Sample Category Title

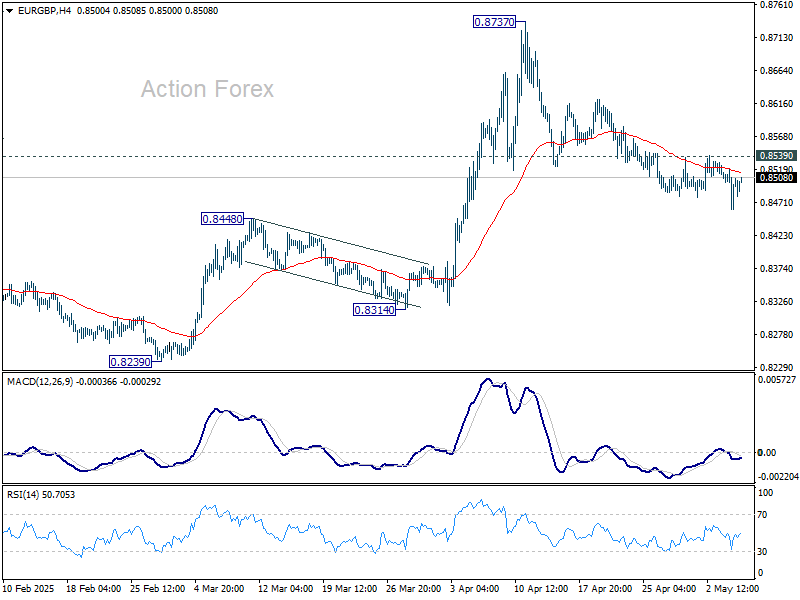

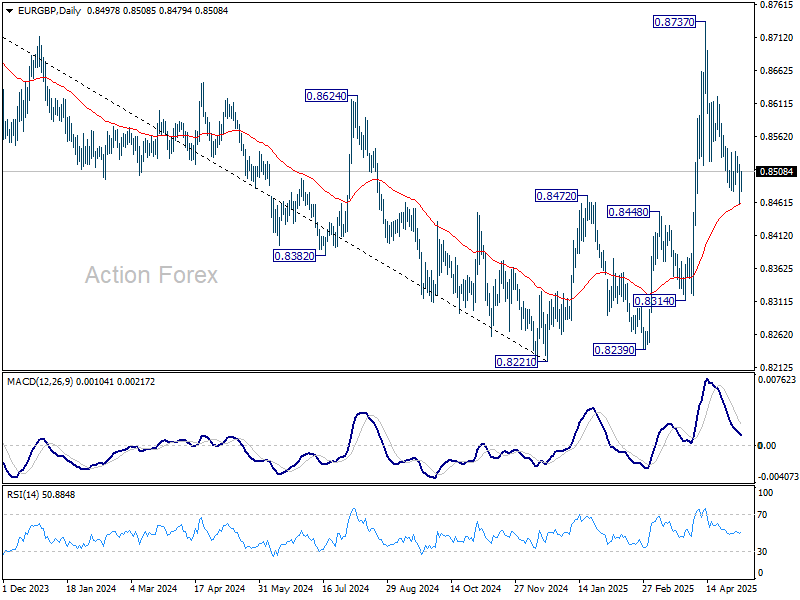

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8471; (P) 0.8496; (R1) 0.8529; More...

Intraday bias in EUR/GBP stays mildly on the downside for the moment. Sustained trading below 55 D EMA (now at 0.8461) will suggest that whole rise from 0.8221 has already complete and turn outlook bearish. Nevertheless, rebound from current level, followed by break of 0.8539 resistance, will suggest that the correction from 0.8737 has completed, and retain near term bullishness.

In the bigger picture, down trend from 0.9267 (2022 high) should have completed at 0.8221, just ahead of 0.9201 key support (2024 low). Rise from 0.8221 is likely reversing the whole fall. Further rise should be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867 next. This will remain the favored case as long as 0.8472 resistance turned support holds. However, firm break of 0.8472 will argue that the down trend hasn't completed yet.

