Sample Category Title

USDJPY Accelerates Within Range After Back-to-Back Positive US Data Surprises

The United States continues to demonstrate why it remains the largest and most powerful economy in the world, consistently surprising markets with its resilience in the past few data releases.

While market participants have been eager to question US strength—especially under President Trump’s “US Exceptionalism” policy, which many feared could backfire—recent economic data continues to challenge that narrative.

Despite ongoing concerns over diplomatic volatility and declining business confidence, the US economy once again delivered upside surprises. The Non-Farm Payrolls (NFP) report, expected at 110K, surprised with a +37K beat, and the more influential ISM Services PMI came in strong—reaffirming underlying economic momentum.

As a result, the US Dollar is regaining its footing. The Dollar Index (DXY) is up approximately 0.35% on the session, and even with an early close ahead of Independence Day, USDJPY surged 1300 pips on the heels of the release.

USDJPY Technical Analysis from the Daily to 1H Charts

USDJPY Daily Chart

USDJPY Daily Chart, July 3, 2025 – Source: TradingView

Overnight, markets perceived some hawkish comments from Bank of Japan's Takata, who mentioned that the BoJ would still look to resume hikes after a pause – such comments did not do much to add strength to the Yen.

Nonetheless, the longer-term range 142.00 to 146.50 range remains intact, with the pair up 1,350 pips on the session.

It remains notable that 146.00 served many times as the higher resistance level within the range, but two occasions of USD dominance (Potential tariff removals in beginning of May and Iran-Israel War) led to what seemed like breakouts before rejecting the Extreme of Range 147.50 to 148.

Broader USD strength following this morning's data could bring the pair to such extremes again if the Greenback keeps rebounding from its lows.

USDJPY 4H Chart

USDJPY 4H Chart, July 3, 2025 – Source: TradingView

The latest round trip within the range led to a wick on the Main Range support (last swing low 142.68), followed by a swift rebound, particularly as markets retested the Intermediate Support at 143.55.

Key Moving Averages are still flat on the 4H timeframe, confirming again the strength of the range, which may only lead to actual breakouts when markets start to price in new fundamental change – mostly expected when respective US and Japanese Central Bank policies diverge further.

The RSI moved quite aggressively higher in this morning's up-move but still had some space before becoming overbought, leaving some margin for manoeuvre for bulls – Let's take a look closer to spot more zones of interest.

USDJPY 1H Chart

USDJPY 1H Chart, July 3, 2025 – Source: TradingView

On this shorter timeframe, we can observe with more details how volatile but rangebound the price action is in the pair. Although there has been many catalysts for breakouts, the action is still contained.

This morning's Hourly bar from the data release did close at its highs and has consolidated at its top, a sign of strength for the USD as seen in other currency pairs.

Look at 144.50 as immediate pivot – a break below would retest the lower parts of the range explored in higher timeframes. Sellers will have to show some strength at the current Lower timeframe Resistance 145.00 to regain some edge.

Staying above here leaves the bulls in control, and a failure of sellers to correct prices will hint at a re-entry within the 146.00 to 146.70 Main Resistance Zone

Safe Trades!

US Equities in a Frenzy, Bolstered by ISM and NFP Beats

Consecutive positive data points in US economic releases have once again boosted sentiment, notably taking Equity and Cryptocurrency markets to a renewed frenzy.

ISM Services PMI came at 50.8 vs 50.5 expected, in the latest round of positive surprises in US Data which should once again deter markets from the weaker United States theme due to volatile Trump Administration policies.

US Equity markets will see an early 1PM Close as Americans prepare their Independence Day 4th of July Holiday.

All US Indices are making new highs, with the Dow close to 100 points from its ATH while the S&P 500 and Nasdaq are still in All-Time High Price discovery.

The latest geopolitical news is revived chances of a ceasefire between Israel and Hamas as both parties seem to finally find common ground.

While markets are busy continuing their path upward, let's discover where participants could find zones of interest for trading for the upcoming week.

Keep an eye on Cryptocurrencies during the long weekend to spot if positive sentiment is pursued throughout the 4 and a half day break for US Traders

Nasdaq, Dow Jones and S&P 500 intra-day Charts

Nasdaq 1H Chart

Nasdaq 1H Chart, July 3, 2025 – Source: TradingView

Buyers got back into control after yesterday's pre-open bearish catalysts post-ADP negative surprise, bouncing on the 22,450 Pivot on a double-bottom.

