U.S. Review

A Glimpse of the Rebound that Might Have Been

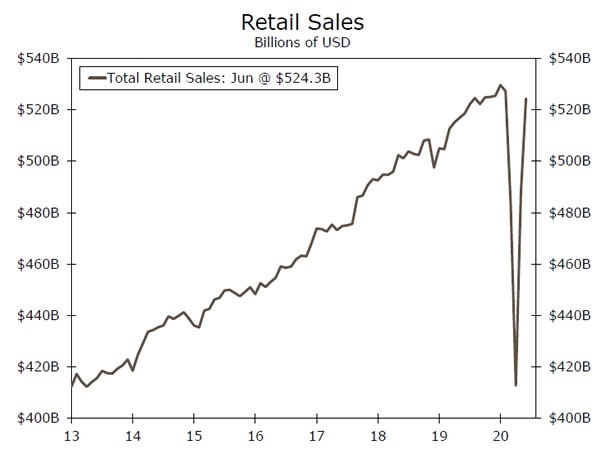

- Two countervailing themes competed for attention this week in financial markets. The first is that for the most part, economic data continue to surprise to the upside and do not yet rule out prospects for that elusive V-shaped recovery. The chart to the right plotting the level of retail sales offers a great example: that is about as close to a V as you get.

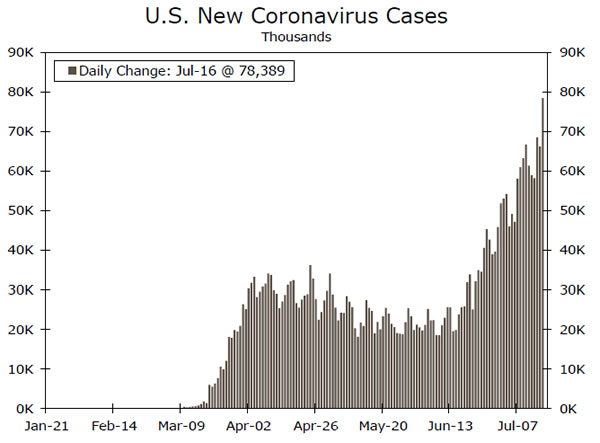

- But the recovery is in jeopardy of being held back by the very thing that got us into this mess to begin with. Coronavirus infections continue to mount and even hit a single-day record north of 78K on Thursday, as officials and businesses are increasingly requiring residents and customers to wear masks to help stop the spread.

Just When Small Business Confidence Was Coming Back

The NFIB Small Business Optimism Index jumped 6.2 points to 100.6 in June, as business re-openings bolstered expectations and hiring. The rebound in Small Business Optimism is heartening, but we fear it may be a bit premature. The survey likely came too early to reflect the sustained rise in new COVID-19 cases, which have now elicited a new round of shutdowns.

The daily increase in new cases reported in the United States on Thursday was a record 78,389. While part of the increase may be a function of increased testing, the positivity rate was 8.5%, up from 4.3% earlier in June. So it is partly increased testing but almost twice as many people that are getting tested are walking away with a positive diagnosis.

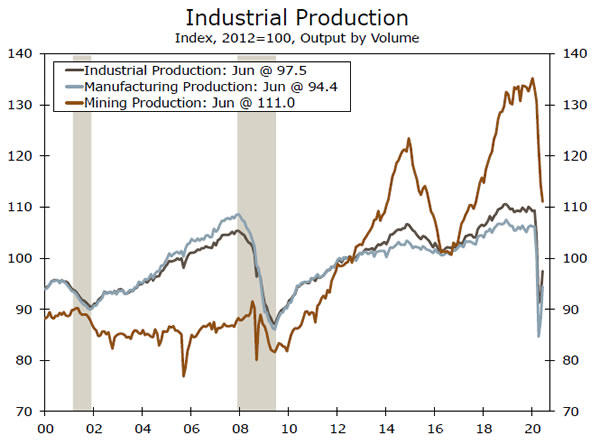

A Sharp Turnaround Was Never in the Cards for IP

As more of the nation’s factories re-opened in June, manufacturing production grew 7.2%. Auto & parts production posted another significant bounce (up 105%), as consumers began to return to dealer lots. However, the rebound extended more broadly beyond the auto sector compared to May, with production in every major manufacturing industry up in June. Despite that, manufacturing output is still down 11% since January.