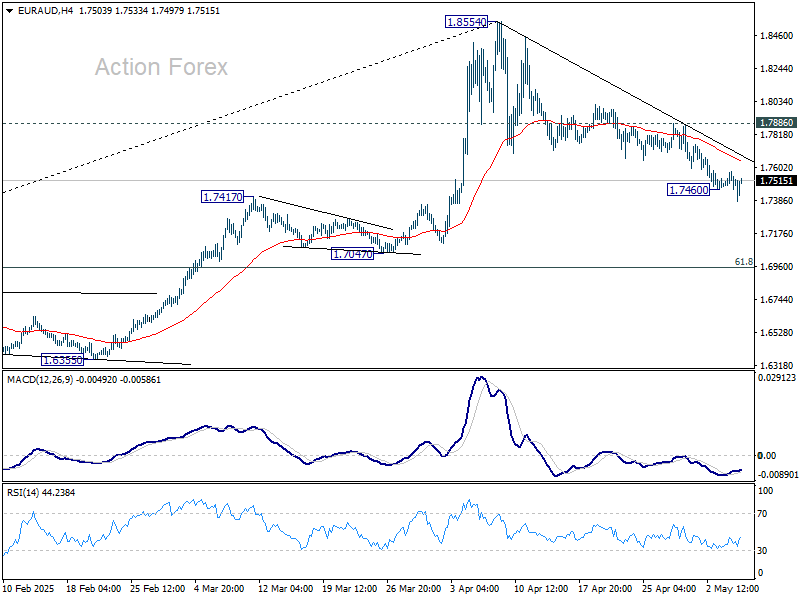

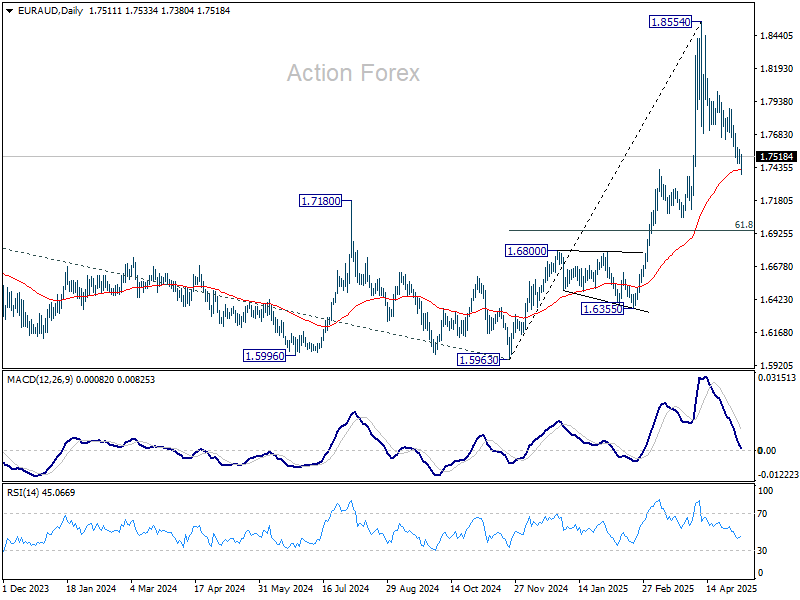

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7455; (P) 1.7515; (R1) 1.7566; More...

EUR/AUD's fall from 1.8554 resumed after brief recovery and intraday bias is back on the downside. Sustained break of 55 D EMA (now at 1.7420) will target 61.8% retracement at 1.6953. On the upside, though, break of 1.7886 resistance will turn bias back to the upside for retesting 1.8554 high.

In the bigger picture, up trend from 1.4281 (2022 low) is in progress for 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. Firm break there will pave the way to 138.2% projection at 1.9806, which is close to 1.9799 (2020 high). Outlook will remain bullish as long as 1.7062 resistance turned support (2023 high) holds even in case of deep pullback.

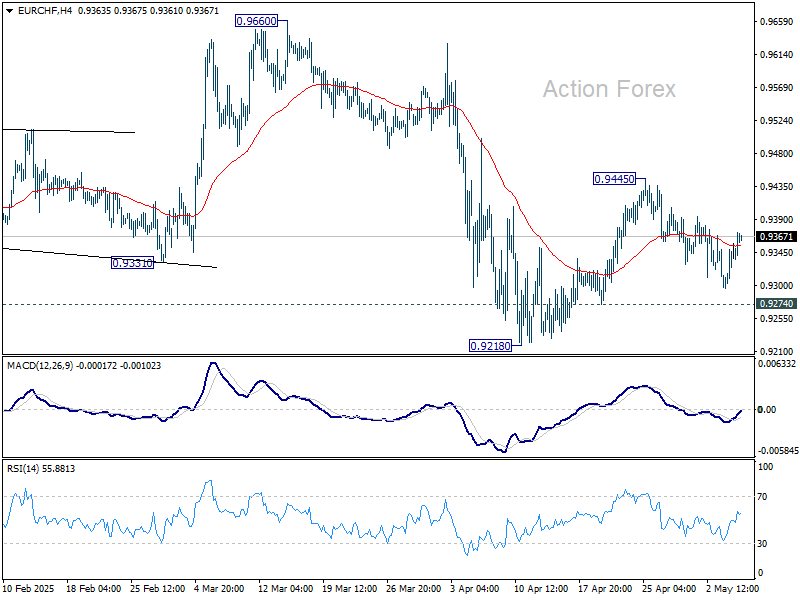

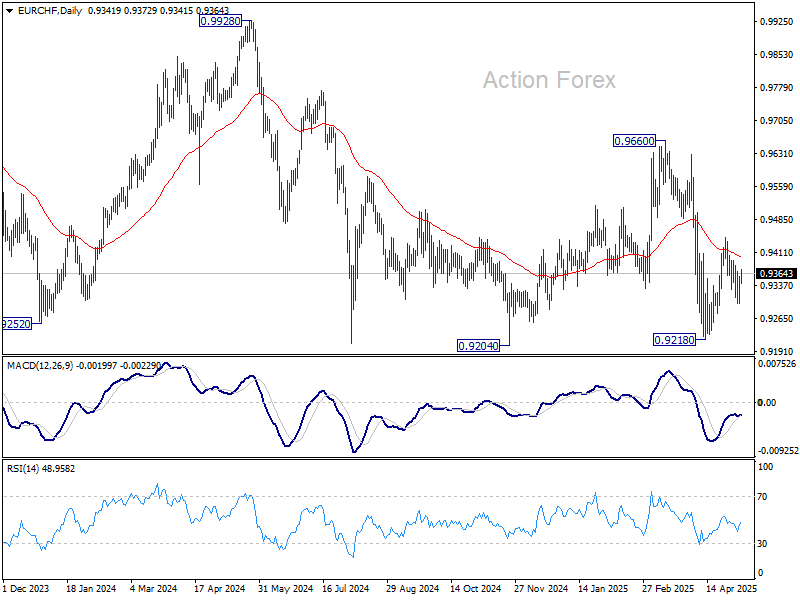

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9310; (P) 0.9335; (R1) 0.9371; More....

No change in EUR/CHF's outlook and intraday bias stays neutral. On the upside, above 0.9445 will resume the rebound from 0.9218, either as a corrective move or the third leg of the pattern from 0.9204. However, break of 0.9274 will suggest that that recovery has completed, and bring retest of 0.9204/18 support zone.