Watch for potential immediate extension resistance at 22,900 – any continuation from here should not see any slowdown before the Potential Major resistance at 23,350 (coinciding with a psychological Level).

Sellers would need to see a break below the just mentioned Pivot just mentioned to take the hand again from the strictly bullish momentum.

Dow Jones 4H Chart

Dow Jones 4H Chart, July 3, 2025 – Source: TradingView

The Dow is in pace to reach a new all time high (currently 45,060 on its CFD) in either this session or the upcoming one on Monday as long as no risk catalyst come into play in the long week-end.

Prices are entering the ATH resistance zone, RSI is way overbought but this is currently not stopping the strong bullish impulse in markets as post-war sentiment and positive data does not give many reasons for bears to step in.

The 4H MA 20 is a good measure for the current continuation of the bullish momentum, which should be defended by buyers – any breach below could point towards an intermediate correction.

Dow Jones 1H Chart

Dow Jones 1H Chart, July 3, 2025 – Source: TradingView

Buyers are looking to maintain the current trend while staying above the 1H MA 20 and 50 and would need to push above the 45,060 All-time highs.

Any break up would point to a push at 45,600 (Level from Fib Extension) and any further continuation towards the 46,000 psychological zone.

Bears would either look at an immediate rejection of the ATH, a break of the upward post-war trendline combined with the Hourly MAs or a rejection of the Fib Extension potential resistance.

In the meantime, prices are firmly in control from Buyers.

S&P 500 1H Chart

S&P 500 1H Chart, July 3, 2025 – Source: TradingView

Buying momentum is truly stellar in the S&P 500 with a continuous and not-to-steep trendline that is most optimal to maintain momentum, further supported by the 1H 20 and 50 Moving Averages.

The current hurdle to breach for buyers is around 6,300 and we are entering such a zone.

S&P Bears could either wait until the potential resistance fib extension resistance at 6,370 or a break of the Continuous Upwards trendline currently around 60 points lower.

Momentum is strong but overbought on many short timeframes, therefore it will be interesting to see if buyers manage to push prices nonetheless.

Safe Trades and an enjoyable long week-end & Independence Day for US Traders!

After NFP surprise, US Dollar Back in Play?

This morning's Non-Farm Payrolls data was more than welcomed for Dollar-Bulls

A 37K Beat on expectations (147K vs 110K exp), accompanied with a lower Unemployment Rate (4.1% vs 4.3% prior) and lower Growth Average Hourly Earnings (=less price pressures) gives path to way lesser chances of stagflation for the US Economy, at least for now.

US Indices have had a fairly muted reaction as Equity markets are still preparing for the open and the release of ISM Services Data at 10:00 expected at 50.5.

However, the US Dollar is the one standout winner and confirms further the idea that 96.50 could be a swing low for the Greenback. Let's take a look at Intra-Day Charts for the Dollar Index and other majors.

Dollar Index and other Majors' Intra-Day Charts

Dollar Index 1H

Dollar Index 1H Chart, July 3, 2025 – Source: TradingView

The DXY shot up close to 600 pips right after the US NFP data release, testing the 200H Moving Average before retracting.

Having attained the target of a much higher timeframe Head and Shoulders (96.50), our last analysis of the US Dollar had mentioned the potential of a temporary end to the selloff in the dollar – at least leading to consolidation, the rest is up to what happens around the globe (not forgetting the Trump Administration) in the upcoming months.

Prices are currently retracting to the Consolidation Support 97.00 Zone which should serve as immediate floor before ISM Services gives more clarity to market participants that aren't off this week relative to their US Dollar demand.

Next step for dollar bulls is to break above 97.50, which would also break above the 1H MA 200 mentioned before and the higher bound of 2025 Descending Channel. This could point to a further test of the Intermediate Resistance 98.00 Zone.

USDJPY 1H

USDJPY 1H Chart, July 3, 2025 – Source: TradingView

The longer-run range is still intact, with the pair up 1,000 pips after the data and seeing some resistance at the Lower timeframe Resistance 145.00 – Further break higher will test the 146.00 Main resistance zone which should warrant further analysis when prices reach that zone.

A further correction points at a 144.50 pivot point.

