Sample Category Title

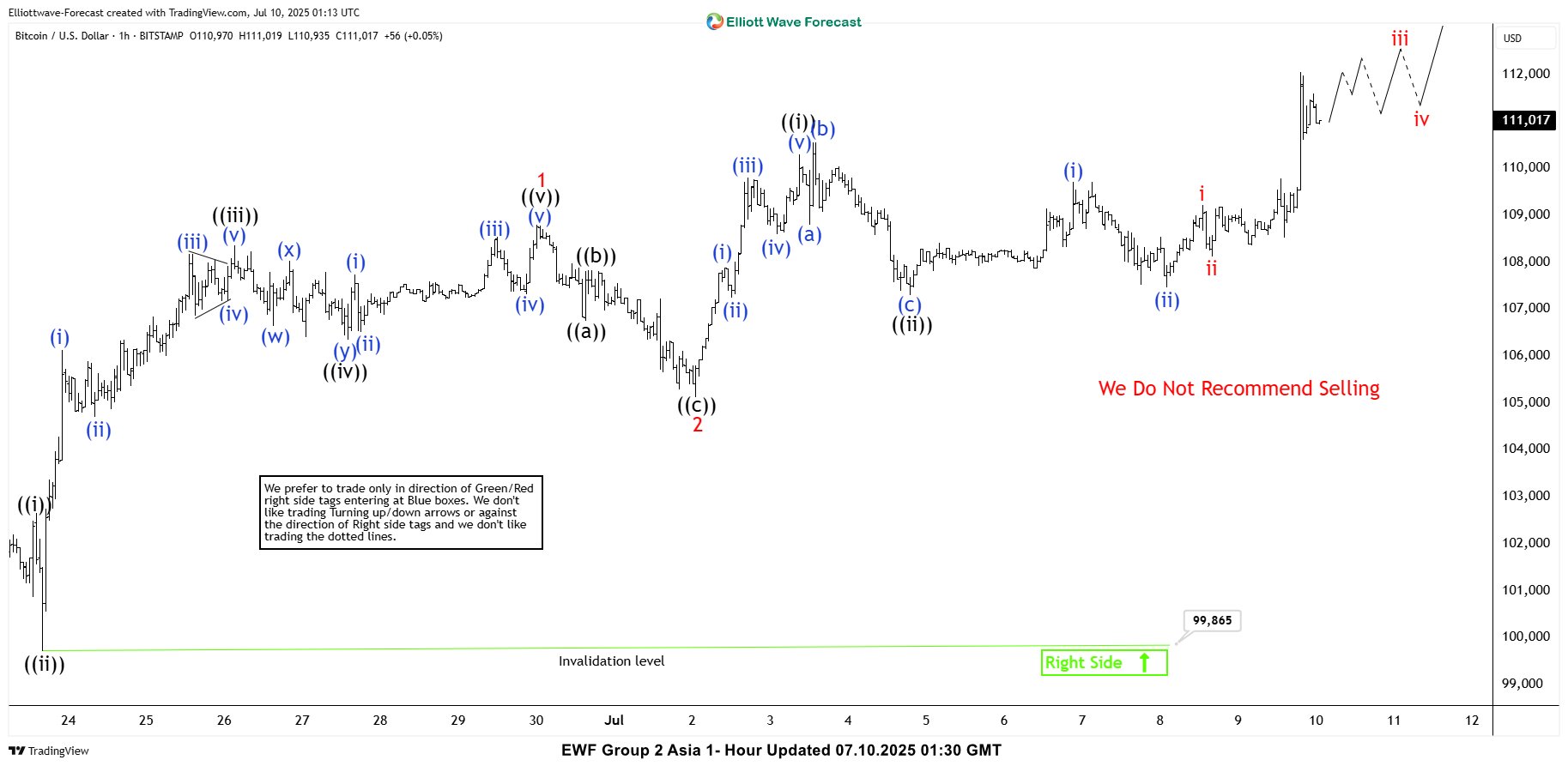

Elliott Wave View: Bitcoin (BTCUSD) Breaking to New All Time High

Bitcoin (BTCUSD) has recently achieved a new all-time high, signaling the onset of the next upward phase in its price trajectory. From the significant low recorded on June 22, 2025, at $98,240, Bitcoin has exhibited a robust five-wave advance, reinforcing the bullish outlook. This rally aligns with a classic five-wave impulse structure per Elliott Wave theory, a framework often used to forecast market trends. Starting from the June 22 low, wave ((i)) peaked at $102,647. It was then followed by a corrective pullback in wave ((ii)) to $99,865. The cryptocurrency then surged in wave ((iii)) to $108,358. Wave ((iv)) concluded at $106,351 after a brief dip. The final leg, wave ((v)), culminated at $108,800, completing wave 1 of a higher-degree impulse.

Subsequently, Bitcoin experienced a wave 2 correction, retreating to $105,130. From this level, it has begun nesting higher in wave 3. This is a phase often associated with strong momentum. Within this structure, wave ((i)) reached $110,292. Wave ((ii)) pullback followed to $107,303, forming an expanded flat pattern. Further subdividing, wave (i) peaked at $109,717, with wave (ii) dips concluding at $107,471. In the near term, as long as the pivotal low at $99,865 remains intact, any pullbacks are likely to attract buyers in a 3, 7, or 11-swing sequence, supporting further upside. This technical setup suggests Bitcoin’s bullish momentum is far from exhausted, with higher levels anticipated as the wave structure continues to unfold.

Bitcoin (BTCUSD) 60-Minute Elliott Wave Technical Chart

BTCUSD Elliott Wave Technical Video

https://www.youtube.com/watch?v=lTeB1IL6ZyA

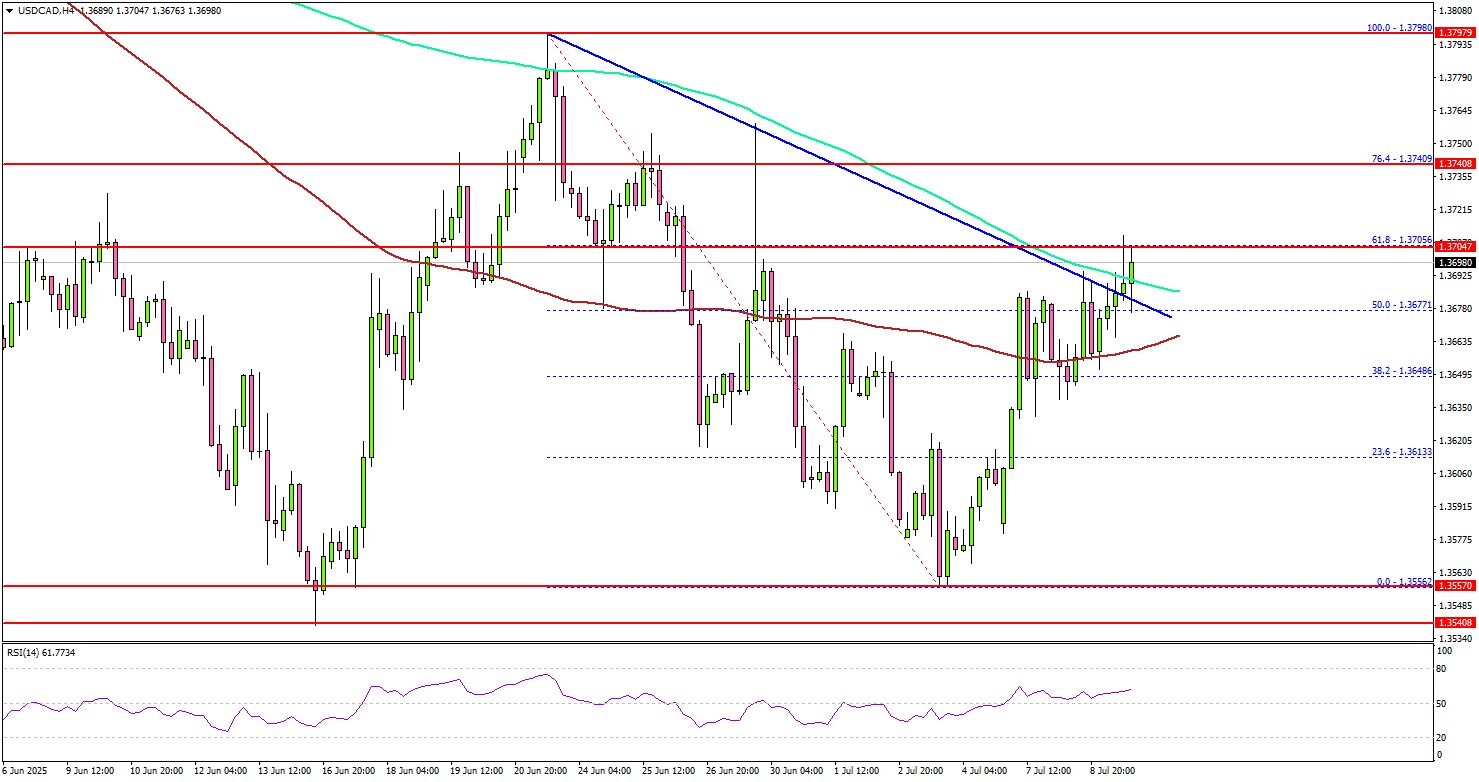

USD/CAD Gears Up — Bullish Momentum Could Take Over Soon

Key Highlights

- USD/CAD started a fresh increase above the 1.3650 resistance.

