Sample Category Title

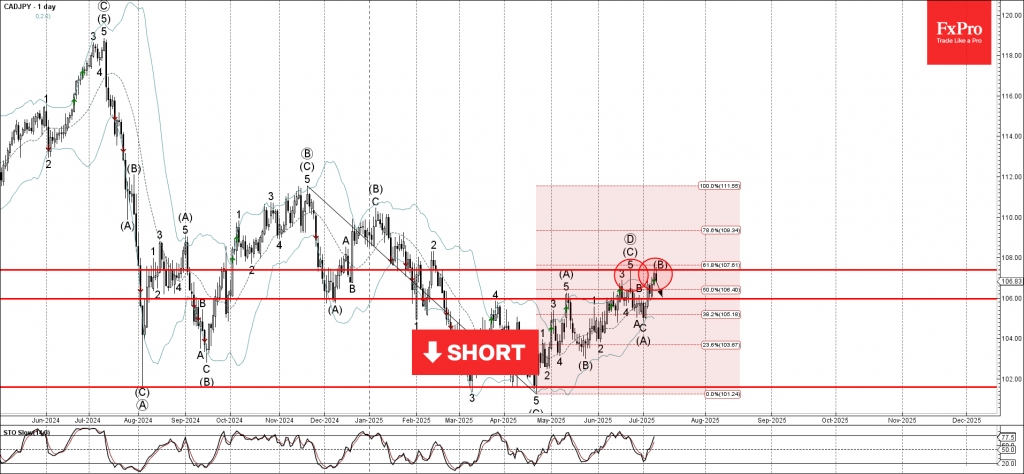

CADJPY Wave Analysis

CADJPY: ⬇️ Sell

- CADJPY reversed from resistance area

- Likely to fall to support level 106.00

CADJPY currency pair recently reversed from the resistance area located between the resistance level 107.40 (former monthly high from June), upper daily Bollinger Band and the 61.8% Fibonacci correction of the downward impulse from November.

The downward reversal from this resistance area stopped the previous intermediate corrective wave (B).

Given the strength of the resistance level 107.40 and moderately bullish yen sentiment seen today, CADJPY currency pair can be expected to fall to the next support level 106.00.

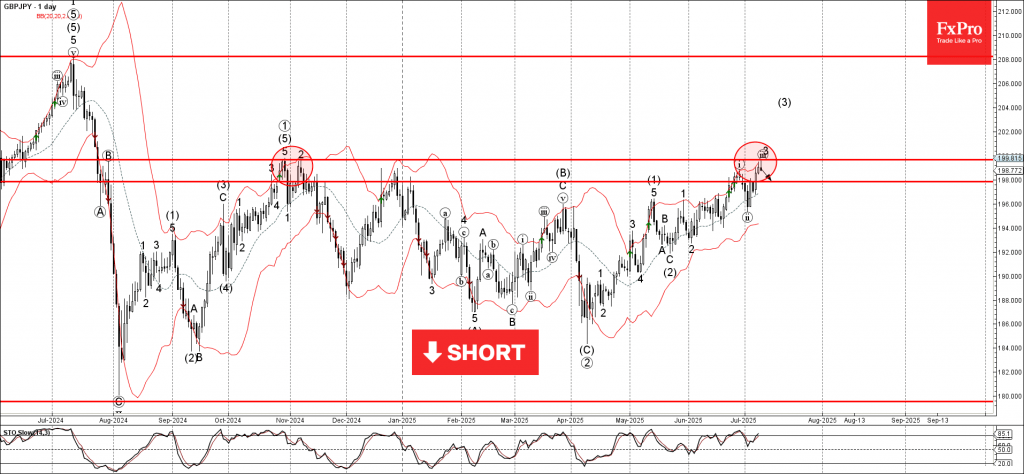

GBPJPY Wave Analysis

GBPJPY: ⬇️ Sell

- GBPJPY reversed from long-term resistance level 199.65

- Likely to fall to support level 198.00

GBPJPY currency pair recently reversed from the strong long-term resistance level 199.65 (former strong resistance from October, November and July) standing near the upper daily Bollinger Band.

The downward reversal from the resistance level 199.65 is likely to form the daily Shooting Star reversal pattern.

Given the bearish divergence on the daily Stochastic indicator and the strength of the resistance level 199.65, GBPJPY currency pair can be expected to fall to the next support level 198.00.