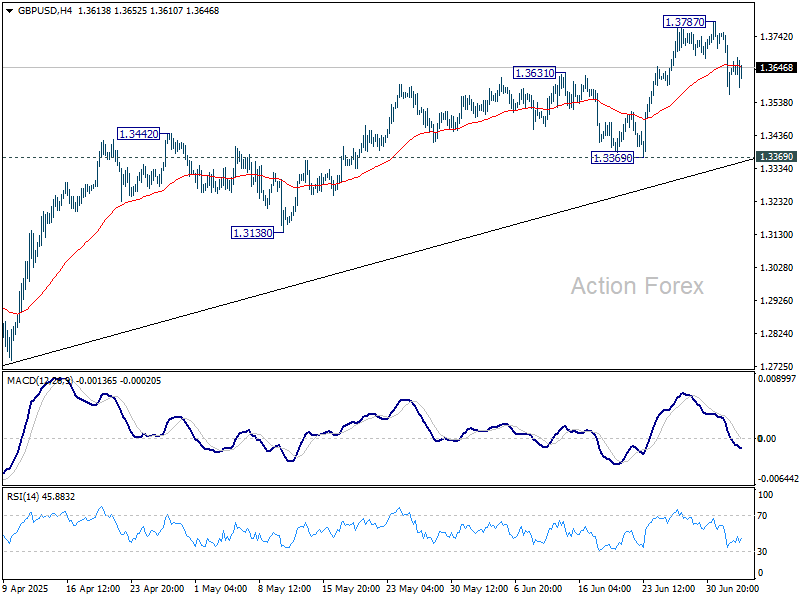

GBPUSD 1H

GBPUSD 1H Chart, July 3, 2025 – Source: TradingView

Cable is looking like bears might take the upper hand in the period coming with the formation of a downwards trendline.

Prices are currently testing the 1.36 major pivot zone – breaking the 1.3563 swing lows points to a swift test of the 1.35 psychological zone.

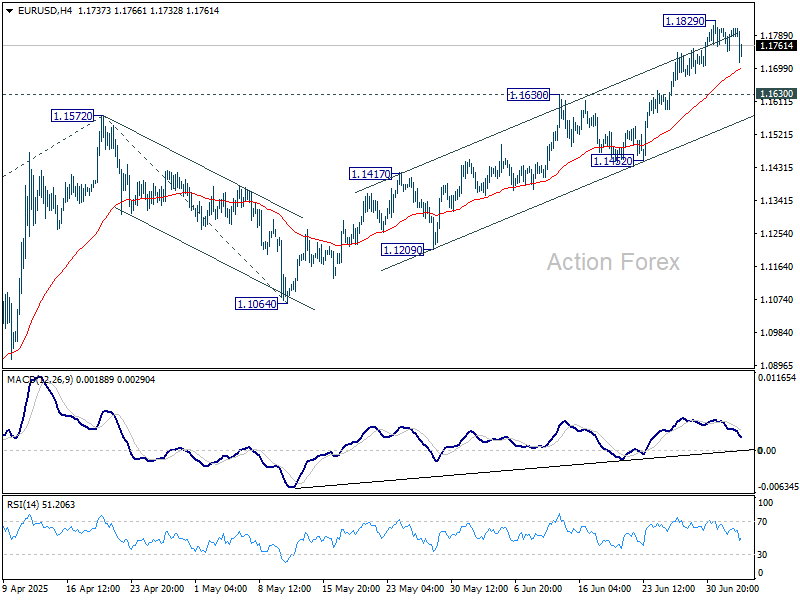

EURUSD 1H

EURUSD 1H Chart, July 3, 2025 – Source: TradingView

Same idea as for Cable, however looking less bearish.

Reactions to the 1.1765 pivot will be important, with bulls having to push above to maintain the Mid-May upwards trendline to retest the current 1.1830 highs.

On the other hand, a break of that trendline will point to a retest of the 1H MA 200 at 1.17, with further support at the 1.16 Resistance turned Support a point below.

Safe Trades!

Sunset Market Commentary

Markets

Odds for a July Fed rate cut fell back to 0% (from 20%) after a solid June payrolls reports. Anticipation had been building after a slight change of tone in Fed comments, given lack of evidence of tarri(n)flationary pressure (so far) and softening activity data. Net job growth rose by 147k in June (vs 106k consensus) with a cumulative 16k upward revision to the previous two month’s numbers. Overall government jobs contributed strongly (+73k; on a state and local, not federal, level). The private sector’s contribution (+74k) is the lowest since October of last year. The unemployment rate fell back from 4.2% to 4.1% despite a lower labour force participation rate (62.3% from 62.4%) which suggest people leaving the labour market (less job seekers than employment gains in household survey) and takes some shine of today’s numbers. Average wage growth slowed more than expected (0.2% M/M & 3.7% Y/Y from 0.4% M/M & 3.8% Y/Y). US Treasuries sold off after payrolls with the yield curve bear flattening. US yields add 9.1 bps (2-yr) to 4.1 bps (30-yr). The rising interest rate differential with Europe gives the dollar some reprieve with EUR/USD falling back from the 1.18 area to currently 1.1750. Weekly jobless claims more or less stabilized at 233k with the ISM services index to be released as we finish this report. Whatever the outcome, it won’t alter the post-payrolls vibe. We keep a closer eye at US Congress where the House might soon switch to a final vote on President Trump’s One Big Beautiful Bill Act. Passing the multiyear budget framework which significantly raises the debt limit could weigh additionally on Treasuries as investors position for the long weekend. US markets are closed for Independence Day tomorrow.

