Sample Category Title

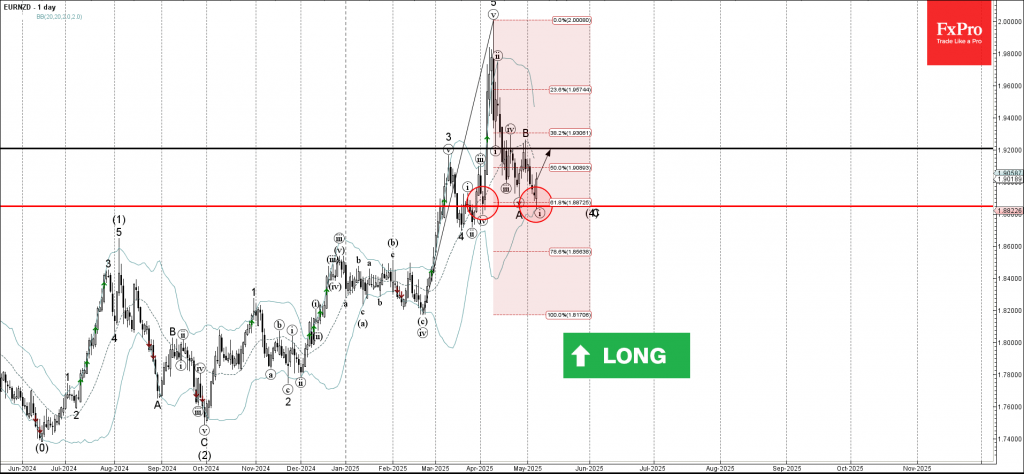

EURNZD Wave Analysis

EURNZD: ⬆️ Buy

- EURNZD reversed from support level 1.8845

- Likely to rise to resistance level 1.9200

EURNZD currency pair recently reversed from the support level 1.8845 intersecting with the lower daily Bollinger Band and the 61.8% Fibonacci correction of the upward impulse from February.

The upward reversal from the support level 1.8845 stopped the C-wave of the active medium-term ABC correction (4) from the start of April.

Given the clear daily uptrend, EURNZD currency pair can be expected to rise to the next resistance level 1.9200.

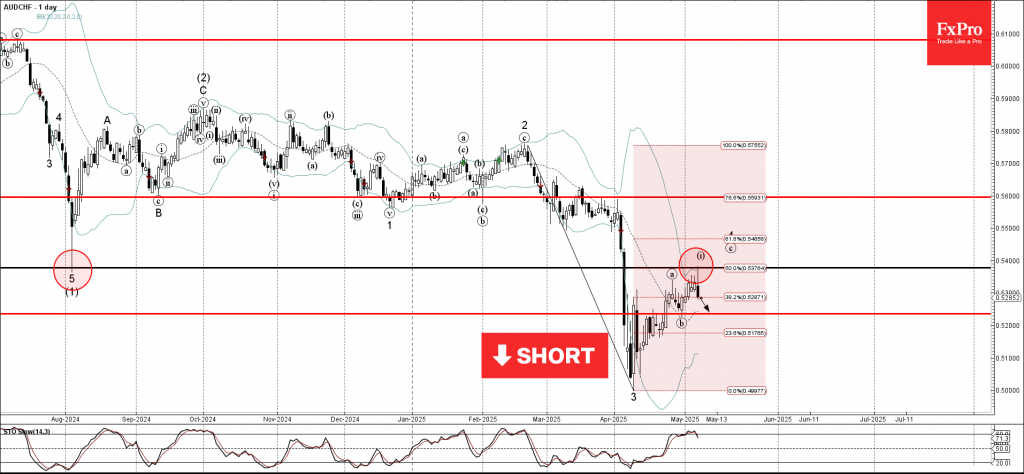

AUDCHF Wave Analysis

AUDCHF: ⬇️ Sell

- AUDCHF reversed from resistance zone

- Likely to fall to support level 0.5235

AUDCHF currency pair recently reversed down from the resistance area between the major resistance level 0.5375 (former multi-month low from last August), the upper daily Bollinger Band and the 50% Fibonacci correction of the downward impulse from February.

The downward reversal from this resistance zone stopped the previous impulse wave C of the short-term ABC correction 4 from the start of April.

Given the strength of the resistance level 0.5375, AUDCHF currency pair can be expected to fall to the next support level 0.5235 (low of the previous correction b).