Overall industrial production (IP) rose a more modest 5.4%, as low oil prices continue to weigh on energy extraction. Mining, which accounts for about 15% of IP, fell 2.9%. That rate of decline, however, is smaller than May, as demand for oil and therefore prices have firmed up a bit as the economy has re-opened.

V-Shaped Recovery in Retail Sales

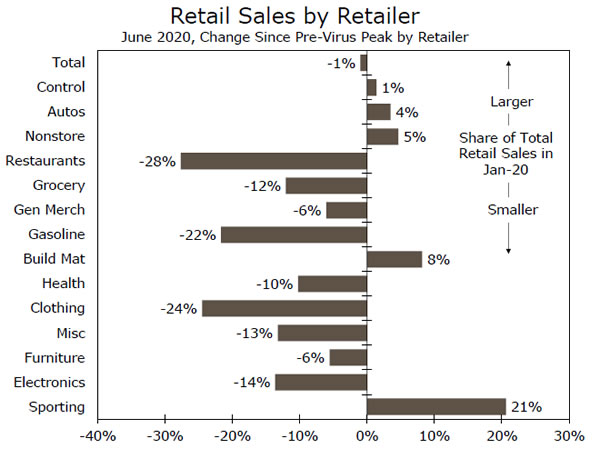

The June retail sales report was much better than expected. The 7.5% surge in June handily exceeded expectations and lifts the overall level of retail sales to within striking distance of its prerecession peak. Clothing stores (+105.1%), auto sales (+8.2%) and restaurants (+20.0%) accounted for most of the gain. Sporting goods stores added another 26.5% in June lifting this category to a level that is more than 20% above its pre-recession peak.

The June report leaves total retail sales just 1.0% off its pre-virus peak, and control group 1.4% above its peak. Were it not for the virus rebound, retail sales would be poised for a full recovery.

This report could be the best example this week of the recovery that might have been. That is not to say that sales are doomed to fall, but it is fair to say the rebound could be fleeting as the country struggles with a reacceleration in case growth that might force new closures. The months ahead may not be so smooth for the retail outlook. While May and June figures benefited from low-base effects as well as a gradual loosening of stay-at-home orders in many parts of the country, July will not have the same wind in its sails. The “easy gains” that were made possible from sharply curtailed spending have already been realized. Going back to square one with a widespread shutdown is not likely for a lot of reasons, but simply slow-walking the re-opening process will result in a less robust rebound not just in consumer spending but for other parts of the economy as well.

U.S. Outlook

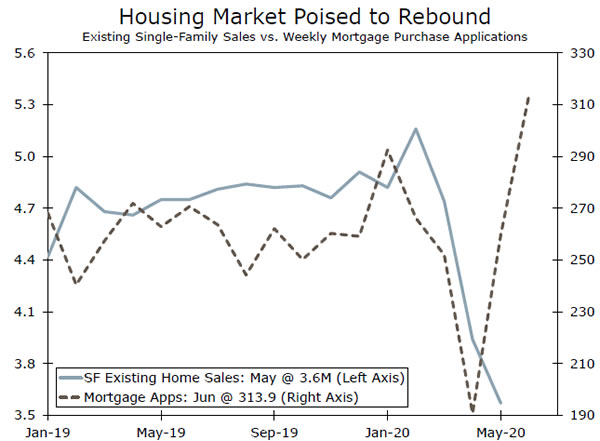

Existing Home Sales • Wednesday

Although much of the country was still in lockdown in May, we expect a solid rebound in existing home sales for June. Pending home sales, which lead existing sales by a month or two, surged 44% in May. In addition, mortgage applications for home purchases increased to their highest level in 11 years last month. New home sales, which will be released on Friday, are also expected to have gained back some ground in June.

As pent up demand following this Spring’s stay-at-home orders is released, we would expect further gains in sales to be more incremental in the coming months. That said, record-low interest rates and a job market that has been less severe on older workers, who are more likely to be buyers, suggest that the housing market should remain a relative bright spot in the economy.