Sunset Market Commentary

Markets

Hardly any data on the agenda to inspire core markets’ trading today. There were also no new headlines from the likes of the UK or Japan highlighting debt sustainability concerns, allow the a momentum slowdown/pauze in the sell-off of ultra-long bonds. Time maybe for some technicals/nearby barriers to do their job. At 3.06%, the Japan 30-y yield has the all-time top (3.20%) in sight. For the UK 30-y yield (currently 4.46%), 4.50% is the final hurdle ahead of the April multi-decade top (5.66%). In this respect, BOE governor Bailey, in comments on the financial stability report, said that the Bank will reflect on curve steepening in the QT decision for the next 12 period starting in October. Similar pattern/nearby resistance for the 30-y German yield (currently at 3.16%, with the March top/2023 top at 3.25%). US yields over the previous week also joined the steepening move. However as markets are still pondering the chances of a resumption of the Fed easing cycle later this year, US (LT & ST) yields are developing in a more neutral/sideways trading pattern. The US 2-y (3.90%) and 10-y (4.40%) yield are a point in case of more sideways oriented ranges (respectively 3.70%/4.10% and 4.10%/6.65%) (cfr graphs infra). Even for the US 30-y yield, while nearing the 5% barrier, the technical resistance levels are somewhat further away (5.2% area). For (US) bond markets, the minutes of the June Fed meeting (this evening), a 10-y (also today) and especially a 30-y US Treasury auction (tomorrow) might provide some additional insight on the short-term market momentum regarding curve steepening. US yields are easing less than 2 bps. German yields ease by a similar ‘amount’. Consolidation, nothing more than that.

As was already was the case of late, the heavy flurry of trade(war) messages from president Trump again had hardly any lasting negative impact on global (FX, yields and equity) markets. Only specific markets (e.g. copper) showed a spike in volatility. Even so, we keep an eye at financial measures of US inflation expectations. E.g, the USD 10-y inflation swap this month rose about 10 bps (2.57%). Nothing really specular, but worth keeping an eye on. European equity markets in the meantime apparently still draw comfort (EuroStoxx +1.4%) from comments (Bloomberg, amongst others) that EU is close to a trade deal with rumored tailor-made exceptions for some sectors of even companies (Airbus, German carmakers with a US production). US equities open marginally higher (S&P 500 + 0.4%) with record levels within reach. On FX markets, USD moves are limited. The greenback maintains recent gains but fails to extend them (DXY 975, EUR/USD 1.171). Yen underperformance is tempering (USD/JPY 146.5).

News & Views

The Czech unemployment rate remained at 4.2% in June. Compared with a year ago, the jobless rate is now 0.6 ppts higher. When adjusting for seasonal effects, the jobless rate rose slightly to 4.5%. That’s the highest since 2017, signalling a gradual cooling of the labor market. This is primarily attributable to the downturn in manufacturing, which has been reducing employment for the third year in a row. In this respect KBC Economics views the latest industrial production data, which signal a stabilisation, with slight optimism. And considering new orders and improved business sentiment (eg. June PMI), it is also a key variable for further developments on the labour market and one of the important arguments why the domestic labour market should stabilise over time. In a broader perspective, KBC Economics’ sticks to the overall story of a continued recovery of the Czech economy with a 0.3% Q/Q growth expected in Q3.

China’s State Council unveiled new measures today to stabilize employment. These include expanded social insurance subsidies, special loans, and targeted support for young people looking for jobs. The support comes as the country’s domestic economy is struggling while the trade war with the US is weighing on the export sector. Latest unemployment figures showed China’s unemployment rate at a relatively low 5% in May after having hit a 2-year high at 5.4% in February. Youth unemployment, however, is far higher with the jobless rate for 16- to 24-year-olds (ex. students) coming in at 14.9% while that for 25- to 29-year-olds (ex. students) stands at 7%.

