Sample Category Title

Pound and Dollar Lead FX on UK-US Trade Deal, BoE Cut Overshadowed

Sterling and the US Dollar are leading gains among major currencies today, lifted by anticipation surrounding the imminent announcement of a comprehensive US-UK trade agreement. The Pound remained resilient after BoE's expected 25bps rate cut. The three-way split within the BoE’s Monetary Policy Committee and the mixed implications of its economic projections have made it difficult for markets to form a decisive reaction.

BoE’s updated economic projections included two alternative scenarios, one based on weaker global demand due to trade disruptions, the other on renewed inflation stickiness from second-round effects. But with global trade dynamics in flux, these projections are highly conditional and arguably academic at this stage. A trade deal with the US may relieve some economic pressure on Britain, but its benefit depends on how the US proceeds with other partners, especially the EU and China.

For now, attention is squarely on the 1400 GMT press conference where US President Donald Trump is expected to formally unveil the UK trade deal. Trump described the agreement as “full and comprehensive,” calling it a first step in a broader realignment of US trade policy. UK Prime Minister Keir Starmer’s office confirmed talks have progressed swiftly and promised an update later today.

Meanwhile, Euro is also holding firm despite signs of growing transatlantic strain. European Commission has announced preparations for countermeasures in response to Washington’s reciprocal tariff regime, launching a WTO dispute and consulting on duties affecting EUR 95B worth of US imports. Still, EC President Ursula von der Leyen emphasized a preference for negotiation, suggesting room remains for diplomacy.

In contrast, Yen is the weakest major currency today, Loonie and Swiss Franc. Aussie and Kiwi are positioning in the middle.

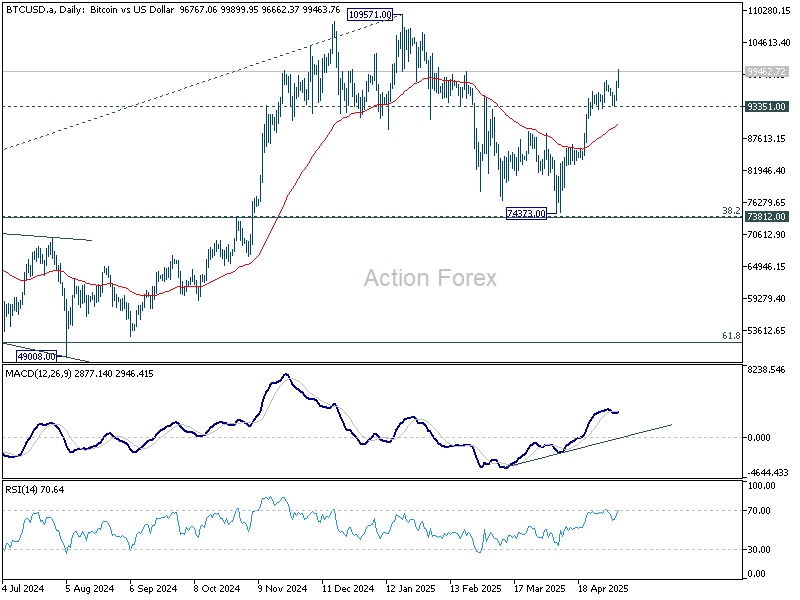

Technically, Bitcoin's rally from 74373 resumed today by breaking through 97944 resistance. Further rally is expected as long as 93351 support holds, to retest 109571 record high. Nevertheless, barring clear sign of upside acceleration, current rise is seen as the second leg a medium term corrective pattern. Hence, strong resistance is expected from 109571 to limit upside to bring near term reversal.

In Europe, at the time of writing, FTSE is up 0.17%. DAX is up 0.80%. CAC is up 0.92%. UK 10-year yield is up 0.025 at 4.489. Germany 10-year yield is up 0.018 at 2.494. Earlier in Asia, Nikkei rose 0.41%. Hong Kong HSI rose 0.37%. China Shanghai SSE rose 0.28%. Singapore Strait Times fell -0.44%. Japan 10-year JGB yield rose 0.025 to 1.325.

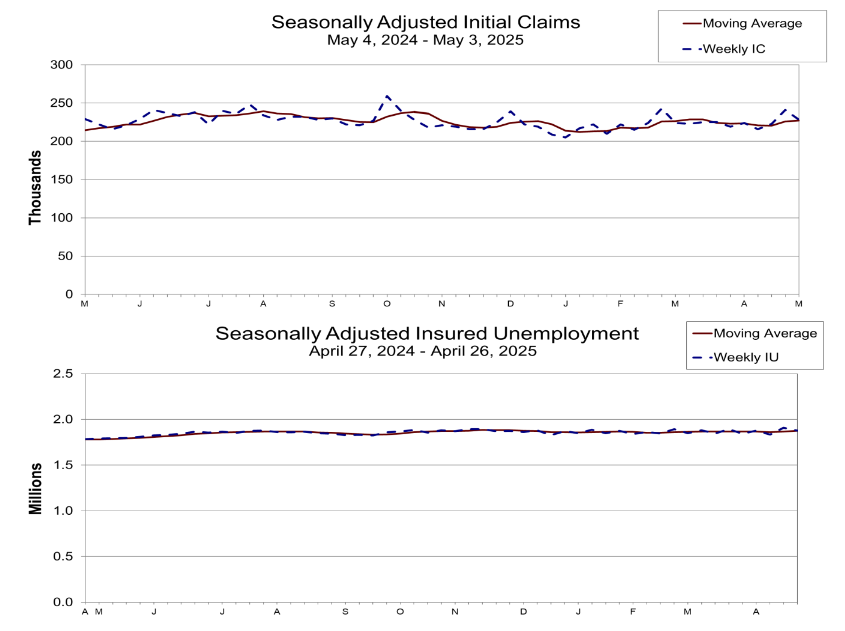

US initial jobless claims fall to 228k vs exp 235k

US initial jobless claims fell -13k to 228k in the week ending May 3, below expectation of 235k. Four-week moving average of initial claims rose 1k to 227k.

Continuing claims fell -29k to 1879k in the week ending April 26. Four-week moving average of continuing claims rose 9k to 1875k.

BoE cuts 25bps, three-way vote split reveals growing rift on rate path

BoE lowered its benchmark Bank Rate by 25 basis points to 4.25% , in line with market expectations. However, the decision revealed a rare three-way split among policymakers.

Five members supported the 25bps reduction, while Catherine Mann and Chief Economist Huw Pill voted to keep rates unchanged. On the dovish end, Swati Dhingra and Alan Taylor backed a deeper 50bps cut.

In its accompanying statement, BoE reiterated that a "gradual and careful approach" remains appropriate as it withdraws monetary restraint.

