Sample Category Title

AUD/USD Attempts Fresh Climb as NZD/USD Slips

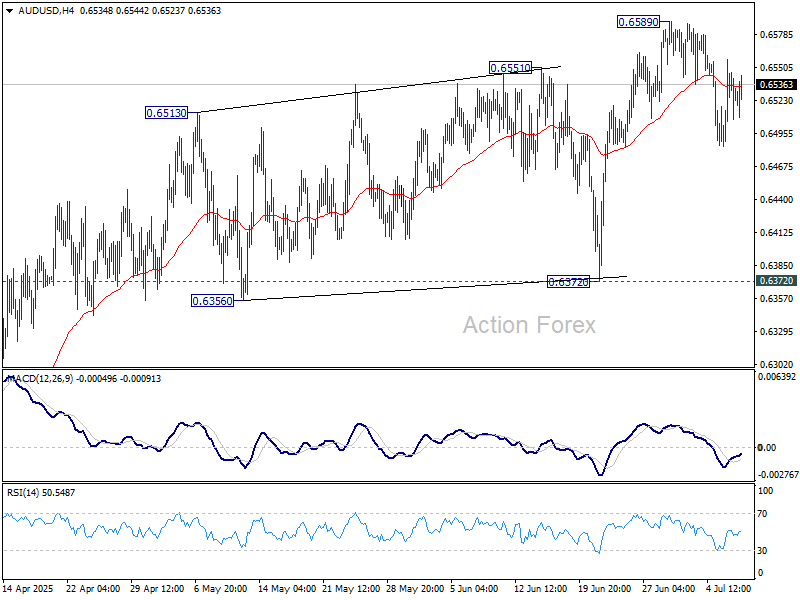

AUD/USD is attempting a fresh increase from the 0.6485 support. NZD/USD is struggling and might decline below the 0.5980 level.

Important Takeaways for AUD/USD and NZD/USD Analysis Today

- The Aussie Dollar found support at 0.6485 and recovered against the US Dollar.

- There is a key bearish trend line forming with resistance at 0.6535 on the hourly chart of AUD/USD at FXOpen.

- NZD/USD is consolidating above the 0.5980 support.

- There is a connecting bearish trend line forming with resistance at 0.6010 on the hourly chart of NZD/USD at FXOpen.

AUD/USD Technical Analysis

On the hourly chart of AUD/USD at FXOpen, the pair started a fresh increase above 0.6550. The Aussie Dollar tested the 0.6585 zone before the bears appeared and pushed it lower against the US Dollar.

The pair declined below the 0.6560 and 0.6550 support levels. The recent low was formed at 0.6485 and the pair is rising again. The bulls pushed it above the 50% Fib retracement level of the downward move from the 0.6588 swing high to the 0.6485 low.

The pair is now consolidating above the 50-hour simple moving average. On the upside, the AUD/USD chart indicates that the resistance is near the 0.6535 zone. There is also a key bearish trend line forming at 0.6535.

The first major resistance might be 0.6550 and the 61.8% Fib retracement level. An upside break above it might send the pair further higher. The next major resistance is near the 0.6560 level. Any more gains could clear the path for a move toward the 0.6585 resistance zone.

If not, the pair might correct lower. Immediate support sits near the 0.6510 level. The next support could be 0.6485. If there is a downside break below 0.6485, the pair could extend its decline toward the 0.6440 zone. Any more losses might signal a move toward 0.6420.

NZD/USD Technical Analysis

On the hourly chart of NZD/USD at FXOpen, the pair also followed AUD/USD. The New Zealand Dollar struggled above 0.6100 and started a fresh decline against the US Dollar.

There was a move below the 0.6050 and 0.6020 support levels. A low was formed at 0.5978 and the pair is now consolidating losses below the 50-hour simple moving average. The NZD/USD chart suggests that the RSI is back below 50 signalling a bearish bias.

On the upside, the pair is facing resistance near the 23.6% Fib retracement level of the downward move from the 0.6120 swing high to the 0.5978 low. There is also a connecting bearish trend line forming with resistance at 0.6010.

The next major resistance is near the 0.6065 level or the 61.8% Fib retracement level. A clear move above the 0.6065 level might even push the pair toward the 0.6120 level. Any more gains might clear the path for a move toward the 0.6150 resistance zone in the coming days.