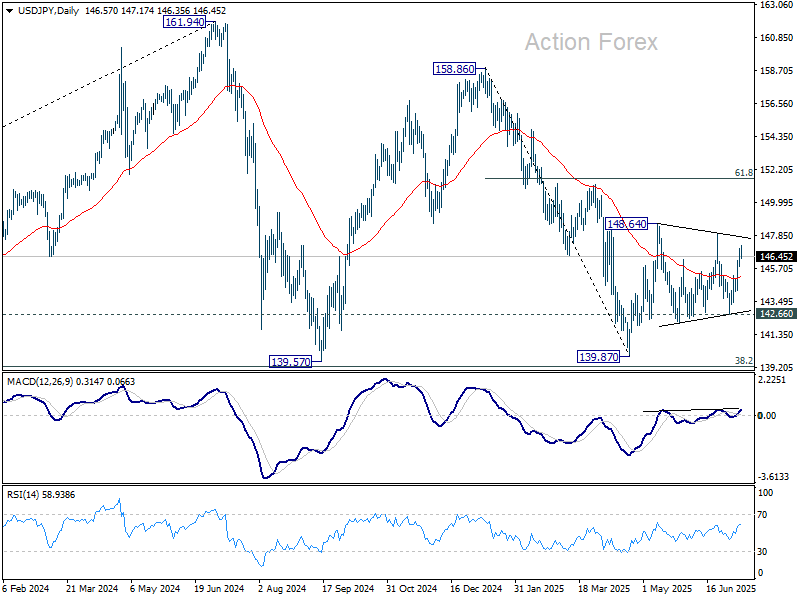

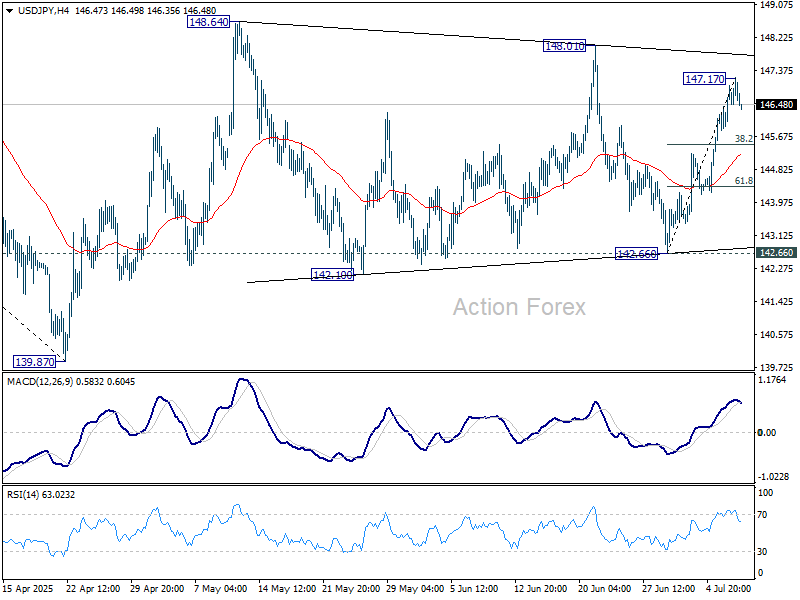

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.94; (P) 146.46; (R1) 147.09; More...

No change in USD/JPY's outlook as it's still bounded in range of 142.66/148.01 and intraday bias remains neutral. On the upside, firm break of 148.01 resistance will resume the rise from 139.87 to 61.8% retracement of 158.86 to 139.87 at 151.22. However, break of 142.66 will bring deeper fall back to retest 139.87 low.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