- It cleared a key bearish trend line with resistance at 1.3675 on the 4-hour chart.

- EUR/USD is slowly moving lower and might test the 1.1650 zone.

- GBP/USD is struggling to restart gains above the 1.3650 level.

USD/CAD Technical Analysis

The US Dollar found support at 1.3550 against the Canadian Dollar. USD/CAD broke the 1.3620 and 1.3650 levels to enter a positive zone.

Looking at the 4-hour chart, the pair cleared a key bearish trend line with resistance at 1.3675, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). There was a move above the 50% Fib retracement level of the downward move from the 1.3798 swing high to the 1.3556 low.

On the upside, the pair could face resistance near the 1.3700 level. The next key resistance sits near the 1.3740 level. A close above the 1.3740 level could set the pace for another increase.

In the stated case, the pair could even clear the 1.3780 resistance. The next major stop for the bulls could be near the 1.3800 resistance.

On the downside, immediate support is near the 1.3660 level. The next key support sits near 1.3640. Any more losses could send the pair toward the 1.3620 support zone.

Looking at EUR/USD, the pair started a short-term downside correction and might decline toward the 1.1650 level.

Upcoming Economic Events:

- Fed's Musalem speech.

- US Initial Jobless Claims - Forecast 235K, versus 233K previous.

Japan’s PPI slows to 2.9% yoy in June, stronger Yen helps ease import costs

Japan's Producer Price Index rose 2.9% yoy in June, easing from May’s 3.3% yoy pace and in line with expectations. The slowdown reflects a moderation in upstream price pressures, as firms begin to benefit from a firmer Yen.

Yen-based import price index dropped -12.3% yoy from a year earlier, deepening from May’s -10.3% yoy fall and signaling that Japan’s currency rebound is dampening raw material costs. Food and beverage prices remained elevated with a 4.5% yoy increase, largely due to persistently high rice costs, though that was slightly softer than the prior month’s 4.7% yoy rise.

Fed minutes reveal deep division on rate path

Minutes from the FOMC’s June 17–18 meeting highlighted a notable divergence among policymakers on whether rate cuts are needed this year. "Most participant" still see at least one cut as likely, citing temporary tariff effects, stable inflation expectations, and signs of cooling in the labor market. "A couple" went further, indicating they would be open to a rate cut at the upcoming July meeting if economic data confirms their outlook.

However, "some participants" pushed back against easing and suggested ""no reductions" this year, pointing to stubbornly high inflation and warning of upside risks. They argued that "upside risks to inflation remained meaningful", with businesses and consumers still expecting higher prices, and with economic activity holding up, rate cuts could be premature. Several added that "may not be far above its neutral level", diminishing the case for near-term action.

Participants generally agreed that risks of both elevated inflation and a weakening labor market have eased somewhat, but remain elevated. "Some" emphasized inflation risks as still "more prominent", while "a few" flagged labor market deterioration as the more pressing concern. The broad message from the minutes was one of uncertainty, with many policymakers seeing the need take a "careful approach" in adjusting monetary policy.

(FED) Minutes of the Federal Open Market Committee

June 17–18, 2025

A joint meeting of the Federal Open Market Committee and the Board of Governors of the Federal Reserve System was held in the offices of the Board of Governors on Tuesday, June 17, 2025, at 9:00 a.m. and continued on Wednesday, June 18, 2025, at 9:00 a.m.1

Review of Monetary Policy Strategy, Tools, and Communications

Committee participants continued their discussions related to their review of the Federal Reserve's monetary policy framework, with a focus on issues related to assessing the risks and uncertainty that are relevant for monetary policy and the potential implications of these issues for the FOMC's policy strategy and communications. The staff reviewed qualitative and quantitative tools that are commonly used to measure uncertainty about the economic outlook and the balance of risks, drawing on U.S. and international experience. The staff then discussed monetary policy strategies that aim to be robust to a variety of economic environments and ways in which risk-management considerations can be incorporated into monetary policy analysis and decisionmaking. The staff also considered the role of scenario analysis as a tool to communicate to the public risks and uncertainty around the economic outlook and their implications for monetary policy.

Participants noted that risks and uncertainty are important factors affecting their decisionmaking and emphasized the need for a policy strategy that aims to achieve the Committee's maximum-employment and price-stability objectives across a wide range of highly uncertain developments. Participants acknowledged that risks and uncertainty about the economy are pervasive and pose challenges to both the design and communication of monetary policy. They remarked that measuring and assessing risks and uncertainty are difficult and that the Committee has been well served by relying on a wide range of indicators, as well as information from business and community contacts, to gauge evolving risks, especially during periods of heightened uncertainty.

Participants remarked that effective communications about risks and uncertainty help the public understand the Committee's decisions and enhance the transparency, accountability, and effectiveness of monetary policy decisions. Participants had a preliminary discussion about a range of issues related to enhancing the Committee's suite of communication tools, including possible changes to the Summary of Economic Projections (SEP) and a potential broader use of alternative scenarios. Participants highlighted, however, the challenges associated with adjustments to these tools and noted that any revisions to the Committee's communication policies would need to be considered carefully and receive broad support across participants.

Participants agreed to continue their discussions of ways to enhance the Committee's communication tools and practices once they completed their review of their Statement on Longer-Run Goals and Monetary Policy Strategy. Participants expected that they would complete that review by late summer.

Developments in Financial Markets and Open Market Operations

The manager turned first to a review of financial market developments. Over the intermeeting period, policy expectations and Treasury yields rose modestly, credit spreads narrowed, and equity prices increased. Markets were attentive to the de-escalation of trade tensions; generally weaker-than-expected economic data releases, with the notable exception of the May employment report; and prospects for fiscal expansion. These factors, on net, resulted in some paring back of investors' perception of downside risk to growth and upside risk to inflation. Results from the Open Market Desk's Survey of Market Expectations were consistent with this interpretation: The median respondent's expectations for real gross domestic product (GDP) growth and personal consumption expenditures (PCE) inflation for 2025 retraced some of the moves that occurred after the April tariff announcements, though growth expectations were still materially lower and inflation expectations remained higher relative to the March survey.

The median respondent's modal path for the federal funds rate in the June survey shifted higher through 2026 and implied two 25 basis point rate cuts both this year and next year. Market-based policy expectations were largely consistent with survey results, with both the futures-based average federal funds rate path and the options-based modal federal funds rate path shifting higher over the intermeeting period. Overall, the changes in the intermeeting period brought policy expectations for the next few quarters back close to where they stood at the time of the March FOMC meeting. However, futures-based policy expectations beyond the next few quarters had not fully retraced the decline seen over the previous intermeeting period, suggesting that perceived medium- and longer-term downside risks to growth remained larger than before the April tariff announcements. Nominal Treasury yields rose 15 to 20 basis points, on net, over the intermeeting period. The manager observed that the rise in shorter-maturity yields was consistent with the upward shift in the expected policy rate path. The rise in longer-maturity yields appeared to reflect, in part, market participants' increasing fiscal concerns: In response to a Desk survey question about the top factors behind the respondents' forecast of the 10-year yield over the next two years, the fiscal outlook was the factor cited by the largest number of respondents.

Market-implied inflation compensation for the year ahead fell about 20 basis points over the intermeeting period, while longer-term inflation compensation measures were little changed. Liquidity conditions for nominal Treasury securities had improved as volatility declined following the stress seen in the previous intermeeting period. The events of April, and the more recent focus in markets around fiscal sustainability issues, did not appear to have affected demand for Treasury securities at auction; an index of auction performance derived from a number of metrics indicated that auction performance had improved modestly over the past several quarters and was currently in line with the longer-run average.

Regarding foreign exchange developments, the broad trade-weighted dollar index fell further during the intermeeting period despite increases in U.S. equity prices and short-term Treasury yields. The manager noted that dollar depreciation continued to be consistent with larger downside revisions to the U.S. growth outlook relative to other major economies, which induced increased currency hedging flows by foreign investors in U.S. assets. The manager also remarked that the sensitivity of the foreign exchange value of the dollar to domestic economic surprises had not fundamentally changed. The available data continued to suggest stability in foreign holdings of U.S. assets.

The manager turned next to money markets and Desk operations. Unsecured overnight rates remained stable over the intermeeting period. Rates in the repurchase agreement (repo) market were softer relative to the previous intermeeting period, including at the May month-end, as reductions in net Treasury bill issuance amid the ongoing debt limit situation resulted in increased demand for repo. With the softness in repo making the overnight reverse repurchase agreement (ON RRP) facility more attractive on a relative basis, usage of the ON RRP facility had been broadly stable, except for the typical spike at month-end. Since the start of the debt issuance suspension period in January, the Treasury General Account (TGA) had declined nearly $420 billion, ON RRP balances had increased about $75 billion, and reserves had increased $150 billion. Key indicators continued to suggest that reserves, which stood at nearly $3.5 trillion, were well into the abundant range. Once the debt limit was addressed, however, the TGA was likely to be rebuilt fairly quickly, which would drain liquidity from the system and result in fast declines in both ON RRP and reserve balances.