While acknowledging progress on inflation, the central bank emphasized the need for policy to stay “restrictive for sufficiently long” to ensure inflation returns sustainably to the 2% target.

In its latest Monetary Policy Report, the BoE’s baseline forecast sees CPI inflation rising to 3.5% in Q3 2025 before easing back to 2% in the medium term.

But policymakers outlined two risk-laden alternative scenarios. The first, a lower demand scenario, assumes heightened uncertainty depresses domestic spending and inflationary pressures fade more quickly. Under this path, the economy faces a wider output gap and inflation runs -0.3% lower than baseline by the three-year horizon.

Conversely, the second scenario envisions higher inflation persistence, where near-term rise in headline inflation triggers second-round effects in wages and prices, compounded by weak productivity growth. In this case, the impact on growth is modest, but inflation runs 0.4% above baseline throughout the forecast period.

RBNZ flags global growth risks as tariffs echo COVID-era disruptions

RBNZ Governor Christian Hawkesby warned today that rising global tariffs are having a clear and negative impact on global economic activity, prompting the central bank to revise down its projections for global growth.

Speaking to a parliamentary committee, Hawkesby called the effects of the tariff wave “unambiguously” harmful. He added that while New Zealand’s exposure to a 10% US tariff on exports poses challenges, the softer New Zealand Dollar may help cushion some of the blow. Nonetheless, weaker demand from key trading partners is now a growing concern for the country’s outlook.

Hawkesby drew a stark comparison between the supply-side disruptions caused by current tariffs and those seen during the COVID-19 pandemic, stressing that both are capable of delivering long-lasting economic distortions.

“We know from our experience, from the COVID experience, that supply side impacts are significant, and that are long-lasting and can create real challenges,” he said.

He added that the situation remains fluid, with considerable uncertainty about how the structural dynamics of the global economy will adjust to this new trade regime.

BoJ minutes: Caught between global uncertainty and domestic price pressures

Minutes from BoJ’s March meeting revealed growing concern among policymakers over the external risks posed by US tariff policies.

One member warned that downside risks from these policies had “rapidly heightened” and could significantly harm Japan’s real economy, suggesting BoJ should "be particularly cautious when considering the timing for the next rate hike."

However, not all board members advocated for a cautious stance. Another member stressed that even amid heightened uncertainty, BoJ should not automatically default to a cautious stance, stating that BOJ "might face a situation where it should act decisively".

A third voice on the board emphasized the importance of incorporating inflation expectations, upside risks to prices, and progress in wage growth into BoJ’s policy deliberations. Domestic developments could still justify tightening if conditions shift meaningfully.

Separately, BoJ Governor Kazuo Ueda reinforced this message in his remarks to parliament today, acknowledging that while food price volatility, particularly for rice, remains elevated, these pressures would ease over time.

Nonetheless, Ueda emphasized the importance of monitoring price developments closely, given the elevated uncertainty in the global economic environment.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.81; (P) 143.40; (R1) 144.43; More...

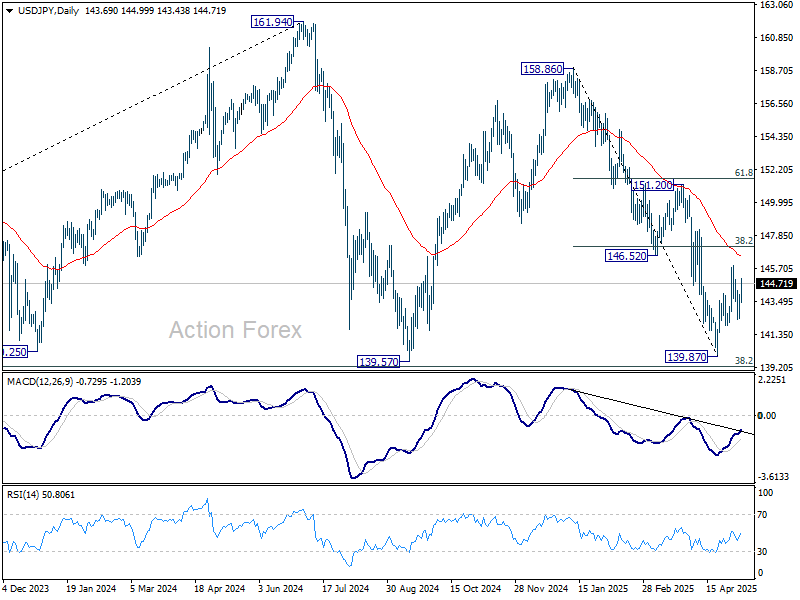

USD/JPY rebounded further today but stays below 145.90 resistance. Overall, rise from 139.87 could extend through 145.90. But near term outlook will stay bearish as long as 38.2% retracement of 158.86 to 139.87 at 147.12 holds, in case of another bounce. On the downside, firm break of 141.96 will argue that rebound from 139.87 has completed as a corrective move. Retest of 139.87 should then be seen next in this case.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

US initial jobless claims fall to 228k vs exp 235k

US initial jobless claims fell -13k to 228k in the week ending May 3, below expectation of 235k. Four-week moving average of initial claims rose 1k to 227k.

Continuing claims fell -29k to 1879k in the week ending April 26. Four-week moving average of continuing claims rose 9k to 1875k.

BoE cuts 25bps, three-way vote split reveals growing rift on rate path

BoE lowered its benchmark Bank Rate by 25 basis points to 4.25% , in line with market expectations. However, the decision revealed a rare three-way split among policymakers.

Five members supported the 25bps reduction, while Catherine Mann and Chief Economist Huw Pill voted to keep rates unchanged. On the dovish end, Swati Dhingra and Alan Taylor backed a deeper 50bps cut.

In its accompanying statement, BoE reiterated that a "gradual and careful approach" remains appropriate as it withdraws monetary restraint.

While acknowledging progress on inflation, the central bank emphasized the need for policy to stay “restrictive for sufficiently long” to ensure inflation returns sustainably to the 2% target.

In its latest Monetary Policy Report, the BoE’s baseline forecast sees CPI inflation rising to 3.5% in Q3 2025 before easing back to 2% in the medium term.

But policymakers outlined two risk-laden alternative scenarios. The first, a lower demand scenario, assumes heightened uncertainty depresses domestic spending and inflationary pressures fade more quickly. Under this path, the economy faces a wider output gap and inflation runs -0.3% lower than baseline by the three-year horizon.

Conversely, the second scenario envisions higher inflation persistence, where near-term rise in headline inflation triggers second-round effects in wages and prices, compounded by weak productivity growth. In this case, the impact on growth is modest, but inflation runs 0.4% above baseline throughout the forecast period.

