With expectations about the Fed’s future course of action changing radically lately, the commodity-linked or risk-sensitive currencies aussie, kiwi, and loonie have been under strong pressure. But why are those currencies suffering and how could they perform in the near future?

What does commodity-linked currencies mean?

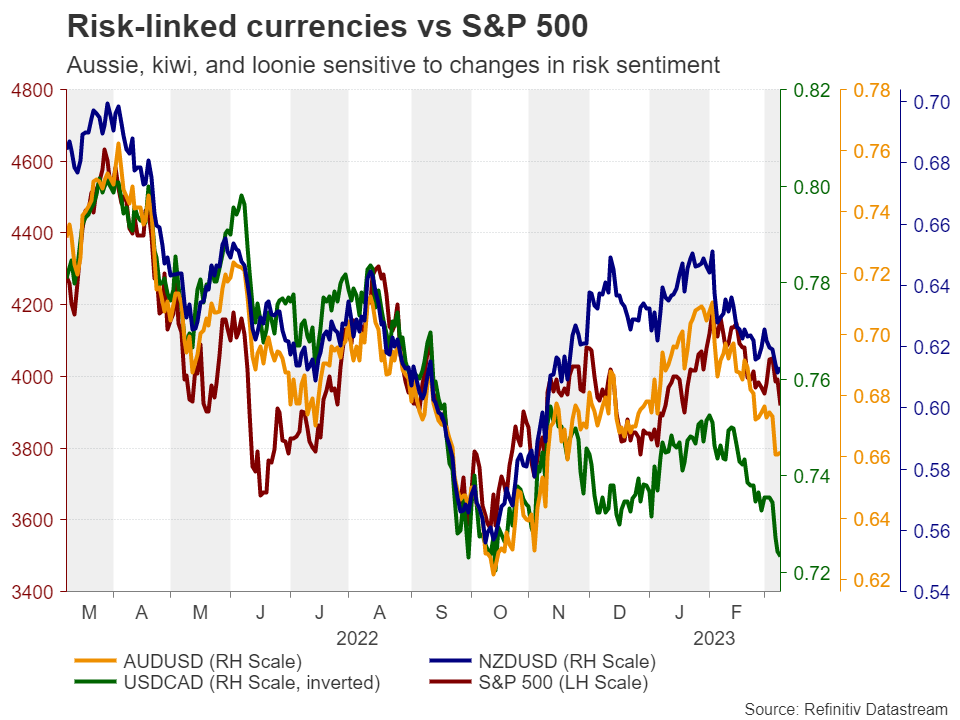

Commodity currencies are the currencies of economies that are sensitive to changes in commodity prices and usually rely on commodity exports for growth. Among the major ones, the three that fit that description are the Australian dollar, the New Zealand dollar, and the Canadian dollar. Their link to commodities makes them sensitive to changes in the global risk sentiment and that’s why they usually have positive correlation with stock indices, like the S&P 500.

For example, iron ore is the leading commodity exported from Australia, with the nation holding the eighth place in terms of copper exports. Due to manufacturing and industrial sectors around the globe using those metals, the demand for them is affected by the performance of the global economy and that’s why the aussie (and for similar reasons the other commodity-linked currencies) is usually moving in tandem with equity indices. For that reason, those currencies are also called risk-sensitive or risk-linked currencies.