The manager also discussed the trajectory of the System Open Market Account (SOMA) portfolio. Since balance sheet runoff commenced in June 2022, SOMA securities holdings had fallen almost $2-1/4 trillion. As a percentage of GDP, the portfolio had declined to close to where it had been at the start of the pandemic. The corresponding drain in Federal Reserve liabilities had largely come out of balances at the ON RRP facility, while reserve levels had been relatively little changed over that period. Respondents to the June Desk survey, on average, expected runoff to end in February of next year, a month later compared with the previous survey, with an expected size of the SOMA portfolio of $6.2 trillion, or about 20 percent of GDP. At that point, the respondents, on average, expected reserves to be at $2.9 trillion and the ON RRP balance to be low.

The manager noted that, starting on June 26, the Desk will begin adding regular morning standing repo facility (SRF) operations to the existing afternoon operations. The additional operations are intended to further enhance the effectiveness of the SRF in its ability to support monetary policy implementation and smooth market functioning.

By unanimous vote, the Committee ratified the Desk's domestic transactions over the intermeeting period. There were no intervention operations in foreign currencies for the System's account during the intermeeting period.

Staff Review of the Economic Situation

The information available at the time of the meeting indicated that consumer price inflation remained somewhat elevated. The unemployment rate continued to be low, and labor market conditions were solid. Available indicators suggested that real GDP was expanding at a solid pace in the second quarter.

Total consumer price inflation—as measured by the 12-month change in the PCE price index—was estimated to have been 2.3 percent in May, based on the consumer and producer price indexes. Core PCE price inflation, which excludes changes in consumer energy prices and many consumer food prices, was 2.6 percent in May. Both total and core inflation were lower than at the beginning of the year. Survey-based measures of short-term inflation expectations remained high, although the extent of increases in recent months had varied considerably and some measures had declined somewhat in May and June. Most survey-based measures of longer-term inflation expectations had held steady.

Recent data indicated that labor market conditions had remained solid. The unemployment rate was 4.2 percent in May, the same as in the previous two months. The labor force participation rate and the employment-to-population ratio moved down in May but remained near their levels since the beginning of the year. Total nonfarm payrolls increased at a solid pace in May, a little above the average monthly rate over the previous four months. The ratio of job vacancies to unemployed job seekers was unchanged at 1.0 in May. Average hourly earnings for all employees rose 3.9 percent over the 12 months ending in May, a little lower than a year earlier.

Recent information suggested that real GDP was rising in the second quarter, after it had declined slightly in the previous quarter. Real private domestic final purchases—which comprises PCE and private fixed investment and which often provides a better signal than GDP of underlying economic momentum—had increased solidly in the first quarter and appeared to be expanding further in the second quarter. Indicators for consumer spending, such as retail sales and motor vehicle purchases through May, pointed to solid PCE growth in the second quarter. Business fixed investment (BFI) rose markedly in the first quarter, apparently boosted by a pull-forward of imported capital goods in anticipation of tariff increases, and incoming data suggested that BFI was rising modestly in the second quarter.

International trade flows continued to be volatile amid substantial shifts in U.S. tariffs. After surging in the first quarter ahead of expected tariff hikes, U.S. imports—especially of consumer goods—declined sharply in April. That decline suggested that the front-loading of imports had stopped after the introduction of broad-based tariffs in early April. By contrast, U.S. exports firmed in April. In mid-May, the U.S. and China agreed to a 90-day reduction in bilateral tariffs, and recent indicators suggested that this change led to a rebound in trade flows.

Economic growth abroad picked up in the first quarter, lifted by the surge in shipments to the U.S.—especially from Europe and Asia excluding China—in anticipation of tariff hikes. More recent indicators pointed to a slowdown in foreign economic activity in the second quarter, partly reflecting lower exports to the U.S. and the effects of elevated uncertainty about the course of global trade policies.

Inflation abroad remained near central bank targets in many foreign economies, although recent data showed renewed inflationary pressures in some countries, notably in Mexico. By contrast, inflation in China remained subdued.

Many foreign central banks eased policy during the intermeeting period, citing concerns about economic growth and, in some cases, further progress on restoring price stability. In their communications, foreign central banks continued to emphasize the need to maintain policy flexibility amid substantial risks and uncertainty.

Staff Review of the Financial Situation

Despite a weakening of near-term inflation pressures, the market-implied path of the federal funds rate over the next year increased over the intermeeting period with improvements in the economic outlook amid a general easing in trade tensions. Near-term inflation compensation declined, while longer-term inflation compensation was little changed. Nominal and real Treasury yields increased moderately, on net, across the maturity spectrum.

Consistent with improving risk sentiment from recent trade developments, broad equity price indexes increased markedly, and credit spreads tightened. Credit spreads narrowed to very low levels relative to their historical distribution, except for the lowest-quality corporate bonds, which stood close to the median of their distribution. The VIX—a forward-looking measure of near-term equity market volatility—declined moderately.

The reduction in trade policy tensions between the U.S. and China led to an improvement in global economic growth prospects and lifted investor risk sentiment. The military conflict between Israel and Iran left only a limited imprint outside of energy markets. On net, equity indexes and market-based policy rate expectations increased in most major foreign economies. The dollar depreciated a bit further.

Conditions in U.S. short-term funding markets remained stable. After increasing over the previous intermeeting period because of incoming tax receipts, the TGA had resumed its decline in response to actions associated with the ongoing federal debt limit situation. Average usage of the ON RRP facility was little changed. Rates in secured markets were, on average, slightly below the effective federal funds rate, likely reflecting low Treasury bill supply.

In domestic credit markets, borrowing costs for businesses, households, and municipalities mostly edged down but remained elevated. Yields on both corporate bonds and leveraged loans declined modestly. Interest rates on small business loans decreased in May. Yields on higher-rated tranches of commercial mortgage-backed securities (CMBS) were little changed or increased slightly, whereas yields on lower-rated CMBS tranches declined, notably so for non-agency securities. Rates on 30-year fixed-rate conforming residential mortgages were little changed and remained elevated. Interest rates on credit card offers ticked up in March and April, while rates on new auto loans were little changed in May.

Financing through capital markets and nonbank lenders was readily accessible for public corporations and large and middle-market private corporations. Issuance of nonfinancial corporate bonds and leveraged loans, which slowed in April, was solid in May and early June, and private credit continued to be broadly available in April and May. Regarding bank credit, commercial and industrial loan growth picked up in April but moderated in May. Commercial real estate (CRE) loan growth was modest in April and May.

Credit remained available for most households. In the residential mortgage market, credit continued to be easily available for high-credit-score borrowers but was tighter for low-credit-score borrowers despite easing slightly in May. Growth in consumer loan balances at banks was robust in April and May.

Credit quality remained solid for large-to-midsize firms, municipalities, and most categories of mortgages, but delinquency rates continued to be somewhat elevated in other sectors. The credit performance of corporate bonds and leveraged loans remained stable in May. Delinquency rates on small business loans in March and April stayed above pre-pandemic levels. In the CRE market, CMBS delinquency rates remained elevated in May. Regarding household credit quality, the rate of serious delinquencies on Federal Housing Administration mortgages remained above pre-pandemic levels in April. By contrast, delinquency rates on most other mortgage loan types continued to stay near historical lows. In the first quarter, credit card and auto loan delinquency rates remained at elevated levels. Student loan delinquencies reported to credit bureaus shot up in the first quarter of the year after the expiration of the on-ramp period for student loan payments and were expected to climb further over the next few quarters. While delinquent student loan borrowers have not shown greater difficulty in meeting other debt payments so far, debt collections on defaulted student loans later this year could boost delinquency rates on other debt.

Staff Economic Outlook

The staff projection of real GDP growth for this year through 2027 was higher than the one prepared for the May meeting, primarily because trade policy announcements led the staff to reduce their assumptions about effective tariff rates relative to those in their previous forecast. With that improved economic outlook, labor market conditions were not expected to weaken as much as in the previous projection, though the unemployment rate was still forecast to rise somewhat through next year and to run a little above the staff's estimate of its natural rate through 2027.

The staff's inflation projection was lower than the one prepared for the May meeting. Tariff increases were expected to raise inflation this year and to provide a small boost in 2026. Inflation was projected to decline to 2 percent by 2027.

The staff continued to view the uncertainty around their economic outlook as elevated, primarily reflecting the uncertainty surrounding changes to trade, fiscal, immigration, and regulatory policies and the associated economic effects. In addition to the baseline forecast, the staff had prepared a number of alternative economic scenarios. The staff judged the risks around the projections of real GDP growth and employment as still skewed to the downside, though they saw the risk of a recession as less than at the time of their previous forecast. The staff continued to view the risks around the inflation forecast as skewed to the upside, as the projected rise in inflation this year could be more persistent than assumed in the baseline projection.