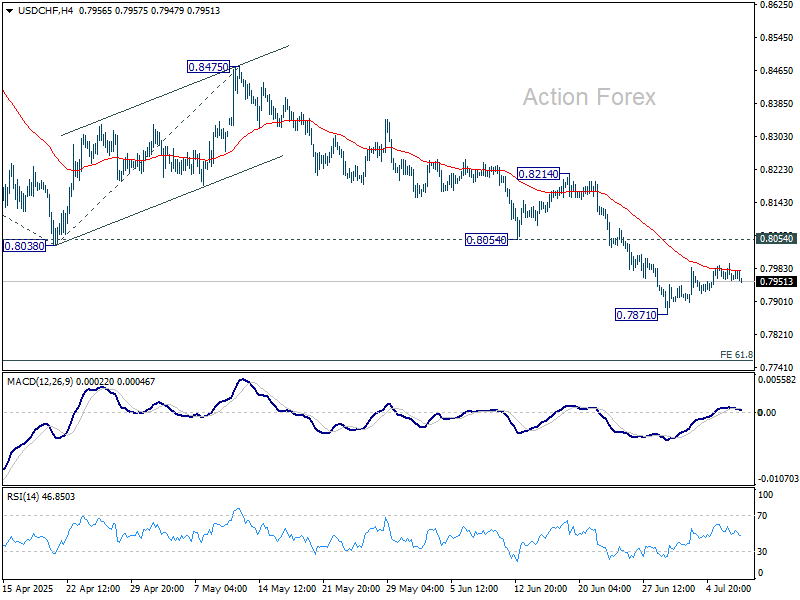

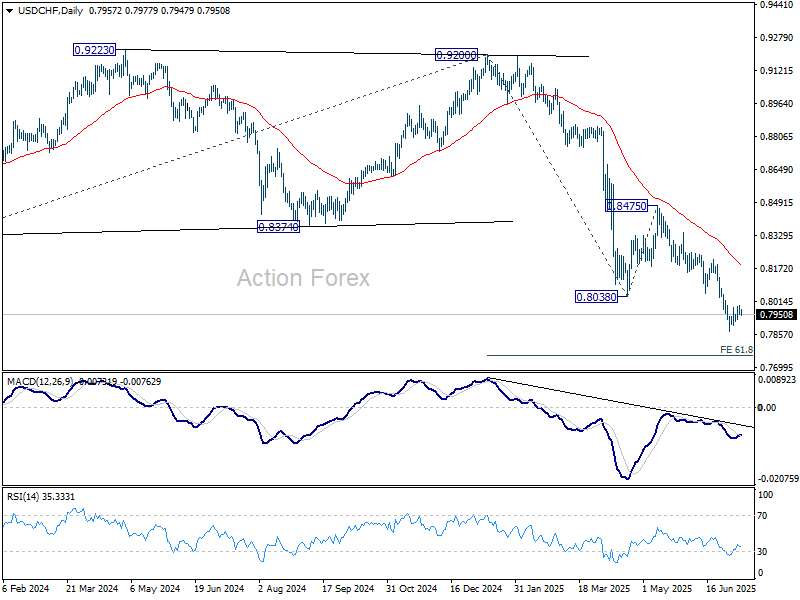

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7941; (P) 0.7968; (R1) 0.7983; More….

Outlook in USD/CHF is unchanged as consolidations continues above 0.7871. Intraday bias remains neutral at this point. While stronger recovery cannot be ruled out, upside should be limited by 0.8054 support turned resistance to bring another fall. Below 0.7871 will extend the larger down trend to 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757. Firm break there will pave the way to 100% projection at 0.7313 next.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