On the downside, there is a support forming near the 0.5980 zone. If there is a downside break below 0.5980, the pair might slide toward 0.5940. Any more losses could lead NZD/USD in a bearish zone to 0.5910.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Multiple, Often Diffuse, Trade Headlines Leave Little Visibility to Set Up Directional Trades

Markets

Markets headlines yesterday still were dominated by the ongoing flurry of trade-war communication as launched by US president Trump. Even so, in particular on interest rate markets, global public debt sustainability was at least as important as a market driver. The trigger again came from two ‘market outsiders’: the UK and Japan, with the impact spilling over globally. In the UK, the publication by OBR of its yearly public risk and sustainability report served as another illustration that the country has no fiscal headroom to address new shocks or take any policy initiatives. In Japan, political uncertainty in the run-up to the July 20 Upper House elections continues to nourish concerns on fiscal sustainability. In a steepening move, Japanese (+9 bp) and UK (+ 6.3 bps) 30-y bonds again underperformed. The German yield curve followed this broader trend (steepening, 2-y +3.5 bps, 30-y +5.4 bps). Interestingly, the US even after OBBB was less affected (yields changing less than 2 bps across the curve). As indicated, the new avalanche of US trade (war) communication at first sight only has far less impact. US president Trump indicated that he won’t extend the tariff pause beyond August 1, threatened a 50% levy on copper imports and other sector tariffs, including a potential 200% levy on pharma imports. BRICS countries still risk an additional 10% levy. One might assume that, at some point, such measures should put upward pressure on US inflation and complicate planning by all economic agents. However, as was the case on Monday after announcing reciprocal tariffs, the impact on markets at the end of the day was modest. US equities finished little changed (S&P 500-0.07%). USD again gained modestly (DXY close 97.52, EUR/USD little changed at 1.1725). Sterling (slightly) underperformed (EUR/GBP 0.863). The yen remained under pressure both against the dollar (USD/JPY close 146.6) and the euro (EUR/JPY 171.9).

Asian equity markets this morning are again ‘meandering ‘, mostly holding in positive territory. The multiple, often diffuse, trade headlines still leave little visibility to set up directional trades and this pattern might continue today. A US-EU trade deal is expected to be announced ‘in the near future’. The FT this morning reports this framework might leave the EU with higher tariffs than those granted to the UK. The eco calendar is again extremely thin with the Minutes of the June Fed policy meeting the exception to the rule. With debt sustainability in focus, we also keep a close eye at a $39 bln US treasury action, the first sale of LT US debt post OBBB and a precursor for tomorrow’s 30-y sale. On FX markets, the dollar continues recent gradual rebound. However, in the likes of DXY or EUR/USD the technical picture hasn’t changed in any profound way.

News & Views

The central bank of New Zealand (Reserve Bank of New Zealand, RBNZ) kept the policy rate unchanged at 3.25% in a move expected by both markets and analysts. The case for another rate cut was considered, mainly over near-term growth momentum and the risk of prolonged weakness in economic activity leading to downward pressure on medium-term inflation. In the end, though, the benefits of waiting until August in light of near-term inflation risks outweighed. Inflation is expected to rise further from the 2.5% in Q1 towards the top of the 1-3% target band before returning to around 2% by early 2026 on spare productive capacity. It also allows the RBNZ to observe developments (ie tariffs) in the global economy and whether domestic economic weakness persists. New Zealand money markets are discounting a two-in-three chance for the RBNZ to cut rates next month. The kiwi dollar holds steady around USD/NZD 0.60.

Chinese consumer prices unexpectedly rose 0.1% year-over-year in June. Consensus was expecting CPI to match May’s -0.1%. Monthly prices fell for a second month straight, though, suggesting deflationary pressures are all but over. June printed -0.1% m/m following May’s -0.2%. Core inflation was flat on a monthly basis and edged up from 0.6% to 0.7% y/y. Government subsidies for home appliance purchases helped CPI to return to positive territory but that’s unlikely to be a lasting and in any case large driver. Services prices held at 0.5% y/y. Adding to evidence of still-strongly low (even negative) price pressures are the June PPIs, which dropped into deeper negative area at -3.6% y/y, a near 2-year low. The Chinese yuan trades a tad weaker around USD/CNY 7.18.

