Sample Category Title

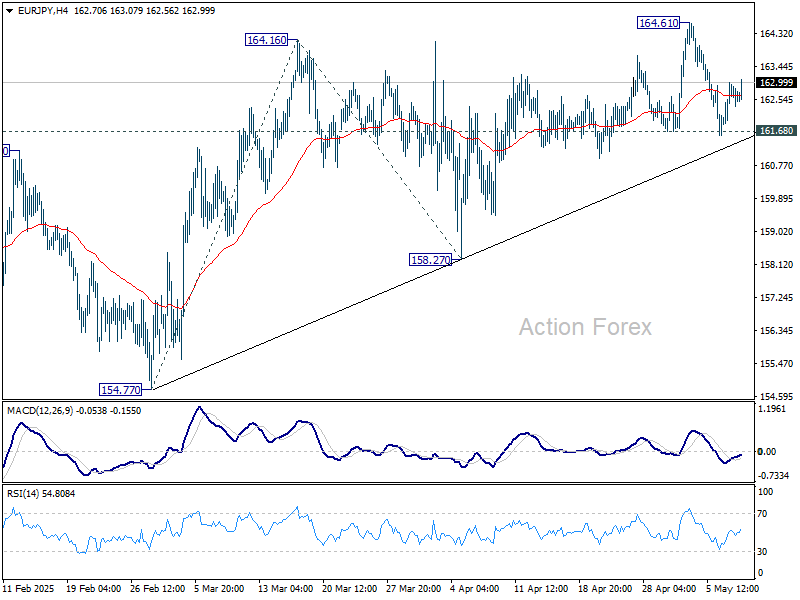

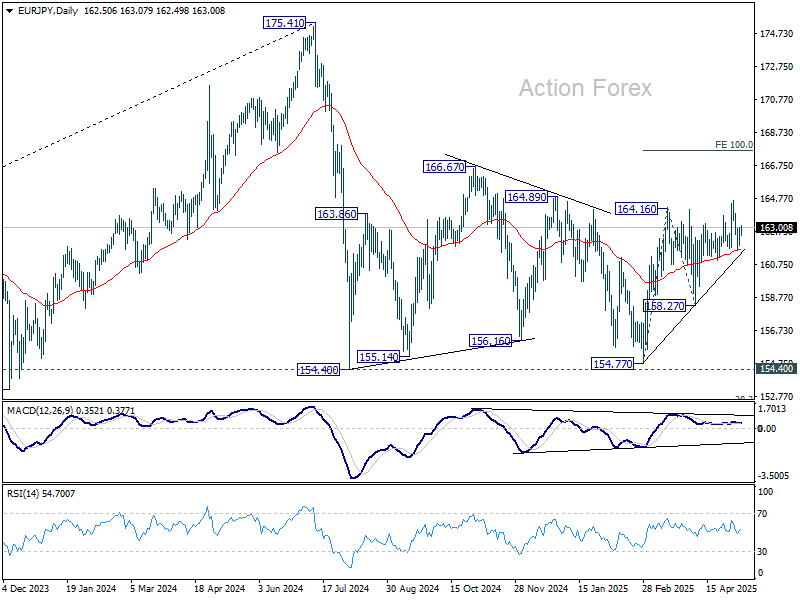

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.01; (P) 162.52; (R1) 163.13; More...

Intraday bias in EUR/JPY stays neutral at this point, and further rise remains mildly in favor. On the upside, above 164.61 will resume the rise from 154.77 to 100% projection of 154.77 to 164.16 from 158.27 at 167.66. However, sustained break of 161.68 will turn bias back to the downside for 158.27 instead.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