Risk-linked currencies suffer as Fed and ECB hike bets rise

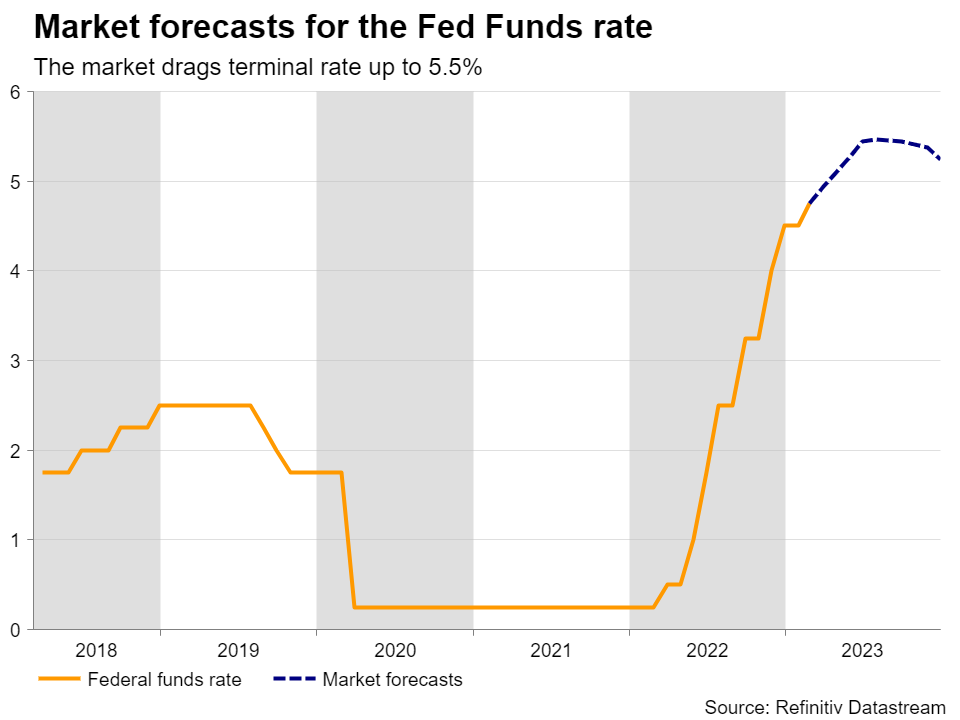

Since the beginning of February all the major currencies have been underperforming against the US dollar, which has staged a stellar comeback as a streak of upbeat US economic releases and hotter-than-expected inflation data prompted market participants to radically increase their Fed hike bets. With Fed Chair Jerome Powell appearing in a hawkish suit on Tuesday and saying that interest rates may rise higher and probably faster than previously anticipated, investors are now assigning a nearly 70% probability for a bigger 50bps hike by the Fed in two weeks, while they see a terminal rate of nearly 5.5%.

This change of heart on US interest rates has also weighed on equities and the broader risk sentiment as higher interest rates mean higher borrowing costs and lower corporate valuations, but also tighter financial conditions that could result in an economic slowdown. But hike bets are not rising only regarding the Fed. The ECB is also expected to raise rates higher than previously anticipated, with money markets now expecting a total of 160 basis points worth of additional rate increases by the end of the year.

Therefore, regardless of what their national central banks are planning to do, the aussie, the kiwi and the loonie have been under pressure, and they could continue feeling the heat of rising hike bets should incoming Eurozone and US data releases continue to corroborate that narrative.

How are they affected by policies of their own central banks?

Having said all that, an interesting question might be: Which currency could be hurt the most? There is no crystal-clear answer, but one major dynamic that could help in arriving at some sort of conclusion may be any divergences between the monetary policy strategies of their respective central banks.

So, kicking off with the BoC, this Wednesday, it refrained from pushing the hike button, becoming the first major central bank to hit the pause button in the current fight against inflation, with the meeting statement providing hints that they could stay on the sidelines until data warrants otherwise. Market participants are pricing nearly another 25bps hike by the end of the year, which leaves ample room for further declines in the loonie should Canadian data continue to disappoint.

Passing the ball to the RBA, policymakers of this Bank did press the hike button when they last met, delivering a 25bps hike and noting that further tightening of monetary policy will probably be needed. However, they added that how much further interest rates need to increase will depend on upcoming data and developments, with Governor Lowe saying a few days after the meeting that they are now closer to also pausing. In terms of market pricing, there is only a 40% probability for another 25bps hike at the upcoming gathering, with the remaining 60% pointing to a pause, but investors see nearly another 50bps worth of increments until December.

Last but not least, the RBNZ hiked by 50bps in February, with the market expecting 80 more basis points worth of hikes this year.

