Canadian labor market saw an employment gain of 290,000 in May, according to data released this morning. Like the United States, the Canadian government has passed measures to support households that have lost income or stopped working due to COVID-19. Workers can receive a taxable benefit of $2,000 every four weeks for up to 16 weeks. But household debt levels are on average much higher in Canada than the United States, and a prolonged period of labor market weakness could lead to major challenges for the Canadian economy down the road.

Global Outlook

U.K. Monthly GDP • Friday

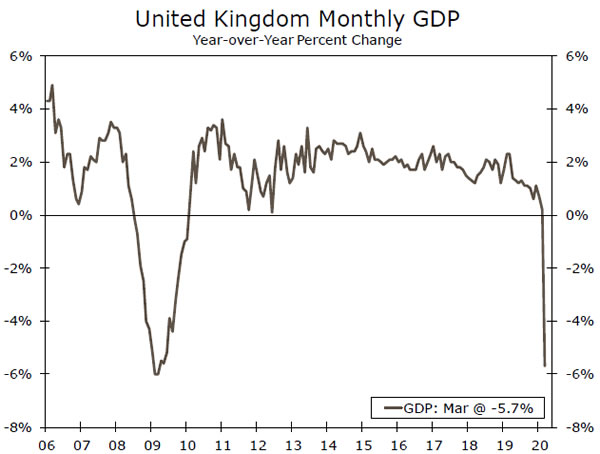

Monthly data on total output in the United Kingdom for March revealed a historic decline. The 5.8% month-over-month, unannualized decline in GDP pushed the year-over-year percent change to -5.7%, essentially on par with the trough during the Great Recession.

The hardest hit sectors in March were accommodation & food services, transportation & storage, education and arts, entertainment & recreation. An even bigger monthly decline is likely coming in April, as it was not until the second half of March that the United Kingdom’s nationwide lockdown fully went into effect. Retail sales excluding auto fuel declined 15.2% in April, nearly four times the decline that occurred in March. Having monthly data for April, which should be the low point of activity not just in the U.K. but in many other countries as well, will offer a good illustration of just how low the trough in output was.

Previous: -5.8% Consensus: -18.0% (Month-over-Month)

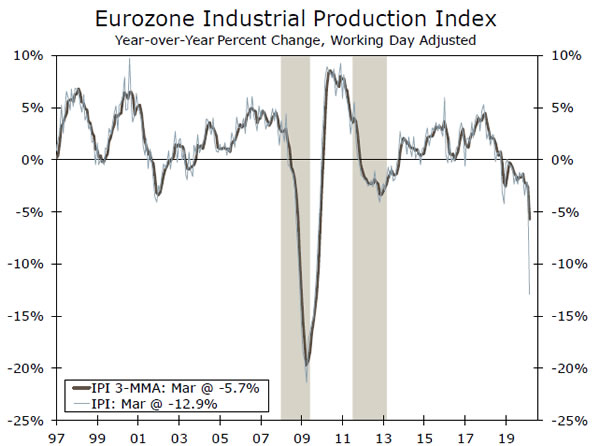

Eurozone Industrial Production • Friday

In March, Eurozone industrial production fell off a cliff, contracting 11.3%. Production of durable consumer goods saw the largest decline, falling 26.3%, even more than the 15.9% contraction in capital goods output. Among Member States for which data are available, the largest decreases in industrial production occurred in Luxembourg, Italy and Slovakia. The Bloomberg consensus looks for an even larger 20.0% month-over-month decline in April.

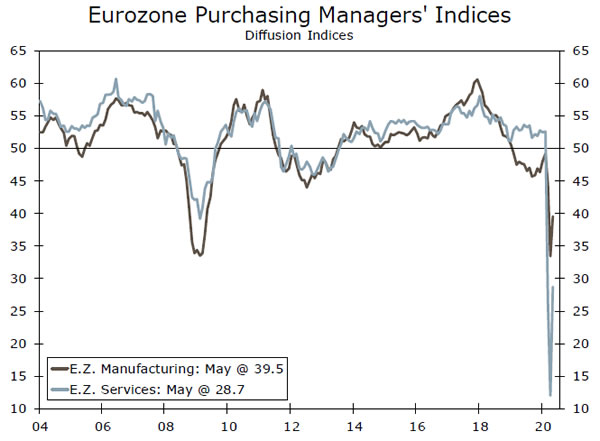

Encouragingly, the April print for industrial production should be the low point. The Eurozone PMI for manufacturing bottomed out at 33.4 in April, rising to 39.4 in May. In our view, the June manufacturing PMI, due out June 23, will be an especially important reading. Financial markets and analysts are well aware that April was a brutal month for economic output around the world, and that directionally activity should improve from there. The pace of that improvement, however, remains the key question to be answered.