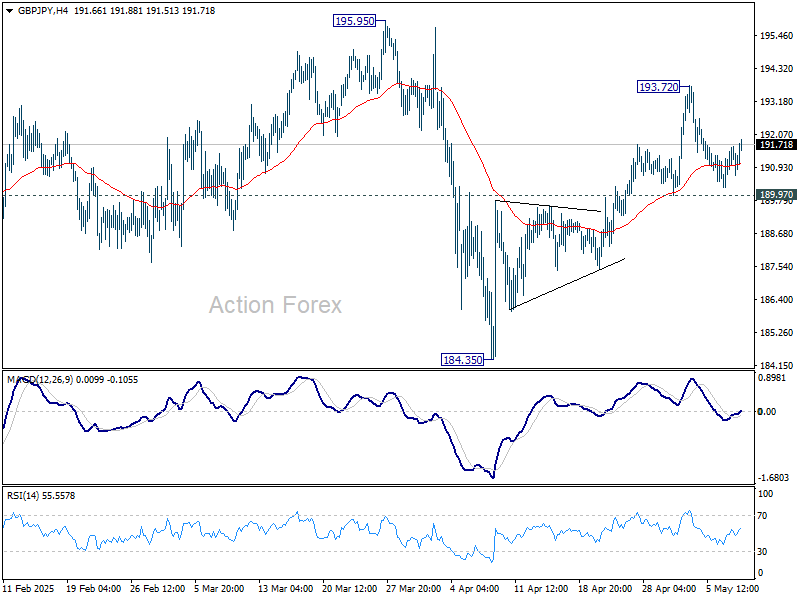

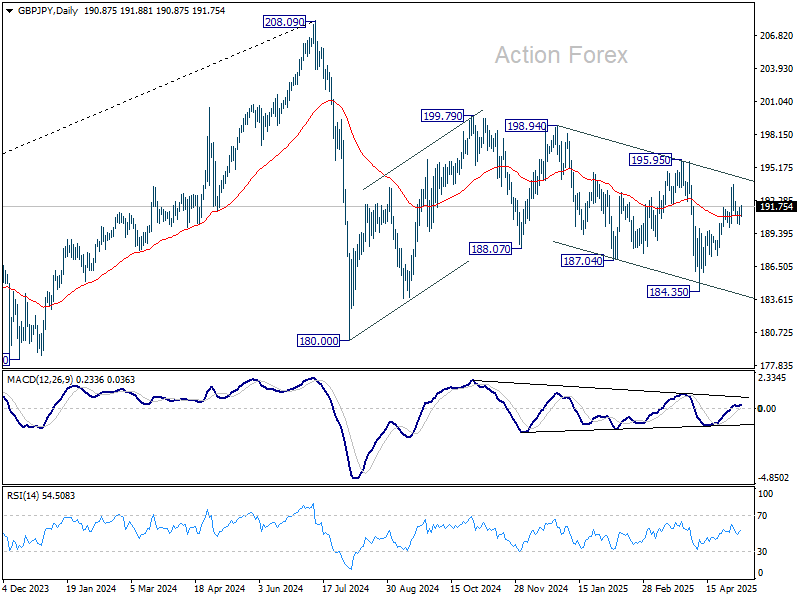

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.50; (P) 191.09; (R1) 191.74; More...

Intraday bias in GBP/JPY remains neutral at this point. With 189.97 support intact, further rise is favor. Above 193.72 will resume the rally from 184.35 and target 195.95 resistance next. However, firm break of 189.97 will turn bias back to the downside for deeper decline.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