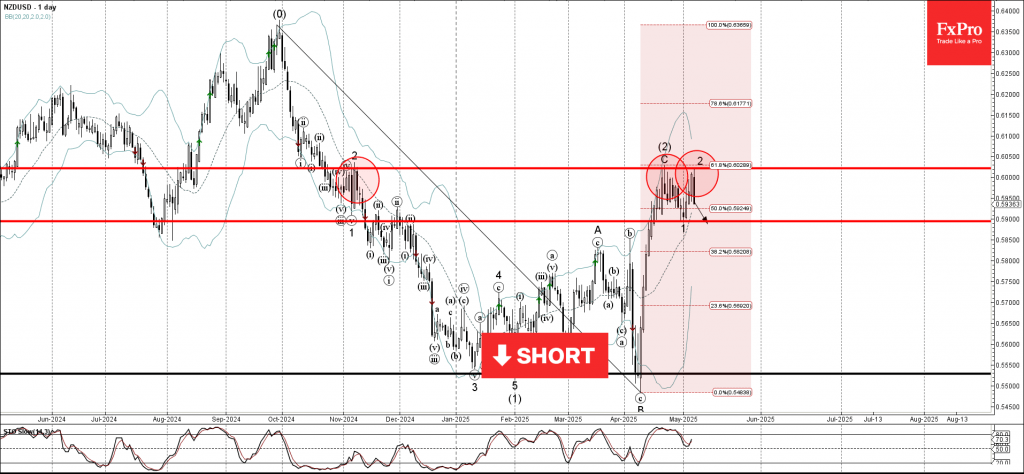

NZDUSD Wave Analysis

NZDUSD: ⬇️ Sell

- NZDUSD reversed from the resistance zone

- Likely to fall to support level 0.5900

NZDUSD currency pair recently reversed down from the resistance zone between the key resistance level 0.6020 (which has been reversing the price from November), the upper daily Bollinger Band and the 61.8% Fibonacci correction of the downward impulse from September.

The downward reversal from this resistance zone stopped the previous short-term correction 2 from the end of April.

Given the strength of the resistance level 0.6020 and the bullish USD sentiment seen today, NZDUSD currency pair can be expected to fall to the next support level 0.5900.

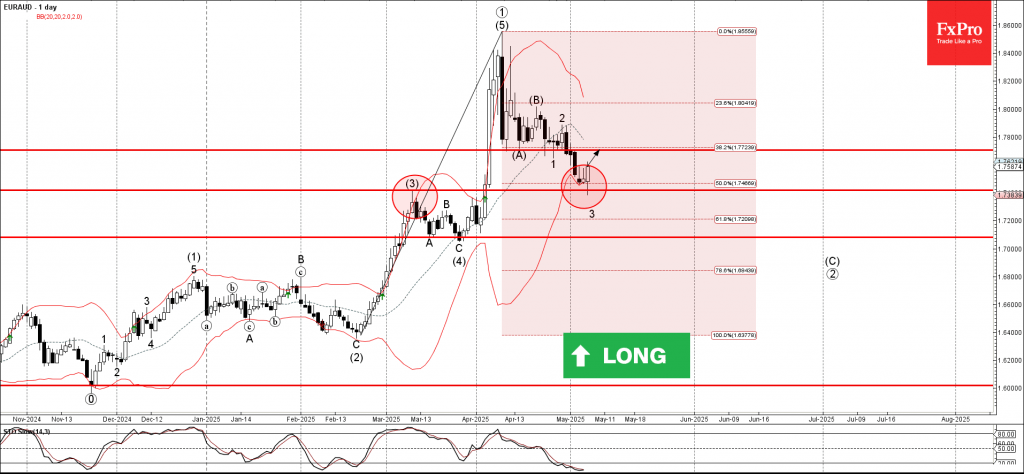

EURAUD Wave Analysis

EURAUD: ⬆️ Buy

- EURAUD reversed from the support zone

- Likely to rise to resistance level 1.7700

EURAUD currency pair recently reversed from the support zone between the support level 1.7415 (former resistance from the start of March), the lower daily Bollinger Band and the 50% Fibonacci correction of the upward impulse from February.

The upward reversal from this support zone stopped the previous short-term impulse wave 3.

Given the strength of the support level 1.7415 and the oversold daily Stochastic, EURAUD currency pair can be expected to rise to the next resistance level 1.7700.

