- Geopolitics and oil price dominate market sentiment

- Equity weakness could persist as cryptos unexpectedly benefit

- Dollar strength could linger if Middle East conflict escalates; could gold follow suit?

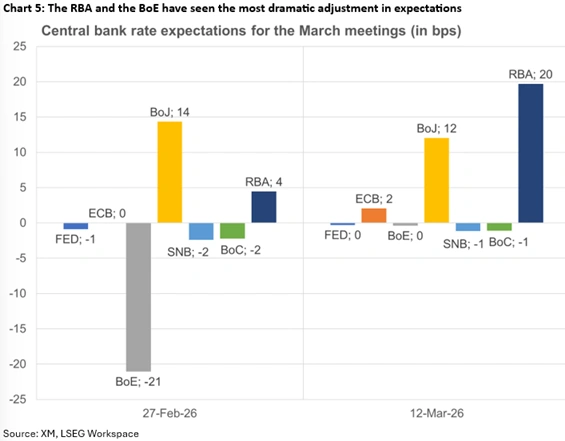

- Seven central banks meet next week; the RBA is closest to a rate hike

- Fed and ECB to remain cautious; SNB could surprise with negative rates

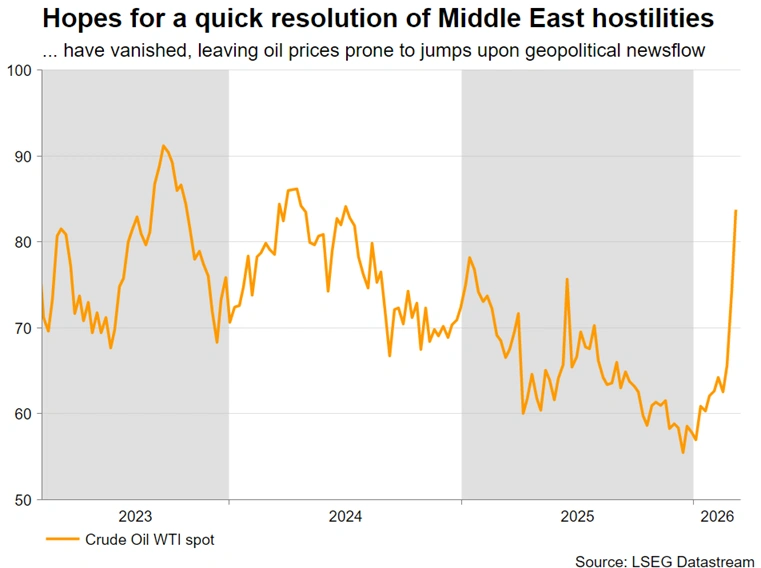

Middle East conflict remains in the driver’s seat

More than ten days after the start of the US-Israel-Iran hostilities, geopolitics remain the main market driving force. Investors are almost entirely focused on the duration of the current conflict and the damage to the real economy.

Notably, the second week of the conflict has revealed cracks in the US-Israel alliance. The Israeli side appears determined to see the conflict through to the end, aiming for regime change in Iran, and pursuing a ground offensive in Lebanon, while the US officials are already thinking ahead to the impact on midterm elections.

There have been conflicting messages from US President Trump and government officials regarding how close to “victory” the alliance currently is, with a period of four to five weeks being touted as the most likely duration of hostilities. Additionally, there are concerns within Republican ranks that rising petrol prices, and a plunging stock market could dent the party’s chances of maintaining a majority in Congress in November.

Meanwhile, Trump has put tariffs in the spotlight once again. The US administration has opened a Section 301 investigation into manufacturing practices of China, the EU, Mexico, Japan and another 12 major trading partners, aiming to replace the tariffs deemed illegal by the US Supreme Court. The universal 15% tariffs imposed after the Court’s decision can only last six months and Trump’s team wants to be ready for the next step.

Oil remains the barometer for risk appetite

Iran continues to control the Strait of Hormuz, severely reducing the flow of oil and gas, while attacking oil installations in fellow Arab countries in retaliation for Israeli attacks on Iranian oil depots. The newly elected spiritual leader quickly confirmed his hardline credentials, opening the door to a protracted conflict.

As long as passage through the Strait of Hormuz remains risky, with only a handful of ships making the round trip since the start of the conflict, oil prices will remain elevated, with the occasional jump higher when hostilities and the rhetoric intensify.

Should there be light at the end of the tunnel with a possible ceasefire – which seems extremely unlikely at this stage – oil might not return to previous low levels, as the current developments have highlighted how easy it is for Iran to disrupt oil and gas supply flows should it wish to do so again.