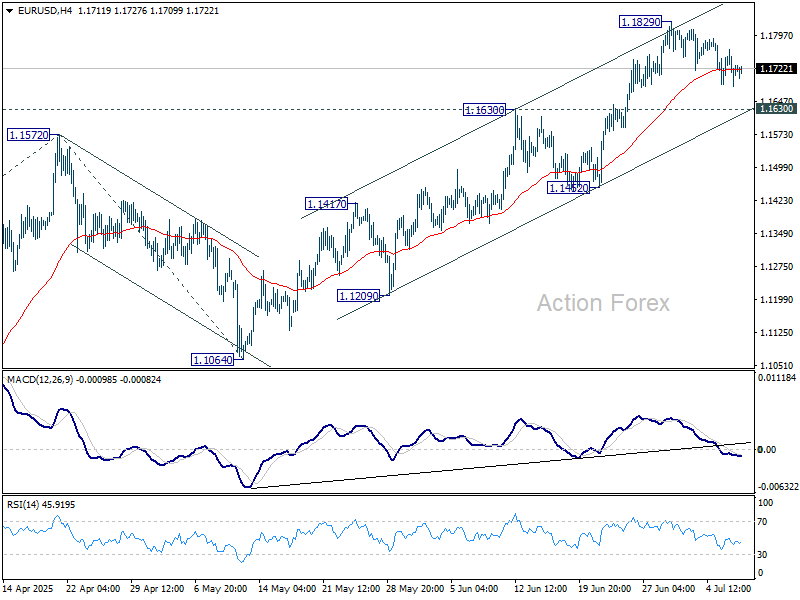

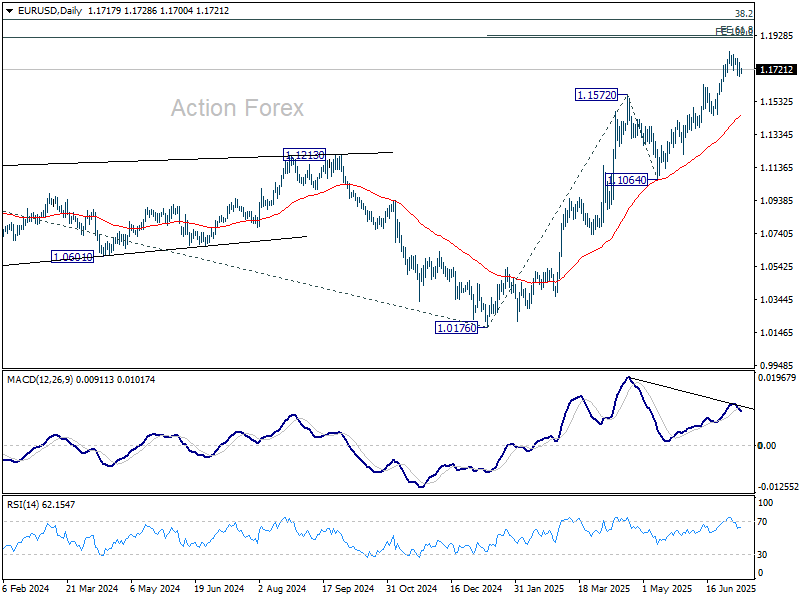

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1684; (P) 1.1724; (R1) 1.1766; More...

Intraday bias in EUR/USD remains neutral as consolidations continues below 1.1829. Downside should be contained by 1.1630 resistance turned support to bring rebound. Firm break of 1.1829 will resume the rise from 1.0176 and target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