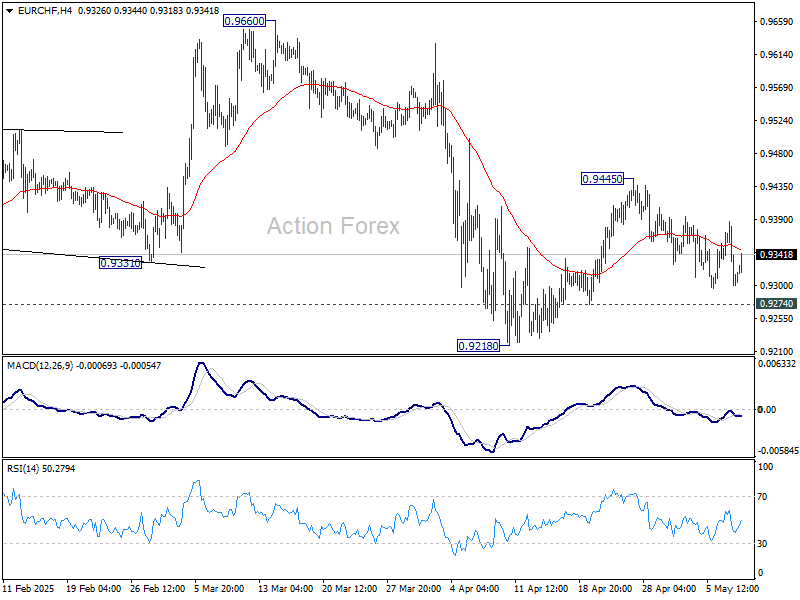

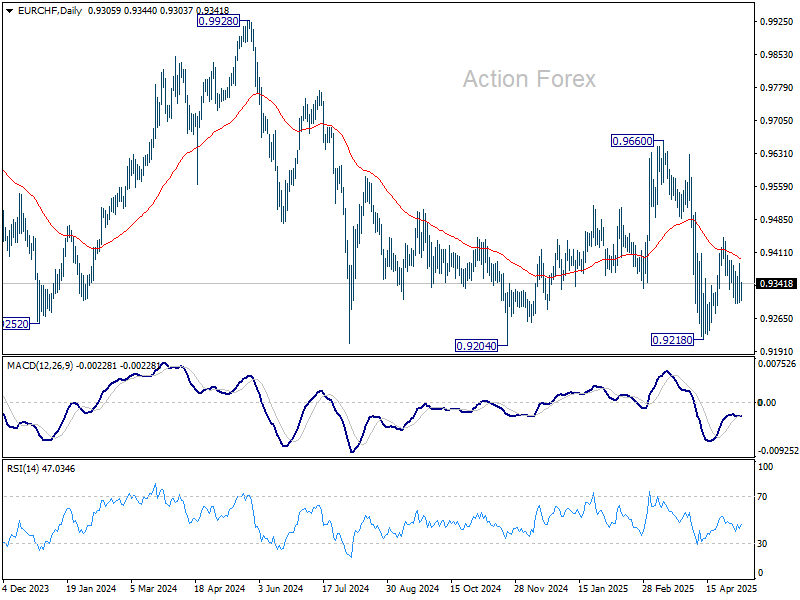

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9278; (P) 0.9333; (R1) 0.9365; More....

Intraday bias in EUR/CHF remains neutral for the moment. On the upside, above 0.9445 will resume the rebound from 0.9218, either as a corrective move or the third leg of the pattern from 0.9204. However, break of 0.9274 will suggest that that recovery has completed, and bring retest of 0.9204/18 support zone.

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9555) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.