Previous: 3.91M Wells Fargo: 4.83M Consensus: 4.75M

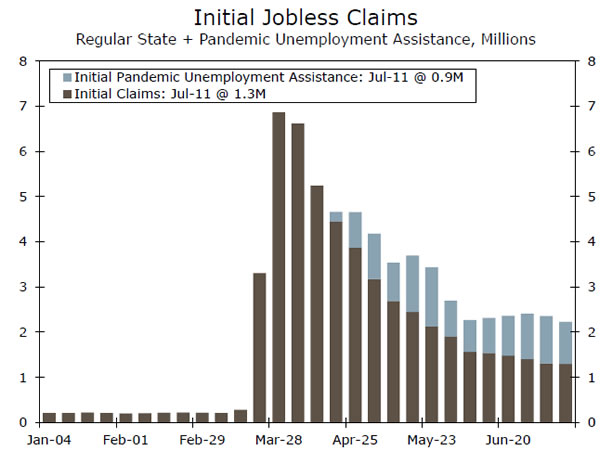

Initial Jobless Claims • Thursday

Initial jobless claims were little changed the week ending July 11, but remain staggeringly high at 1.30 million. More encouraging was the drop in initial claims under the Pandemic Unemployment Assistance program, which covers self-employed workers, independent contractors and gig workers. For the week ending July 4, the total number of workers receiving benefits under regular state unemployment programs fell 422K, but at 17.3 million, underscores the pervasive weakness in the labor market.

Next week’s claims figures will give a timely indication of the extent to which the labor market’s recovery may be faltering. As more states and localities have back-tracked on re-openings or capacity of some businesses, an uptick in layoffs may be in store.

Previous: 1.30M Consensus: 1.28M

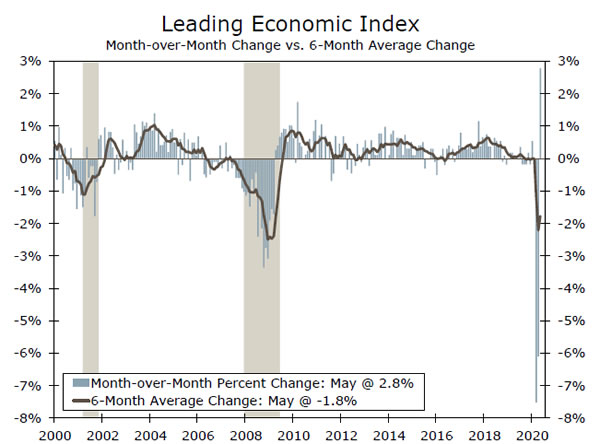

Leading Economic Index • Friday

The Leading Economic Index (LEI) may seem a bit dated these days with daily reports on routing requests, TSA passenger screenings and Open Table reservations closely watched. That said, it continues to offer a succinct look at how businesses, households and financial market participants are eying the future. In May, the 2.8% increase in the LEI confirmed that economic activity began to recover. We expect to see another gain in June. New orders for manufacturers jumped in June, as did consumers’ expectations of the economy. Meanwhile, stock prices continued to climb and initial claims trudged lower.

While a number of the traditional forward-looking indicators point to activity having picked up through June, we expect to see more moderate advances in the near term following the reacceleration in case growth, the reversal of some re-openings and consumers staying home a bit more in recent weeks.

Previous: 2.8% Wells Fargo: 2.1% Consensus: 2.4%

Global Review

Central Banks on Hold; China Data Somewhat Mixed

- The European Central Bank and Bank of Canada both met this week. As expected, no major policy changes were made and both central banks remain committed to keep interest rates low and asset purchases in place for the time being.