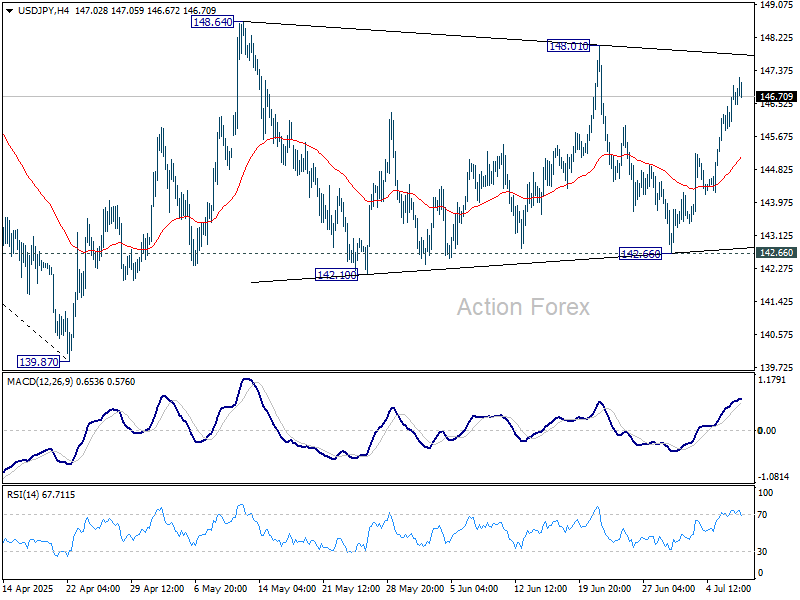

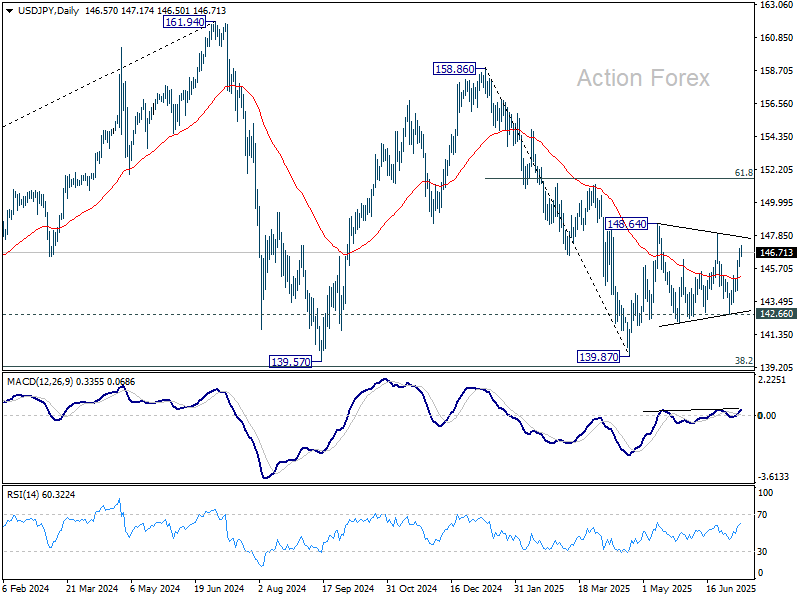

USD/JPY Daily Outlook

Daily Pivots: (S1) 145.94; (P) 146.46; (R1) 147.09; More...

USD/JPY is still bounded in range of 142.66/148.01 and intraday bias remains neutral. On the upside, firm break of 148.01 resistance will resume the rise from 139.87 to 61.8% retracement of 158.86 to 139.87 at 151.22. However, break of 142.66 will bring deeper fall back to retest 139.87 low.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