One day after Westminster drama, UK PM Starmer and Chancellor Reeves tried to pull themselves together. Starmer by saying his Finance Minister will be in her role for a very long time to come. Reeves by absolutely committing to her fiscal rule that current spending must be matched by tax receipts, even as she has to restore her £10bn buffer. The act of support and commitment helped undo part of yesterday’s sell-off in UK Gilts. UK yields lose 2 bps to 5.4 bps (30-yr) today but of course compared with a 20 bps increase yesterday. Markets are aware that the next battle (scraping two-child cap on welfare payments to larger families) arrives soon and could again trigger internal Labour rebellion forcing the government’s hand. The Autumn Budget is another key event that will keep Gilt markets on edge. EUR/GBP drops back from 0.8650 to 0.8620 today after gaining almost one big figure yesterday.

News & Views

Swiss inflation returned into positive territory in June rising 0.2% M/M and 0.1% Y/Y (from -0.1% Y/Y in May). Core inflation (ex-fresh and seasonal products, fuel and energy) also rose slightly from 0.5 Y/Y to 0.6% Y/Y. Looking at the structure of the CPI development, prices of domestic products rose 0.2% M/M and 0.7% Y/Y. Prices of imported goods were unchanged M/M but declined 1.9% Y/Y. Goods and services prices (respectively -0.1% M/M and -1.6% Y/Y; 0.3% M/M and 1.1% Y/Y) showed a similar divide, mirroring the impact of the strong franc on imported inflation. The ‘rebound’ in Swiss inflation comes as the Swiss National Bank (SNB) last month cut the policy rate by 0.25% back to zero. At that time the SNB forecasted that inflation could hold with the 0%-2% range of price stability over the policy horizon (0.2% on average this year). It is prepared to adjust policy as necessary, but highlighted side-effects of a negative policy rate. In this respect, today’s data might bring some relieve. The Swiss franc eases marginally ( EUR/CHF 0.935). Money markets see a 50%-probability of a return to negative rates by year-end.

Japan’s largest group of labour unions (Rengo) today announced that it secured an average wage rise of 5.25% in this year’s annual wage negotiations. It marks the biggest rise in 34 years. While slightly lower than the preliminary tally indicated in March (5.46%), it was still substantially higher than the average pay rise of 5.1% reached last year and 3.58% in 2023. Rengo executives indicated that they this year focused on higher wages at smaller companies, representing about 70% of the employees. Wage increases for this category were up 4.65% from 4.45%, further narrowing gap with the hikes at larger corporations. However, smaller companies often have less pricing power to pass through higher costs. Despite bigger increases, wages are still eroded by 2%+ inflation which complicates the government and the BOJ’s aim to install a positive spiral of higher real wages supporting domestic consumption. Even so, the wage data might lay to groundwork for the BoJ to consider further policy normalization once the uncertainty due to the trade tensions subsides later this year.

US ISM services rebounds to 50.8 in June, implies 0.7% annualized GDP growth

US ISM Services PMI bounced back into expansion territory in June, rising to 50.8 from 49.9 in May, and slightly ahead of expectation of 50.3. While the headline marked a return to growth, it remained below the 12-month average of 52.4.

Looking at some details, new orders jumped to 51.3 from 46.4, suggesting some revival in demand, while business activity improved from 50.0 to a solid 54.2. However, others details of the report were more mixed. The employment component slumped to 47.2 from 50.7y, signaling contraction in service-sector hiring. Prices paid remained elevated at 67.5, marking the seventh straight month above 60.

According to ISM, the June PMI level implies an annualized GDP growth of around 0.7%.

US: Payroll Gains Decelerate in June

Non-farm employment increased by 147k in June, well above market expectations for a gain of 106k. Job gains for the prior two months were also revised higher by roughly 16k jobs.