Previous: -12.9% Consensus: -28.3% (Year-over-Year)

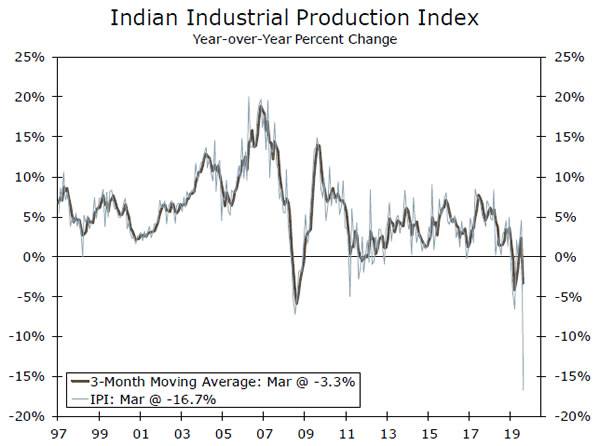

India Industrial Production • Friday

India has been one of the world’s fastest growing economies over the past decade, but even its high-flying economy cannot escape the damage done by COVID-19. On March 24, the government of India ordered a nationwide lockdown be put in place, and only recently has the country begun to relax the restrictions.

Industrial production growth collapsed in March, falling to -16.7% year-over-year, and other data have been equally as disastrous. The IHS Markit composite PMI for April was a stunning 7.2, down from 50.6 the previous month, in large part due to a 5.4 reading for the services component. The manufacturing PMI was better at 27.4, but still fell from 51.8 in March. Thus, no different than the Eurozone or other major economies, April is likely to see an even larger decline in industrial output. Such weak growth during a global recession is unusual for fast-growing emerging market economies like India and contributes to our forecast for a historic contraction in global GDP in 2020.

Previous: -16.7% Consensus: -47.5% (Year-over-Year)

Point of View

Interest Rate Watch

Bond Investors Sniff Out a Recovery

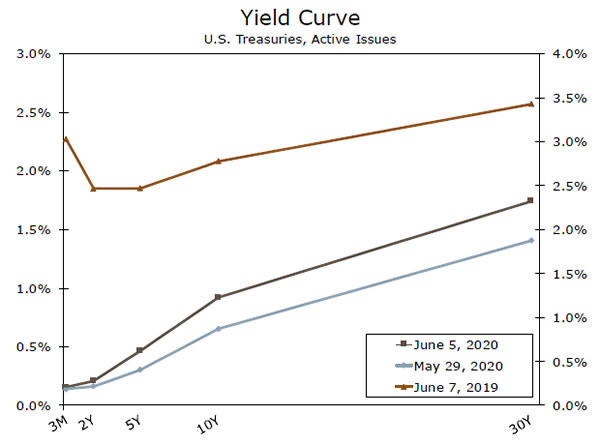

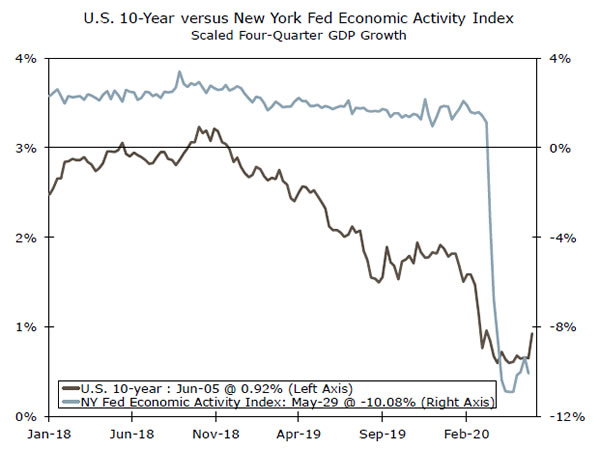

Despite this morning’s still atrocious employment figures, the financial markets appear to have picked up the scent of an economic recovery. Most of the official economic data reflect the period from at least a month ago. The May employment data, for example, tell us what transpired from mid-April to mid-May. State economies began to re-open in late May, and high frequency data on individual mobility from Apple and Google, hours worked from Homebase, and restaurant dining and even air travel from OpenTable and the TSA all show modest improvement. An economic awakening is clearly underway and there is very good chance the bottom has already been put in.

The anticipation of improving economic data over the next six months has pulled bond yields higher and steepened the yield curve. Equities have also rallied, even in the face of the street unrest throughout much of the country, as the George Floyd tragedy has displaced COVID-19 from the headlines.

While news about possible vaccines remain promising, there are still a number of unknowns regarding the virus and the economic outlook. On an optimistic note, nothing was broken in the U.S. economy prior to the COVID-19 outbreak. Moreover, unusually quick and well-targeted policy moves by the Fed, Congress and the Trump administration appear to have prevented the health care crisis from becoming a financial crisis or systemic economic crisis. That said, there is still a great deal of uncertainty about whether the U.S., Asia and Europe will see a second wave of the virus. Trade relationships have also been disrupted and COVID-19 has spread disturbingly to the developing world, particularly Brazil and India, presenting a continuing threat to supply chains.