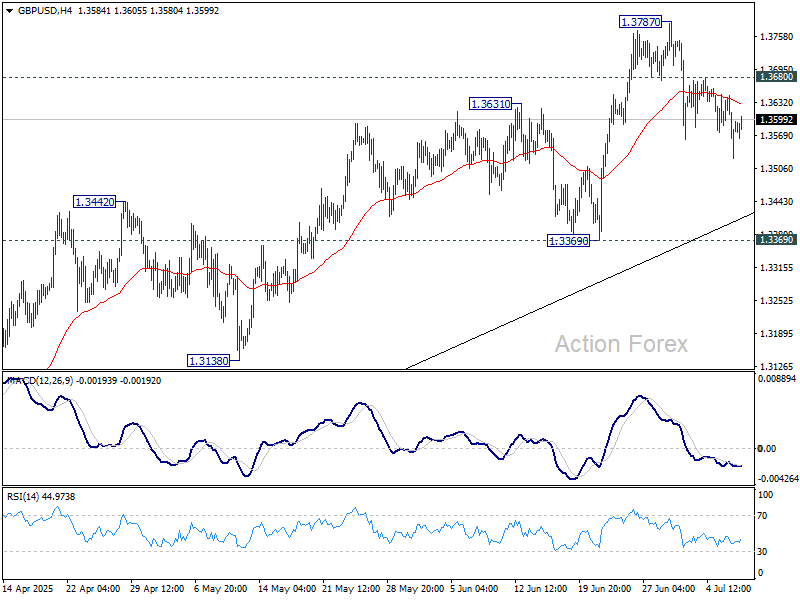

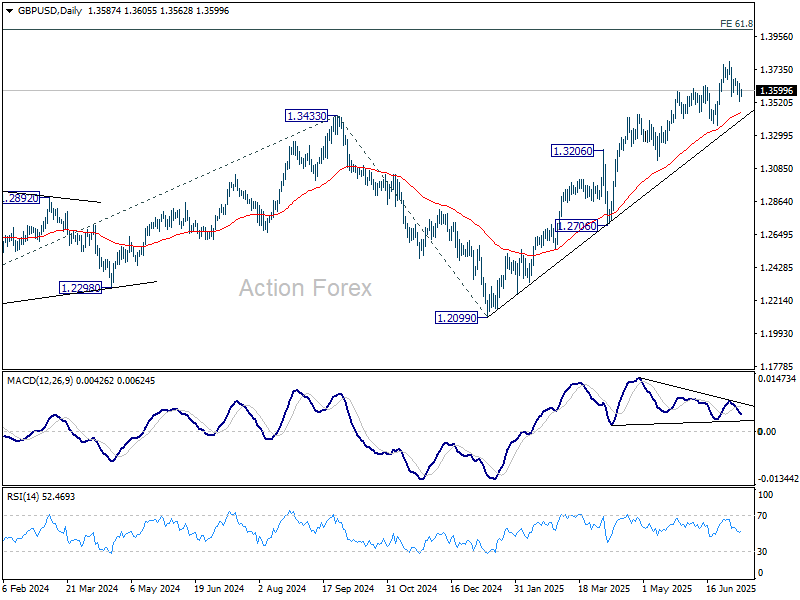

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3530; (P) 1.3589; (R1) 1.3651; More...

Intraday bias in GBP/USD remains neutral for the moment. Correction from 1..3787 might extend lower, but downside should be contained by 1.3369 support to bring rebound. On the upside, above 1.3680 minor resistance will bring retest of 1.3787. Firm break of 1.3787 will resume larger up trend to 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2985) holds, even in case of deep pullback.