(BOE) Bank Rate reduced to 4.25%

Monetary Policy Summary, May 2025

The Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. The MPC adopts a medium-term and forward-looking approach to determine the monetary stance required to achieve the inflation target sustainably.

At its meeting ending on 7 May 2025, the MPC voted by a majority of 5–4 to reduce Bank Rate by 0.25 percentage points, to 4.25%. Two members preferred to reduce Bank Rate by 0.5 percentage points, to 4%. Two members preferred to maintain Bank Rate at 4.5%.

There has been substantial progress on disinflation over the past two years, as previous external shocks have receded, and as the restrictive stance of monetary policy has curbed second-round effects and stabilised longer-term inflation expectations. That progress has allowed the MPC to withdraw gradually some degree of policy restraint, while maintaining Bank Rate in restrictive territory so as to continue to squeeze out persistent inflationary pressures.

Underlying UK GDP growth is judged to have slowed since the middle of 2024, and the labour market has continued to loosen.

Progress on disinflation in domestic price and wage pressures is generally continuing. Twelve-month CPI inflation fell to 2.6% in March from 2.8% in February, close to expectations in the February Monetary Policy Report. Although indicators of pay growth remain elevated, a significant slowing is still expected over the rest of the year. Wholesale energy prices have fallen back since the February Report. Previous increases in energy prices are still likely to drive up CPI inflation from April onwards, to 3.5% for 2025 Q3. Inflation is expected to fall back thereafter. Measures of household inflation expectations have risen recently.

Uncertainty surrounding global trade policies has intensified since the imposition of tariffs by the United States and the measures taken in response by some of its trading partners. There has subsequently been volatility in financial markets, and market-implied policy rates have moved lower. Prospects for global growth have weakened as a result of this uncertainty and new tariff announcements, although the negative impacts on UK growth and inflation are likely to be smaller.

The Committee remains focused on returning CPI inflation sustainably to target in the medium term. In deciding the appropriate degree and pace of monetary policy adjustments required to achieve this, the Committee has considered a range of possibilities for how domestic inflationary pressures could evolve, as well as the broader circumstances that could necessitate varying the course of policy.

The May Report sets out two illustrative scenarios. In one scenario, there could be weaker supply and more persistence in domestic wages and prices, including from second-round effects related to the near-term increase in CPI inflation. In another scenario, inflationary pressures could ease more quickly owing to greater or longer-lasting weakness in demand relative to supply, in part reflecting uncertainties globally and domestically.

Monetary policy is not on a pre-set path. The Committee will remain sensitive to heightened unpredictability in the economic environment and will continue to update its assessment of risks.

At this meeting, the Committee voted to reduce Bank Rate to 4.25%, reflecting continued progress in disinflation though with risks to inflation remaining in both directions.

Based on the Committee’s evolving view of the medium-term outlook for inflation, a gradual and careful approach to the further withdrawal of monetary policy restraint remains appropriate. The Committee will continue to monitor closely the risks of inflation persistence and what the evidence may reveal about the balance between aggregate supply and demand in the economy. Monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further. The Committee will decide the appropriate degree of monetary policy restrictiveness at each meeting.

Minutes of the Monetary Policy Committee meeting ending on 7 May 2025

1: Before turning to its immediate policy decision, the Committee discussed: the international economy; monetary and financial conditions; demand and output; and supply, costs and prices. The latest data on these topics were set out in the accompanying May 2025 Monetary Policy Report.

2: The Committee discussed recent global economic developments, and in particular the likely impact on the outlook for UK inflation of the various changes to trade tariffs that had recently been announced by the United States and some of its trading partners. These potential impacts were discussed in more detail in Box C of the May Report.

3: These trade policy developments were likely to reduce UK activity, and to create further risks to the downside. The impact on UK inflation was more ambiguous at this stage. The baseline expectation was that these developments would push down slightly on inflation over the forecast period. There were material risks on both sides around this judgement, however, including from: weaker global demand; the degree of diversion of exports to non-US markets; how closely the pass-through from global export prices to domestic consumer prices matched previous experience; the level of disruption to supply chains; the extent of further tariff policy announcements; and the risk of broader fragmentation of the global economy and financial system. The Committee would monitor the relevant indicators closely, and would continue to use multiple analytical approaches to evaluate the impact of these developments.

4: Financial markets had been volatile globally following the trade policy announcements in early April, as set out in the May Report. Almost all respondents to the Bank’s latest Market Participants Survey (MaPS) were expecting a 25 basis point reduction in Bank Rate at this MPC meeting, in line with market pricing. Since the MPC's previous meeting the median MaPS respondent expected 75 basis points of further Bank Rate cuts this year, although the overall distribution was now skewed towards more cuts. This was consistent with the market-implied path declining by just under 100 basis points over the rest of the year.

5: The Committee discussed the extent to which movements in UK markets had reflected international factors. International considerations had clearly been the most prominent influence during this period, although, given the US-specific nature of the tariff policy announcements, it was not surprising that the previously close relation between US and UK markets had weakened appreciably in recent weeks. MaPS respondents reported that international factors had generally pushed down on the prospects for activity and inflation, and therefore on near-term UK policy rate expectations, partly offset by the upward impact of domestic factors on inflation.

6: Monthly GDP growth in February had been much stronger than expected, at 0.5%, and Bank staff now estimated that headline GDP growth in 2025 Q1 had been 0.6%. But this news had been accounted for largely by erratic factors, for instance those that had affected output in the manufacturing sector. Bank staff estimated that underlying growth in Q1 had been around zero. Headline GDP growth was projected to slow sharply in Q2, to 0.1%, with risks to the downside, given the signal from high-frequency data. The S&P Global UK composite output PMI had fallen sharply in April, although it remained unclear how much of this decline stemmed from a potentially reversible deterioration in business sentiment.

7: The Committee discussed the extent to which developments in activity had reflected underlying demand and supply drivers, acknowledging that both were likely to have played a role. In the baseline forecast, a margin of slack was expected to continue to open up over the coming years, sufficient to remove remaining excess inflation persistence. Conditioned on the market-implied path for Bank Rate, monetary policy was expected to continue to restrain aggregate demand, while fiscal consolidation was expected to play a greater role in the latter part of the forecast. Potential productivity growth was also expected to pick up. The balance of risks around the baseline forecast for GDP growth was judged to be somewhat to the downside.

8: Twelve-month CPI inflation had fallen to 2.6% in March. The latest evidence from key indicators suggested that progress on underlying disinflation in domestic prices and wages had generally continued, supported by the restrictiveness of monetary policy.