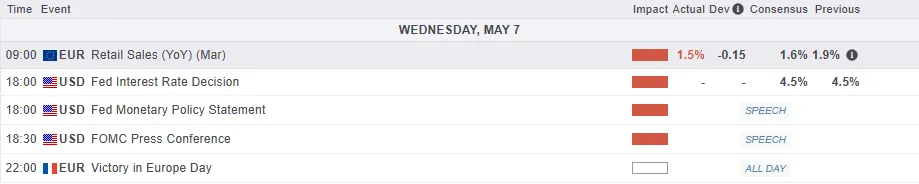

Fed stands pat, notes solid economy and elevated inflation

As expected, Fed held its benchmark interest rate unchanged at 4.25–4.50% for the fourth consecutive meeting, with a unanimous vote from the FOMC.

In its post-meeting statement, Fed acknowledged that recent data have been influenced by fluctuations in net exports, but emphasized that overall economic activity continues to expand at a "solid pace."

The statement reinforced Fed’s confidence in the labor market, noting that the unemployment rate has "stabilized at a low level" and that conditions "remain solid."

Inflation was described as “somewhat elevated.”

Full statement below.

Federal Reserve Issues FOMC Statement

Although swings in net exports have affected the data, recent indicators suggest that economic activity has continued to expand at a solid pace. The unemployment rate has stabilized at a low level in recent months, and labor market conditions remain solid. Inflation remains somewhat elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. Uncertainty about the economic outlook has increased further. The Committee is attentive to the risks to both sides of its dual mandate and judges that the risks of higher unemployment and higher inflation have risen.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 4-1/4 to 4-1/2 percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Susan M. Collins; Lisa D. Cook; Austan D. Goolsbee; Philip N. Jefferson; Neel Kashkari; Adriana D. Kugler; Alberto G. Musalem; and Christopher J. Waller. Neel Kashkari voted as an alternate member at this meeting.

(FED) Federal Reserve Issues FOMC Statement

Although swings in net exports have affected the data, recent indicators suggest that economic activity has continued to expand at a solid pace. The unemployment rate has stabilized at a low level in recent months, and labor market conditions remain solid. Inflation remains somewhat elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. Uncertainty about the economic outlook has increased further. The Committee is attentive to the risks to both sides of its dual mandate and judges that the risks of higher unemployment and higher inflation have risen.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 4-1/4 to 4-1/2 percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Susan M. Collins; Lisa D. Cook; Austan D. Goolsbee; Philip N. Jefferson; Neel Kashkari; Adriana D. Kugler; Alberto G. Musalem; and Christopher J. Waller. Neel Kashkari voted as an alternate member at this meeting.

FOMC Ahead: Will Powell Surrender the Dollar to Trump?

Markets are eagerly awaiting the outcome of the Fed meeting. Economists and analysts are unanimous that no rate changes are expected, and the rate will remain in the current range of 4.25%-4.50%. Despite developments in India and Pakistan and news of upcoming talks between the US and China, the market is poised for strong moves, remaining in a state of uncertainty about the central bank’s next steps.

Since Trump took office, the Fed has tightened its interest rate policy in response to the pro-inflationary risks expected from tariffs. Rising inflation expectations in the US confirm this trend.

Recent GDP and trade balance data showed an increase in imports before tariffs were imposed, which has a negative effect on the economy. However, this effect can be seen because of strong demand supported by positive employment data.