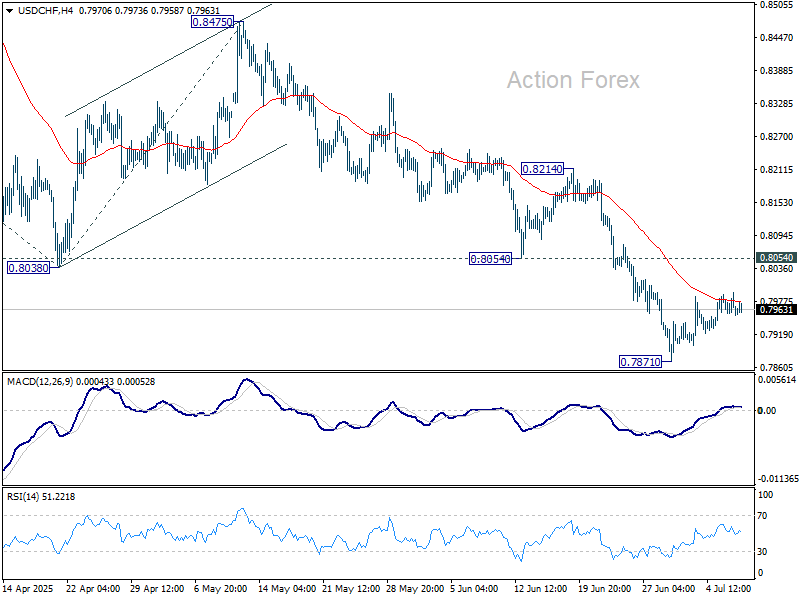

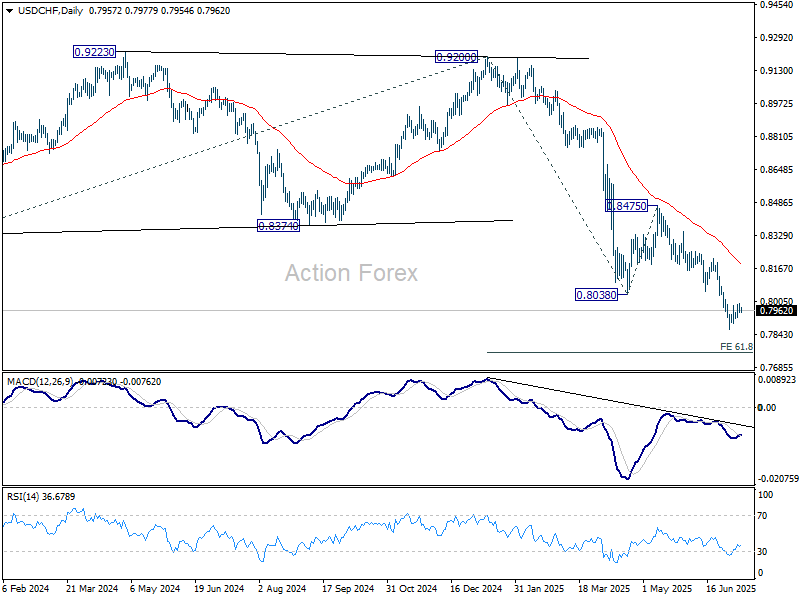

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7941; (P) 0.7968; (R1) 0.7983; More….

Intraday bias in USD/CHF remains neutral as consolidations from 0.7871 is still in progress. Stronger recovery cannot be ruled out, but upside should be limited by 0.8054 support turned resistance to bring another fall. Below 0.7871 will extend the larger down trend to 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757. Firm break there will pave the way to 100% projection at 0.7313 next.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

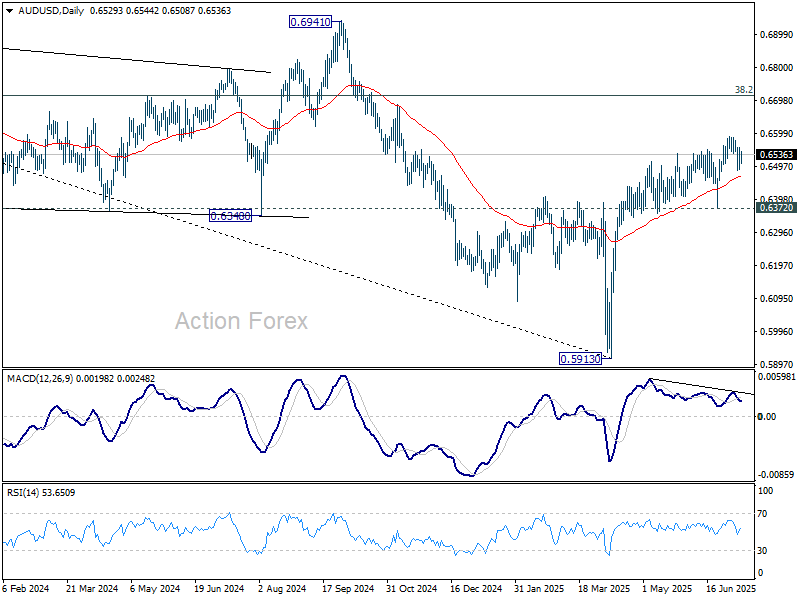

AUD/USD Daily Report

Daily Pivots: (S1) 0.6493; (P) 0.6526; (R1) 0.6562; More...

AUD/USD is staying in consolidation below 0.6589 and intraday bias remains neutral. Overall, further rally is still expected as long as 0.6372 support holds. On the upside, firm break of 0.6589 will resume the rise from 0.5913 and target 0.6713 fibonacci level.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).