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9555) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.

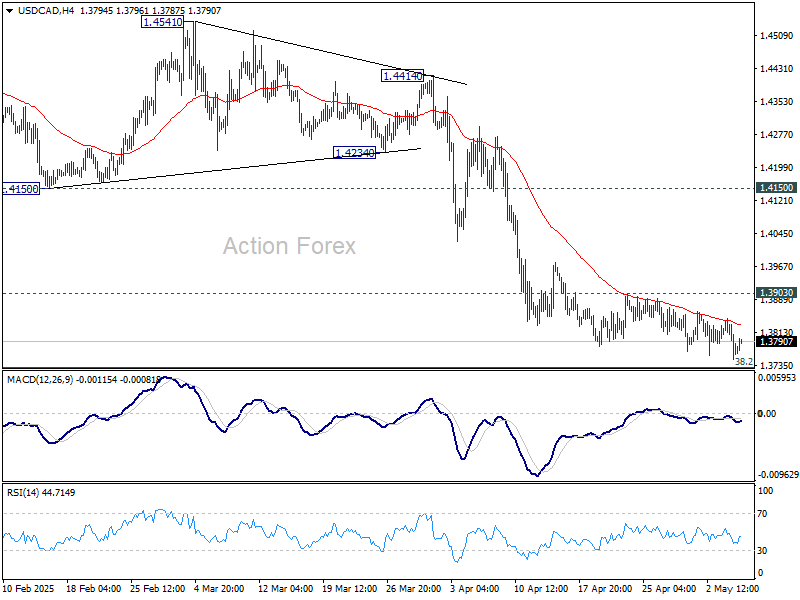

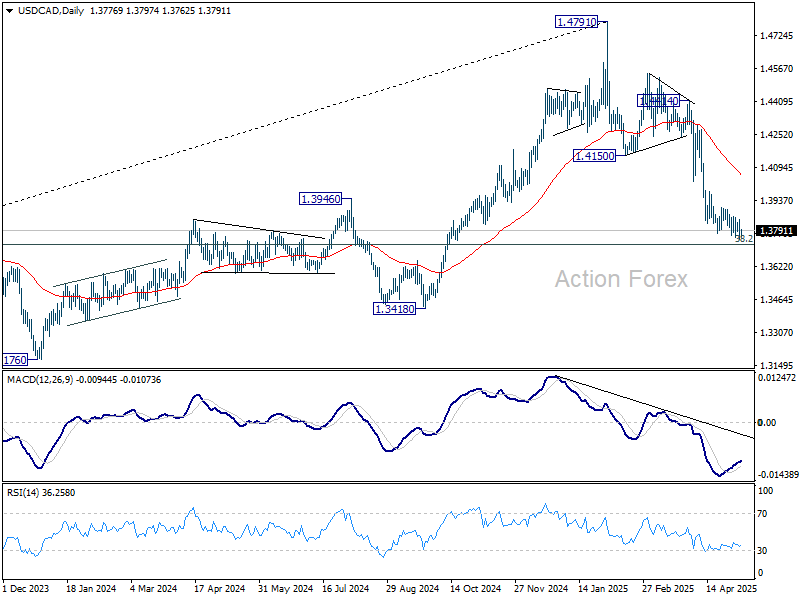

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3736; (P) 1.3791; (R1) 1.3830; More...

No change in USD/CAD's outlook and further decline remains mildly in favor with 1.3903 resistance intact, for 1.3727 fibonacci level next. However, considering bullish convergence condition in 4H MACD, firm break of 1.3903 resistance should indicate short term bottoming, and turn bias back to the upside for stronger rebound to 55 D EMA (now at 1.4056).

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4150 resistance turned support holds. Firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.