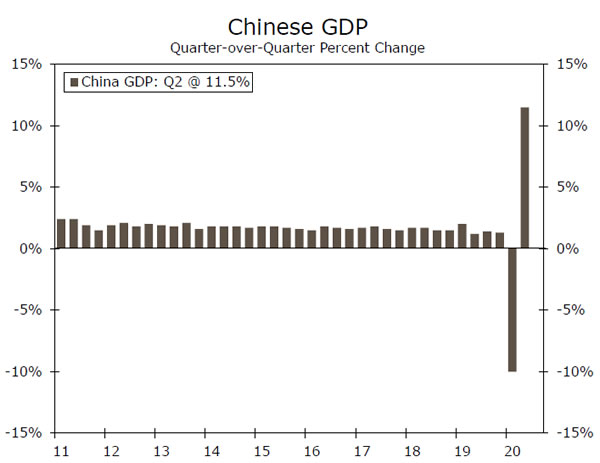

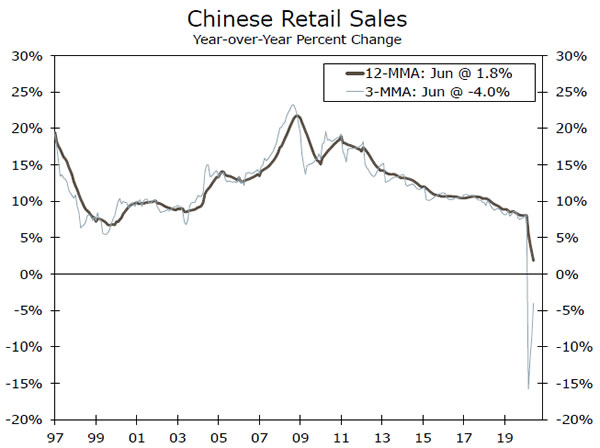

- China GDP data beat expectations, signaling the recovery in the world’s second-largest economy is gathering momentum. While the Q2 headline GDP print was stellar, June retail sales missed consensus expectations and may be calling into question the strength of the recovery as we head into the second half of the year.

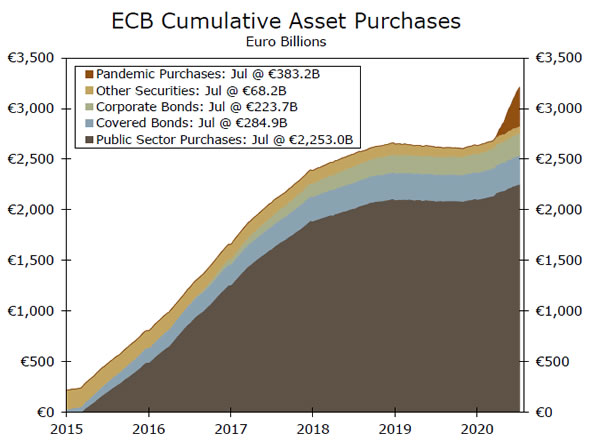

ECB Keeps Policy Steady

The European Central Bank (ECB) met on Thursday, but policymakers announced no major shifts in monetary policy. Instead, ECB policymakers opted to keep interest rates unchanged. ECB President Christine Lagarde indicated that policymakers will not allow monetary policy to be constrained, as the central bank seeks to support the Eurozone economy in the wake of the COVID- 19 crisis. The ECB statement also mentioned the ECB’s pandemic emergency purchase program (PEPP) will remain in place until at least June 2021 and it will continue to reinvest any maturing securities until at least the end of 2022. As far as the quantitative easing program, Lagarde explicitly mentioned the central bank will purchase assets totaling the initial target of €1,350B and the pace of purchasing assets each month will remain constant at €20B. Perhaps more important were Lagarde’s comments on a potential coordinated fiscal response across all Eurozone countries. She continued to stress the importance of an EU recovery fund. We believe progress will be made toward a formal approval of additional EU fiscal stimulus.