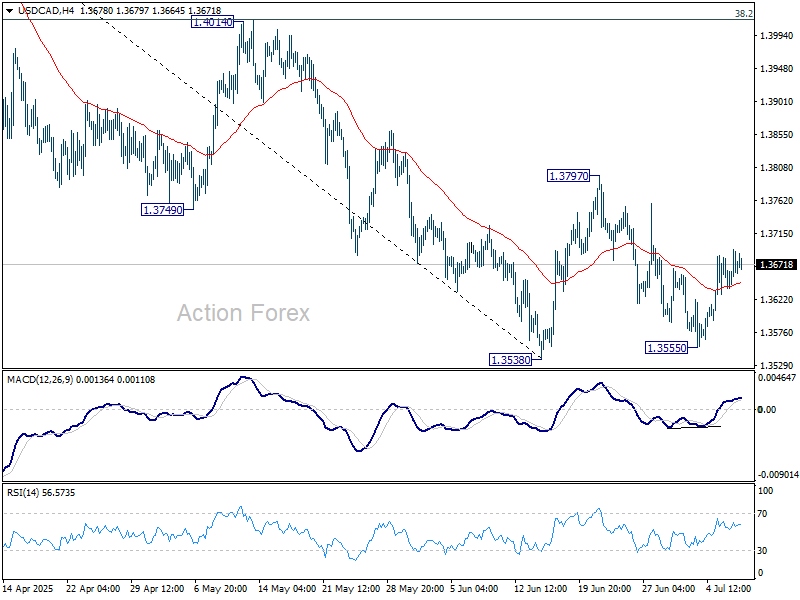

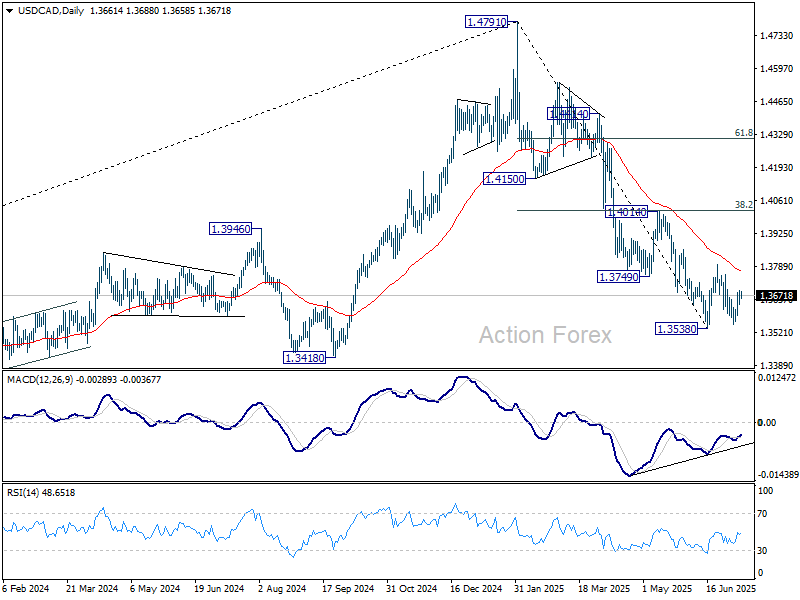

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3636; (P) 1.3666; (R1) 1.3692; More...

No change in USD/CAD's outlook as corrective pattern from 1.3538 is in the third leg. Intraday bias stays mildly on the upside for 1.3797 resistance and possibly above. On the downside, firm break of 1.3538/55 support zone will confirm resumption of whole decline from 1.4791.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

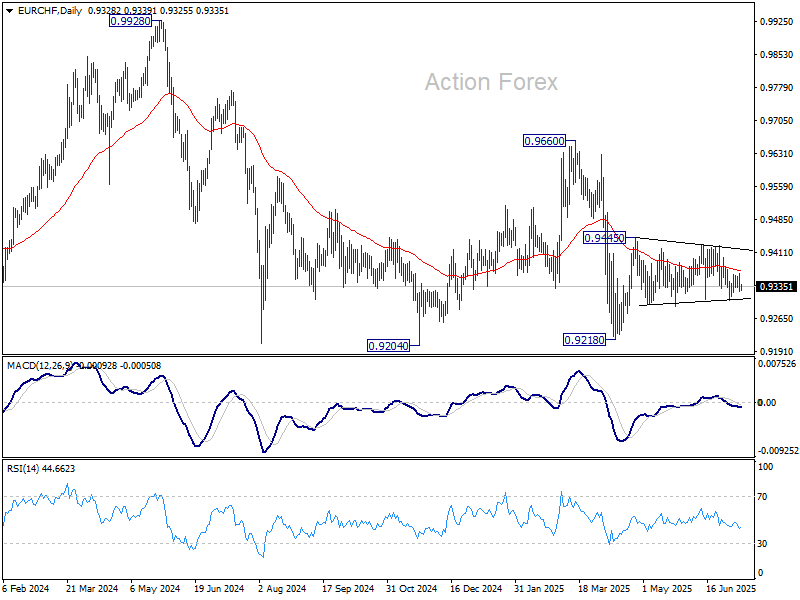

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9316; (P) 0.9341; (R1) 0.9358; More....