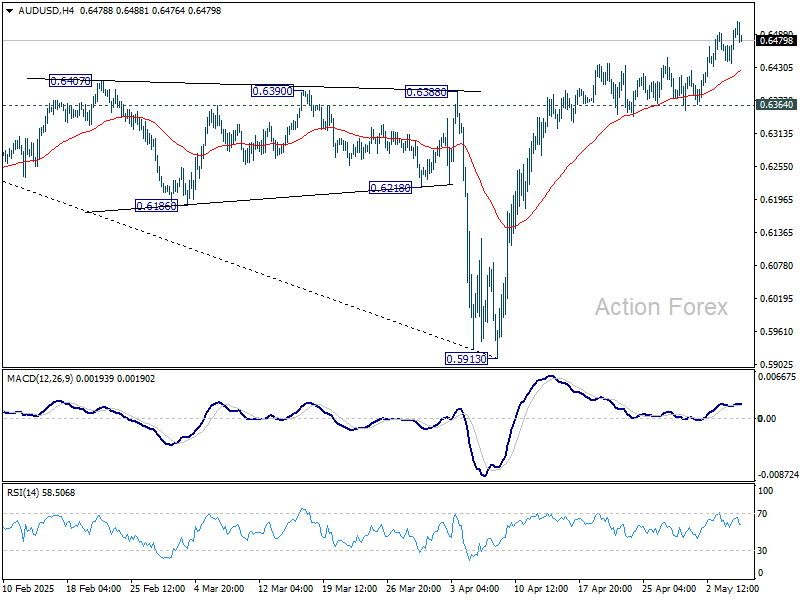

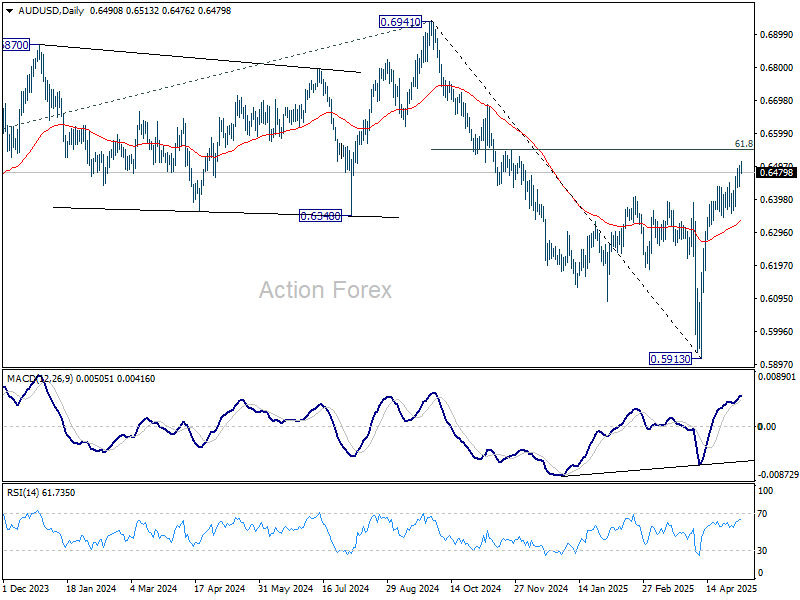

AUD/USD Daily Report

Daily Pivots: (S1) 0.6455; (P) 0.6478; (R1) 0.6519; More...

Intraday bias in AUD/USD stays mildly on the upside for the moment. Rebound from 0.5913 is in progress for 61.8% retracement of 0.6941 to 0.5913 at 0.6548. On the downside, though, break of 0.6364 support will indicate short term topping, and turn bias to the downside for 55 D EMA (now at 0.6336) and below.

In the bigger picture, as long as 55 W EMA (now at 0.6443) holds, the down trend from 0.8006 (2021 high) should resume later to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.

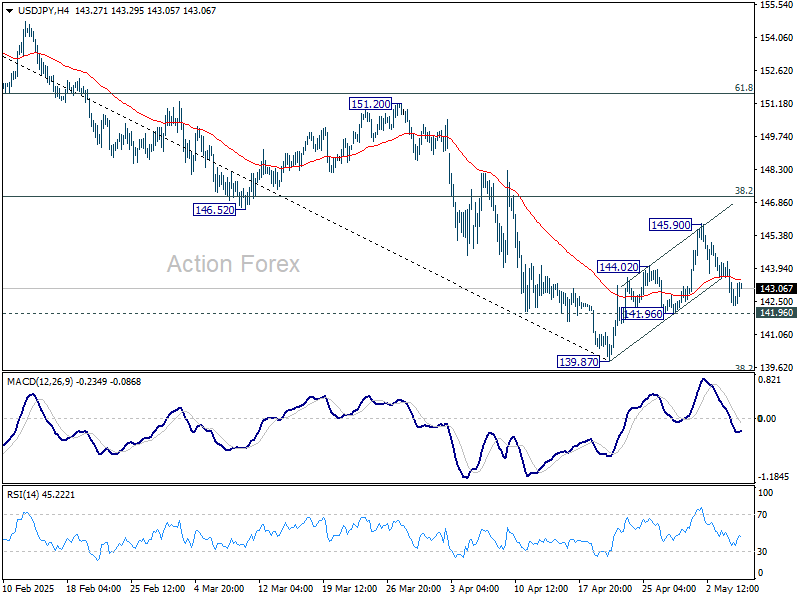

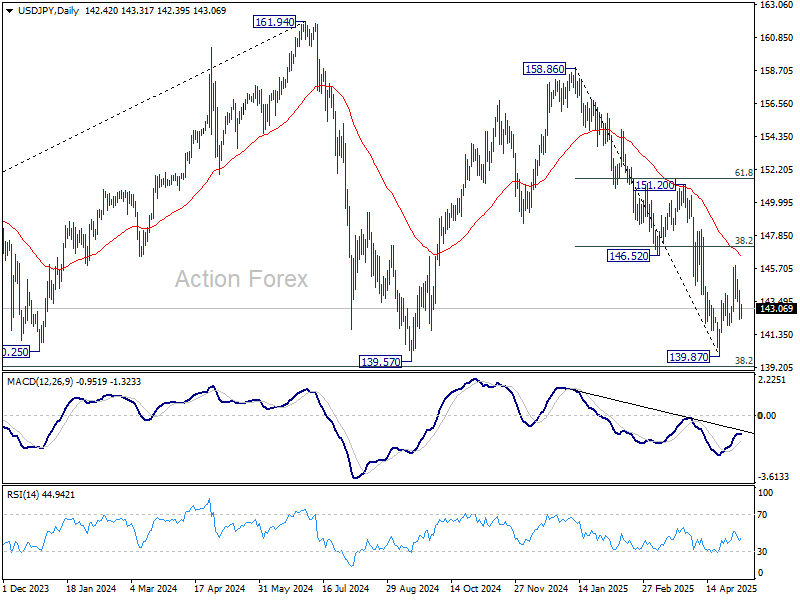

USD/JPY Daily Outlook

Daily Pivots: (S1) 141.76; (P) 143.01; (R1) 143.67; More...

