The Federal Reserve will be meeting for the first time since yields exploded higher and the Biden stimulus bill became law. The Bank of England and Bank of Japan will announce their decisions too. Will the Fed and other central banks take their cues from the European Central Bank and respond to the bond market selloff by stepping up their purchases? The debate about whether higher yields warrant fresh policy action will likely dominate the market conversation, especially as there’s nothing terribly exciting on the data front. Nevertheless, key indicators out of Australia, New Zealand and the United States will be watched in the coming days.

Fed to kick off trio of central bank meetings

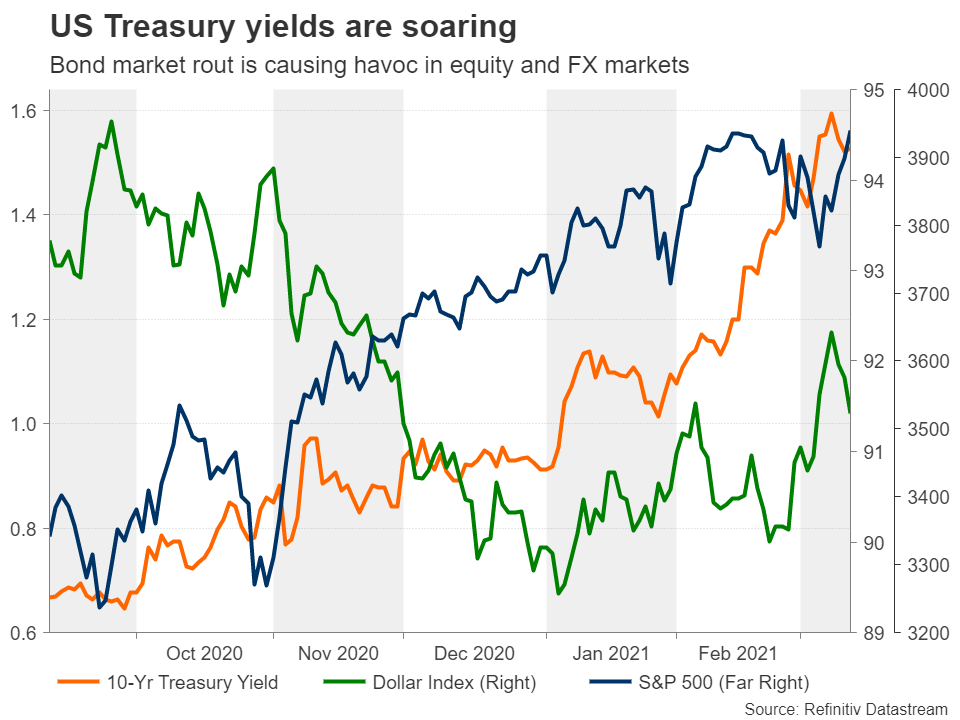

It’s FOMC week and the world will be watching what the Fed’s response will be to the spiked volatility in bond markets that’s upset tech stocks and revived the US dollar. If one is to go by Chair Jerome Powell’s last remarks, those investors hoping for new policy measures shouldn’t hold their breath. Powell has indicated he would be concerned by a persistent tightening in financial conditions but that there’s nothing too disorderly in financial markets at the moment.

Healthy demand for the latest Treasury auctions and tame inflation numbers have helped steady bond markets over the past week, making it even less likely the Fed will see a need for fresh action at its March 16-17 meeting. However, that’s not to say there won’t be any market moving headlines as the Fed will be publishing its updated dot plot chart and Powell will for sure be quizzed about yields in his press briefing on Wednesday. Given how sensitive markets have become to the fluctuations in Treasury yields, even the slightest suggestion by Powell that FOMC members discussed changing the composition of their asset purchases could be enough to cause a storm. Similarly, if Powell doesn’t go far enough in explaining where the Fed stands on rising yields, there could be another tantrum.