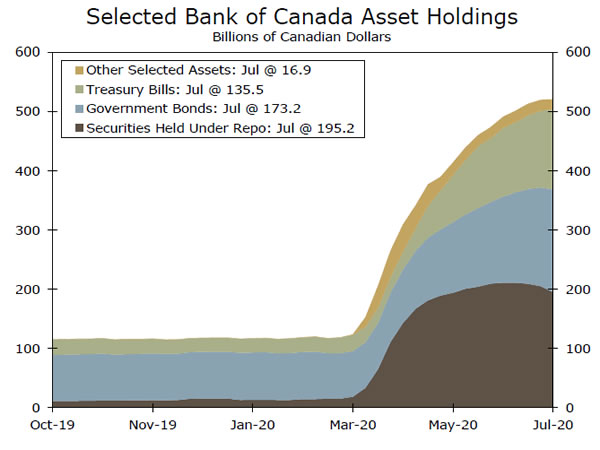

No Changes From the Bank of Canada

Similar to the ECB, the Bank of Canada (BoC) chose to make no significant changes at its meeting this week. Amid the COVID-19 led slowdown in the domestic economy, the BoC cut its overnight rate to 0.25% and has signaled it plans to keep rates at this level for the time being. In fact, the BoC suggested rate hikes would not be considered until at least 2023 or until unemployment fell back to pre-pandemic levels and inflation returned to the central banks 2% target. The Bank of Canada has also embarked on a quantitative easing program, the first in its history, and has remained committed to purchasing C$5B of government bonds per week. In addition, the BoC provided forward guidance that asset purchases would continue until the economic recovery is “well underway.” As of our latest forecasts, we expect the Canadian economy to contract around 8% this year, so asset purchases and low interest rates are certainly required in an effort to combat the economic effects from COVID-19.

China GDP Beats Expectations, but Risks Remain

Late Thursday night, China released Q2 GDP data with the headline figures beating consensus estimates, and providing optimism that the economic recovery in China is underway. GDP expanded 11.5% quarter-over-quarter in Q2, beating our forecast of 9.5%, while some other indicators such as industrial production and fixed-asset investment also firmed more than expected. China’s data releases were mostly positive, although June retail sales were slightly less stellar and could be an indication of the slowing momentum. June retail sales missed expectations and contracted 1.8% year-over-year against consensus expectations for an increase of 0.5%. Despite the miss relative to consensus, we remain constructive on the outlook for the Chinese economy. As of now, we forecast the economy to expand around 1% this year; however, we will be focused on additional data releases in the coming weeks to gauge the strength of the recovery. In addition, tensions with the United States could play a role in the recovery, and we will pay attention to any new escalations.

Global Outlook

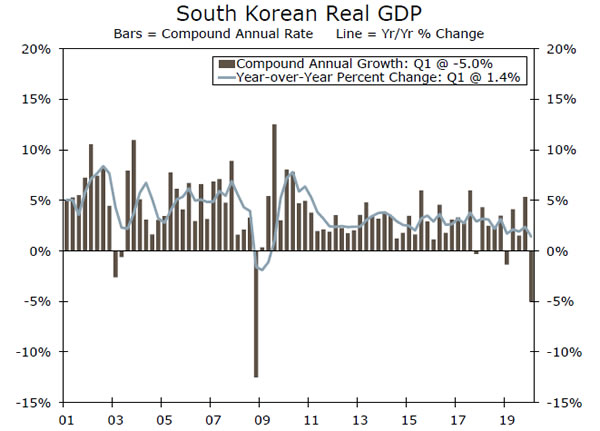

South Korea GDP • Wednesday

South Korea is one of the first countries to release its Q2 GDP data. We expect the economic contraction to be quite severe. For most of the second quarter, Korea had strict lockdown and social distancing measures in place to contain the spread of COVID-19. Over time, lockdowns have mostly been lifted and mobility throughout the country has returned back to pre-virus levels. However, Korea’s economy is highly dependent on exporters, and given the subdued nature of the global economy, demand for Korean goods and services likely collapsed. This week, we saw Singapore, another Asian country reliant on exports, experience a historic contraction in its second quarter GDP. While Korea’s data may be slightly better than Singapore, we expect a pretty sharp decline, which should lead to an annual contraction in Korea’s economy. We expect the global recovery to get underway in Q3, which should help the economy rebound going forward.