9: The Committee discussed the outlook for a range of nominal indicators. Private sector regular pay growth was expected to slow significantly further by the end of 2025, to around 3¾%, consistent with the latest indications from the Bank’s Agents’ contacts, and from the DMP Survey. That said, survey measures of household inflation expectations had risen further in recent months, perhaps suggesting that households had become more sensitive to inflationary pressures, having recently experienced very high rates of inflation in 2022. Businesses’ medium-term CPI inflation expectations had increased slightly recently, although indicators of medium-term inflation expectations derived from financial markets had generally continued to trend downwards.

10: CPI inflation was expected to rise to a peak of 3.5% on average in 2025 Q3, in large part reflecting developments in household energy bills and, to a lesser degree, regulated prices. This projected increase in headline inflation was still expected to be temporary. The Committee recognised the risk that this projected increase in headline inflation, along with the current trajectory of household inflation expectations, might pose additional risks to persistence if non-linearities were to emerge beyond specific inflation thresholds.

The immediate policy decision

11: The Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. The MPC adopts a medium-term and forward-looking approach to determine the monetary stance required to achieve the inflation target sustainably.

12: Underlying UK GDP growth was judged to have slowed since the middle of 2024, and the labour market had continued to loosen.

13: Progress on disinflation in domestic price and wage pressures had generally continued. Twelve-month CPI inflation was 2.6% in March, close to expectations in the February Monetary Policy Report. Although indicators of pay growth had remained elevated, a significant slowing was still expected over the rest of the year. Wholesale energy prices had fallen back since the February Report. Previous increases in energy prices were still likely to drive up CPI inflation from April onwards, to 3.5% on average in 2025 Q3. Inflation was expected to fall back thereafter.

14: Uncertainty surrounding global trade policies had intensified since the imposition of tariffs by the United States and the measures taken in response by some of its trading partners. There had subsequently been volatility in financial markets, and market-implied policy rates had moved lower. Prospects for global growth had weakened as a result of this uncertainty and new tariff announcements, although the negative impacts on UK growth and inflation were likely to be smaller.

15: The Committee remained focused on returning inflation sustainably to the target. In the baseline forecast set out in the May Monetary Policy Report, inflation was expected to return to around the 2% target in the medium term. Overall, the Committee judged that the risks around GDP growth in the baseline forecast were somewhat to the downside, while the risks around the CPI projection were two-sided.

16: In reaching its judgement, and against a backdrop of increased uncertainty, the Committee had been assessing a wide range of risks around the baseline forecast, from both domestic and global factors. The May Monetary Policy Report set out two illustrative scenarios from a much broader set of plausible paths the economy could take. These were intended to explore different economic mechanisms, to which members attached different weights.

17: In the first scenario, greater or longer-lasting weakness in demand relative to supply, in part reflecting uncertainties globally and domestically, might further mitigate inflationary pressures over the medium term. Underlying GDP growth had been weak, and global trade policy uncertainty had risen sharply, which was likely to weigh on household consumption and business investment. It was possible in this environment of uncertainty that precautionary saving could rise and consumption could weaken.

18: In the second scenario, greater persistence in domestic wage- and price-setting, both from additional second-round effects related to the near-term increase in headline CPI inflation and from weaker aggregate supply, might exacerbate the persistence of inflation. Underlying services consumer price inflation and indicators of wage growth had been moderating, but remained at elevated levels. There was evidence that the near-term inflation expectations of firms and households had recently become more reactive to changes in current CPI inflation than they had been pre-Covid. In addition, there were upside risks to inflation stemming from softer growth in potential productivity.

19: More broadly, there were growing risks from potential global trade arrangements. Depending on how trade policies unfolded, UK inflation could be affected by a wide range of factors such as shifts in trade patterns, supply chain disruptions in the UK and abroad, and movements in global exchange rates. It was possible that the ultimate net effect of these developments could be materially more disinflationary for the UK than in the baseline forecast, but it was also possible that the effect could be slightly inflationary in the longer term. Overall, it was too early to conclude over what period and to what degree different economic effects could materialise.

20: All members stressed that monetary policy was not on a pre-set path. The Committee would remain sensitive to heightened unpredictability in the economic environment and would continue to update its assessment of risks.

21: At this meeting, five members voted to reduce Bank Rate to 4.25%. Prior to the latest global developments, most members in this group had judged that this policy decision would be finely balanced between no change in Bank Rate and a further reduction. Although the current impact of the global trade news should not be overstated, the news was sufficient for those members to judge that a reduction in Bank Rate was warranted. This level of Bank Rate would still leave the stance of monetary policy sufficiently restrictive to bear down on inflationary pressures, were they to re-intensify. For the other members in this group, even in the absence of the latest global news, the case for a reduction in Bank Rate at this meeting had been fairly clear. Underlying domestic disinflation was progressing as expected and monetary policy restrictiveness was bearing down on activity.

22: Two members preferred a 0.5 percentage point reduction in Bank Rate at this meeting based on the outlook. The most significant contributions to the expected pickup in inflation would come from one-off tax and administered prices and past energy shocks. Incoming wage settlements had so far been close to the Agents’ annual pay survey figure for the end of 2025, and were approaching sustainable rates, while consumer spending remained weak and investment subdued. Along with domestic demand shifts and emerging slack, recent global developments in energy and trade policy pointed to potential downward risks to global growth and world export prices. In the medium term, a continued monetary policy stance that was too restrictive risked inflation deviating from the 2% target on a sustained basis and the opening up of an unduly large output gap. Given this balance of risks, a less restrictive policy path was warranted.

23: Two members preferred to hold Bank Rate at 4.5%, recognising that short-end market interest rates had already eased by around 40 basis points since the MPC’s previous meeting. For these members, the labour market was proving more resilient than expected, business surveys signalled continued inflationary pressures, and household expectations of inflation had firmed. All these indicators pointed to continued inflation persistence owing in part to structural rigidities on the supply side of the economy. Holding Bank Rate unchanged at this meeting would ensure that monetary policy remained sufficiently restrictive to weigh against stubborn inflationary pressures.

24: Based on the Committee’s evolving view of the medium-term outlook for inflation, a gradual and careful approach to the further withdrawal of monetary policy restraint remained appropriate. The Committee would continue to monitor closely the risks of inflation persistence and what the evidence may reveal about the balance between aggregate supply and demand in the economy. Monetary policy would need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term had dissipated further. The Committee would decide the appropriate degree of monetary policy restrictiveness at each meeting.

25: The Chair invited the Committee to vote on the proposition that:

- Bank Rate should be reduced by 0.25 percentage points, to 4.25%.