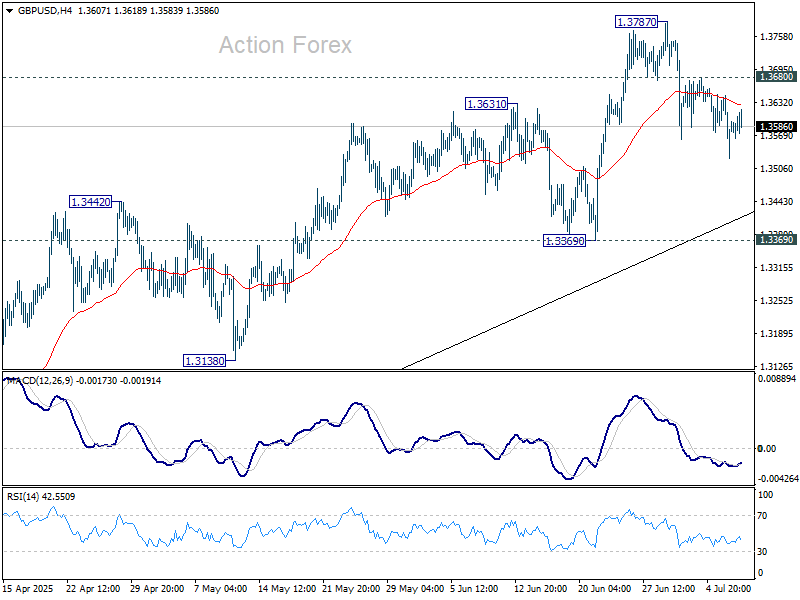

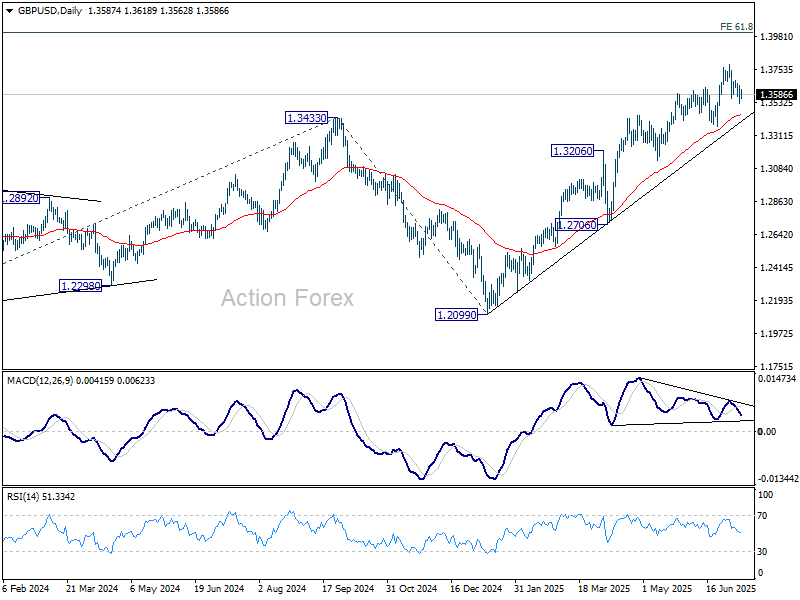

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3530; (P) 1.3589; (R1) 1.3651; More...

Intraday bias in GBP/USD remains neutral and correction from 1.3787 could extend lower. But downside should be contained by 1.3369 support to bring rebound. On the upside, above 1.3680 minor resistance will bring retest of 1.3787. Firm break of 1.3787 will resume larger up trend to 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2985) holds, even in case of deep pullback.

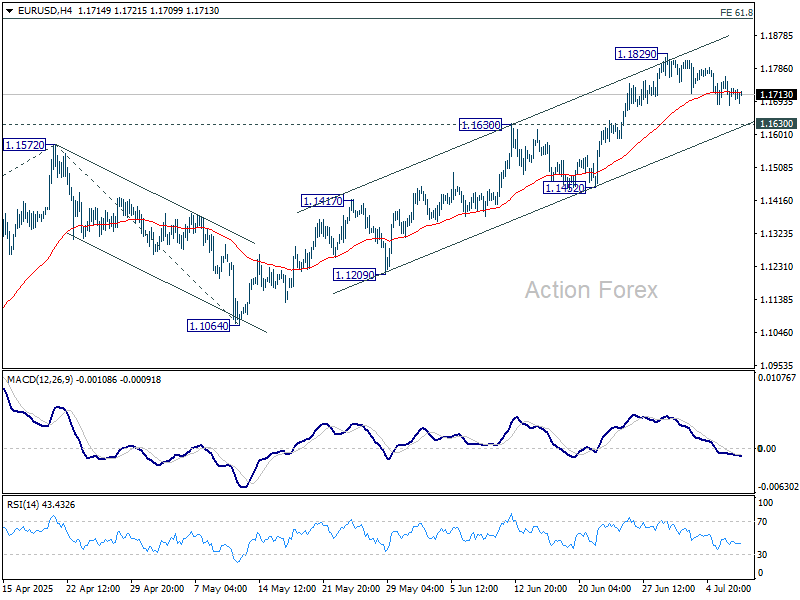

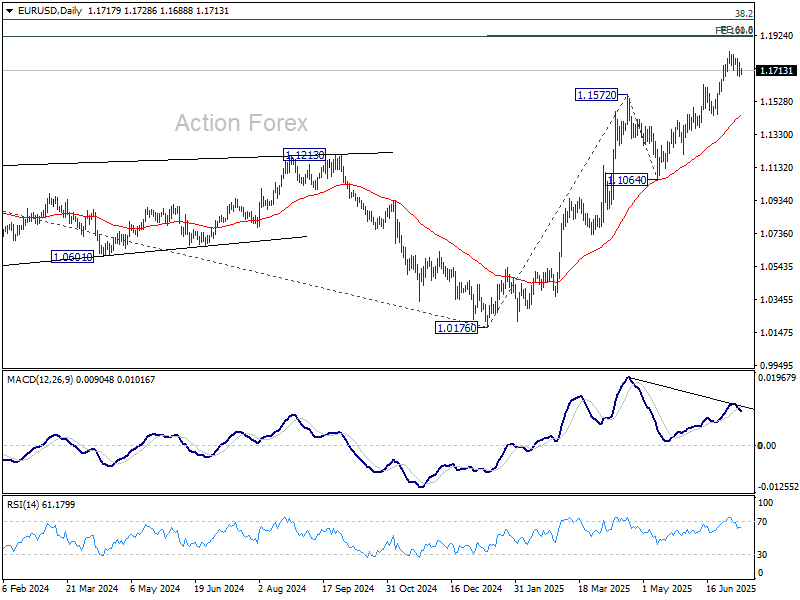

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1684; (P) 1.1724; (R1) 1.1766; More...