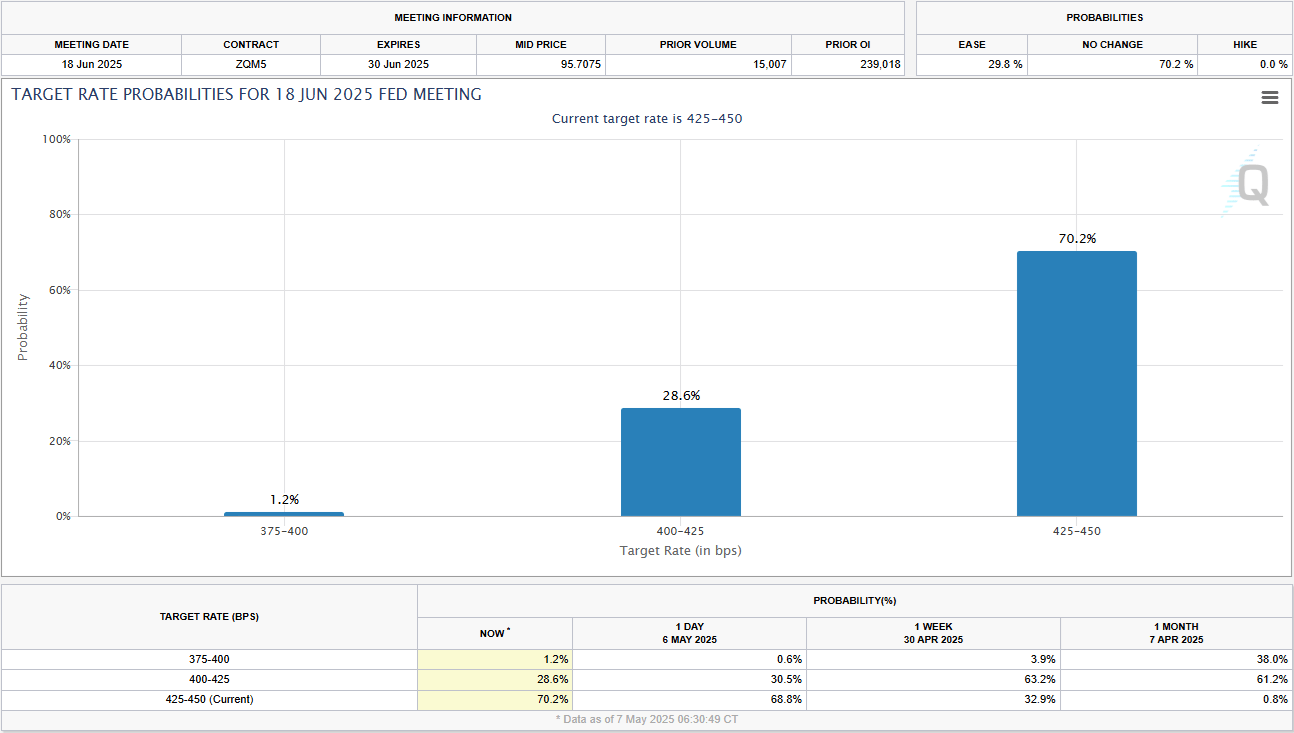

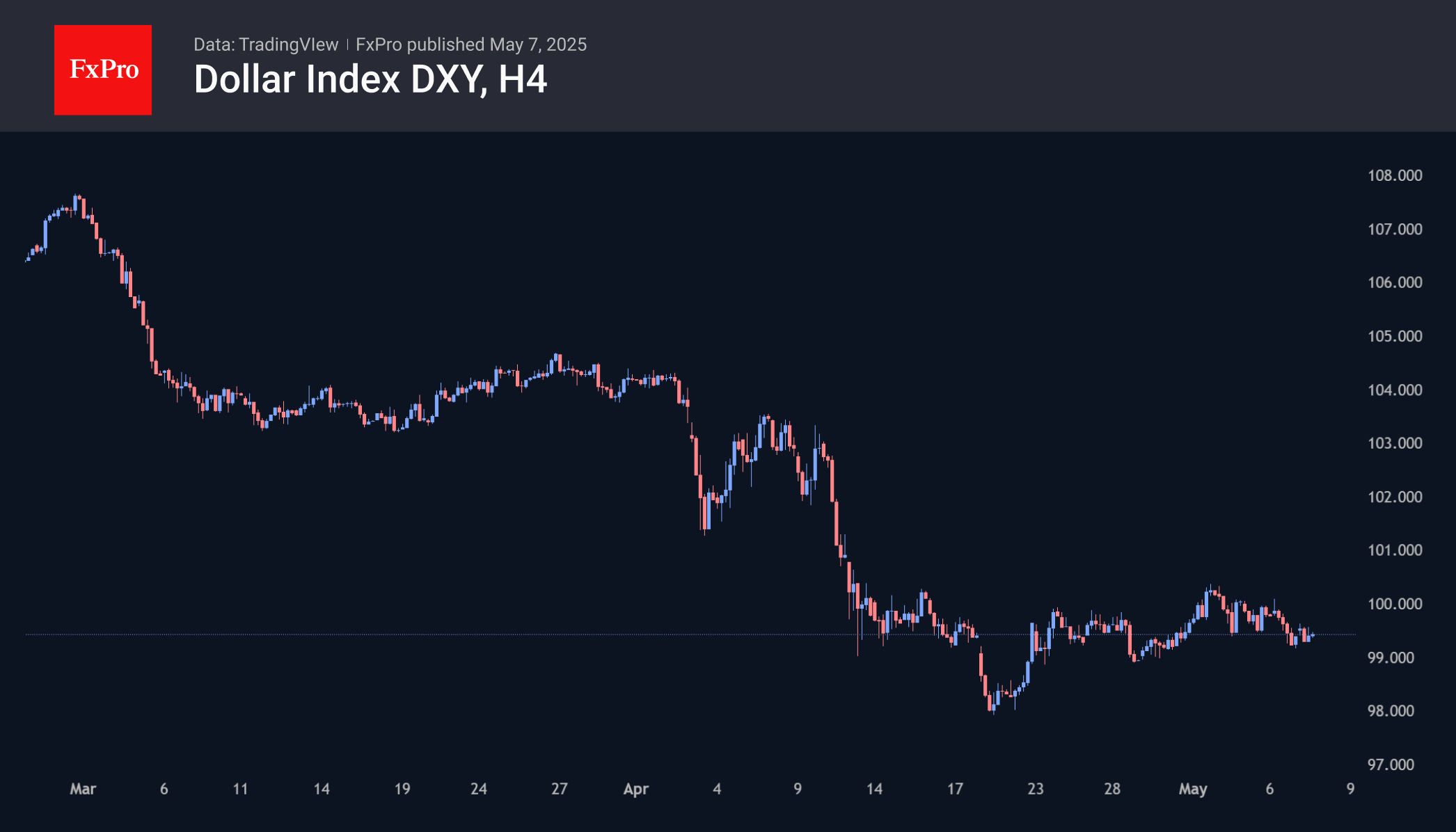

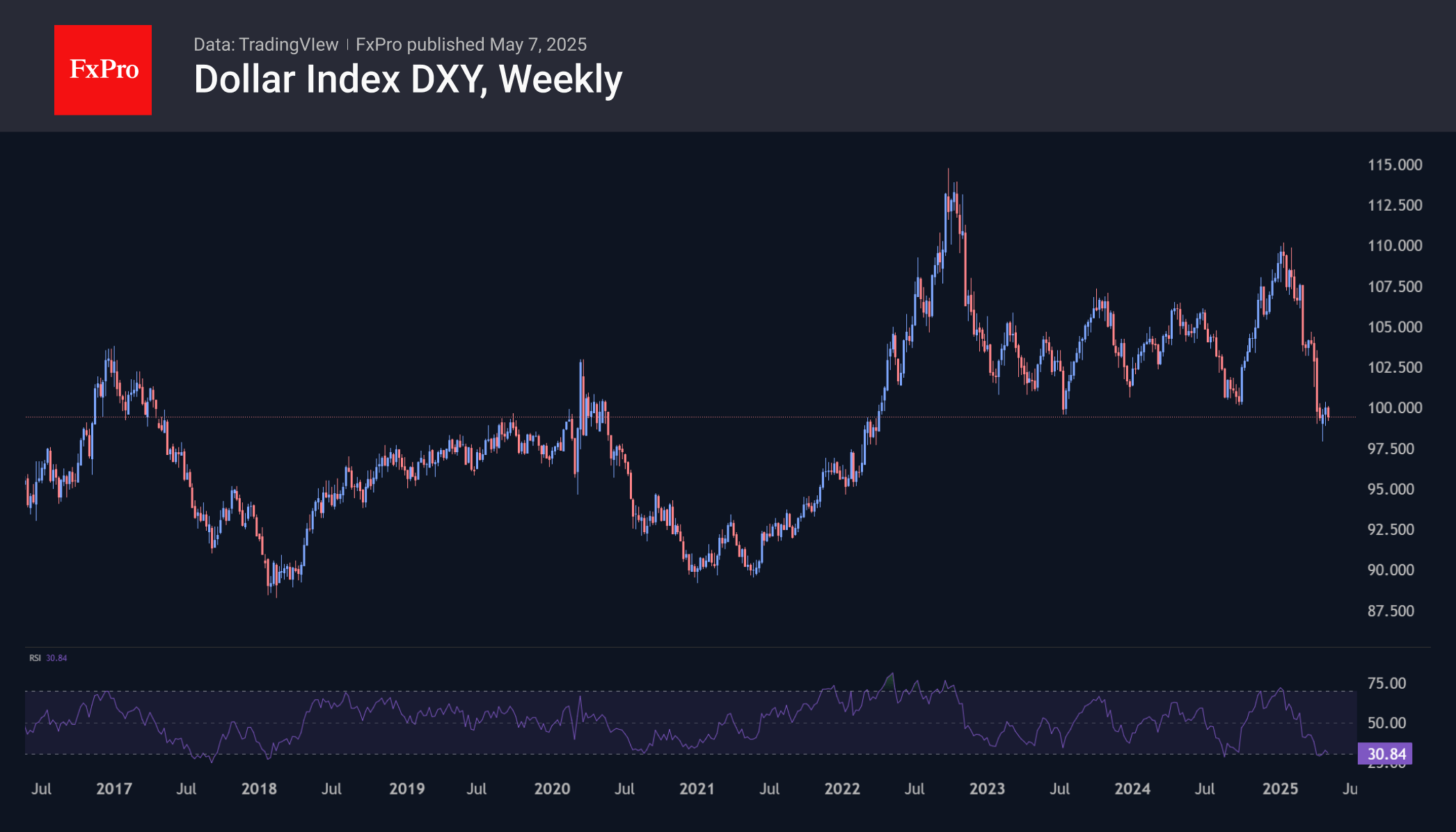

Rate expectations for the June meeting shifted in favour of ‘no change’, with a 70% probability of such an outcome versus 0.8% a month earlier. This supported the US currency. The DXY index remains at the same level as on April 11th after declining due to trade conflicts. The Fed may maintain a cautious tone on inflation, which will support the USD, but tariff disputes are the main influence on the USD exchange rate.

Since the beginning of the year, USD declines have clearly correlated with escalating tariff threats. If Powell complies with Trump’s demands and outlines the need to cut rates soon, this could lead to a USD sell-off. Historically, this behaviour has been accompanied by consolidation and continued rate cuts rather than an immediate rebound. This would also support the stock market.

However, such a reversal of events would contradict Powell’s previous statements and is not supported by significant economic data.

S&P 500 Analysis, Fed Meeting & Economic Outlook

