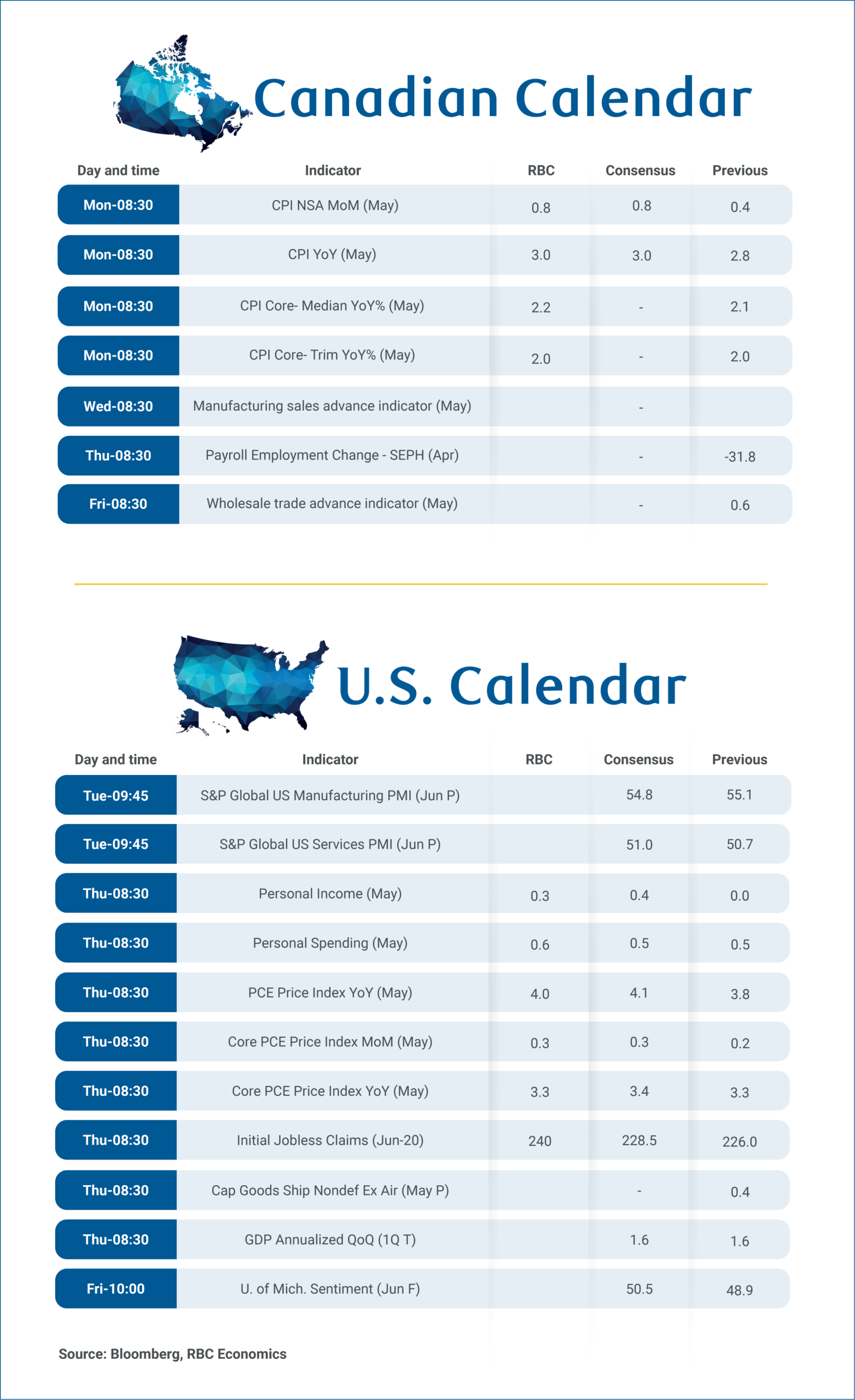

Canada’s Consumer Price Index report for May on Monday will provide an updated reading on inflation trends following the Bank of Canada’s decision to leave interest rates unchanged earlier this month.

We expect headline inflation to rise to 3% year-over-year in May, up from 2.8% in April. Energy prices are expected to remain the largest contributor to price growth with the annual gain likely edging higher after jumping to 19% in April. But, food price inflation likely also increased. We look for a tick up to 3.8% after slowing to 3.5% in April from 4% in March.

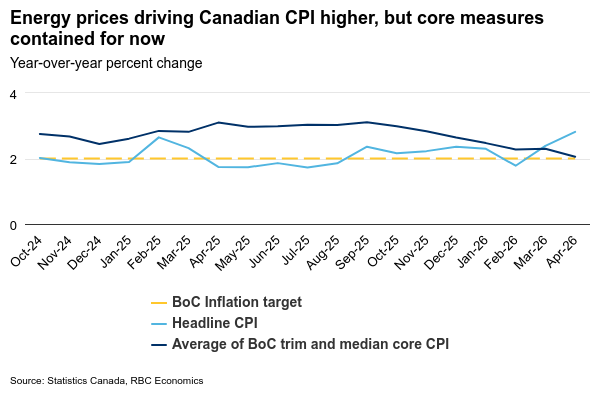

Energy prices have continued to drive headline inflation higher, but there’s nothing the BoC can do about global oil prices.

The central bank would be far more concerned about a broadening of price pressures beyond directly impacted energy prices. But, recent reports have generally shown strength in headline CPI has been concentrated in a limited number of categories with underlying measures staying closer to the BoC’s 2% inflation target.

We look for core inflation measures to remain largely contained in May despite the increase in headline inflation. CPI growth excluding food and energy likely held at 1.5% y/y, while the BoC’s preferred median and trim CPI measures stayed close to the 2% target.

The May report will also incorporate updated CPI basket weights based on 2025 consumer spending patterns. The largest changes include higher weights for transportation, health and personal care expenditures, partially offset by a lower weight for shelter. While the revised basket may result in modest changes to the contribution of specific components, we expect little impact on total inflation measurements.

Canada’s April Survey of Employment, Payrolls and Hours (SEPH) will be watched closely after a larger-than-expected bounce back in jobs in the timelier Labour Force Survey (LFS) in May. Job vacancies in the SEPH (not available in LFS) will be key, and have been edging higher in a sign that labour demand is stabilizing. We expect SEPH wage growth will continue to underperform surprisingly firm LFS readings in April. But, May data showed LFS wage growth slowed to 3% y/y, more consistent with an edging lower but still elevated unemployment rate.

We expect U.S. personal income to rise 0.4% m/m in May, trailing the 0.6% m/m increase we anticipate for personal spending, indicating consumers are continuing to spend beyond their income growth. This spending is being funded by drawing down savings rather than higher incomes with the personal savings rate expected to potentially decline further from April’s 2.6%. The data should confirm that U.S. consumers are maintaining spending momentum at the expense of their savings buffer.

{kind=link}