Previous: -1.3% (Quarter-over-Quarter) Consensus: -2.3%

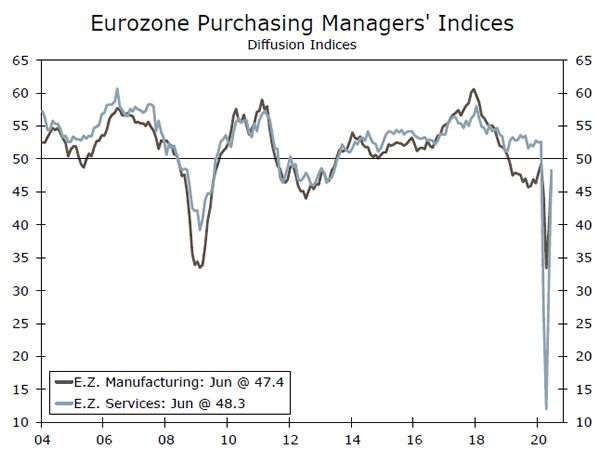

Eurozone PMIs • Friday

Over the past month or so, there have been indications that the worst of the COVID-19 slowdown could be behind the Eurozone. We will get further evidence of how the recovery is materializing next week with the manufacturing and services PMI releases. PMI data have rebounded quite well off their lows in April; however, they remain below the 50 level indicating they are still in contraction territory. As lockdown measures gradually get lifted and the spread of COVID-19 continues to be contained, we believe there are compelling reasons the Eurozone economy will continue to recover and sentiment data could improve further. In addition, we believe additional fiscal stimulus is likely to be deployed across the Eurozone, which would further support the economic recovery going forward. We have become less pessimistic on the Eurozone as data improve and now believe the economy is set to contract a little more than 7.5% this year.

Previous: 47.4 (Manufacturing) ; 48.3 (Services) Consensus: 50.0; 51.0

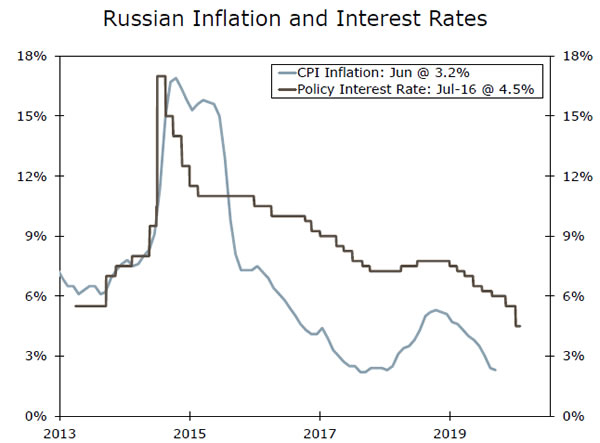

Russia Monetary Policy • Friday

Toward the end of next week the Central Bank of Russia will meet to determine monetary policy. In all likelihood, Russian policymakers will move forward with another cut to its main policy rate, the question becomes by how much. Consensus estimates expect a 25 bps rate cut; however, the risks are skewed toward more easing. CPI inflation has ticked higher, but remains well below the central bank’s 4.00% target, while oil prices remain subdued and the currency has stabilized for the time being. In our view, we believe the central bank has adequate policy space to cut more aggressively if it chooses to without causing a major disruption to the currency. Looking past next week’s meeting, we also believe it is likely the central bank sticks with its easing cycle for the rest of the year and continues to cut interest rates. Until inflation picks up meaningfully and the local economy shows signs of recovery, post-COVID monetary policy is likely to remain quite easy.

Previous: 4.50% Consensus: 4.25%

Point of View

Interest Rate Watch

Central Banks on Hold, for Now

As we discussed in more detail on Page 4, there were policy meetings this week at the European Central Bank (ECB) and the Bank of Canada (BoC). To nobody’s surprise, both central banks did not make any substantive changes to their respective policy stances. That said, both central banks indicated that they are prepared to provide further accommodation, if needed. The next policy meeting is scheduled for September 9 at the BoC and September 10 at the ECB.

The Federal Open Market Committee (FOMC) will meet on July 29, and we expect that the committee will maintain its target range for the fed funds rate at 0.00% to 0.25%. That said, the FOMC could potentially adopt some other stimulative measures. We will discuss the different policy options facing the FOMC in our next “Fed Flashlight Report,” which we intend to publish next week.

