U.S. Highlights

- The ISM Services index expanded at the fastest pace in four months with demand components rising and supply side challenges normalizing.

- The Fed’s Beige book pointed to a further softening in demand, while also suggesting that labor markets remained tight.

- A hot labor market is contributing to the Fed’s hard line on inflation emphasized in speeches this week. This solidified market expectations for a three-quarter hike in September.

Canadian Highlights

- The Bank of Canada increased the overnight rate by another 75 basis points, to 3.25% this week, matching market expectations.

- The labour market continued to cool in August. Employment fell by 40k jobs, marking the third consecutive monthly decline, and the unemployment rate rose by 0.5 percentage points. However, wage growth continued to accelerate.

- Higher interest rates are beginning to slow the economy and increase headwinds for borrowers. Still, getting inflation back to target will take time, and the BoC is not ready to hit the pause button just yet.

U.S. – Fedspeak Solidifies Bets for Supersized Hike

The first post-Labor-Day week was scant on economic data, but markets had plenty of remarks from FOMC members to digest. Fed speakers’ hawkish message led Treasury yields higher, with the 2-Year yield up 12 basis points (bps) and the 10-Year yield up 10 bps on the week, at time of writing. The economic data was largely second tier sentiment surveys, which sent some conflicting signals.

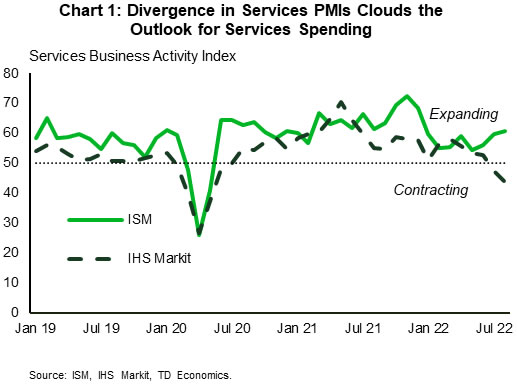

The ISM Services index rose in August, expanding at the fastest pace in four months. The underlying measures remained on the right track. The demand components – such as business activity and new orders – reached above 60 for the first time since December and March, respectively. Meanwhile, supply-side challenges continue to normalize with employment subindex moving into the expansionary territory, supplier deliveries times returning to their pre-pandemic average, and prices paid component easing.

Yet, the reading came as a surprise as consensus was pricing a moderation, and the other services flash indicator – the IHS Markit PMI – contracted in August. Demand components were especially contrasting, as the ISM index suggested strengthening while the IHS Markit pointed to a looming demand destruction (Chart 1). The differences in methodology explain the divergence in the signals: the ISM index includes a broader range of industries (including construction and mining) and reflects business conditions of its members who tend to be larger and more established companies. The IHS measure therefore better reflects the sentiment of small- and medium-sized enterprises, but we find that the ISM index has stronger historical correlations with services spending.

While this divergence clouds the outlook, we expect the truth to lie somewhere in the middle, with current economic activity remaining unchanged. This sentiment was echoed in the Fed’s Beige book that gathers anecdotal information on current economic conditions through July and August across Federal Reserve Bank districts. The report characterizes consumer spending as “steady” and points to expectations for further softening of demand over the next six to twelve months. On the other hand, respondents indicated that labor market conditions remained tight, but also pointed to a slower pace of wage increases and moderating salary expectations.

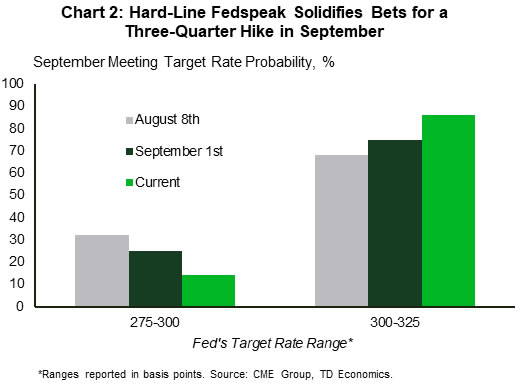

The tightness of labor market is a big part of why the Fed takes a hardline inflation fighting stance. FOMC speakers took every opportunity to reinforce their unanimity on this front ahead of the central bank’s black-out period prior to its September 21st rate decision. Chair Powell was very explicit by stating that the Committee wants to soften growth enough to “cause the labor market to get back into better balance, and then that will bring wages back down to levels that are more consistent with 2% inflation over time.” Investors heard it loud and clear with the federal funds futures markets now have greater conviction that the Fed will hike 75 basis to 3.25% (Chart 2). Moreover, the market appears less convinced that there will be rate cuts next year, buying into the Vice Chair Brainard’s “we are in this for as long as it takes to get inflation down” mantra.