Over the past three months non-farm payrolls gained an average of 150k jobs, roughly equal to the twelve-month average.

Private payrolls rose 74k, with most of the gains concentrated in health care & social assistance (+58.6k).

In the household survey, the increase in civilian employment (+93k) came up against a declining labor force (-130k), pushing the unemployment rate down by 0.1 percentage points (ppts) to 4.1%. Meanwhile, the labor force participation rate ticked down by 0.1 ppts to 62.3%.

Average hourly earnings (AHE) were up 0.2% month-on-month (m/m) – halving May's gain. On a twelve-month basis, AHE ticked down to 3.7% (from 3.8% in May), with the three-month annualized rate falling 0.5 ppts to 3.1%.

Aggregate weekly hours fell 0.3% m/m after remaining unchanged over the past two months.

Key Implications

The June gain in non-farm payrolls outpaced expectations considerably, as non-cyclical sectors including health care and government carried the report. While federal payrolls continued to decline in June, state & local government payrolls recorded its largest gain in two and a half years. Absent this spike, the employment report would have come in roughly on-par with expectations. This combined with the cooling in average hourly earnings is indicative of a stable but slowing labor market, which we expect to gradually apply upward pressure to the unemployment rate through the second half of the year.

For its part, the Federal Reserve is unlikely to be deterred from their current patient stance on monetary policy given the stability of overall employment trends. This gives the Fed time to continue to assess developing inflation dynamics under tariffs. Market pricing currently expects the Fed to cut rates twice before year-end, with a first cut expected in September.

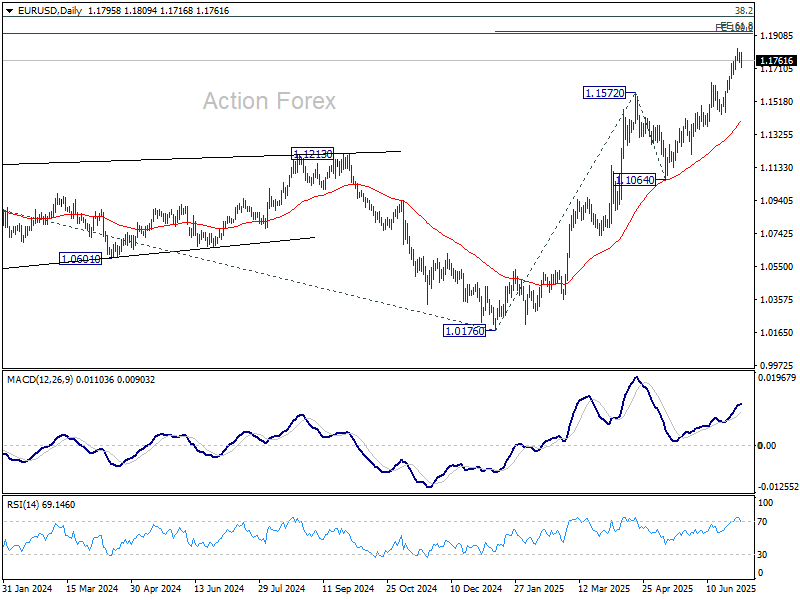

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1761; (P) 1.1785; (R1) 1.1824; More...

EUR/USD dips lower today as consolidation from 1.1829 extends. Outlook is unchanged and intraday bias remains neutral. Downside of retreat should be contained by 1.1630 resistance turned support to bring another rally. On the upside, break of 1.1829 will target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

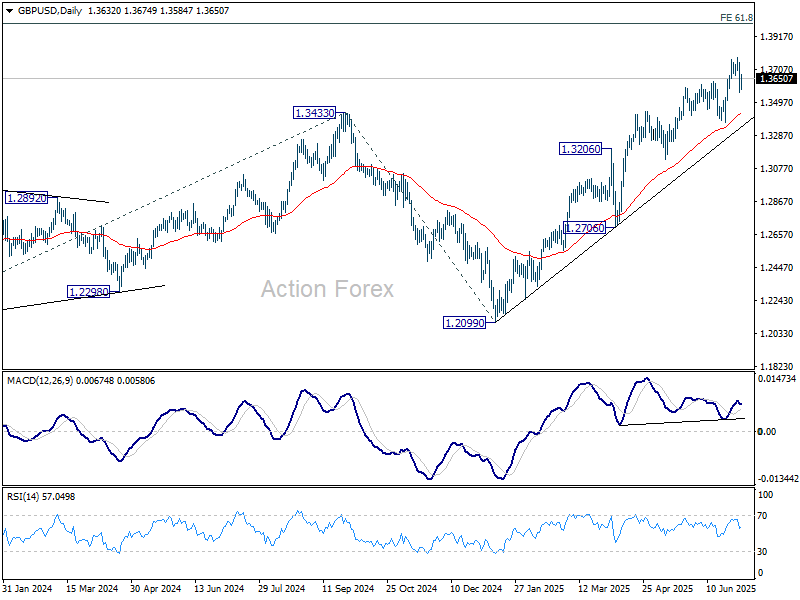

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3547; (P) 1.3651; (R1) 1.3738; More...