USD/JPY recovered ahead of 141.96 support and intraday bias stays neutral for the moment. Rebound from 139.87 might still extend higher. But outlook will stay bearish as long as 38.2% retracement of 158.86 to 139.87 at 147.12 holds, in case of another bounce. On the downside, firm break of 141.96 will argue that rebound from 139.87 has completed as a corrective move. Retest of 139.87 should then be seen next in this case.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

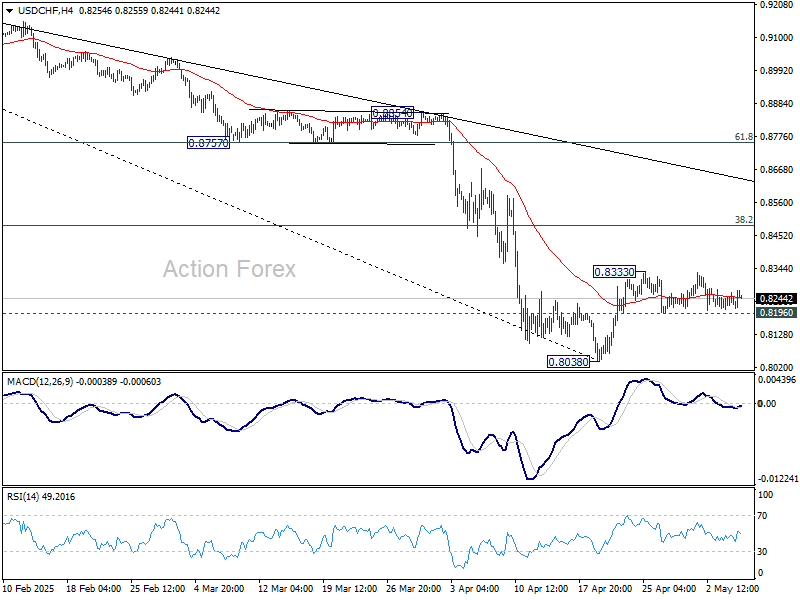

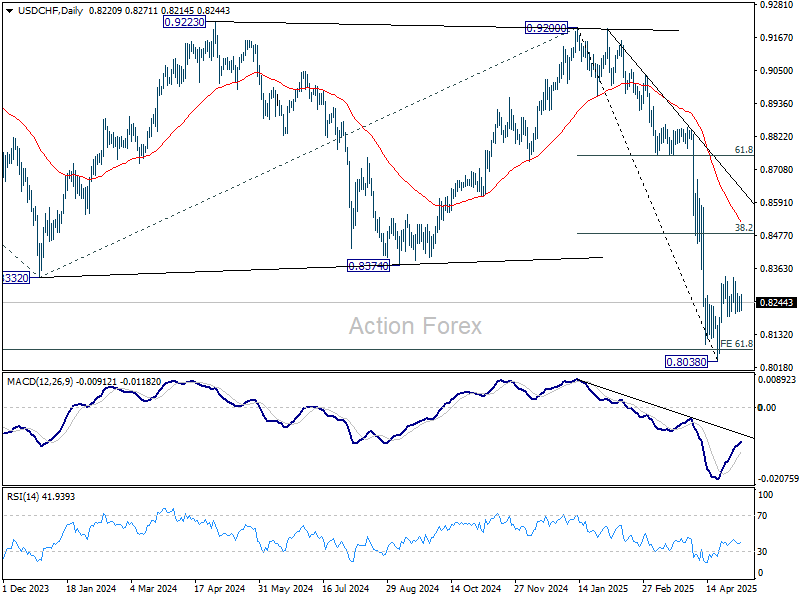

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8201; (P) 0.8233; (R1) 0.8254; More….

Range trading continues in USD/CHF below 0.8333 and intraday bias stays neutral. On the upside, above 0.8333 will resume the rebound from 0.8038. However, upside should be limited by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. On the downside, below 0.8196 minor support will bring retest of 0.8038. Firm break there will resume larger down trend.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8763) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