EUR/USD's consolidation from 1.1829 is still extending and intraday bias stays neutral. Downside should be contained by 1.1630 resistance turned support to bring rebound. On the upside, firm break of 1.1829 will resume the rise from 1.0176 and target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

Dollar Pauses as Markets Await FOMC Minutes, Overall Action Muted

Activity in the forex market cooled today as traders adopted a cautious stance ahead of June FOMC minutes. With no major surprises expected, the minutes are unlikely to shift current expectations for a Fed hold at the July 30 meeting. That baseline has been reinforced by the latest shift in trade war dynamics, after US President Donald Trump effectively pushed the tariff truce deadline back to August 1.

The new deadline means Fed will be making its next rate decision before key developments on trade materialize, leaving the central bank in the dark on one of the most important macro variables. With clarity on tariffs likely delayed, Fed officials have even more reason to stick with their current wait-and-see approach. The FOMC minutes may still offer insight into how dovish policymakers like Governor Christopher Waller and Michelle Bowman are positioning, but the broad tone is expected to remain cautious.

On trade, Trump said Tuesday evening that at least seven new tariff letters would be issued Wednesday morning, with more to follow later in the day. He also indicated the EU would be informed of its specific tariff rate “probably” within two days, but added that Brussels had grown more cooperative in recent talks.

European Commission President Ursula von der Leyen maintained a guarded tone, reaffirming that the bloc is working in good faith to strike a deal but remains prepared for all scenarios. A Commission spokesperson said talks were advancing and a deal could potentially be reached before the August 1 deadline.

In terms of currency performance, Dollar continues to lead for the week, although it’s struggling to build further momentum, especially against European majors. Swiss Franc and British Pound remain firm, while the Japanese Yen lags sharply. New Zealand and Canadian Dollars are also under pressure, while Euro and Australian Dollar sit in the middle.

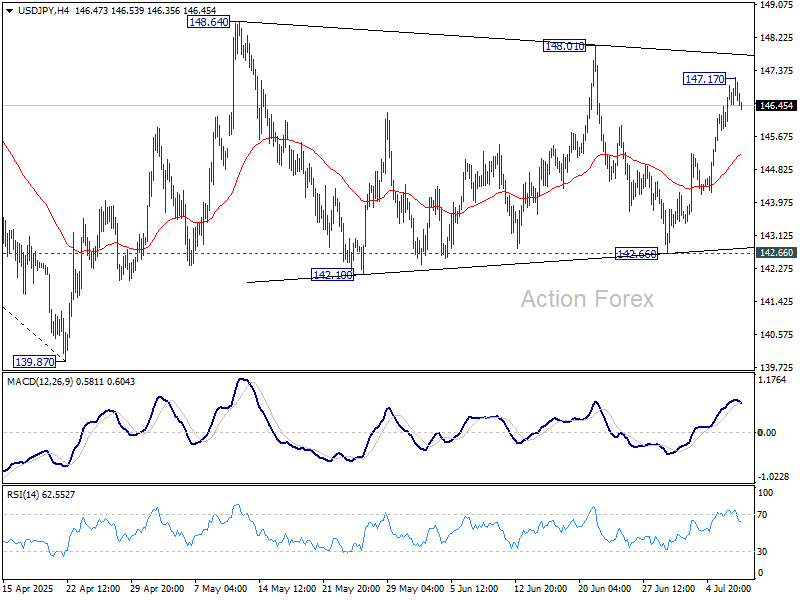

Technically, USD/JPY’s rally from 142.66 appears to be losing steam after hitting 147.17. A short-term pullback is increasingly likely. Recent price action suggests a triangle formation from 148.64, and the next dip may complete that pattern as the fifth leg. Downside would be contained by 61.8% retracement of 142.66 to 147.17 at 144.38. The pair should then be ready to rise through 148.64 to resume the whole rebound from 139.87. Let's see if it unfolds this way.

In Europe, at the time of writing, FTSE is up 0.09%. DAX is up 1.26%. CAC is up 1.32%. UK 10-year yield is down -0.013 at 4.623. Germany 10-year yield is down -0.012 at 2.68. Earlier in Asia, Nikkei rose 0.33%. Hong Kong HSI fell -1.06%. China Shanghai SSE fell -0.13%. Singapore Strait Times rose 0.25%. Japan 10-year JGB yield rose 0.016 to 1.507.