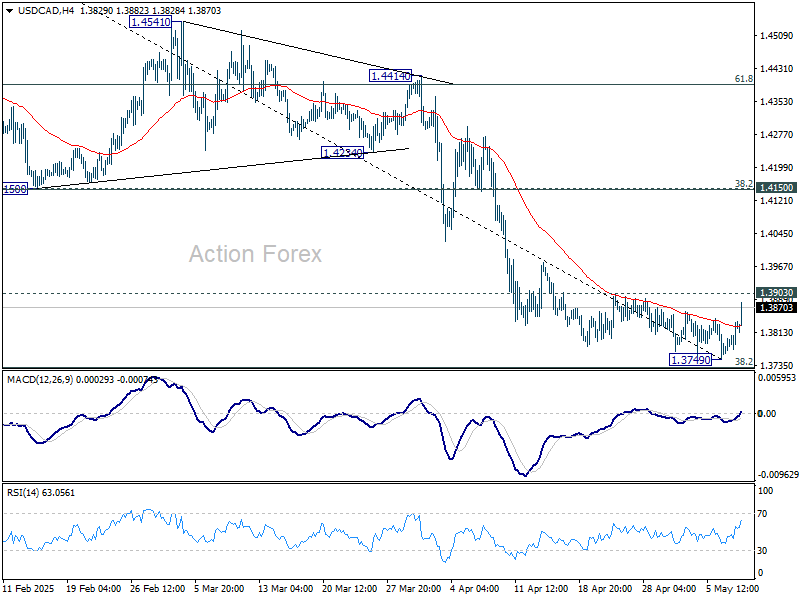

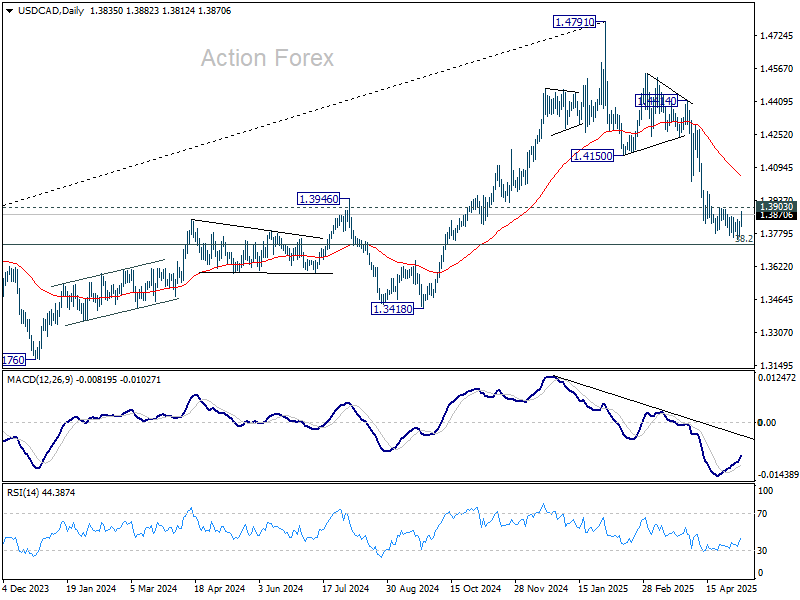

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3789; (P) 1.3814; (R1) 1.3864; More...

Intraday bias in USD/CAD is neutral for the moment. Considering bullish convergence condition in 4H MACD, firm break of 1.3903 resistance should confirm short term bottoming at 1.3749, ahead of 1.3727 fibonacci level. Intraday bias will be back on the upside for 1.4150 cluster resistance (38.2% retracement of 1.4791 to 1.3749 at 1.4147).

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4150 resistance turned support holds. Firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.

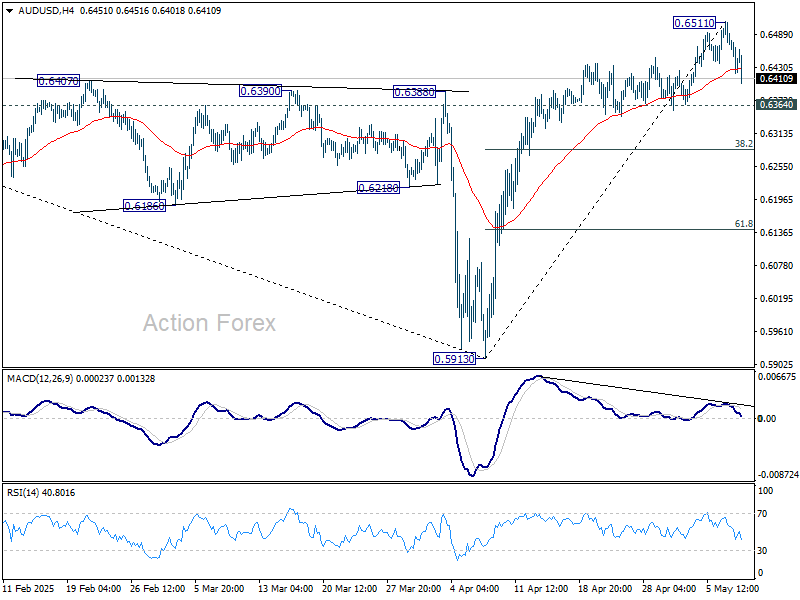

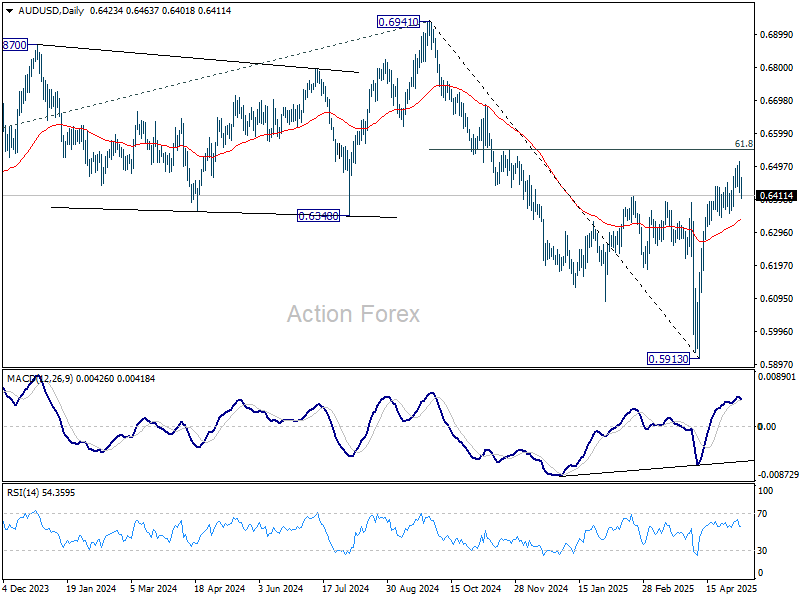

AUD/USD Daily Report

Daily Pivots: (S1) 0.6392; (P) 0.6454; (R1) 0.6486; More...