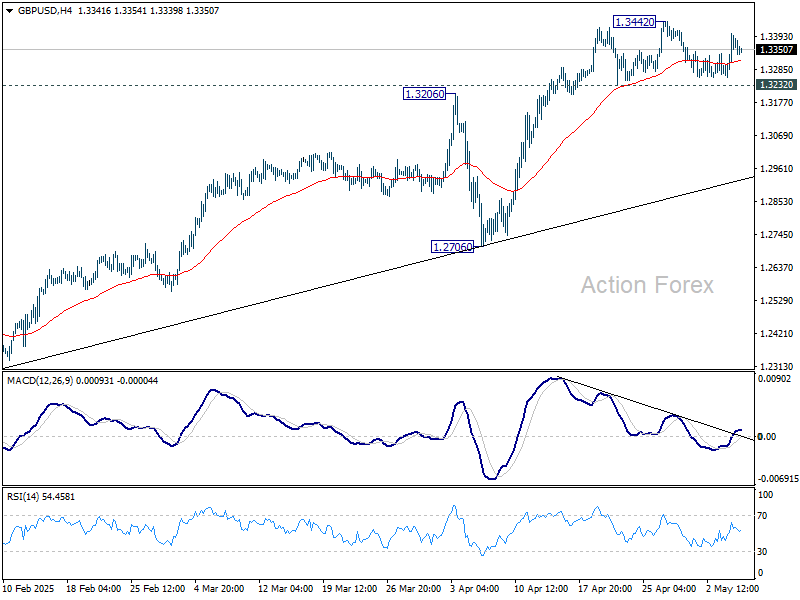

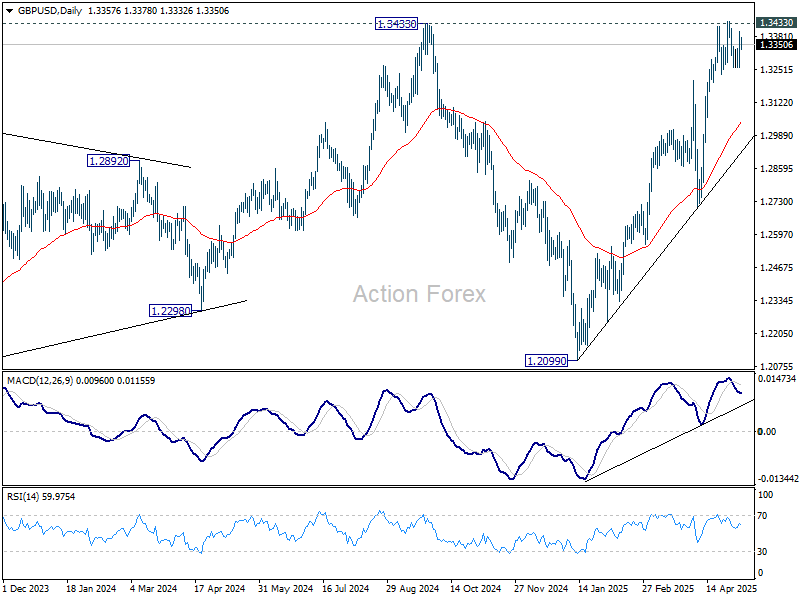

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3286; (P) 1.3344; (R1) 1.3428; More...

GBP/USD is staying in range below 1.3442 and intraday bias remains neutral. On the downside, firm break of 1.3232 support will indicate short term topping and rejection by 1.3433 key resistance. Intraday bias will be back on the downside for deeper pullback to 55 D EMA (now at 1.3044) and possibly below. On the upside, decisive break of 1.3433 key resistance will confirm larger up trend resumption.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could either be resuming the up trend, or the second leg of a consolidation pattern. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on decisive break of 1.3433 at a later stage.

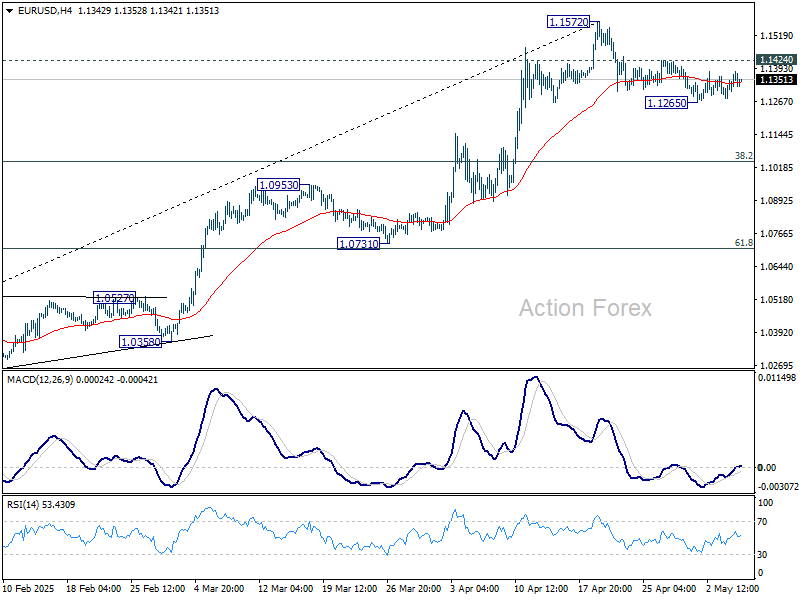

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1306; (P) 1.1344; (R1) 1.1407; More...

Intraday bias in EUR/USD remains neutral for the moment as range trading continues above 1.1265. On the downside, below 1.1265 will resume the corrective fall from 1.1572 short term top. But downside should be contained by 38.2% retracement of 1.0176 to 1.1572 at 1.1039. On the upside, break of 1.1424 will suggest that the correction has completed and bring retest of 1.1572 high.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0808) holds.

Thaw in US-China Tensions With Geneva Talk Scheduled, But Markets Stay Guarded Before FOMC

Positive developments out of Asia offered some encouragement to global investors today, though market responses remained muted. China unveiled a wide-ranging stimulus package, cutting both its seven-day reverse repo rate and the reserve requirement ratio to inject liquidity to stabilize the economy. In parallel, officials from the US and China announced plans to hold a key meeting in Geneva this Saturday, in what could mark the first serious effort to thaw trade relations since US President Donald Trump’s latest round of steep tariffs.

Despite these encouraging headlines, equity markets across Asia posted only modest gains. Currency markets showed slightly more reaction, with Kiwi outperforming after Q1 unemployment rate came in steady. Aussie and Loonie also posted small gains. Dollar is holding firmer ahead of Fed’s decision later today. Meanwhile, Yen softened, paring gains from earlier in the week. Euro is staying on the softer side. Political risk in Europe remains elevated even after Germany’s new chancellor Friedrich Merz finally secured parliamentary backing. Swiss Franc is positioning in the middle along Sterling.

On the trade front, US Treasury Secretary Scott Bessent and Trade Representative Jamieson Greer are set to meet China’s top economic planner He Lifeng in Switzerland, with both sides signalling willingness to engage. Bessent stated that current tariff levels, reaching as high as 145% on Chinese imports, amount to “an embargo." He reiterated that the US seeks “fair trade, not decoupling.” China’s official statement echoed this sentiment, saying the re-engagement decision balances “global expectations,” “China’s interests,” and the needs of “US industry and consumers.”

Canadian Prime Minister Mark Carney met with Trump overnight in what he termed a "constructive" first step toward reshaping North American trade relations. Meanwhile, the UK and India announced a new agreement that will see most goods traded become tariff-free within a decade, marking a notable milestone for the Starmer government.