Participants' Views on Current Conditions and the Economic Outlook

In conjunction with this FOMC meeting, participants submitted their projections of the most likely outcomes for real GDP growth, the unemployment rate, and inflation for each year from 2025 through 2027 and over the longer run. The projections were based on participants' individual assessments of appropriate monetary policy, including their projections of the federal funds rate. The longer-run projections represented each participant's assessment of the rate to which each variable would tend to converge under appropriate monetary policy and in the absence of further shocks to the economy. Participants also provided their individual assessments of the level of uncertainty and the balance of risks associated with their projections. The SEP was released to the public after the meeting.

Participants noted that the available data showed that economic growth was solid and the unemployment rate was low. Participants observed that inflation had come down but remained somewhat elevated. Growth in consumer spending and business investment had been solid, though many participants observed that measures of household and business sentiment remained weak. Participants judged that uncertainty about the outlook was elevated amid evolving developments in trade policy, other government policies, and geopolitical risks, but that overall uncertainty had diminished since the previous meeting. Some participants commented that high uncertainty had the potential to restrain economic activity, including private-sector hiring, in the near term. Participants judged that there were downside risks to employment and economic activity and upside risks to inflation, but that these risks had decreased as expectations about effective tariff rates and their effects had declined from levels in April.

Participants observed that inflation had eased significantly since its peak in 2022 but remained somewhat elevated relative to the Committee's 2 percent longer-run goal. Participants noted that the progress in returning inflation to target had continued even though that progress had been uneven. Some participants observed that services price inflation had moved down recently, while goods price inflation had risen. A few participants noted that there had been limited progress recently in reducing core inflation. Some participants noted that geopolitical developments in the Middle East posed an upside risk to energy prices.

In discussing their outlooks for inflation, participants noted that increased tariffs were likely to put upward pressure on prices. There was considerable uncertainty, however, about the timing, size, and duration of these effects. Many observed that it might take some time for the effect of higher tariffs to be reflected in the prices of final goods because firms might choose not to raise prices on affected goods and services until they had run down inventories of products imported before the increase in tariffs or because it would take some time for tariffs on intermediate goods to work through the supply chain. Several participants commented that upward pressure on prices could be greater if tariffs disrupted supply chains or acted as a drag on productivity. Many participants noted that the eventual effect of tariffs on inflation could be more limited if trade deals are reached soon, if firms are able to quickly adjust their supply chains, or if firms can use other margins of adjustment to reduce their exposure to the effects of tariffs. Several participants noted that firms not directly subject to tariffs might take the opportunity to increase their prices if other prices rise, particularly those of complementary products. Participants relayed a range of assessments from their business contacts regarding the extent to which tariff-related cost increases would be passed on to consumers. Several participants observed that the pass-through of tariffs might be limited if households and businesses exhibit a low tolerance for price hikes or if firms seek to increase their market share as others raise their prices. A few participants noted that the pass-through of tariff-related costs likely would be greater for smaller businesses or businesses with narrow profit margins.

Participants noted that longer-term inflation expectations continued to be well anchored and that it was important they remain so. Several participants commented that shorter-term inflation expectations had been elevated and that this development had the potential to spill over into longer-term expectations or to affect price and wage setting in the near term. While a few participants noted that tariffs would lead to a one-time increase in prices and would not affect longer-term inflation expectations, most participants noted the risk that tariffs could have more persistent effects on inflation, and some highlighted the fact that such persistence could also affect inflation expectations. Some participants observed that because inflation has been elevated for some time, there was a heightened risk of longer-term inflation expectations becoming unanchored if there is a long-lasting rise in inflation.

In their discussion of the labor market, participants judged that conditions remained solid and that the labor market was at, or near, estimates of maximum employment. Several participants observed that the recent stability of the labor market reflected a slowing in both hiring and layoffs, and several participants also mentioned that their contacts and business survey respondents reported pausing hiring decisions because of elevated uncertainty. Several participants noted that immigration policies were reducing labor supply. In their outlook for the labor market, most participants suggested that higher tariffs or heightened policy uncertainty would weigh on labor demand, and many participants expected a gradual softening of conditions. A few participants noted that some indicators already provided signs of softness and that they would be attentive to indications of further labor market weakening. Some participants observed that wage growth had continued to moderate and that it was not expected to contribute to inflationary pressures.

Participants judged that economic activity had continued to grow at a solid pace, although uncertainty remained elevated. The outlook was for continued economic growth, although a majority of participants expected that the pace of growth was likely to moderate going forward. Regarding the household sector, several participants observed that some recent data indicated continued solid consumer spending growth, whereas several other participants pointed to other data that suggested softening. Several participants noted that lower- and moderate-income households were switching to lower-cost items and brands or that these households could be disproportionately affected by tariff-related price increases. Many participants observed that measures of household sentiment remained low, although these measures had risen a bit recently. A few participants noted that consumer sentiment had not been a good predictor of consumer spending in recent years.

In their discussion of the business sector, participants noted that activity remained solid, although there have been signs of softening, and many observed that indicators of business sentiment remained low. With respect to investment spending, several participants reported that business contacts had indicated that their firms were proceeding with existing investment projects but that heightened uncertainty was making them cautious about beginning new projects, especially larger ones; some smaller new investments or those with more certain payoffs were still being undertaken. Several participants noted that financing from both banks and financial markets was readily available for larger investment projects. A couple of participants noted that business investment in artificial intelligence could boost productivity. Several participants commented that there had been signs of softening production activity in the manufacturing sector and pointed to reductions in orders and shipments in manufacturing surveys or in reports of business contacts. A couple of participants noted that the agricultural sector faced strains from low crop prices and high input costs.

In their consideration of monetary policy at this meeting, participants noted that inflation remained somewhat elevated. Participants also observed that recent indicators suggested that economic activity had continued to expand at a solid pace, although swings in net exports and inventories had affected the measurement and interpretation of the data. Participants further noted that the unemployment rate remained at a low level and that labor market conditions had remained solid. Participants observed that uncertainty about the economic outlook had diminished amid a reduction in announced and expected tariffs, which appeared to peak in April and had subsequently declined, but that overall uncertainty continued to be elevated. All participants viewed it as appropriate to maintain the target range for the federal funds rate at 4-1/4 to 4-1/2 percent. Participants judged it appropriate to continue the process of reducing the Federal Reserve's securities holdings.

In considering the outlook for monetary policy, participants generally agreed that, with economic growth and the labor market still solid and current monetary policy moderately or modestly restrictive, the Committee was well positioned to wait for more clarity on the outlook for inflation and economic activity. Participants noted that monetary policy would be informed by a wide range of incoming data, the economic outlook, and the balance of risks. Most participants assessed that some reduction in the target range for the federal funds rate this year would likely be appropriate, noting that upward pressure on inflation from tariffs may be temporary or modest, that medium- and longer-term inflation expectations had remained well anchored, or that some weakening of economic activity and labor market conditions could occur. A couple of participants noted that, if the data evolve in line with their expectations, they would be open to considering a reduction in the target range for the policy rate as soon as at the next meeting. Some participants saw the most likely appropriate path of monetary policy as involving no reductions in the target range for the federal funds rate this year, noting that recent inflation readings had continued to exceed the Committee's 2 percent goal, that upside risks to inflation remained meaningful in light of factors such as elevated short-term inflation expectations of businesses and households, or that they expected that the economy would remain resilient. Several participants commented that the current target range for the federal funds rate may not be far above its neutral level.

Various participants discussed risks that, if realized, would have the potential to affect the appropriate path of monetary policy. Regarding upside risks to inflation, participants noted that, if the imposition of tariffs were to generate a larger-than-expected increase in inflation, if such an increase in inflation were to be more persistent than anticipated, or if a notable increase in medium- or longer-term inflation expectations were to occur, then it would be appropriate to maintain a more restrictive stance of monetary policy than would otherwise be the case, especially if labor market conditions and economic activity remained solid. By contrast, if labor market conditions or economic activity were to weaken materially, or if inflation were to continue to come down and inflation expectations remained well anchored, then it would be appropriate to establish a less restrictive stance of monetary policy than would otherwise be the case. Participants noted that the Committee might face difficult tradeoffs if elevated inflation proved to be more persistent while the outlook for employment weakened. If that were to occur, participants agreed that they would consider how far the economy is from each goal and the potentially different time horizons over which those respective gaps would be anticipated to close.

In considering the likelihood of various scenarios, participants agreed that the risks of higher inflation and weaker labor market conditions had diminished but remained elevated, citing a lower expected path of tariffs, encouraging recent readings on inflation and inflation expectations, resilience in consumer and business spending, or improvements in some measures of consumer or business sentiment. Some participants commented that they saw the risk of elevated inflation as remaining more prominent, or as having diminished by less, than risks to employment. A few participants saw risks to the labor market as having become predominant. They noted some recent signs of weakening in real activity or the labor market, or commented that conditions could weaken in the future, particularly if policy were to remain restrictive. Participants agreed that although uncertainty about inflation and the economic outlook had decreased, it remained appropriate to take a careful approach in adjusting monetary policy. Participants emphasized the importance of ensuring that longer-term inflation expectations remained well anchored and agreed that the current stance of monetary policy positioned the Committee well to respond in a timely way to potential economic developments.