This is certainly not the first time the markets climbed a wall of worry. The financial markets are forward-looking and reflect expectations for better economic times. Our sense is some of the recent enthusiasm in the stock market and rise in rates may prove to be too much too soon. The road to recovery will likely have plenty of twists and turns along the way.

Credit Market Insights

Consumer Credit & the COVID Crisis

With millions of Americans losing their job over the past couple of months, a wave of household delinquencies appeared to be on the horizon. Thus far, there have been signs of strained consumer balance sheets, but not quite as many defaults as many anticipated. Part of this may be due to the fact that it takes time for missed payments to be counted, particularly in official aggregates. In the NY Fed’s Q1 Household Debt & Credit Report, the authors noted that “it is not surprising that there are few signs of the COVID-19 pandemic in these data,” because missed payments aren’t recorded as delinquencies until a full statement period has passed. More recent reports from private companies & advocacy groups suggest some consumers have had difficulties making payments. In its April industry report, TransUnion reported increases in the percent of accounts in hardship (e.g., affected by disaster, in forbearance, etc.) across loan categories, but showed declines in the delinquency rates for most loan types. Meanwhile, the percentage of individuals making rent payments fell in April, before increasing to 93.3% in May, according to the NMHC’s rent tracker.

While many households are facing a shakier financial foundation after COVID-19, the deterioration has not been as dramatic as feared. Stimulus checks and increased UI benefits have certainly played a large role in this, but whether these programs are extended and whether delinquent balances will increase with passing months remains to be seen.

Topic of the Week

If a Virus Rebound Is Out, the Bottom Is In

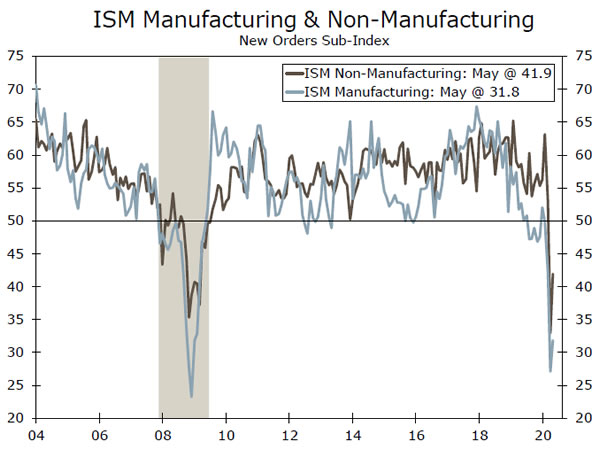

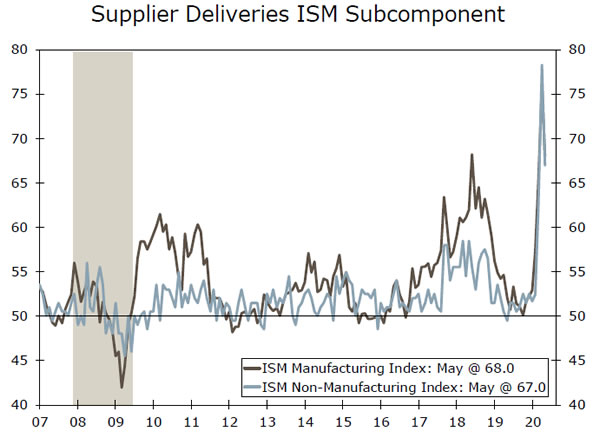

The ISM surveys this week both told a similar story: activity was still declining in May but not as much as it was in April. If the U.S. economy can successfully re-open without a re-emergence of the virus, the bottom in many measures of economic activity are now in. That is not to say that things will be easy from here; far from it. But, conditions are no longer getting worse.

The performance of the various subcomponents in both the manufacturing and the service sector ISMs were slightly more encouraging. This is most evident in the case of supplier deliveries. This measure fell in both reports. Had that not been the case, the headline improvement in May would have been even larger. The idea with measuring supplier deliveries is that the longer a business has to wait to get the parts and components it needs (in normal times), the better the economy is likely doing. Occasionally, supply-chain disruptions can result in this component rising even in the absence of brisk demand. That has been the case in recent months: a counterweight that has saved the headline ISM number from even steeper declines.

Another less-sanguine takeaway from the still-high readings for supplier deliveries is that businesses across the spectrum are still having a difficult time getting the supplies they need. That is as true for manufacturers who are having trouble sourcing the input components they need as it is for retail shops getting in-demand merchandise on the shelves.

Employment increased only modestly in both measures, certainly not anything that would have justified today’s blowout jobs number for May.

While activity restarts amid a pickup in services demand, a complete rebound in the services sector may be slower to gain momentum. In our view, the manufacturing sector may face longer lags still due to both supply chain disruption and worries about global growth. The virus impact is beginning to wane here, but it is still growing globally.

{kind=link}