On balance, though, the key takeaway from the Fed meeting will be whether there is enough concern at this point to switch bond purchases towards longer-dated Treasuries. Ahead of the meeting, investors will be gazing at the February retail sales figures on Tuesday and building permits and housing starts on Wednesday. The New York and Philadelphia Feds’ manufacturing gauges on Monday and Thursday, respectively, might attract some attention too.

With the dollar retreating from its March highs in recent sessions and Wall Street rebounding from its dip to set fresh records, it will be interesting to see which way Powell will tilt sentiment.

Bank of England to reaffirm guidance

Like in the US, 10-year UK gilts have seen the biggest increase among major economies, fuelling the pound higher. The Bank of England has so far followed a similar stance to the Fed in interpreting the jump in yields as a natural response to a healthier economic outlook on the back of the UK’s rapid vaccination campaign.

However, with UK government borrowing set to soar further in 2021 and a full reopening of the economy still being months away, the BoE can’t afford to let long-term borrowing costs rise too sharply, which tend to tighten financial conditions. Hence, policymakers may attempt to keep a lid on the surge in yields on Thursday by re-emphasizing their forward guidance and keep the option of negative rates firmly on the table.

If the Bank goes as far as suggesting that investors are overly optimistic about the expected rate path that shows rising odds of a rate hike in 2022, sterling could suffer a knock back, particularly against the dollar. However, should policymakers simply maintain cautious optimism, this would give traders the perfect excuse to resume buying the pound and selling long-term gilts.

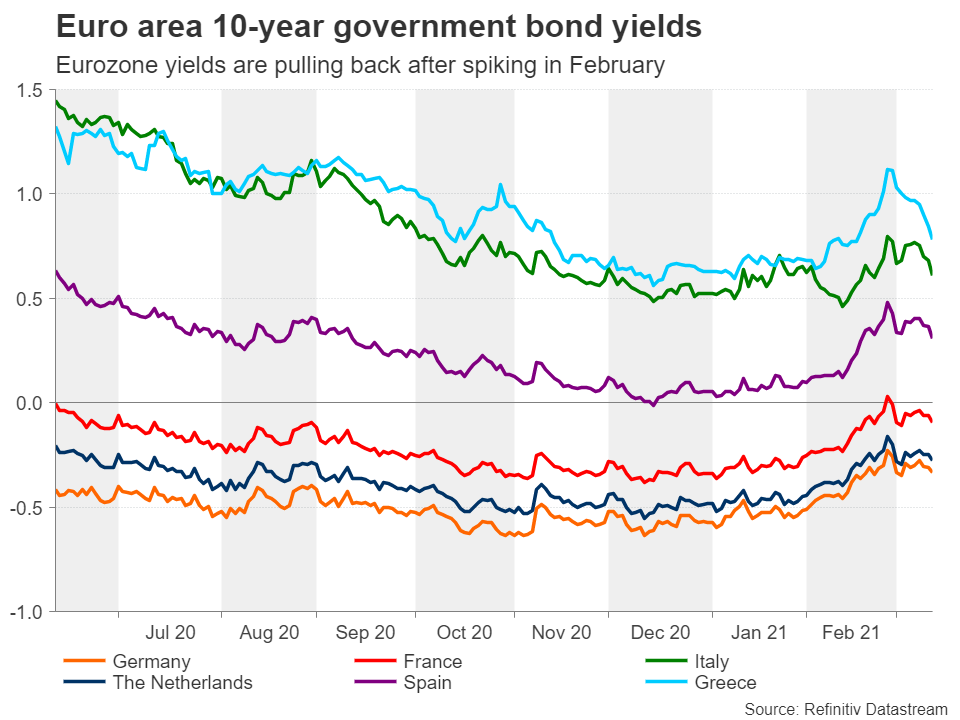

Euro lifted by ECB’s surprise, next test is the Fed

The ECB took markets by surprise when it announced at its March meeting that it plans to “significantly” accelerate its bond purchases over the next quarter. But while the decision was met by a notable drop in Eurozone sovereign bond yields, the euro edged higher. Expectations that the ramped-up purchases would boost growth in the region is one reason why the single currency went in the opposite direction. But the main explanation is that the euro was being led by a weaker dollar. The fact is the ECB had been making fewer purchases in the first quarter and so the significance of the decision isn’t so great when viewing it in this context.