Committee Policy Actions

In their discussions of monetary policy for this meeting, members agreed that although swings in net exports had affected the data, recent indicators suggested that economic activity had continued to expand at a solid pace. Members agreed that the unemployment rate had remained at a low level and that labor market conditions had remained solid. Members concurred that inflation remained somewhat elevated. Members agreed that it was appropriate to acknowledge in the postmeeting statement that uncertainty about the economic outlook had diminished but remained elevated, and the Committee was attentive to the risks to both sides of its dual mandate. The assessment that uncertainty had declined reflected, in part, a reduction in the expected level of tariffs, which appeared to peak in April and had subsequently declined.

In support of its goals, the Committee agreed to maintain the target range for the federal funds rate at 4-1/4 to 4-1/2 percent. Members agreed that, in considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee would carefully assess incoming data, the evolving outlook, and the balance of risks. All members agreed that the postmeeting statement should affirm their strong commitment both to supporting maximum employment and to returning inflation to the Committee's 2 percent objective.

Members agreed that, in assessing the appropriate stance of monetary policy, the Committee would continue to monitor the implications of incoming information for the economic outlook. They would be prepared to adjust the stance of monetary policy as appropriate if risks emerged that could impede the attainment of the Committee's goals. Members also agreed that their assessments would take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

At the conclusion of the discussion, the Committee voted to direct the Federal Reserve Bank of New York, until instructed otherwise, to execute transactions in the SOMA in accordance with the following domestic policy directive, for release at 2:00 p.m.:

"Effective June 20, 2025, the Federal Open Market Committee directs the Desk to:

- Undertake open market operations as necessary to maintain the federal funds rate in a target range of 4-1/4 to 4-1/2 percent.

- Conduct standing overnight repurchase agreement operations with a minimum bid rate of 4.5 percent and with an aggregate operation limit of $500 billion.

- Conduct standing overnight reverse repurchase agreement operations at an offering rate of 4.25 percent and with a per-counterparty limit of $160 billion per day.

- Roll over at auction the amount of principal payments from the Federal Reserve's holdings of Treasury securities maturing in each calendar month that exceeds a cap of $5 billion per month. Redeem Treasury coupon securities up to this monthly cap and Treasury bills to the extent that coupon principal payments are less than the monthly cap.

- Reinvest the amount of principal payments from the Federal Reserve's holdings of agency debt and agency mortgage-backed securities (MBS) received in each calendar month that exceeds a cap of $35 billion per month into Treasury securities to roughly match the maturity composition of Treasury securities outstanding.

- Allow modest deviations from stated amounts for reinvestments, if needed for operational reasons."

The vote also encompassed approval of the statement below for release at 2:00 p.m.:

"Although swings in net exports have affected the data, recent indicators suggest that economic activity has continued to expand at a solid pace. The unemployment rate remains low, and labor market conditions remain solid. Inflation remains somewhat elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. Uncertainty about the economic outlook has diminished but remains elevated. The Committee is attentive to the risks to both sides of its dual mandate.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 4-1/4 to 4-1/2 percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments."

Voting for this action:Jerome H. Powell, John C. Williams, Michael S. Barr, Michelle W. Bowman, Susan M. Collins, Lisa D. Cook, Austan D. Goolsbee, Philip N. Jefferson, Adriana D. Kugler, Alberto G. Musalem, Jeffrey R. Schmid, and Christopher J. Waller.

Voting against this action: None.

Consistent with the Committee's decision to leave the target range for the federal funds rate unchanged, the Board of Governors of the Federal Reserve System voted unanimously to maintain the interest rate paid on reserve balances at 4.4 percent, effective June 20, 2025. The Board of Governors of the Federal Reserve System voted unanimously to approve the establishment of the primary credit rate at the existing level of 4.5 percent.

It was agreed that the next meeting of the Committee would be held on Tuesday–Wednesday, July 29–30, 2025. The meeting adjourned at 10:10 a.m. on June 18, 2025.

Notation Vote

By notation vote completed on May 27, 2025, the Committee unanimously approved the minutes of the Committee meeting held on May 6–7, 2025.

Attendance

Jerome H. Powell, Chair

John C. Williams, Vice Chair

Michael S. Barr

Michelle W. Bowman

Susan M. Collins

Lisa D. Cook

Austan D. Goolsbee

Philip N. Jefferson

Adriana D. Kugler

Alberto G. Musalem

Jeffrey R. Schmid

Christopher J. Waller

Beth M. Hammack, Patrick Harker, Neel Kashkari, and Lorie K. Logan, Alternate Members of the Committee

Thomas I. Barkin, Raphael W. Bostic, and Mary C. Daly, Presidents of the Federal Reserve Banks of Richmond, Atlanta, and San Francisco, respectively

Joshua Gallin, Secretary

Matthew M. Luecke, Deputy Secretary

Brian J. Bonis, Assistant Secretary

Michelle A. Smith, Assistant Secretary

Mark E. Van Der Weide, General Counsel

Richard Ostrander, Deputy General Counsel

Trevor A. Reeve, Economist

Stacey Tevlin, Economist

Beth Anne Wilson, Economist

Shaghil Ahmed, Brian M. Doyle, Eric M. Engen, Joseph W. Gruber, Anna Paulson, and Egon Zakrajšek, Associate Economists

Roberto Perli, Manager, System Open Market Account

Julie Ann Remache, Deputy Manager, System Open Market Account

Jose Acosta, Senior System Engineer II, Division of Information Technology, Board

Sriya Anbil, Group Manager, Division of Monetary Affairs, Board

Philippe Andrade,2 Vice President, Federal Reserve Bank of Boston

Roc Armenter, Executive Vice President, Federal Reserve Bank of Philadelphia

Alyssa Arute,3 Assistant Director, Division of Reserve Bank Operations and Payment Systems, Board

Ayelen Banegas, Principal Economist, Division of Monetary Affairs, Board

Becky C. Bareford, First Vice President, Federal Reserve Bank of Richmond

Lisa Barrow, Vice President, Federal Reserve Bank of Cleveland

William F. Bassett, Senior Associate Director, Division of Financial Stability, Board

Michael Bauer,2 Senior Research Advisor, Federal Reserve Bank of San Francisco

Travis J. Berge,2 Section Chief, Division of Research and Statistics, Board

Dario Caldara,2 Adviser, Division of International Finance, Board

Mark A. Carlson, Adviser, Division of Monetary Affairs, Board

Michele Cavallo, Special Adviser to the Board, Division of Board Members, Board

Wendy E. Dunn, Adviser, Division of Research and Statistics, Board

William Dupor, Senior Economic Policy Advisor II, Federal Reserve Bank of St. Louis

Eric C. Engstrom, Associate Director, Division of Monetary Affairs, Board

Giovanni Favara,2 Deputy Associate Director, Division of Monetary Affairs, Board

Laura J. Feiveson, Special Adviser to the Board, Division of Board Members, Board

Giuseppe Fiori,2 Principal Economist, Division of International Finance, Board

Jonas Fisher,2 Senior Vice President, Federal Reserve Bank of Chicago

Glenn Follette, Associate Director, Division of Research and Statistics, Board

Etienne Gagnon, Senior Associate Director, Division of International Finance, Board

Vaishali Garga,2 Principal Economist, Federal Reserve Bank of Boston

Michael S. Gibson, Director, Division of Supervision and Regulation, Board

Jonathan E. Goldberg, Principal Economist, Division of Monetary Affairs, Board

François Gourio, Senior Economist and Economic Advisor, Federal Reserve Bank of Chicago

Christopher J. Gust, Associate Director, Division of Monetary Affairs, Board

François Henriquez, First Vice President, Federal Reserve Bank of St. Louis

Edward Herbst,2 Section Chief, Division of Monetary Affairs, Board

Valerie S. Hinojosa, Section Chief, Division of Monetary Affairs, Board

Sara J. Hogan,3 Senior Financial Institution Policy Analyst I, Division of Reserve Bank Operations and Payment Systems, Board

Jane E. Ihrig, Special Adviser to the Board, Division of Board Members, Board

Benjamin K. Johannsen,2 Assistant Director, Division of Monetary Affairs, Board

Michael T. Kiley, Deputy Director, Division of Monetary Affairs, Board

Don H. Kim, Senior Adviser, Division of Monetary Affairs, Board

Elizabeth Klee, Deputy Director, Division of Monetary Affairs, Board

Scott R. Konzem, Senior Economic Modeler II, Division of Monetary Affairs, Board

Michael Koslow,3 Associate Director, Federal Reserve Bank of New York

Spencer D. Krane,2 Senior Vice President, Federal Reserve Bank of Chicago

Sylvain Leduc, Executive Vice President and Director of Economic Research, Federal Reserve Bank of San Francisco

Andreas Lehnert, Director, Division of Financial Stability, Board

Paul Lengermann, Deputy Associate Director, Division of Research and Statistics, Board

Eric LeSueur,3 Policy and Market Analysis Advisor, Federal Reserve Bank of New York

Kurt F. Lewis, Special Adviser to the Chair, Division of Board Members, Board

Logan T. Lewis, Section Chief, Division of International Finance, Board

Laura Lipscomb, Special Adviser to the Board, Division of Board Members, Board

Francesca Loria,2 Principal Economist, Division of Monetary Affairs, Board

David López-Salido, Senior Associate Director, Division of Monetary Affairs, Board