Intraday bias in AUD/USD is turned neutral with current retreat. On the upside, above 0.6511 will resume the rise from 0.5913 to 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, considering bearish divergence condition in 4H MACD, break of 0.6364 support should confirm short term topping. Intraday bias will be turned back to the downside for 38.2% retracement of 0.5913 to 0.6511 at 0.6283.

In the bigger picture, as long as 55 W EMA (now at 0.6443) holds, the down trend from 0.8006 (2021 high) should resume later to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.

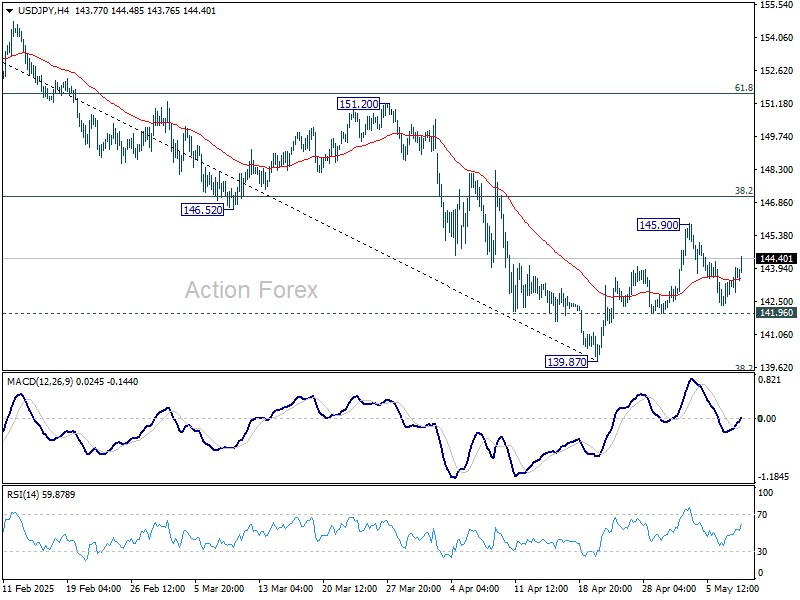

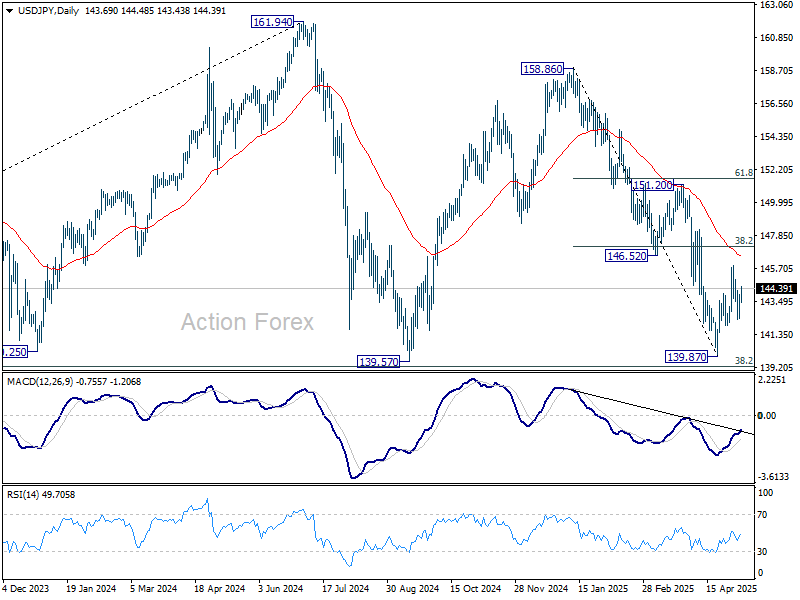

USD/JPY Daily Outlook

Daily Pivots: (S1) 142.81; (P) 143.40; (R1) 144.43; More...