ECB’s Lane: Global uncertainty goes beyond tariffs, includes investment and security risks

ECB Chief Economist Philip Lane said in a speech today that the recent 25bps rate cut was necessary to prevent temporary inflation undershoots from becoming persistent. Speaking about the June policy decision, Lane emphasized the influence of falling energy prices, a stronger Euro, and a deteriorating materially changed outlook on ECB’s latest projections.

He also highlighted growing uncertainty over the international trade system, citing risks that extend beyond tariffs to include new non-tariff barriers, shifts in investment frameworks, and increased convergence between economic and national security policies.

Against this backdrop, Lane reaffirmed the ECB’s "meeting-by-meeting". He stressed that "data dependence also extends to the incoming data on policy settings outside the monetary domain", since shifts in international and domestic policy regimes are highly relevant for future inflation dynamics.

BoE's Bailey warns of financial vulnerabilities amid global fragmentation

BoE Governor Andrew Bailey cautioned on Wednesday that risks tied to geopolitical tensions and the fragmentation of global trade and financial markets remain high. Speaking on the evolving macroeconomic development, Bailey said the world economy faces “material uncertainty,” and warned that some geopolitical threats have already begun to crystallize, impacting financial market behavior.

He noted a “notable change” in the usual correlations between the US Dollar and other US assets such as equities and Treasury yields. This breakdown, Bailey warned, increases the likelihood of sharp corrections in risk assets, abrupt shifts in allocation, and prolonged periods of market dislocation. Such dynamics could expose vulnerabilities in market-based finance and ripple into the UK by tightening the availability and cost of credit.

Bailey also stressed that trade fragmentation, while geopolitical in nature, has clear economic consequences. “Fragmenting the world economy is bad for activity,” he said, citing basic trade theory. The knock-on effects, he added, would likely weigh on employment and global growth.

RBNZ holds at 3.25%, signals easing path remains open

RBNZ left its Official Cash Rate unchanged at 3.25% on Wednesday, in line with market expectations, but maintained a clear easing bias in its statement.

While headline inflation is projected to briefly rise toward the top of the 1–3% target band by mid-2025, policymakers expect it to return near 2% by early 2026, supported by spare economic capacity and waning domestic price pressures.

The policy path forward remains clouded by global headwinds, sue to rising tariff tensions and geopolitical uncertainty.

The statement noted that "If medium-term inflation pressures continue to ease as projected, the Committee expects to lower the Official Cash Rate further."

China CPI turns positive, but PPI slump deepens

China’s consumer inflation returned to positive territory in June for the first time in five months, with headline CPI rising 0.1% yoy, above expectations of -0.1% yoy. The improvement was driven by a 0.7% annual rise in core CPI — the strongest core reading since April 2024. The data suggests a modest pickup in domestic demand, although the pace remains fragile as headline inflation is barely above zero.

On the producer side, deflation deepened. PPI fell -3.6% yoy, marking its sharpest drop since July 2023 and extending a nearly three-year deflationary streak. The continued subdued industrial demand reflects the challenges facing China’s manufacturing sector.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1684; (P) 1.1724; (R1) 1.1766; More...

EUR/USD's consolidation from 1.1829 is still extending and intraday bias stays neutral. Downside should be contained by 1.1630 resistance turned support to bring rebound. On the upside, firm break of 1.1829 will resume the rise from 1.0176 and target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

ECB’s Lane: Global uncertainty goes beyond tariffs, includes investment and security risks

ECB Chief Economist Philip Lane said in a speech today that the recent 25bps rate cut was necessary to prevent temporary inflation undershoots from becoming persistent. Speaking about the June policy decision, Lane emphasized the influence of falling energy prices, a stronger Euro, and a deteriorating materially changed outlook on ECB’s latest projections.

He also highlighted growing uncertainty over the international trade system, citing risks that extend beyond tariffs to include new non-tariff barriers, shifts in investment frameworks, and increased convergence between economic and national security policies.

Against this backdrop, Lane reaffirmed the ECB’s "meeting-by-meeting". He stressed that "data dependence also extends to the incoming data on policy settings outside the monetary domain", since shifts in international and domestic policy regimes are highly relevant for future inflation dynamics.