Jonathan P. McCarthy, Economic Research Advisor, Federal Reserve Bank of New York

Benjamin W. McDonough, Deputy Secretary and Ombudsman, Office of the Secretary, Board

Alisdair G. McKay,2 Monetary Advisor, Federal Reserve Bank of Minneapolis

Yvette McKnight,2 Senior Agenda Assistant, Office of the Secretary, Board

Mark Meder, First Vice President, Federal Reserve Bank of Cleveland

Ann E. Misback, Secretary, Office of the Secretary, Board

David Na, Lead Financial Institution Policy Analyst, Division of Monetary Affairs, Board

Edward Nelson, Senior Adviser, Division of Monetary Affairs, Board

Giovanni Nicolò,2 Principal Economist, Division of Monetary Affairs, Board

Anna Nordstrom, Head of Markets, Federal Reserve Bank of New York

Alyssa T. O'Connor, Special Adviser to the Board, Division of Board Members, Board

Michael G. Palumbo, Senior Associate Director, Division of Research and Statistics, Board

Matthias Paustian,2 Assistant Director, Division of Research and Statistics, Board

Karen M. Pence, Deputy Associate Director, Division of Research and Statistics, Board

Paolo A. Pesenti,4 Director of Monetary Policy Research, Federal Reserve Bank of New York

Eugenio P. Pinto, Special Adviser to the Board, Division of Board Members, Board

Andrea Raffo, Senior Vice President, Federal Reserve Bank of Minneapolis

Samuel Schulhofer-Wohl, Senior Vice President, Federal Reserve Bank of Dallas

Kirk Schwarzbach, Special Assistant to the Board, Division of Board Members, Board

Zeynep Senyuz, Special Adviser to the Board, Division of Board Members, Board

Andre F. Silva, Principal Economist, Division of Monetary Affairs, Board

Thiago Teixeira Ferreira, Special Adviser to the Board, Division of Board Members, Board

Judit Temesvary, Principal Economist, Division of International Finance, Board

Paula Tkac, Director of Research, Federal Reserve Bank of Atlanta

Robert L. Triplett III, First Vice President, Federal Reserve Bank of Dallas

Daniel J. Vine, Principal Economist, Division of Research and Statistics, Board

Donielle A. Winford, Senior Information Manager, Division of Monetary Affairs, Board

Alexander L. Wolman, Vice President, Federal Reserve Bank of Richmond

Rebecca Zarutskie,2 Senior Vice President, Federal Reserve Bank of Dallas

Molin Zhong,2 Principal Economist, Division of Financial Stability, Board

_______________________

Joshua Gallin

Secretary

1. The Federal Open Market Committee is referenced as the "FOMC" and the "Committee" in these minutes; the Board of Governors of the Federal Reserve System is referenced as the "Board" in these minutes. Return to text