S&P 500 and Nasdaq 100 futures rose after the U.S. and China announced a meeting in Switzerland this week. Treasury Secretary Bessent said the talks would aim to ease tensions, not make a deal, and noted that current tariff levels can't continue.

The US open has seen more caution however, with the S&P 500 trading slightly lower than its high of the day around the 5667 handle.

The S&P 500 is more than 8% away from its record high notched in February, even though all indexes have recouped declines logged since Trump's announcement of "Liberation Day" reciprocal tariffs on April 2.

On the earnings front, AMD shares rose 1.2% in premarket trading after the chipmaker predicted higher-than-expected second-quarter revenue. Disney shares jumped 8.4% as strong U.S. theme park spending and more streaming customers pushed its quarterly results above expectations. Uber shares fell 4.1% after missing revenue forecasts and warning of a 1.5% currency-related hit to second-quarter bookings growth.

Looking at the FX market, the DXY continues to struggle and seems unable to gain acceptance above the psychological 100.00 mark. This has led to gains for many currencies with the only currencies losing ground being the safe haven Yen and Swiss Franc.

Gold prices are struggling to recapture the $3400 handle as sentiment improves and haven flows continue to ebb back and forth. Gold is looking to break the $3400 handle as it trades at $3396 at the time of writing.

Economic data releases

For now the US calendar is pretty quiet in terms of data but we do have the Federal reserve interest rate meeting later today.

The Fed is expected to keep interest rates steady at 4.25%-4.50%. Traders will focus on Jerome Powell's comments to see if President Trump's policies might affect future rate cuts.

Hopes for lower rates have dropped recently due to a strong U.S. economy, especially the latest jobs report. Money markets now expect three quarter-point rate cuts this year, down from four at the start of April.

For a more comprehensive breakdown of the FOMC meeting and ways to navigate it, please read Trading the FOMC Meeting: Key Levels & Analysis for EURUSD and USDJPY

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the day - S&P 500

From a technical standpoint, the S&P 500 had risen in early trade but does appear to have run into some resistance at the 5669 handle.