26: Five members (Andrew Bailey, Sarah Breeden, Megan Greene, Clare Lombardelli and Dave Ramsden) voted in favour of the proposition. Four members voted against the proposition. Two members (Swati Dhingra and Alan Taylor) preferred to reduce Bank Rate by 0.5 percentage points, to 4%. Two members (Catherine L Mann and Huw Pill) preferred to leave Bank Rate unchanged, at 4.5%.

Operational considerations

27: On 7 May, the stock of UK government bonds held for monetary policy purposes was £620 billion. The MPC had been briefed on the amended operational arrangements for gilt sales in 2025 Q2, ahead of their publication in a Market Notice on 10 April.

28: The following members of the Committee were present:

- Andrew Bailey, Chair

- Sarah Breeden

- Swati Dhingra

- Megan Greene

- Clare Lombardelli

- Catherine L Mann

- Huw Pill

- Dave Ramsden

- Alan Taylor

Sam Beckett was present as the Treasury representative.

David Roberts was also present on 29 April and 2 May, as an observer for the purpose of exercising oversight functions in his role as a member of the Bank’s Court of Directors.

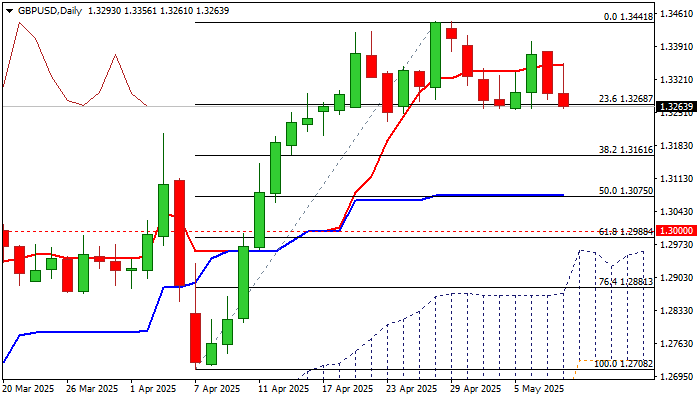

GBP/USD: Key Support Zone Remains Under Pressure Ahead of US-UK Trade Deal Announcement

Cable holds in red on Thursday and pressuring key support zone after overnight’s 0.5% jump on news of possible US/UK trade deal, was quickly reversed.

The US President Trump is expected to announce the details of initial trade deal with Great Britain later today that would mark a foundation for further negotiations.

Meanwhile, The Bank of England’s MPC will hold their policy meeting today and widely expected to cut interest rates by 0.25%.

Overall situation looks a bit brighter, as uncertainty over US tariffs started to fade, energy prices were lower, and inflation outlook looks more optimistic that would provide more space for maneuver for the central bank.

Technical picture on daily chart is expected to remain predominantly bullish while the price action holds above 1.3250 zone (floor of recent range / Fibo 23.6% retracement of 1.2708/1.3444 upleg) where several attacks were recently rejected.

However, warning signals from falling 14-d momentum which is attempting to break into negative territory, may contribute to renewed probes through key supports, with firm break of 1.3270/34 pivots to open way for deeper correction and expose immediate targets at 1.3200 (psychological) and 1.3161 (Fibo 38.2% / 30DMA).

Conversely, ability to hold above recent range floor would signal further sideways mode, though with bearish bias as long as the price stays in the lower part of the range and capped under daily Tenkan-sen (1.3351).

Res: 1.3295; 1.3351; 1.3402; 1.3444.

Sup: 1.3232; 1.3200; 1.3163; 1.3100.