2. Attended through the discussion of the review of the monetary policy framework. Return to text

3. Attended through the discussion of developments in financial markets and open market operations. Return to text

4. Attended through the discussion of economic developments and the outlook. Return to text

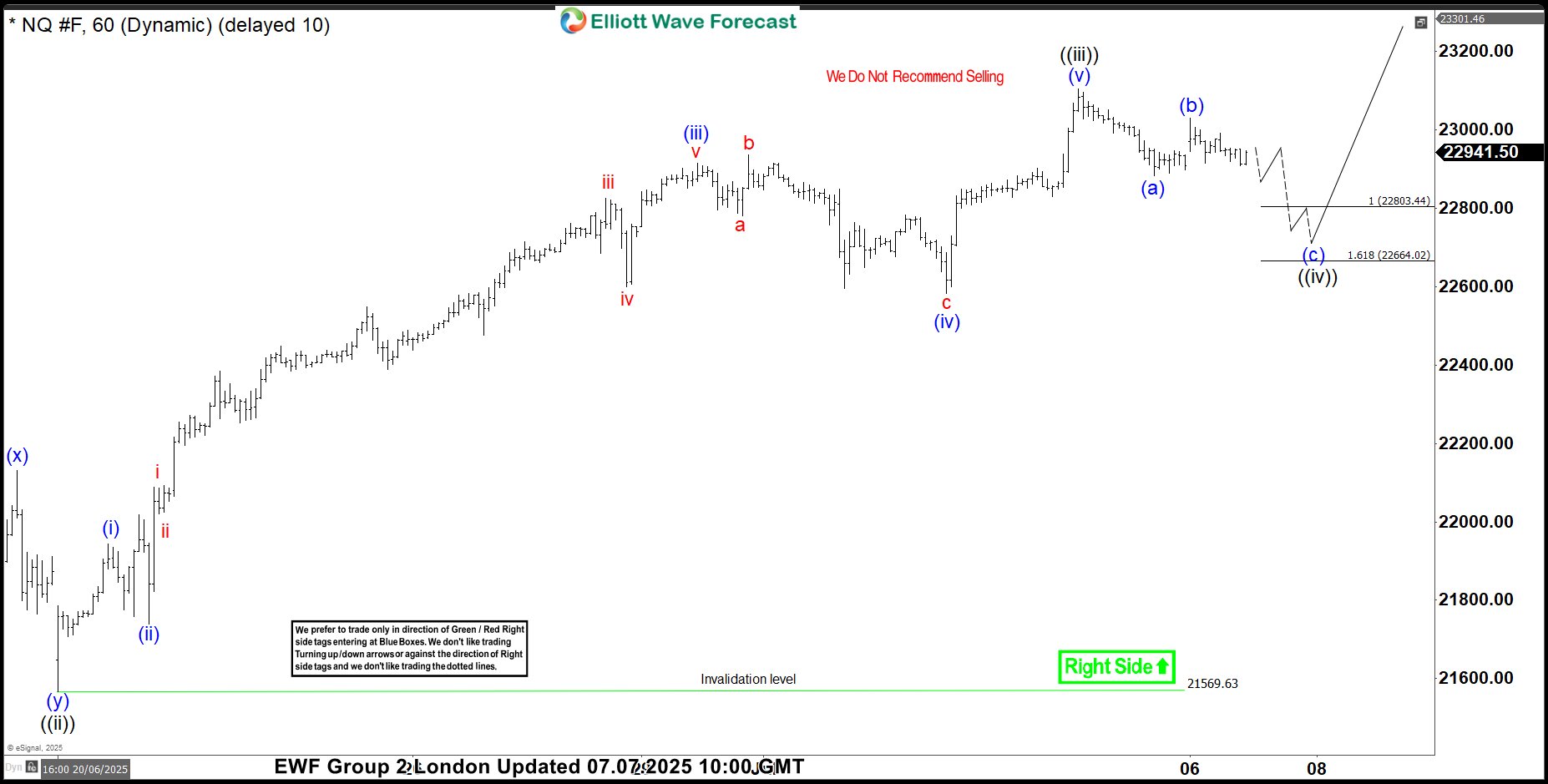

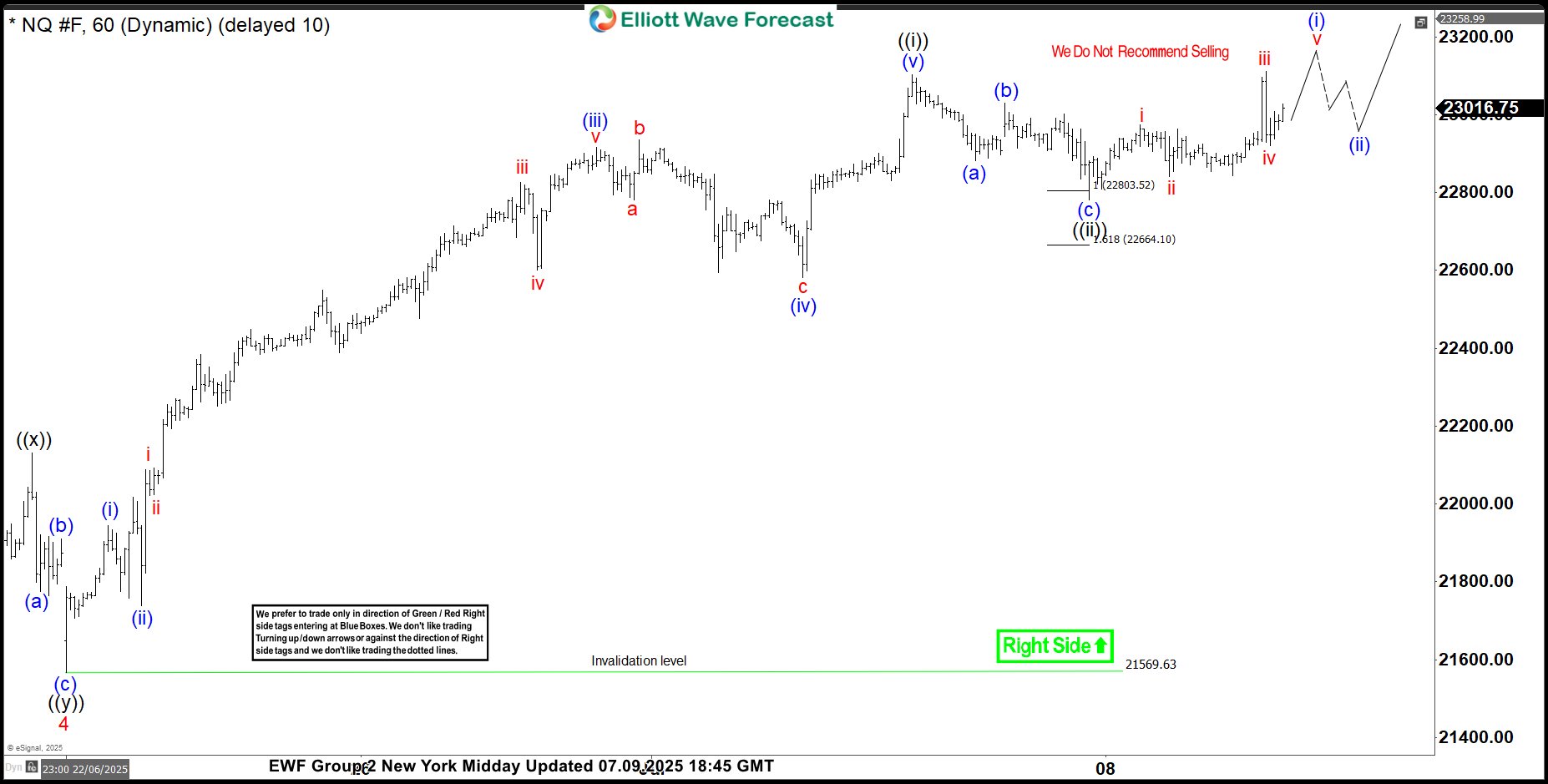

NASDAQ (NQ_F) Elliott Wave: Forecasting the Rally From the Equal Legs Zone

Hello fellow traders. In this technical article we’re going to look at the Elliott Wave charts of NASDAQ (NQ_F) published in members area of the website. As our members know, $NQ_F is forming impulsive bullish sequences in the cycle from the 16441.7 low. Recently, we forecasted the end of the short-term pull back and called for a further rally. In the following text, we’ll explain the Elliott Wave analysis and present target areas.

NQ_F Elliott Wave 1 Hour Chart 07.07.2025

NASDAQ is forming a three-wave pullback which still looks incomplete at the moment. Our members know that we can easily identify the reversal area by measuring the Equal Legs zone, (a) related (b), which comes in at the 22803.44-22664.02 area. We expect buyers to appear within the mentioned zone and to see a further rally in NASDAQ ($NQ_F) from there.

You can learn more about Elliott Wave Patterns at our Free Elliott Wave Educational Web Page

90% of traders fail because they don’t understand market patterns. Are you in the top 10%? Test yourself with this advanced Elliott Wave Test

NQ_F Elliott Wave 1 Hour Chart 07.07.2025

NASDAQ found buyers as expected at the Equal Legs area and has delivered a decent rally so far. The price broke toward new highs, confirming the next leg is already in progress.

Ethereum’s Steady Performance Sets the Stage for Upside Breakout

The second largest cryptocurrency has been on a consistent grind in the past two weeks after seeing some heavy selling flows during the Israel-Iran War, taking its prices close to the $2,000 mark but since, has been posting a slow but strong rally, fuel for further continuation.

Crypto markets haven't taken a significant direction for a while, but it doesn't mean that no opportunities are availables – Ranges give the opportunity for markets to cool down and prepare for further moves, while consolidating Volume-at-Price.

Market theory implies that the more prices are at an equilibrium (rangebound), the more solid the anchor of value for all participants.

With cryptos consolidating at much higher levels than prior years, this shows a resilience for cryptocurrency markets and gives it more credibility for traditional investors to start inputting more flows.

For example, since mid-May 2025, Bitcoin has been consolidating between $100,000 to $110,000 – despite giving to many players the opportunity to take their profits, markets did not retrace. Ranges also provide opportunities for scalpers who may attempt to trade highs and lows.

Same for Ethereum which has been holding between $2,350 to $2,750 for close to two months now, and despite these prices being not too close from the Ether's ETH, it still consolidates at a relative high value, particularly after the 2025 Q1 Heavy Selling.

Where does Ethereum stand after close to 2 months of consolidation?

Ethereum Daily Chart

Ethereum Daily Chart, July 9, 2025 – Source: TradingView

The Daily chart shows decent consolidation with two fakeouts – it can happen that fakeouts lead to players being trapped beyond consolidation levels and create movements on the other side of the range.

An upside fakeout in mid-June led to a retracement down to the $2,174 lows only a few days after.

Since, however, buyers have stepped in consistently using the 50-Day Moving Average as support for continuous buying. with Momentum not moving too fast to the upside (due to the speed and consistency of the buying move), the conditions for an upward breakout are starting to assemble.

A strong buying candle above the 2,750 range highs would be necessary to confirm the hypothesis as a range is poised to hold as long as it holds before the inverse is proven true.

Keep an eye on sentiment in other cryptos, particularly altcoins to spot how crypto players are moving.

Ethereum 4H Chart

Ethereum 4H Chart, July 9, 2025 – Source: TradingView

The 4H Candles further give signs of the consistent grind, however it will be essential to spot how buyers react to the increasingly overbought conditions of the shorter timeframe.

The 4H MA 50 is also accompanying the trend with a not-to-steep and stable trendline forming since the war-lows.

Prices will have to hold above the $2,570 mid range level for a breakout to the upside above the $2,750 range highs – June fakeout highs are at $2,880

ETHBTC check-up

ETH outperforming Bitcoin is essential for other altcoins to keep growing, as was the case in past cycles, which would provide yet another sign of consistency for the Cryptocurrency markets.

After a downside fakeout, ETHBTC is getting back into its range but still has to overcome the 2.46% mid-range level before showing more bullish signs.

FOMC Minutes: ‘A Couple’ of Policymakers to Consider Rate Cuts in July and ‘Most’ Before Year-End

Minutes from the Fed’s June 17-18 policy meeting, released at 14:00 EDT, have done little to change the narrative surrounding future monetary policy decisions.

Markets predict the Federal Reserve will maintain rates on July 30th and make its first 2025 rate cut in its September 17th decision.

Fed Minutes June 17-18: Key takeaways

Unanimous in vote to maintain the federal fund rate between 4.25 and 4.50%, minutes reaffirmed the Fed’s concerns on tariff-borne inflation, although acknowledged that uncertainty on the general economic outlook has “diminished but remains elevated”

While predictions for a July rate cut remain essentially unchanged, the minutes shed light on the diverging views held by policymakers about how lax the Fed should be during the current easing cycle

EUR/USD, OANDA, TradingView, 09/07/2025

"Most participants assessed that some reduction in the target range for the federal funds rate this year would likely be appropriate, noting that upward pressure on inflation from tariffs may be temporary or modest, that medium- and longer-term inflation expectations had remained well anchored, or that some weakening of economic activity and labor market conditions could occur."

Minutes of the Federal Open Market Committee, June 17–18, 2025

Fed Minutes June 17-18: Majority expect rate reduction this year

In a nutshell, three schools of thought currently exist amongst Fed policymakers, albeit to varying degrees of popularity:

- The majority of policymakers think that at least some reduction in the federal fund rate is both likely and appropriate before year-end, drawing reference to the temporary impact of tariffs on inflation, and longer-term inflation trends remaining “well-anchored”

- Some policymakers think that the most appropriate path would be to make no reductions in the federal fund rate before year-end, mentioning that inflation remains sticky, and importantly, above the 2% target