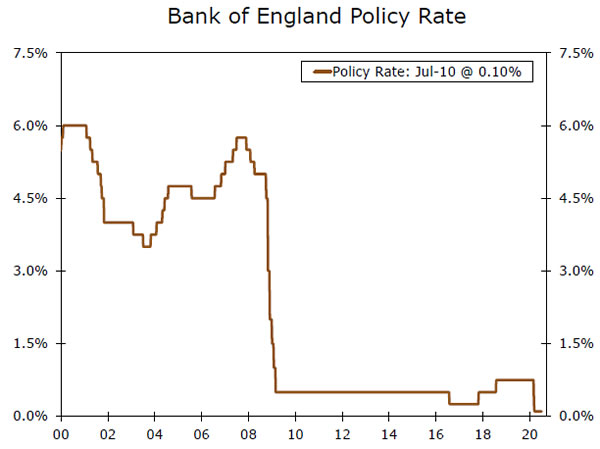

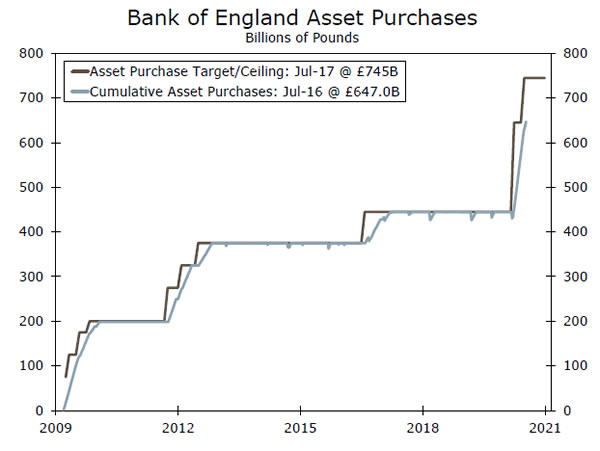

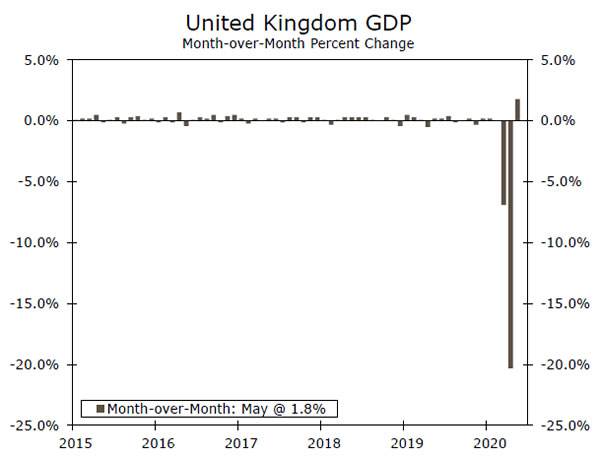

The Bank of England (BoE) will hold its next policy meeting on August 6. The Monetary Policy Committee cut its Bank Rate to 0.10% in March (top chart), and the present setting is probably as low as the MPC is willing to take it. However, the MPC has other tools at its disposal. Specifically, the BoE, like many other central banks, has engaged in quantitative easing purchases of assets. Prior to March, the BoE held £375 billion worth of assets, mostly U.K. government bonds, on its balance sheet (middle chart). Over the past few months, the MPC has raised the target amount of asset holdings to £745 billion, and the BoE is well on its way to reaching that target.

The U.K. economy has been hit hard by the pandemic. The economy contracted 2.2% (not annualized) in the first quarter, and we estimate that real GDP nosedived roughly 15% in Q2. This estimate seems reasonable in light of data that were released this week showing that GDP rose only 1.8% in May following the plunge of 20.3% in April (bottom chart).

Given the current weakness in the economy and uncertainties related to Brexit, which could restrain growth later this year, we look for the BoE to increase the target for its asset holdings by another £100 billion in the fourth quarter of this year.

Credit Market Insights

Delinquency: Sign of Slippage

The housing market has remained a bright spot during the COVID-19 crisis, but recently released delinquency data indicate the first sign of possible slippage. According to the CoreLogic Loan Performance Insights Report, the overall mortgage delinquency rate rose to 6.1% in April, which is the highest rate since 2016. The 2.5 percentage point (pp) gain from March broke a two-and-a-half year streak of declines.