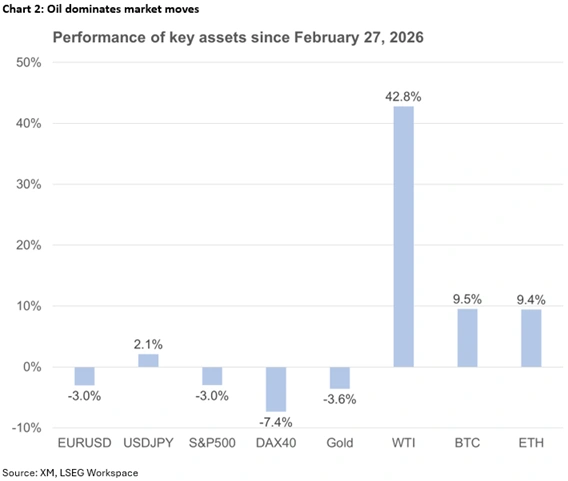

Cryptos outperform equities since the start of the conflict

Equity indices have been under only modest pressure so far this week. One could say that investors are potentially too optimistic about the US’s ability to secure the Strait of Hormuz, restoring the supply of oil. Surprisingly, cryptocurrencies have been faring better than equities since the start of the Middle East conflict. Bitcoin is up 9.3% since February 27, while the S&P 500 index is down 3% in the same period.

Another risk-off reaction is clearly on the cards upon a genuine escalation of hostilities. That could take the form of Iran targeting non-military targets, hitting the US navy, an Israeli attempt to remove the newly elected supreme leader, and/or preparing a ground offensive against Iranian nuclear installations.

Such a series of events might finally boost demand for safe haven assets, most of which have been disappointing so far. Gold has failed to rally above $5,200, ignoring data suggesting that the People’s Bank of China remains a steady driving force of demand for gold, while the yen has been a victim of the dollar’s exceptional performance.

Central bank meeting in the spotlight

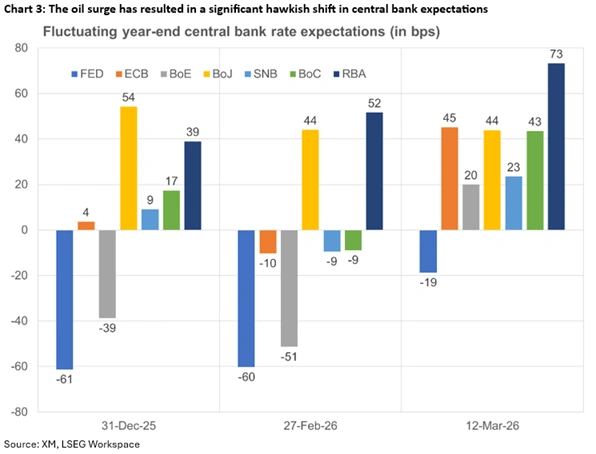

Amidst ballooning concerns for a repeat of the post-COVID inflation surge choking most economies, seven central banks will hold their respective policy meetings next week. Some are expected to alter rates, others to prove less exciting than anticipated, but all have been experiencing sharp adjustments in market rate expectations.

Rate hikes from the RBA and the BoJ next week?

Both the RBA (Tuesday, 03:30 GMT) and the BoJ (Thursday, 03:30 GMT) are seen closer to announcing a rate hike next week compared to the rest of the group.

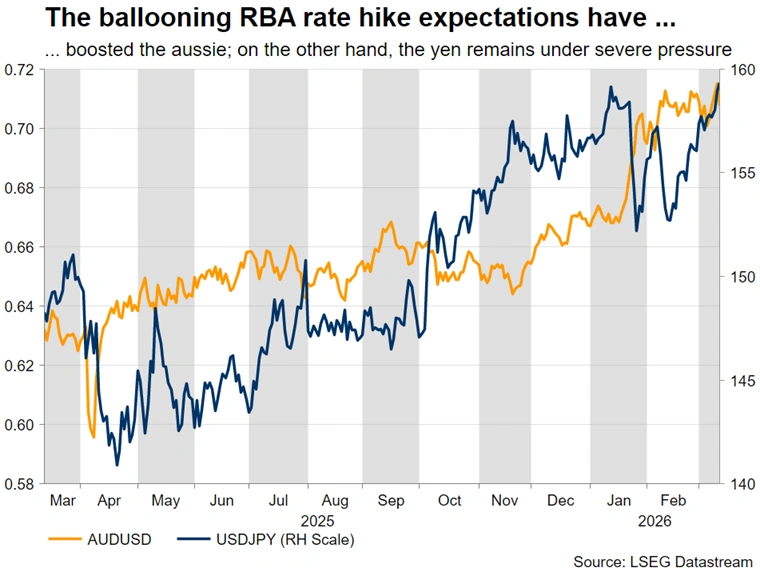

The RBA hiked in January and has been hawkish since then, with RBA Deputy Governor Andrew Hauser warning about “an oil price shock posing upside risks to inflation”, and hence further supporting rate hike expectations. The aussie has been resisting the dollar’s strength and a rate hike announcement could push this pair towards the mid-2022 highs.