Loonie could be hurt the most

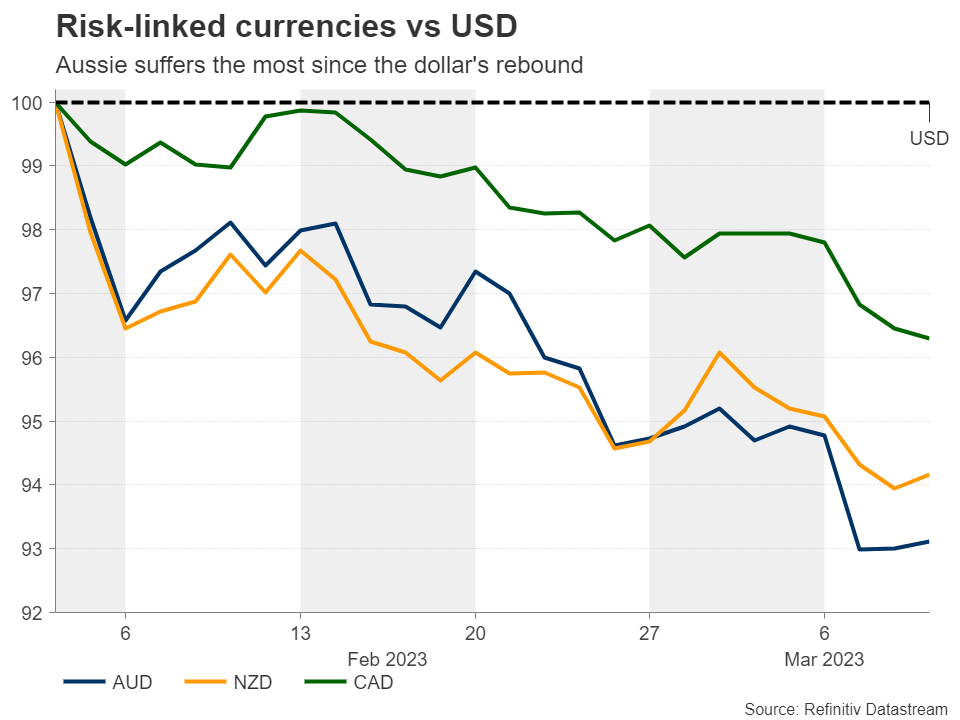

Putting everything together, it seems that there is a decent divergence between the RBNZ and the other two Banks, and thus the kiwi may be the first to be dismissed as a potential answer. Now, between the other two, the aussie took the most beating since the dollar’s rebound on February 3. However, following Powell’s hawkish remarks before Congress and the BoC’s dovish decision this Wednesday, the loonie accelerated its slide, although it has been holding better compared to the other two.

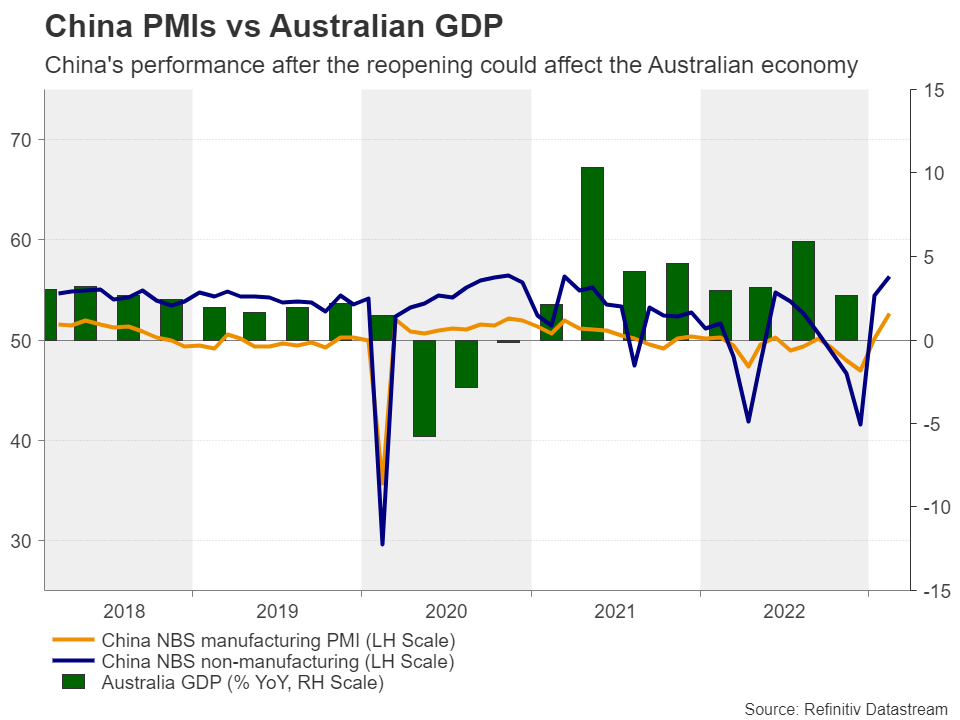

With the BoC appearing more dovish than the RBA, this suggests that from a risk-to-reward perspective, the loonie may be a better choice for exploiting further declines. In other words, there may be more room for the loonie to extend its slide. On top of that, Australia has closer trading ties with China and thus, it is more sensitive to developments surrounding the world’s second largest economy. Therefore, with the Chinese PMIs pointing to a notable improvement after the nation’s reopening from the strict COVID-related curbs, the environment may be slightly more favorable for the aussie hereafter.

Ergo, should market participants keep their Fed hike bets elevated, all three of the major risk-liked currencies could continue to slide against the dollar, but the one to suffer the most may be the loonie.