Intraday bias in EUR/CHF remains neutral as range trading continues. On the upside, break of 0.9428/45 resistance zone will resume the rebound from 0.9218. On the downside, break of 0.9305 will bring retest of 0.9218 low instead.

In the bigger picture, while downside momentum has been diminishing as seen in W MACD, there is no sign of bottoming yet. EUR/CHF is still staying below 55 W EMA (now at 0.9433) and well inside long term falling channel. Outlook will stay bearish as long as 0.9660 resistance holds. Break of 0.9204 (2024 low) will confirm resumption of down trend from 1.2004 (2018 high).

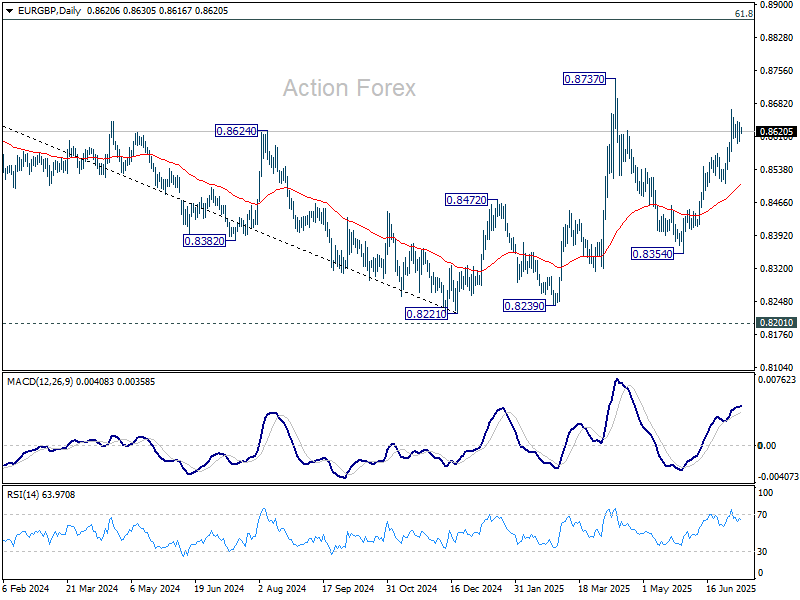

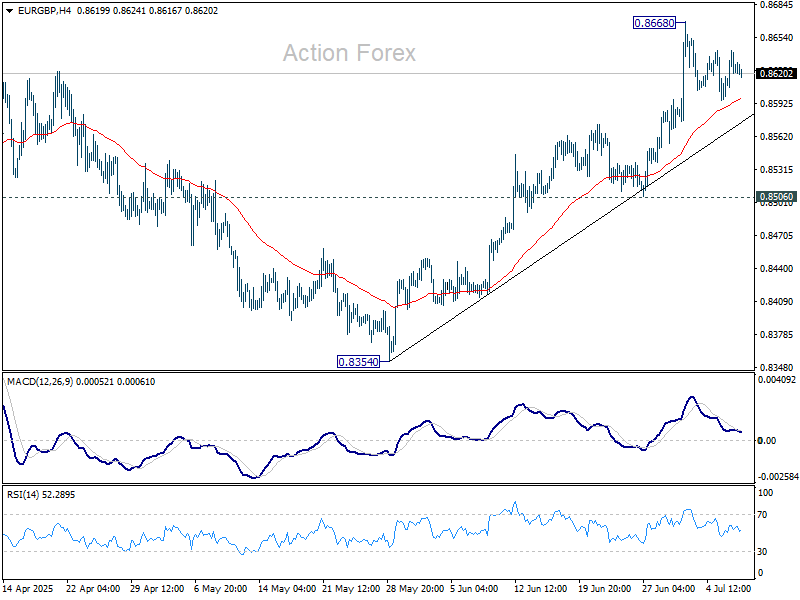

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8602; (P) 0.8622; (R1) 0.8647; More...

EUR/GBP is staying in consolidations below 0.8668 and intraday bias stays neutral. Further rise is expected as long as 0.8506 support holds. Above 0.8668 will target a retest on 0.8737 high. Decisive break there will resume the whole rise from 0.8221 low.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the downside from 0.9267 (2022 high). But even if it's a correction, firm break of 0.8737 will still pave the way to 61.8% retracement of 0.9267 to 0.8221 at 0.8867.