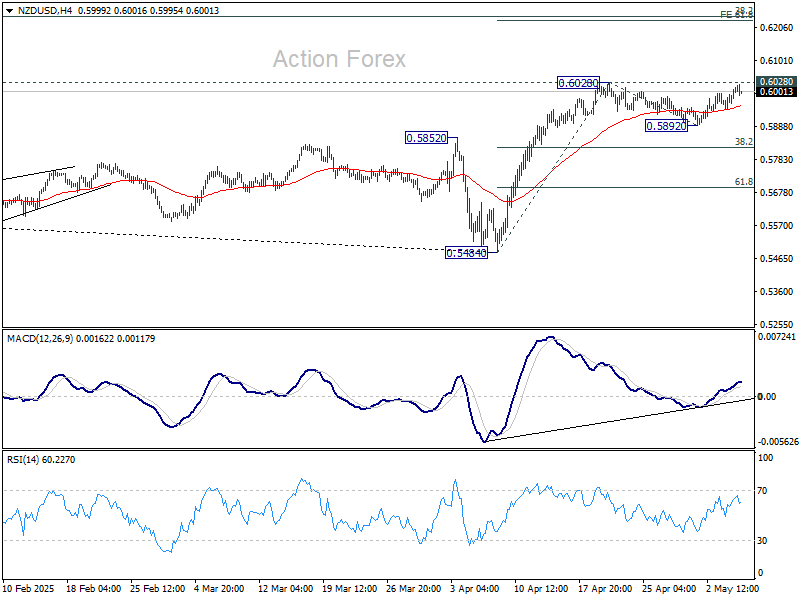

Technically, immediate focus in NZD/USD is on 0.6028 resistance. Firm break there will resume rise from 0.5484. Next target is 61.8% projection of 0.5484 to 0.6028 from 0.5892 at 0.6228. Rejection by 0.6028 will extend the consolidation pattern from there with another falling leg. But downside should be contained by 38.2% retracement of 0.5484 to 0.6028 at 0.5820 in this case.

In Asia, at the time of writing, Nikkei is up 0.06%. Hong Kong HSI is up 0.49%. China Shanghai SSE is up 0.64%. Singapore Strait Times is up 0.07%. Japan 10-year JGB yield is up 0.016 at 1.278. Overnight, DOW fell -0.95%. S&P 500 fell -0.77%. NASDAQ fell -0.87%. 10-year yield fell -0.035 to 4.308.

Looking ahead,Germany factory orders, France trade balance, Swiss foreign curreny reserves, UK PMI construction and Eurozone retail sales will be released in European session. Later in the day, main focus in on FOMC rate decision and press conference.