BoJ rate hike expectations have been stable throughout this period, as the Middle East developments have added another layer of complexity to the BoJ. However, a successful Shunto round, with sizeable wage increases agreed, should unlock the April rate move, provided the US-Israel-Iran conflict does not escalate further. This means that a likely hawkish tilt on Thursday might put a temporary stop to the recent rally in dollar/yen, though Japanese authorities are on high alert to intervene if the pair climbs towards 160, even ahead of the BoJ meeting.

Could the SNB, the BoE or the BoC surprise on Thursday?

The first SNB meeting of 2026 comes at a crucial time. The Swiss franc is already up 2.8% this year against the euro, with decent gains versus both the dollar and the pound. The appreciation has not been consistent throughout this year, with the latest geopolitical developments adding to demand for the franc.

The SNB has allegedly already intervened to stem the franc rally, but this has proven ineffective. A dovish tilt, or a return to negative rates on Thursday (08:30 GMT) might prove insufficient to change franc’s fate, leaving aggressive intervention as the only option.

Ahead of the Middle East conflict, the 5-4 vote at the February meeting, dovish rhetoric and weakening data had beefed up the chances of a March BoE rate cut to 80%. This has completely reversed, with the market pricing out rate cuts for 2026. The pound has benefited from this reversal, significantly outperforming the euro, but this move might look exaggerated given the BoE’s dovish pedigree. The probable lack of a hawkish message on Thursday (12:00 GMT) could open the way to a reversal of this pound rally.

Similarly, Bank of Canada officials will probably be torn between the positive impact from the increased oil prices and weakening domestic economy, which is once again targeted by US tariffs. The loonie has been surprisingly resisting the dollar strength, but that might change on Wednesday as a balanced BoC rhetoric might upset expectations of a gradual tightening later in the year.

Could the Fed and the ECB meetings prove less exciting?

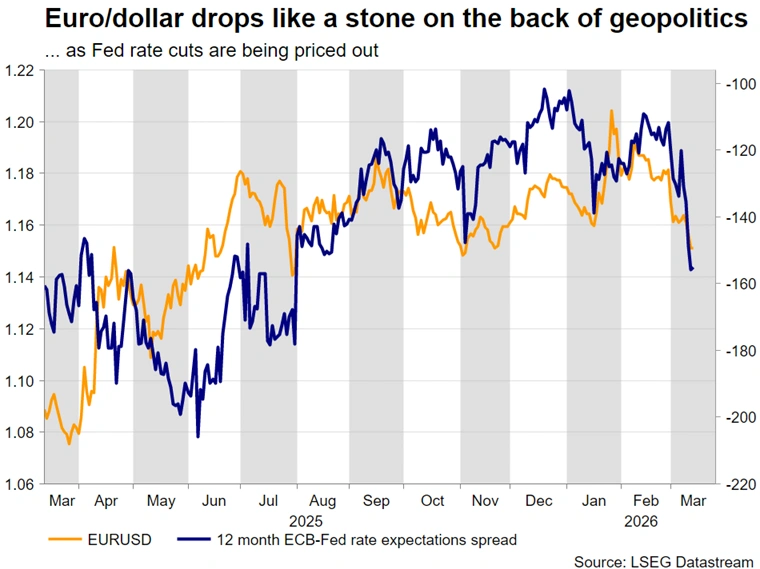

The latest developments have completely altered the rate outlook for the two heavyweights. The ECB – being more price conscious compared to the Fed at this juncture – is seen tightening its monetary policy stance by 44bps in 2026, up from just 4bps at the start of the year. This repricing looks exaggerated and has offered little assistance to the euro, which is down 2.6% this month against the dollar, the strongest monthly drop since November 2024.

Few surprises are expected on Thursday (13:15 GMT), as President Lagarde is poised to repeatedly highlight and emphasize the ECB’s readiness to quelch any likely prices increased from becoming entrenched, but will most likely stay short of signalling a hawkish shift.

Finally, the dollar has been outperforming its main counterparts so far in 2026, with euro/dollar dropping by around five big figures below its late January peak of 1.2081 and getting close to the lower boundary of the recent rectangle. Wednesday’s meeting (18:00 GMT) will be the penultimate one for Chair Powell, and hence a balanced and cautious tone is expected to dominate. That said, all eyes will be on the Summary of Economic Projections (SEP) and the dot plot as expectations for two rate cuts have diminished following the current oil price surge.

{kind=link}