The largest increases were in early-stage delinquencies. The share of mortgages that went from current to 30 days past due increased to 3.4% in April. For perspective, this is the highest reading in more than 20 years, comfortably surpassing the previous 2% peak in Nov-2008. The share of mortgages that were 30-59 days past due rose 2.5 pp compared to a year-earlier. While things appear to be deteriorating, more serious measures of delinquency remained low. The share of mortgages that are 90 days or more past due remained at its lowest since 2000, and the share of mortgages in some stage of foreclosure, was the lowest in more than 20 years.

Despite record job loss, households have largely been made whole in recent months by increased unemployment benefits. With some benefits set to expire at the end of July, households may fall under pressure to meet mortgage payments, potentially leading to further increases in delinquencies. Mortgage rates, however, continue to slide lower—the 30-year fixed rate fell to a record low this week—suggesting purchase and refinancing demand may continue to rise. We will monitor delinquencies in the months ahead.

Topic of the Week

The 2020 Election: A Summer Update

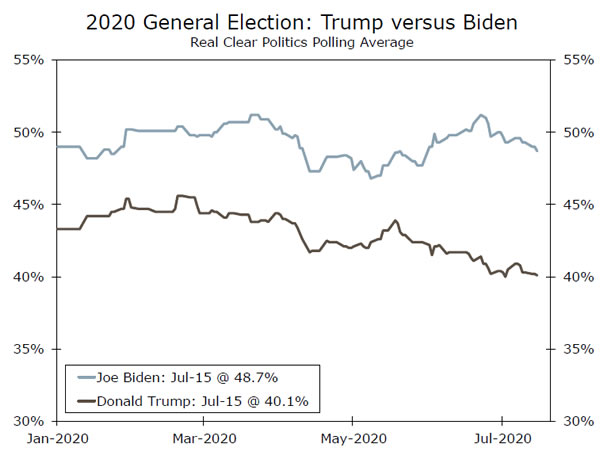

The 2020 U.S. Presidential election is scheduled for November 3, and there are some key dates on the horizon that signal the heart of campaign season will soon be upon us. At present, Joe Biden has a sizable lead in the national polls (top chart), nearly three times bigger than the lead Hillary Clinton had in mid-July 2016. Polling at the Congressional level looks equally as robust for the Democrats. But how much can we really trust the polls? Weren’t the polls wildly off in 2016?

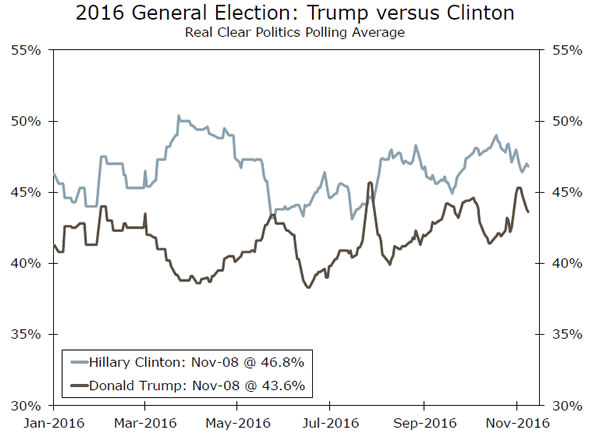

To some extent, the surprise election of Donald Trump in 2016 was the result of polling issues. But in speaking with clients, we have come to believe that some financial market participants tend to overweight the role played by polling errors. At the national level, the Real Clear Politics (RCP) polling average was actually more accurate in 2016 than it had been in the previous few elections.

So what happened? One major factor was that in the final few weeks Donald Trump made up ground (bottom chart). Exit polls provide additional evidence that President Trump performed well among late deciding voters. Additionally, there were more polling issues at the state level, particularly in Wisconsin and Michigan, which had not gone for a Republican presidential candidate since the 1980s. In the four states Trump won by the smallest margins, the RCP polling average understated Trump’s support by an average of 3.7 percentage points. But at present, Biden’s lead in those states ranges from +5.2 in Florida to +7.5 in Michigan.

If the election were held today, we suspect Joe Biden would rightly be considered a healthy favorite going into the vote tally. But elections are fluid, with twists and turns and inflection points even in normal times. In 2020, with a historic pandemic raging and significant uncertainty about what the world will look like come November, we believe it is even more important to remain attentive to changes in the election landscape.

{kind=link}