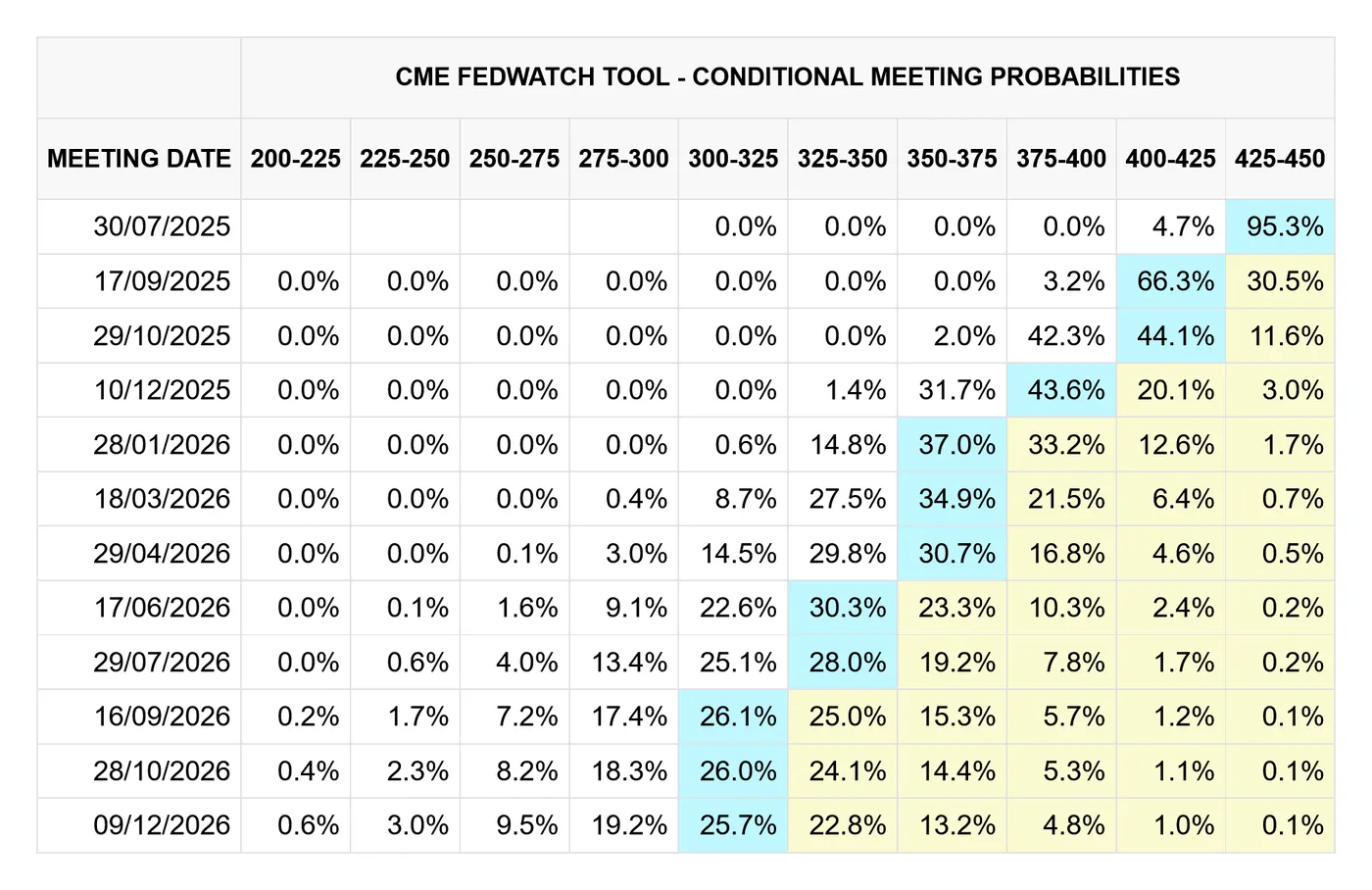

- A couple of policymakers are in support of reductions in the federal fund rate as soon as the next meeting, should “data evolve in line with expectations”

CME FedWatch, CME Group 24/06/2024

Fed Minutes June 17-18: “Swings” in export data spook Fed

With the latest on Trump tariffs hitting headlines again earlier this week, minutes released today from the Federal Reserve’s June meeting, renewing fears of tariff-borne inflation, could perhaps have come at a better time.

In the report, the Fed cited the potential for tariffs to disrupt supply chains and affect productivity. The Fed also questioned the consistency of recent export data, inferring that tariffs and their short-term effect on exports are muddying the waters that would otherwise allow the Federal Reserve a more straightforward path towards rate cuts.

Remaining staunch in their ‘wait-and-see’ policy for much of this year, while assuring that future decisions will be made on data alone, most will remain unsurprised that the Federal Reserve is erring on the side of caution.

When considering recent developments on US trade, extending tariff deadlines to August 1st, concerns made in FOMC minutes are now somewhat vindicated, and this offers the Fed further rationale to delay rate cuts, should they wish to.

Fed Minutes June 17-18: Inflation remains above the 2% target

Somewhat predictably, minutes would confirm that the Federal Reserve seems less concerned about the trend of falling inflation and more concerned that it remains above the target of 2%, mentioning recent PCE figures.

Cited as “somewhat elevated” both in the immediate policy statement and minutes, the phrasing around inflation highlights ongoing concern, especially compared to the more complimentary commentary of current US labor numbers.

The report’s description of the labor market as “solid” and unemployment as “low” would suggest that, in a vacuum, recent labor market numbers would support the notion of rate cuts.

Minutes Show the Fed Is Edging Closer to the Rate Cut

The Federal Open Market Committee (FOMC) held the policy rate steady in the target range of 4.25-4.5% at its June 17-18th meeting. The minutes from that meeting highlighted that trade and policy uncertainty and their impact on inflation remained a focal point of discussion. However, uncertainty was rated as having diminished since May (as Liberation Day tariffs have been postponed and trade war with China de-escalated) leading to a less pessimistic economic outlook relative to the previous minutes.

The staff projection in June – not to be confused with the Summary of Economic Projections – was generally upgraded. Real GDP growth in 2025 and 2026 was higher than what was presented at the May meeting, mainly due to the reduction in assumptions about the effective tariff rate. As a result, both the unemployment rate and inflation were now expected to increase by less, than in the previous forecast. Policy uncertainty remained high, and the economic risks continued to be "skewed to the downside", although risk of a recession has diminished.

FOMC participants viewed the current labour market as solid, acknowledging that both hirings and layoffs have remained steady in light of heightened uncertainty and reduction in labour supply due to immigration policy. That being said, most participants expected labour market conditions to gradually soften, noting that wage growth has continued to moderate suggestive of weakening labor demand.

Regarding inflation, participants acknowledged that inflation remained elevated and recent progress has been uneven, with services inflation moving down recently while goods inflation has picked up. They also noted limited progress in lowering core inflation. Participants appeared in consensus that tariffs will put upward pressure on inflation, but there remained considerably uncertainty on the timing, size and duration of these effects, namely, large inventories could help firms delay passing higher costs to consumers. While some participants noted that tariffs would lead to a one-time increase in prices and thus would not affect inflation expectations, most participants noted that tariffs could have more longer lasting effects on inflation increasing the risk of inflation expectations becoming unanchored.

The vote to hold rates steady was unanimous. Participants assessed that the Committee was well positioned to wait for more clarity on inflation and policy front given that the economy remained solid, and the monetary policy was only "moderately or modestly restrictive". However, most participants thought that some reduction in the fed funds rate this year "would likely be appropriate", but couple of participants noted that if the data continued to evolve in-line with their expectation "they would be open to considering a reduction in the target rate for the policy rate as soon as at the next meeting".

Key Implications

The FOMC participants acknowledged that the economy continues to perform well, uncertainty has diminished somewhat, and the labor market remains solid. That said, there appears to be less consensus among participants regarding the impact of tariffs on inflation, with some suggesting a short-term impact, while others are concerned about longer lasting effects.

Still, the minutes suggest that momentum for a rate cut is building within the FOMC. We are also of this view. Despite the economy’s resilience so far, this strength is likely to fade in the second half of the year (forecast), with both the unemployment rate and inflation expected to trend higher. Trade policy remains a key source of uncertainty, with tensions escalating recently, but the deadline to reach deals to avoid Liberation Day tariffs was pushed to August 1st. We expect that the FOMC's July 30th meeting is likely too early for enough certainty to have emerged for the Fed to cut rates, but the minutes suggest we could see a dissent or two on a stand pat decision. Markets currently favor a September rate cut, and we are inclined to agree.

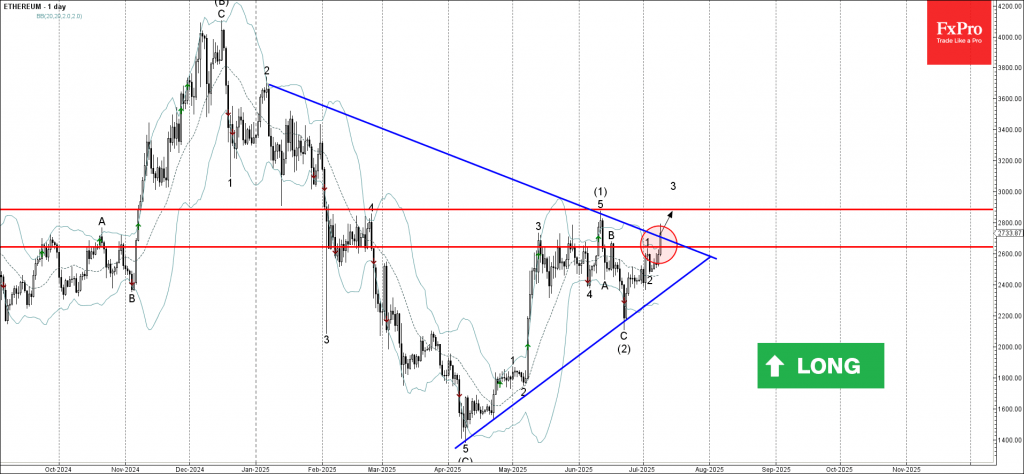

Ethereum Wave Analysis

Ethereum: ⬆️ Buy

- Ethereum broke the resistance area

- Likely to rise to resistance level 2885.00

Ethereum cryptocurrency recently broke the resistance area located between the resistance level 2645.00 (which stopped wave 1 at the start of July) and the resistance trendline of the weekly Triangle from January.

The breakout of this resistance area accelerated the active short-term impulse wave 3 of the intermediate impulse wave (3) from June.

Given the strongly bullish sentiment seen across the crypto markets today, Ethereum cryptocurrency can be expected to rise to the next resistance level 2885.00 (top of wave (1) from June).