Intraday bias in USD/JPY remains neutral for the moment. Rebound from 139.87 could extend through 145.90. But near term outlook will stay bearish as long as 38.2% retracement of 158.86 to 139.87 at 147.12 holds, in case of another bounce. On the downside, firm break of 141.96 will argue that rebound from 139.87 has completed as a corrective move. Retest of 139.87 should then be seen next in this case.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

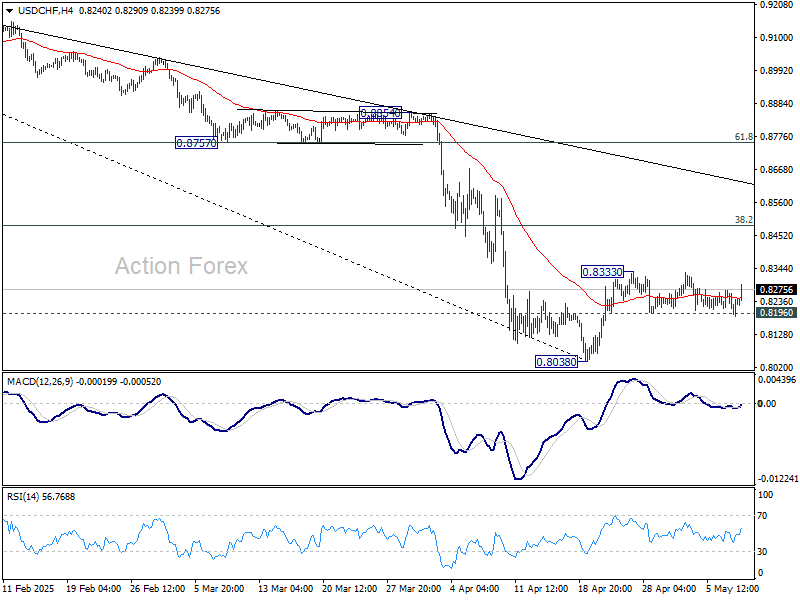

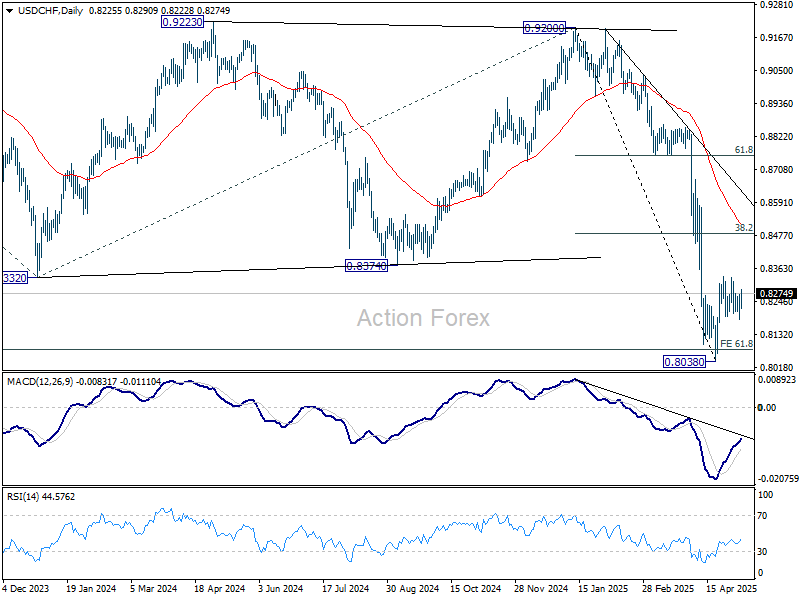

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8192; (P) 0.8232; (R1) 0.8278; More….