Canada – BoC Hiked Again with More to Come

The Bank of Canada has clearly taken the “go big or go home” expression to heart this week by delivering another large increase in its key interest rate (report). Following the 75-basis point hike the overnight rate rose to 3.25% – the highest level in over 14 years. The increase was bang on market expectations, leading to a muted market reaction, even as the statement was quite hawkish, stating that “given the outlook for inflation, the Governing Council still judges that the policy interest rate will need to rise further.”

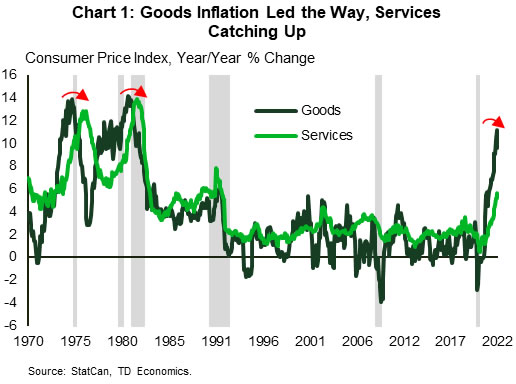

Indeed, as we wrote in this week’s report, the Bank still has the long and winding road ahead of it as it tries to wrestle inflation back to its 2% target. The recent declines in gasoline and other commodity prices have helped to bring headline inflation lower from its peak in June. However, the bad news is that the core inflation (which excludes food and energy) continues to move up, as the past surge in goods prices and healthy wage gains have passed through to prices for services. Past episodes of high inflation in the 70s and early 80s tell us that services prices are stickier. They lag goods’ prices in that they take longer to rise, but once they begin to accelerate, they can continue to increase even in an economic downturn (Chart 1). This raises the risk of a longer period of high inflation despite slowing growth.

In addition to this, there is a lag between changes to interest rates and their impact on consumer demand and inflation. Interest rate sensitive sectors– such as housing – cool quickly, but it takes longer for higher interest rates to reach other parts of the economy. This may further delay the normalization of inflation. Indeed, this was re-iterated by Senior Deputy Governor Carolyn Rogers in her speech this week, where she stated that “getting inflation back to 2% will take some time.”

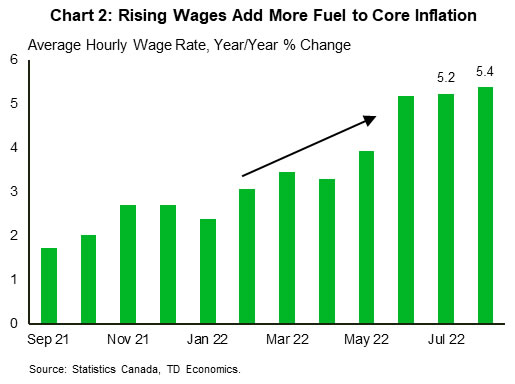

Rising wages are also adding more fuel to core inflation, as evidenced by today’s jobs report. Even as the labour market cooled further in August, with the economy shedding 40k on the month and employment down 113k since May, wage growth continued to accelerate (Chart 2). Average hourly wages were up 5.4% from a year ago – a pick-up from a 5.2% pace in July. All in all, while economic growth is cooling, the economy still has a lot of momentum. As such, we see further upside to the overnight rate, which could reach 4% by the end of this year, as the Bank vowed to “not sleep easy until we can get inflation back to target.”

Until that happens, borrowers will not sleep easy either. Next week’s release of the national balance sheet and financial flow accounts for Q2 is expected to show the first of many increases in the household debt service ratio (DSR). The DSR is expected to eclipse its pre-pandemic peak by early 2023. By the end of 2023, total debt servicing costs are projected to be 30% higher relative to 2022Q1, with the average borrower spending an extra $2500 per year on debt.

{kind=link}