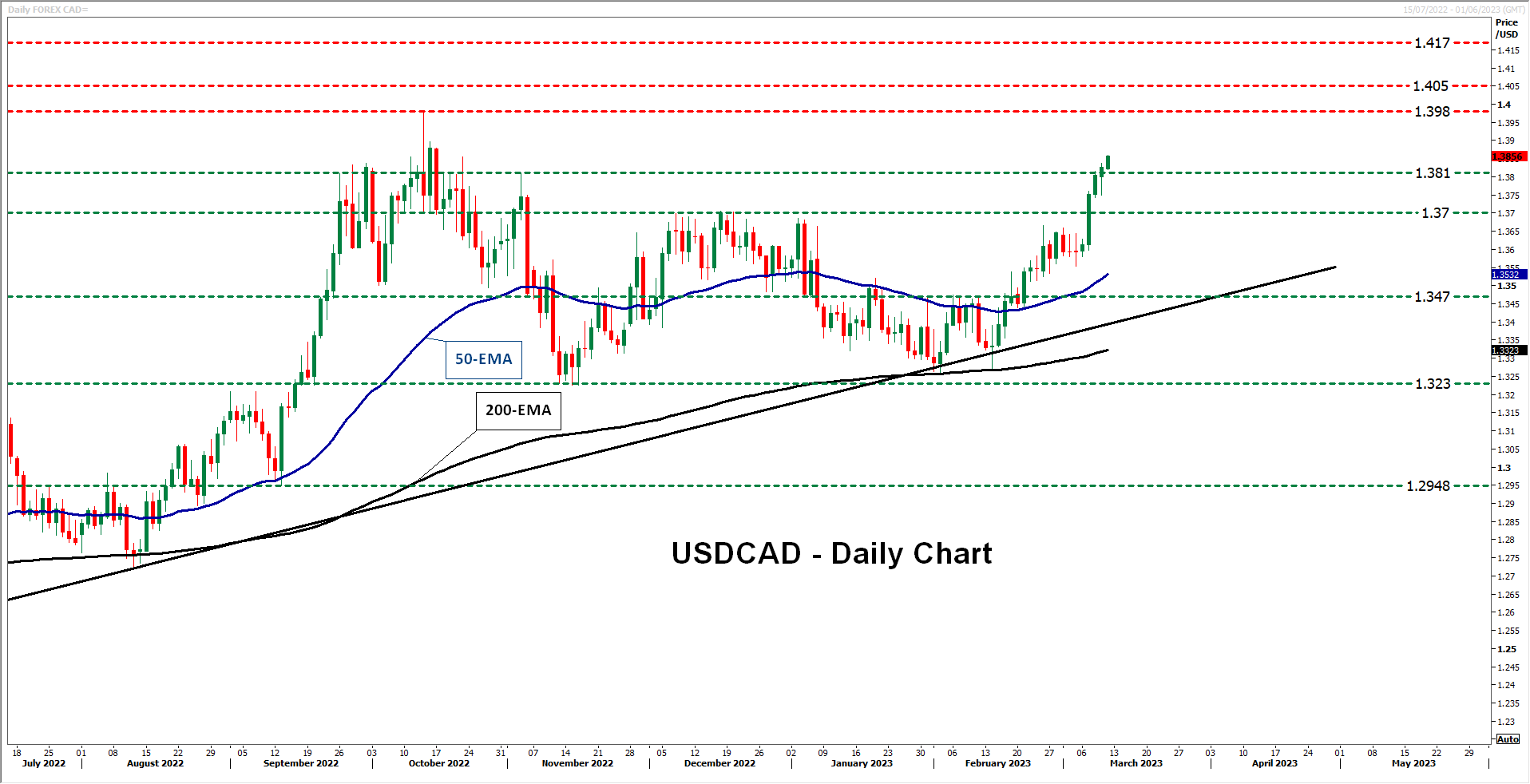

Dollar/loonie gets closer to its October high

Dollar loonie has been in a rally mode since Tuesday, breaking two important resistance areas since then; the 1.3700 zone, which acted as a ceiling between December 7 and January 3, and the 1.3810 barrier, marked by the high of November 3. Overall, the pair is trading well above the uptrend line drawn from the low of June and well above the 50- and 200-day exponential moving averages.

Dollar/loonie now seems to be heading towards the peak of October 3 at 1.3980, which is also the highest point since May 2020. If the bulls are strong enough to overcome it, they could aim for the high of May 22, 2020, at 1.4050, the break of which could see scope for extensions towards the peak of May 7, 2020, at 1.4170.

On the downside, the positive outlook could be dismissed upon a dip below 1.3470. Such a dip could also signal the break of the aforementioned uptrend line and allow declines towards the key territory of 1.3230, which offered support in November and February, and acted as resistance back in July. If that important area fails to stop the bears this time around, its break could set the stage for declines towards the low of September 13 at 1.2955.

{kind=link}