GBP/USD is extending consolidations below 1.3787 and intraday bias remains neutral. Deeper retreat cannot be ruled out, but downside should be contained above 1.3369 support to bring another rally. Firm break of 1.3787 will resume larger rise to 1.4004 projection level next.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2983) holds, even in case of deep pullback.

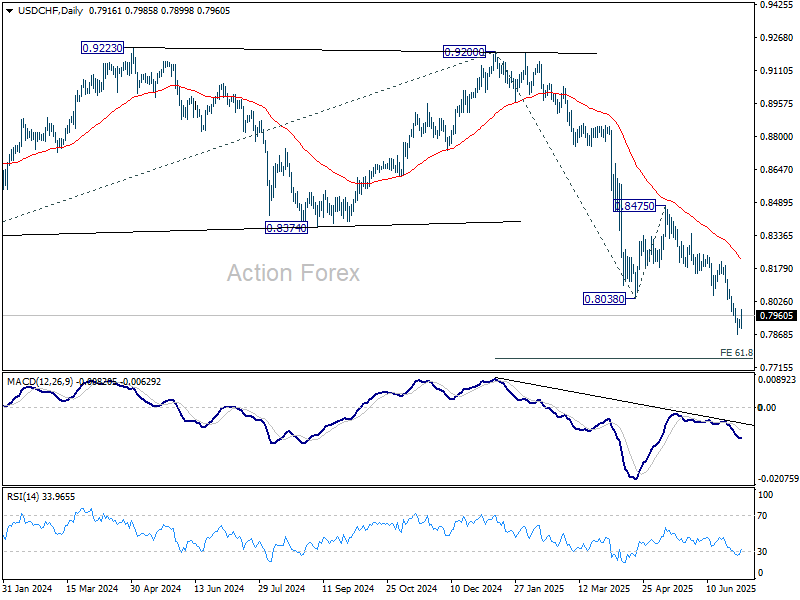

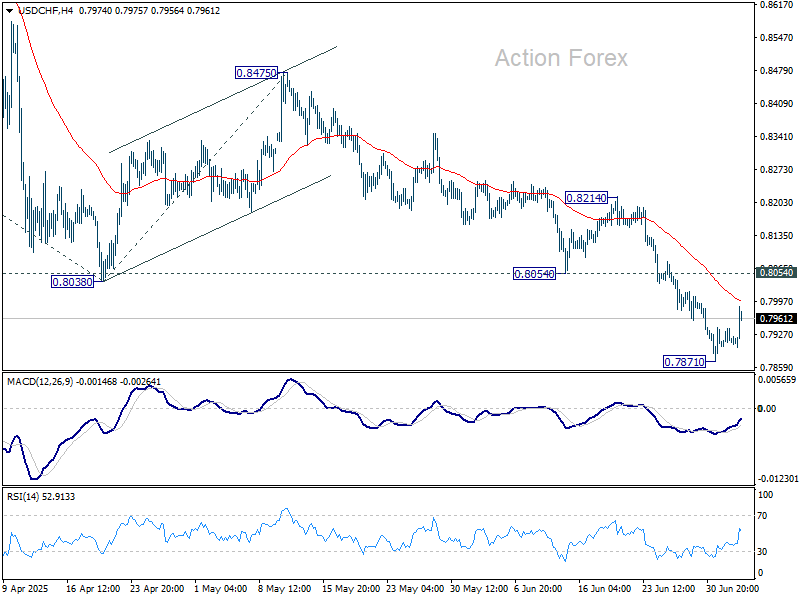

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7902; (P) 0.7921; (R1) 0.7941; More….

USD/CHF's recovery from 0.7871 extends higher today and outlook is unchanged. More consolidations could be seen but upside should be limited by 0.8054 support turned resistance to bring another fall. Below 0.7871 will extend the larger down trend to 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757. Firm break there will pave the way to 100% projection at 0.7313 next.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.