Looking ahead, the only worthy releases in the next seven days are Germany’s ZEW economic sentiment survey on Tuesday and the final Eurozone CPI estimate on Wednesday, none of which are anticipated to provide much direction to the single currency. This leaves the euro fully exposed to the outcome of the Fed meeting. Should the Fed successfully dampen tapering fears, pushing Treasury yields lower, the euro would be in a strong position to extend its rebound from 3-month lows to above the key $1.20 level.

Bank of Japan’s policy review in focus

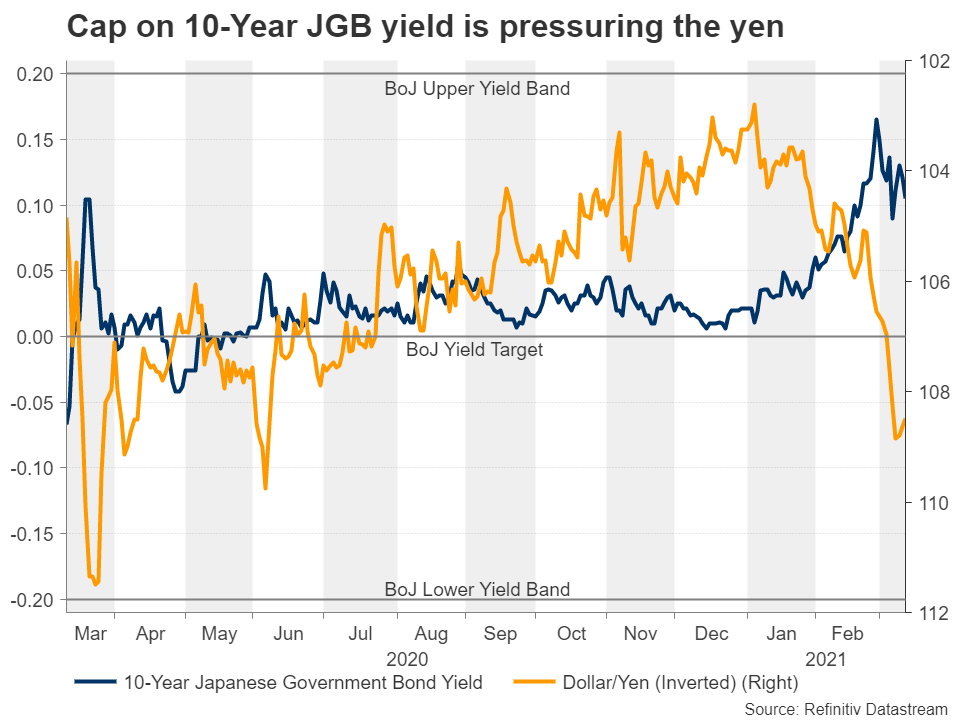

The last of the week’s central bank decisions will come on Friday by the Bank of Japan. Although no change in policy is expected by the BoJ, Governor Haruhiko Kuroda will unveil the Bank’s review of its monetary policy strategy. All the indications are that there will be no dramatic overhaul in the BoJ’s policy framework. Letting 10-year JGB yields move more freely within the 20-point implicit band on either side of the 0% target and exempting more reserves from being charged negative rates are likely adjustments to the Bank’s carefully devised policy of “quantitative and qualitative monetary easing with yield curve control”.

Kuroda has already strongly hinted that the yield band itself won’t be widened, contrary to earlier rumours, which means there’s no prospect of 10-year JGBs climbing past 0.20% anytime soon, keeping Japanese yields depressed while rival yields surge. It’s no wonder therefore that the Japanese yen, along with the Swiss franc, is the worst performing major currency this year.

The yen looks poised to deepen its year-to-date depreciation if the BoJ confirms that there are indeed no plans to widen the yield band. On the data front, January machinery orders (Monday) and February trade (Wednesday) and inflation (Friday) figures are due but unlikely to have much of an impact on yen crosses.