USD/CHF breached 0.8196 support but quickly recovered. Intraday bias remains neutral first. On the upside, above 0.8333 will resume the rebound from 0.8038. However, upside should be limited by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. On the downside, firm break of 0.8196 will bring retest of 0.8038. Firm break there will resume larger down trend.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8763) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

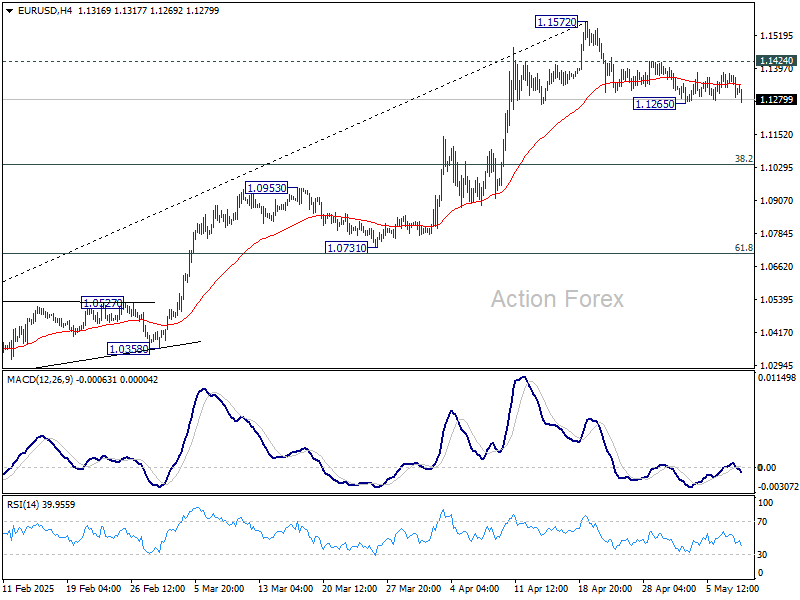

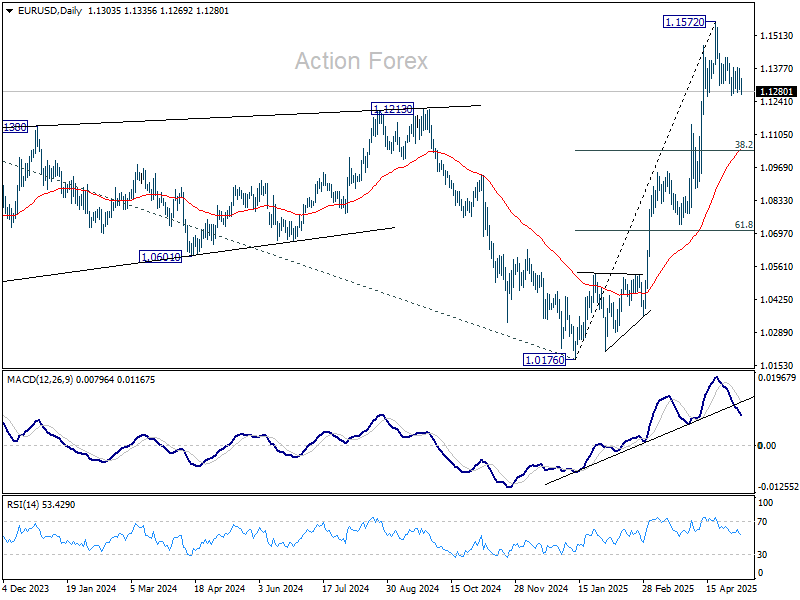

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1270; (P) 1.1324; (R1) 1.1356; More...

Intraday bias in EUR/USD remains neutral for the moment, as range trading continues. On the downside, below 1.1265 will resume the corrective fall from 1.1572 short term top. But downside should be contained by 38.2% retracement of 1.0176 to 1.1572 at 1.1039. On the upside, break of 1.1424 will suggest that the correction has completed and bring retest of 1.1572 high.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0808) holds.