The index is looking to snap a two day losing streak with a key area of resistance ahead at 5755 which houses the 200-day MA.

Following the trendline break on April 25, there does appear more scope for a move higher from a technical standpoint. However, this may only come to fruition of positive rhetoric continues on a trade deal with China.

A move beyond the 5755 handle opens up a potential run toward 5828 and 5910 respectively.

A move lower from here may find support at 5538 and 5500.

Source: TradingView.com (click to enlarge)

Sunset Market Commentary

Markets

For clues for tonight’s FOMC outcome, we grab back to Fed Chair Powell’s speech for the Economic Club of Chicago on April 16, a couple of days before the blackout period and still in the aftermath of the US tariff announcements. Powell started by pointing out that the level of the tariff increases announced so far by the new Administration is significantly larger than anticipated. The same is likely to be true of the economic effects, which will include higher inflation and slower growth. The Fed’s obligation is to keep longer-term inflation expectations well anchored and to make certain that a one-time increase in the price level does not become an ongoing inflation problem. As the central bank acts to meet that obligation, they will balance their maximum employment and price-stability mandates, keeping in mind that, without price stability, it cannot achieve the long periods of strong labor market conditions that benefit all Americans. The Fed may find itself in the challenging scenario in which their dual-mandate goals are in tension. If that were to occur, Powell suggests that they consider how far the economy is from each goal, and the potentially different time horizons over which those respective gaps would be anticipated to close. During the Q&A he stressed on multiple occasions that the Fed’s goals aren’t in tension right now with the labour market still being strong. The April unemployment rate (4.2%) was in line with the FOMC’s projection for the NAIRU. That’s a very strong hint that the Fed is well positioned to wait for greater clarity before considering any adjustments to its policy stance. It’s the way the Fed handled in the past under Powell. Once they were certain about inflation risks in 2022, they started a tightening cycle including four consecutive 75 bps rate hikes. When the Sahm rule (recession indicator) was triggered in September of last year, the Fed didn’t hesitate and implemented a 50 bps rate cut. Over the course of this year, Powell thinks that both metrics (unemployment & inflation) will on balance move away from target. Taking in mind that they’ll see how far away each is from target, this also suggests in first instance a clear focus on inflation. Inflation isn’t projected to return below the 2% target over the policy horizon while runaway inflation expectations from consumers and companies (over trade & fiscal policy) risk becoming self-fulfilling. We feel comfortable with our base case scenario of a long pause, stretching at least into September. US money and interest rate markets lowered the probability of a June Fed rate cut from 75% ahead of Powell’s speech to 30% currently. A 25 bps rate cut is discounted by the July meeting with a second one expected to follow in September. A hawkish pause by the Fed could trigger a new social media rant by US President Trump and a sell-off in US Treasuries and equities. The dollar failed to really profit from calmer market circumstances recently with EUR/USD 1.1274/76 solid support even in case of more interest rate support.

News & Views

Swedish headline inflation using a fixed interest rate (CPIF) rose by 0.2% m/m to 2.3% y/y in April compared to the 0.4% and 2.4% expected. Excluding energy, core CPIF quickened from being flat in March to 0.5% m/m to be up 3.1% y/y with both missing the bar (0.7% & 3.2%) as well. The numbers are the last data to feed into tomorrow’s Riksbank policy meeting. The main policy rate stands at 2.25% since January’s final cut with the central bank in its wake clearly hinting it could well be the final one. Money markets bought into that narrative until the Liberation Day mayhem erupted. Speculation lingered since then for further cuts to aid a sluggish and potentially further weakening economy. Odds after today’s data increased with an August cut again fully priced in. The Swedish krona depreciated slightly after the inflation print, pushing EUR/SEK to 10.91. That’s still among the strongest SEK levels of the last couple of years.

French president Macron and the freshly appointed German chancellor Merz in a joint article for Le Figaro newspaper pledged to reset ties between the two countries after both drifted apart under former German chancellor Scholz. Choosing to join forces in the face of several threats including a continental war that shattered the “illusion of guaranteed peace”, global competition and the threat of a trade war they “will make the most of Franco-German coordination and instincts to make Europe more sovereign, with an emphasis on security, competitiveness, and convergence.” The article was released so that it coincided with Merz’s visit in Paris, the chancellor’s first foreign and therefore symbolically important trip.