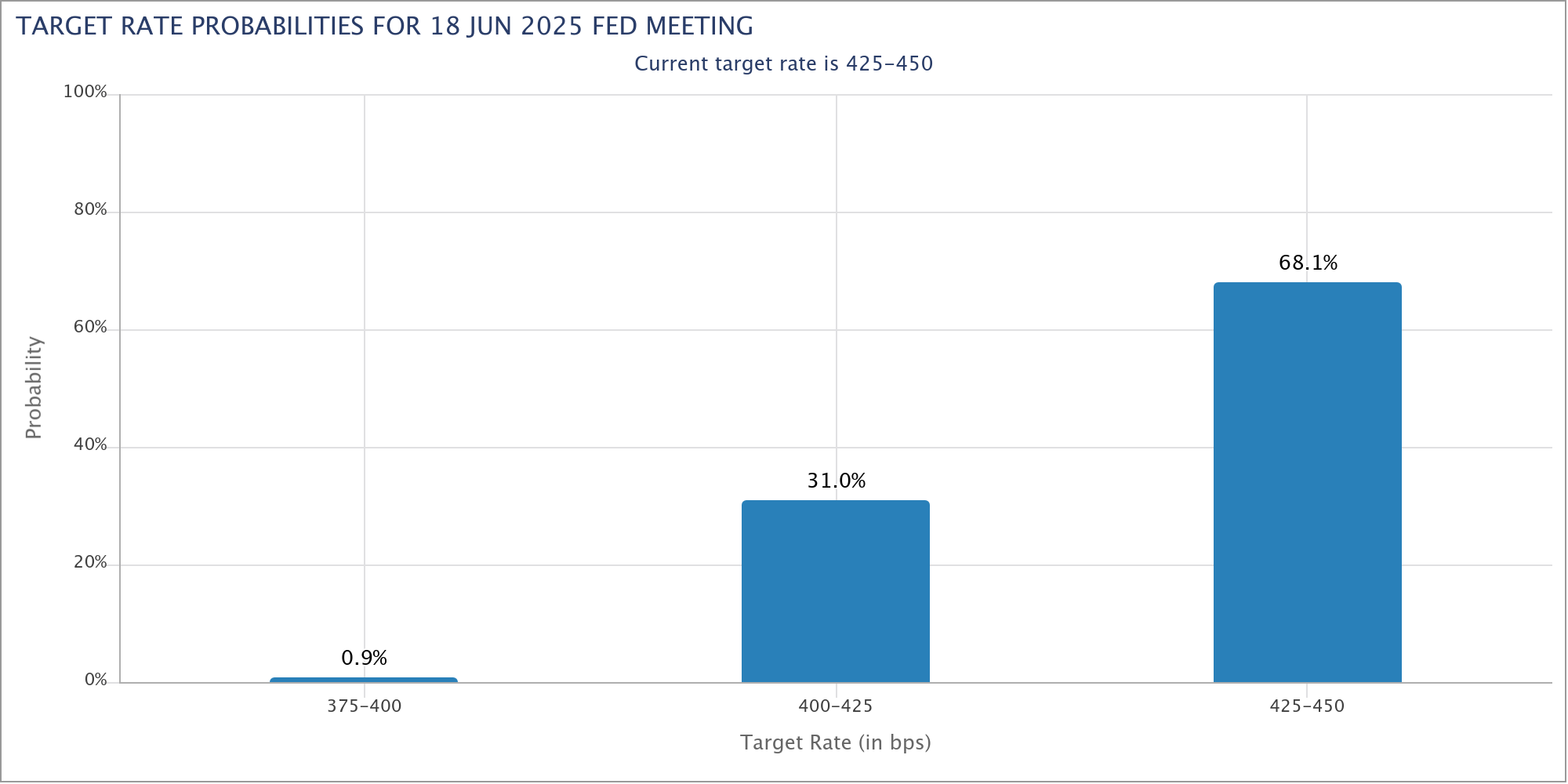

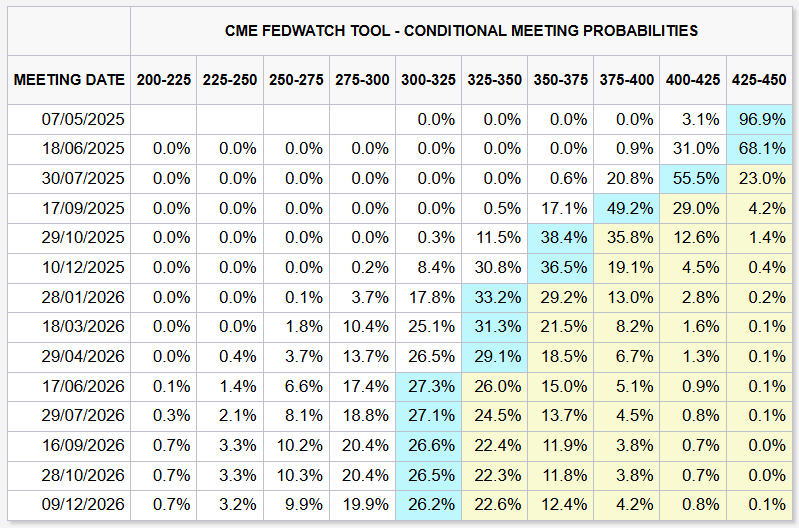

Fed to holds fire as markets look to July for next cut

Fed is widely expected to leave its benchmark interest rate unchanged at 4.25–4.50% today. With no update to its economic projections or dot plot this time, attention will turn squarely to the post-meeting statement and Chair Jerome Powell’s press conference.

The prevailing message is likely to be one of patience, as policymakers face mounting uncertainties tied to the unresolved tariff war and its eventual economic impact.

Central to Fed's wait-and-see approach is the need for clarity on two fronts: whether US President Donald Trump’s reciprocal tariffs are fully enacted, and how inflation expectations evolve in response. These factors, especially in light of ongoing geopolitical and trade risks, argue against any near-term policy moves.

As such, June is seen as too soon for a shift, with the expected to remain on hold until more definitive clarity emerge, probably not until the tariff ceasefire expires in early July.

Market pricing reflects this outlook top. Fed funds futures assign just a 32% chance of a cut in June, but expectations firm up thereafter, with roughly 75% probability of three 25 bps cuts by year-end, bringing rates down to 3.50–3.75%.

Japan’s PMI composite finalized at 51.2, input inflation jumps to 2-year high

Japan’s private sector returned to expansion in April, as the final PMI Composite rose to 51.2 from March’s 48.9. The improvement was driven entirely by the services sector, with its PMI climbing to 52.4, while manufacturing remained in contraction.

According to S&P Global’s Annabel Fiddes, stronger services activity helped offset the drag from factories, where new orders fell sharply in response to the global tariff environment.

While services firms reported stronger demand, confidence among both services and manufacturing sectors deteriorated. Businesses expressed concern about the broader global outlook and the negative implications of recent US tariff moves on growth potential.

Adding to the pressure, input price inflation accelerated to a two-year high, prompting firms to raise selling prices to protect margins.

NZ employment grow 0.1% in Q1, wages growth cool

New Zealand’s employment grew just 0.1% qoq as expected, while the unemployment rate held steady at 5.1%, better than forecast of 5.3%.

However, the quality of employment deteriorated, with a notable shift from full-time to part-time roles. Over the year, full-time employment dropped by -45k while part-time roles increased by 25k.

Participation rate edged down to 70.8% and the employment rate slipped to 67.2%, both suggesting a gradual loss in labor market momentum.

Wage growth also moderated, with the labour cost index rising 2.9% annually, down from 3.3% in the previous quarter.

PBoC unleashes broad-based monetary easing including rate and RRR cuts

China’s central bank has announced a sweeping set of monetary policy measures to support its economy, starting with a 10bps cut in the seven-day reverse repo rate to 1.40%, effective May 8. In a more aggressive move, the PBoC will also slash the reserve requirement ratio by 50bps, releasing approximately CNY 1T into the banking system.

The new package is structured into three categories: quantitative, price-based, and structural tools. The quantitative arm focuses on long-term liquidity via the RRR cut. The price-based measures involve lowering benchmark and structural policy rates. The structural component aims to channel credit into strategic areas such as technological innovation, consumption, and inclusive finance.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1306; (P) 1.1344; (R1) 1.1407; More...

Intraday bias in EUR/USD remains neutral for the moment as range trading continues above 1.1265. On the downside, below 1.1265 will resume the corrective fall from 1.1572 short term top. But downside should be contained by 38.2% retracement of 1.0176 to 1.1572 at 1.1039. On the upside, break of 1.1424 will suggest that the correction has completed and bring retest of 1.1572 high.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0808) holds.