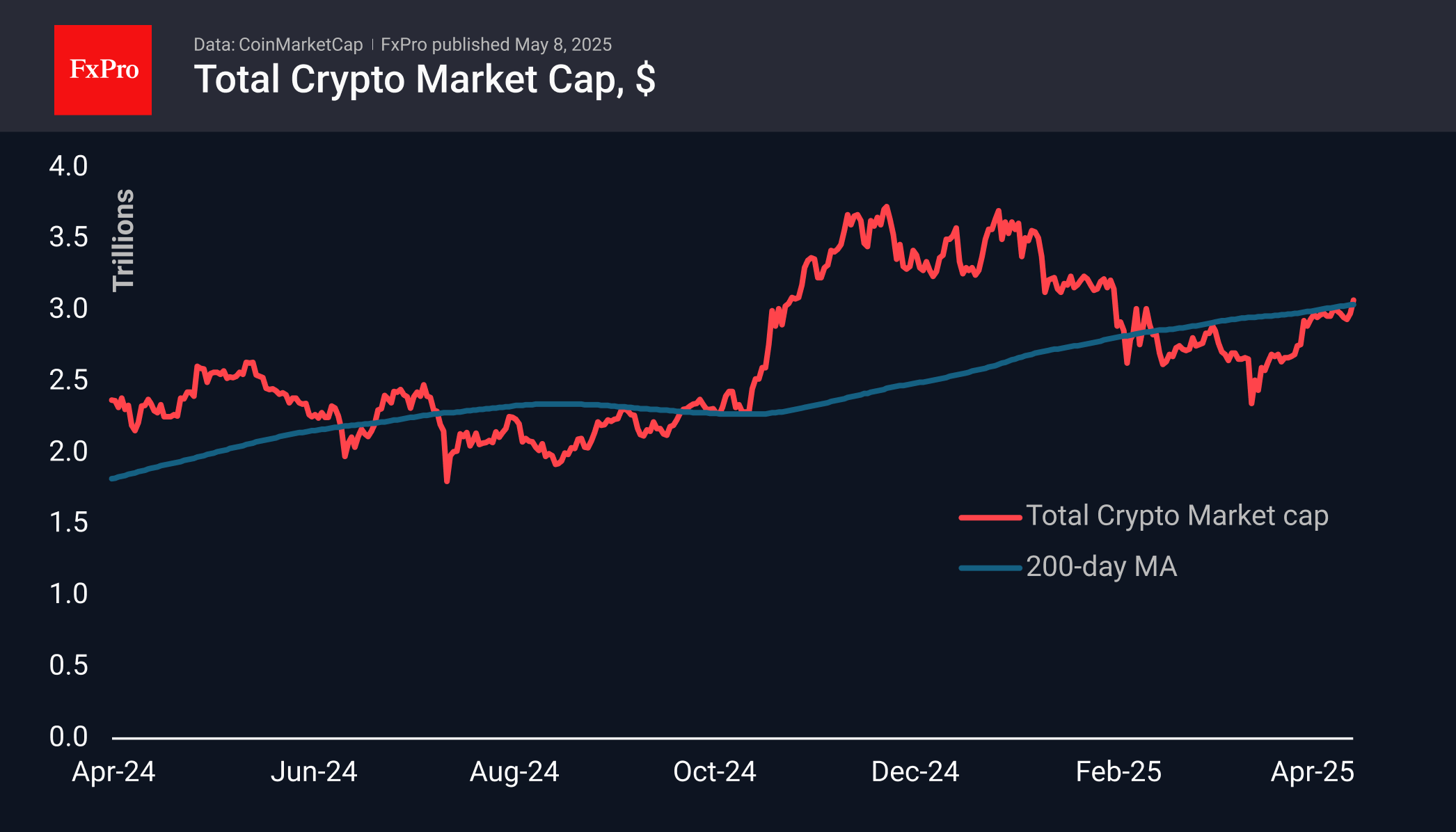

Crypto Market Has Moved to Growth After a Pause

Market picture

Crypto Market cap has increased by 2.8% in the last 24 hours to $3.07 trillion, reacting positively to the US-China trade talks scheduled for the weekend. The recent move above this round level was preceded by a two-week consolidation just below it. Technically, the market is also showing appreciation with a rise above the 200-day moving average. The next upside target is the $3.20 trillion area, where the market stayed for most of February.

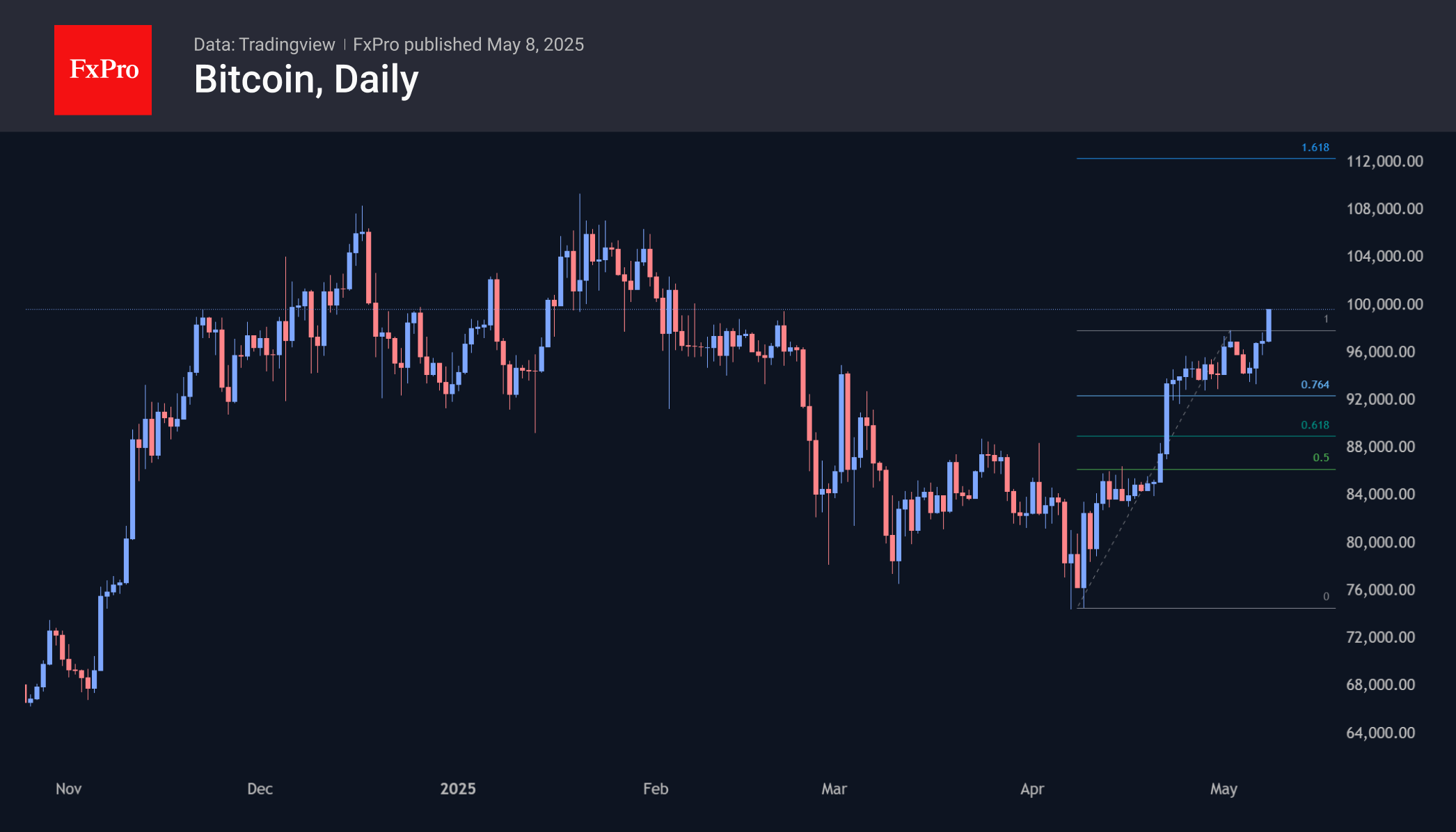

Bitcoin has reached the $99K mark, last seen in early February. Technically, a Fibonacci extension has begun with a potential upside of 161.8% from the rally from 9 April to 2 May to above $112K. Reaching the April lows fits into a broader scenario of a correction from the global rally from last September to January this year, with a target in the $162K area and upside potential of over 60%.

News background

The current dynamics of BTC net realised gains do not indicate the formation of a macro top but signal the entry into the ‘zone of caution’, CryptoQuant reports. Investors continue to take profits after quotes recover, which is consistent with late-stage bull market behaviour.

New Hampshire has become the first US state to pass a bitcoin reserve law. The governor signed the law after approval from the state House and Senate. The document allows the Treasury to use up to 5% of the funds to invest in BTC and precious metals.

On 7 May, the Ethereum network activated a major upgrade to Pectra, including 11 key enhancements to improve usability and efficiency.

Standard Chartered forecasts the value of the Binance-linked token BNB to rise to $2775 by 2028, which implies a more than 4-fold increase in value.

BTC/USD Analysis: Price Edges Close to the $100k Mark

Yesterday, the price of Bitcoin climbed above $99,000 – a level not seen since late February this year.

However, the bullish momentum proved insufficient to breach the psychological $100,000 barrier, and this morning the leading cryptocurrency is holding above $98,000. Since the start of the month, the BTC price has risen by nearly 5%.

Why is Bitcoin rising?

Two main drivers may have contributed to yesterday’s price surge:

→ Expectations of a forthcoming trade agreement between the US and (reportedly) the UK, already announced by Donald Trump. Well-known cryptocurrency analyst Anthony Pompliano stated that the upcoming deal “means the odds of reaching new all-time highs in 2025 are increasing.”