Commodity-linked currencies held hostage to US yields

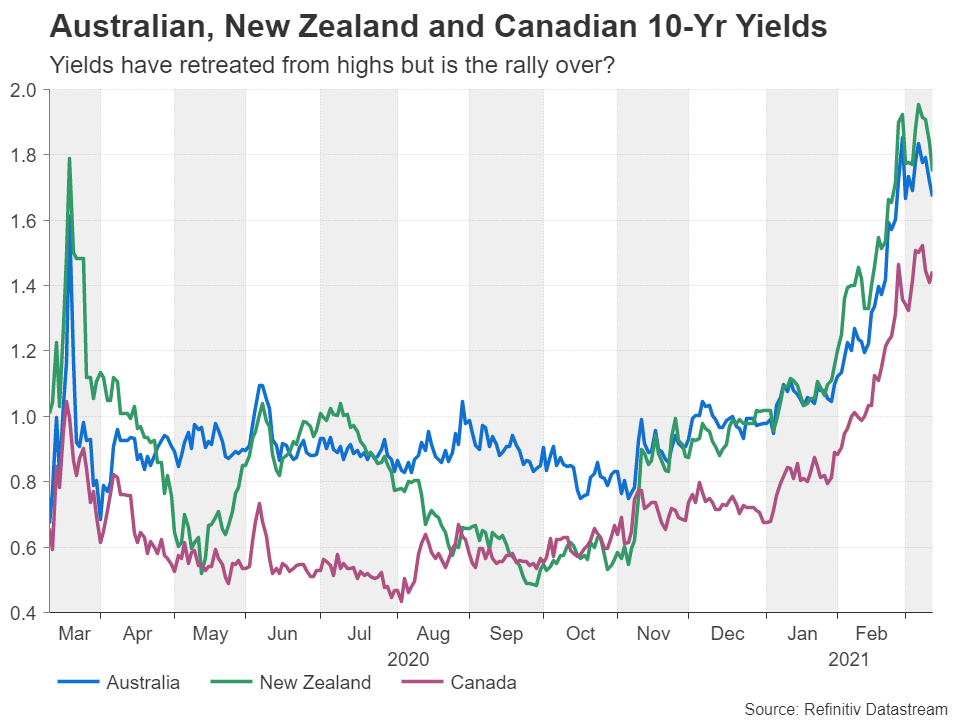

After a powerful rally in February, the commodity-linked Australian, New Zealand and Canadian dollars have come crashing down in March. The move is somewhat mirrored in commodity prices (except for oil) and interestingly, in the government bond yields of the respective currencies. Although not much has changed in terms of the outlook. If anything, the global recovery is on an even more solid footing now that President Biden’s $1.9 trillion relief package has received its final seal of approval and vaccinations around the world are gathering pace.

What has changed, however, is that US Treasury yields have remained elevated whilst other yields have receded slightly. In particular, Australian and New Zealand government bond yields are well off their highs as their central banks have been the most vocal in pushing back against this upward spiral. Canadian yields haven’t fallen as much as the Bank of Canada doesn’t seem ready to intervene in the bond markets on the same scale as its aussie and kiwi counterparts. Plus, the spillover effects from the US stimulus will be felt the most in Canada, which trades closely with America. Thus, the Canadian dollar’s pullback in March has been comparingly modest.

Should the Fed provide some kind of a signal next week that it won’t allow financial conditions to tighten much further, the greenback could take a plunge, boosting the likes of the aussie, kiwi and loonie. Otherwise, the commodity dollars might find some support in the upcoming data.

The Australian dollar will be eying industrial output and retail sales numbers out of China on Monday, as well as domestic employment figures and preliminary retail sales readings for February on Thursday and Friday, respectively. The fourth quarter GDP estimate for New Zealand will be important for the kiwi on Thursday, and in Canada, traders will be monitoring inflation (Wednesday) and retail sales (Friday) numbers.

{kind=link}