→ The Federal Reserve’s decision to maintain interest rates at their current level for another month, despite growing pressure from US President Donald Trump, who just weeks ago threatened to dismiss Fed Chair Jerome Powell for “cutting rates too late.” Market participants may have interpreted this as a bullish signal for cryptocurrencies.

BTC/USD Technical Analysis

In our previous analysis (2 May), we:

→ extended the long-term upward channel (highlighted in blue);

→ suggested that the uptrend in the Bitcoin chart had resumed following a correction along line R – a view supported by the current bullish trajectory (indicated with purple lines).

Price behaviour around the $95,000 level is particularly noteworthy. This level previously acted as both support and resistance (as shown with arrows), and in late April and early May, the Bitcoin price appeared to stabilise near it (marked), which may be interpreted as a temporary equilibrium between supply and demand.

Yesterday’s rise may indicate that the balance has shifted in favour of the buyers. How resilient the current positive sentiment proves to be could be revealed by how BTC/USD behaves in the face of a potential attempt to breach the psychological $100,000 level.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service. Open your trading account now or learn more about crypto CFD trading with FXOpen.

*Important: At FXOpen UK, Cryptocurrency trading via CFDs is only available to our Professional clients. They are not available for trading by Retail clients. To find out more information about how this may affect you, please get in touch with our team.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Dollar Strengthens Following Fed Verdict

The USD/JPY and USD/CAD currency pairs are showing moderate gains following yesterday’s meeting of the US Federal Reserve. As expected, the American central bank kept its key interest rate unchanged. However, the tone of the accompanying statement and Jerome Powell’s comments were perceived by the market as less dovish than anticipated. Fed officials reaffirmed their willingness to maintain current rates for a longer period until there is clear evidence of easing inflationary pressure. The Fed Chair also noted that recent macroeconomic data does not provide sufficient grounds to begin a rate-cutting cycle in the coming months. These signals supported the US dollar and contributed to corrective moves in major currency pairs.

The USD/JPY pair has strengthened towards the 144.00 mark, reflecting the dollar’s overall resilience amid rising US bond yields. However, market participants remain cautious due to the potential for intervention by Japanese monetary authorities should the yen weaken further. The USD/CAD pair is trading above 1.38, still influenced by moderately weak oil prices and steady demand for the dollar.

Today, investor focus turns to the Bank of England’s meeting, where no change in the base rate is expected. However, the key market driver will likely be the tone of the regulator’s accompanying statement. Additional volatility may be triggered by Friday’s Canadian employment data release, which could significantly impact the Canadian dollar’s performance.

USD/JPY

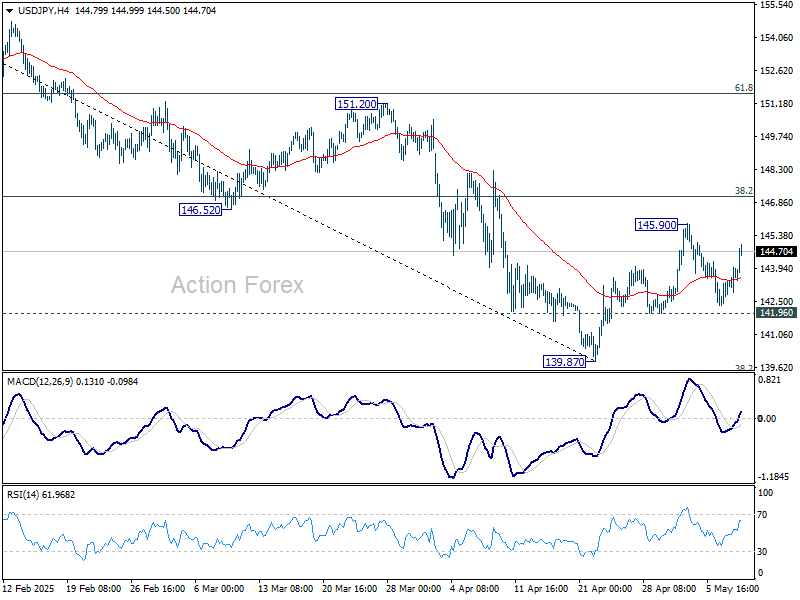

Yesterday’s Fed meeting allowed USD/JPY buyers to find support just above 142.00 and push the pair more than 100 pips higher. Technical analysis suggests a potential continuation of the upward move towards the 146.00–145.30 area, as several bullish candlestick patterns have formed on the daily timeframe — including a "piercing line" on 22 April and a "bullish engulfing" pattern on 7 May.

The following news events could influence USD/JPY price action:

- Today at 15:30 (GMT+3): US Initial Jobless Claims

- Today at 15:30 (GMT+3): US Unit Labour Costs

- Today at 20:00 (GMT+3): Atlanta Fed’s GDPNow estimate

USD/CAD

Unlike USD/JPY, the USD/CAD pair has not shown a confident upward trend. Buyers managed to hold the pair above 1.3800, but daily volatility remains extremely low. Should the 1.3820–1.3800 zone become established as support, a move towards 1.3900 could follow. Conversely, a break below the multi-day support at 1.3750 may trigger a resumption of the medium-term downtrend.

The following events could affect USD/CAD pricing:

- Today at 17:00 (GMT+3): Bank of Canada Financial System Review

- Tomorrow at 15:30 (GMT+3): Canada Employment Change

- Tomorrow at 15:30 (GMT+3): Canada Unemployment Rate

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

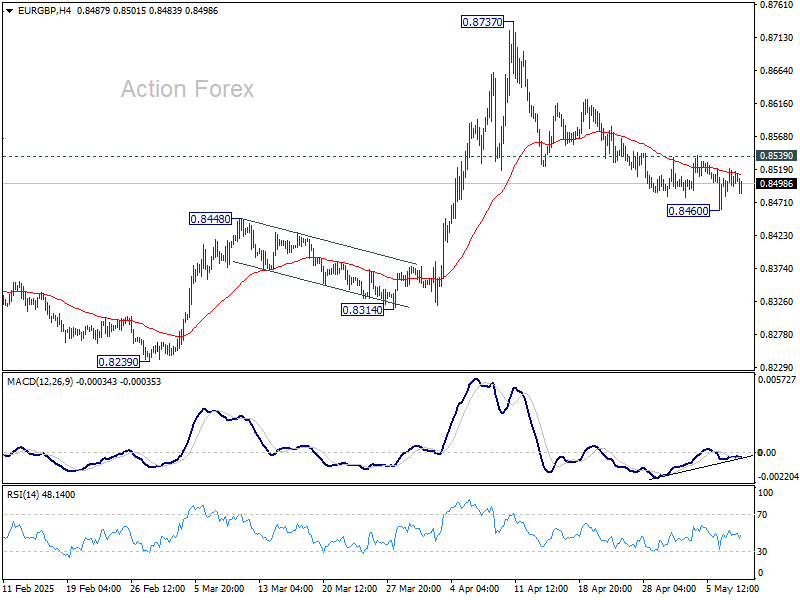

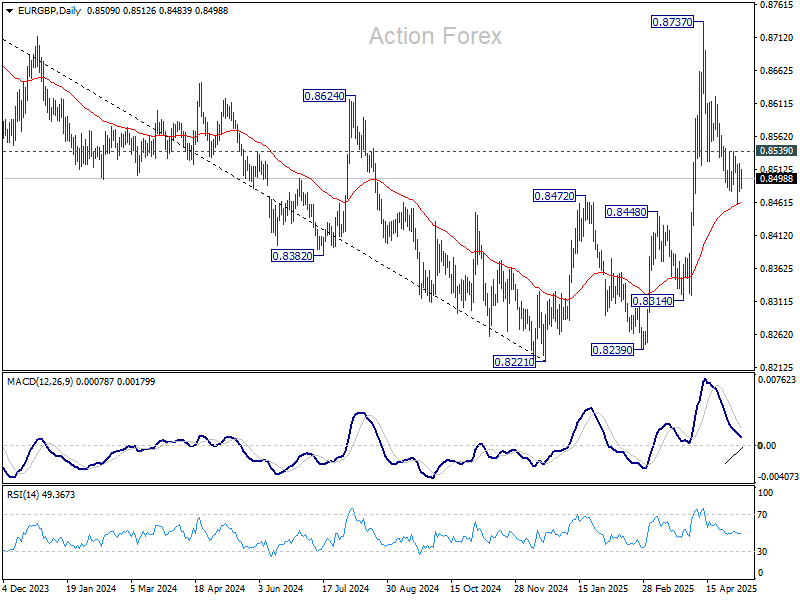

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8482; (P) 0.8502; (R1) 0.8523; More...

Intraday bias in EUR/GBP is turned neutral again with current recovery. Break of 0.8539 resistance will indicate that fall from 0.8737 has completed as a correction, after defending 55 D EMA (now at 0.8462). Intraday bias will be turned back to the upside for retest 0.8737 resistance. However, sustained trading below 55 D EMA will suggest that whole rise from 0.8221 has already complete and turn outlook bearish.

In the bigger picture, down trend from 0.9267 (2022 high) should have completed at 0.8221, just ahead of 0.9201 key support (2024 low). Rise from 0.8221 is likely reversing the whole fall. Further rise should be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867 next. This will remain the favored case as long as 0.8472 resistance turned support holds. However, firm break of 0.8472 will argue that the down trend hasn't completed yet.

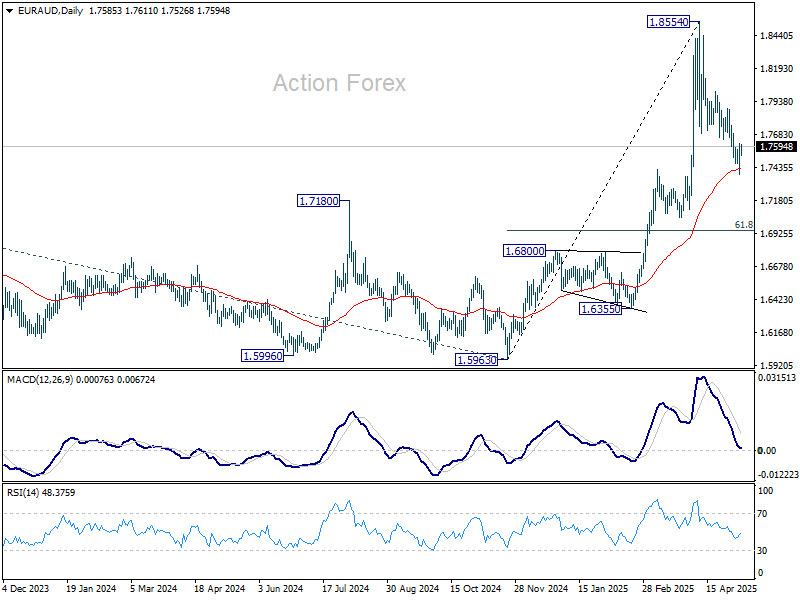

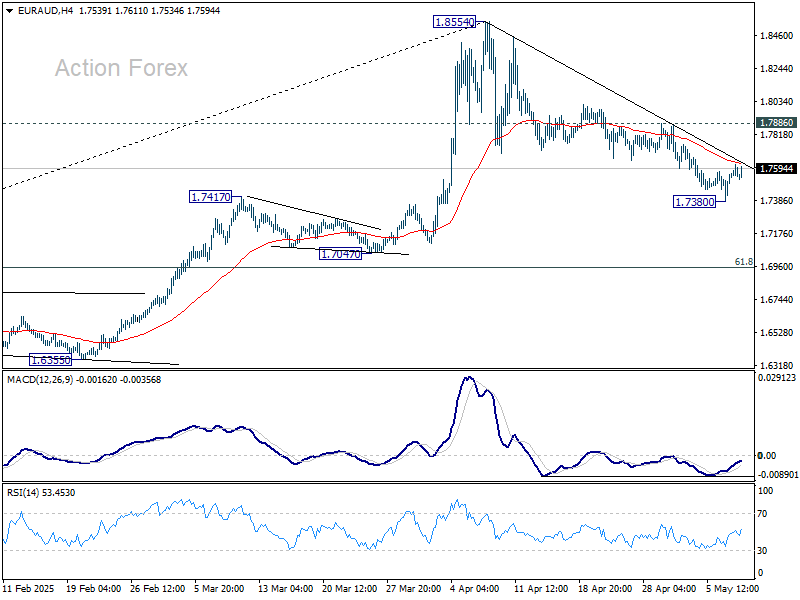

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7442; (P) 1.7533; (R1) 1.7679; More...

Intraday bias in EUR/AUD is turned neutral first with current recovery. On the upside, firm break of 1.7886 resistance will argue that fall from 1.8553 has completed as a correction at 1.7380. Intraday bias will be turned back to the upside for retesting 1.8554. However, sustained trading below 55 D EMA (now at 1.7428) will target 61.8% retracement at 1.6953.

In the bigger picture, up trend from 1.4281 (2022 low) is in progress for 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. Firm break there will pave the way to 138.2% projection at 1.9806, which is close to 1.9799 (2020 high). Outlook will remain bullish as long as 1.7062 resistance turned support (2023 high) holds even in case of deep pullback.