Focus Turns to UK Today, Not Only Because of BoE Meeting

Markets

“We think we’re in the right place to wait and see how things evolve” wraps up yesterday’s press conference by Fed Chair Powell. Comments were very similar to the ones made on April 16 before the Economic Club of Chicago. The official statement pointed out that compared to March, uncertainty about the economic outlook has increased further and that risks of both higher unemployment and higher inflation have risen. If the dual-mandate goals are in tension, the US central bank will consider how far the economy is from each goal, and the potentially different time horizons over which those respective gaps would be anticipated to close. With inflation above target and the unemployment rate currently in line with the NAIRU-estimate from the March Summary of Economic Projections, this suggests a clear focus on inflation still. US economic activity has continued to expand at a solid place, although swings in net exports have affected the data. We stick with our call of a prolonged Fed pause, stretching at least over Summer. US money markets currently discount a 20% probability to a June cut and a 80% probability to action in July. Once risks to the labour market materialize, we think the Fed will immediately opt bigger (50 bps) rate cuts, using the policy room towards neutral levels. It’s hard to pinpoint that exact moment, if it even were to occur. As Powell said: “it’s not a situation where we can be pre-emptive because we actually don’t know what the right response to the data will be until we see more data.” Yesterday’s status quo didn’t really surprise. US Treasury yields yesterday lost 0.6 bps (2-yr) to 3.8 bps (7-yr) with the belly of the curve outperforming the wings. The dollar gained against the euro (EUR/USD 1.1301 close) but that move coincided more with news that the Trump administration plans to rescind Biden-era AI chip curbs as part of a broader effort to revise semiconduction trade restrictions. The latter helped a positive close for the likes of Nasdaq (+0.27%) and S&P 500 (+0.43%) as well, overturning earlier losses.

Focus turns to the UK today. Not only because of the scheduled BoE policy meeting, but also as US President Trump is expected to announce a framework of a trade deal with the UK. It’s the first such announcement which should start negotiations on tariff rates, non-tariff barriers, digital trade,… in coming months. Sterling welcomed the news with EUR/GBP dipping below the 0.85-handle this morning. The UK central bank is expect to deliver a 25 bps rate cut. A new Monetary Policy Report will balance growth and inflation risks and might put the BoE on a more activist future path compared to the quarterly cutting pace in place since August of last year.

News & Views

The Czech central bank (CNB) lowered policy rates by 25 bps yesterday to 3.5%. The cut was priced in, especially following a bigger-than-expected drop in April inflation to 1.8%, the slowest pace since 2018. The CNB noted, however, that services inflation remains elevated amid above-average wage growth and warned for significantly rising property prices. It beefed up its inflation forecast in the spring update for 2025 to 2.5% and for 2026 to 2.2% compared to the winter edition. The balance of risks is still modestly inflationary overall, with the CNB mentioning risks of inertia in services and food inflation, higher public spending, increased wage demands and an acceleration in (property) lending activity. Governor Michl in the presser later added that these inflation risks limit the room for further easing but also said that there was no agreement whether yesterday’s “very cautious” cut was the last one in the current cycle. The GDP forecast for this year remained unchanged at 2% while the one for next year was downgraded to 2.1%. The impact of the trade conflict on both inflation and growth could not “reliably assed at the moment”. Czech swap yields finished between 3.3-7.7 bps lower. The Czech koruna ended the day higher though (EUR/CZK 24.91).

“Taking into account incoming information, including lower current and forecasted inflation, decreasing wage growth and weaker data on economic activity, in the Council’s assessment, the adjustment of the level of the NBP interest rates became justified.” And with that, the National Bank of Poland (NBP) yesterday slashed interest rates for the first time since late 2023 by 50 bps to 5.25%. While making it sound like a no-brainer now, the decision does mean a sharp U-turn by the central bank, not least by its governor who up until a month ago suggested no rate cuts until 2026. Glapinski changed his tone dramatically following the April policy meeting, which took place after Trump’s Liberation Day announcement. It meant yesterday’s cut was also widely expected, resulting stoic PLN trading around EUR/PLN 4.265 afterwards. The NBP statement offered no guidance on future moves but Glapinski might during the presser later today.

Fed Who? Trade Hopes Fuel Risk Appetite

This week’s Federal Reserve (Fed) meeting went according to plan. It was hawkish—though just about as hawkish as expected. The Fed kept interest rates unchanged, as widely anticipated, and signalled it's in no rush to cut them before gathering more data to assess the real impact of the tariff policy. It believes tariffs could lead to higher inflation and higher unemployment. And even though the spike in inflation is expected to be temporary, there’s a chance it could linger.

The thing is, the Fed thinks that US unemployment remains low and demand steady enough to allow the Fed to sit on its hands until there's more clarity. Some members even stated they would not support pre-emptive rate cuts to shield against a slowing economy. ‘It’s not a situation where we can be pre-emptive, said Chair Powell. ‘Because we actually don’t know what the right response to the data will be until we see more data.’ Fair enough. He’s not Superman—he doesn’t have a crystal ball and can’t predict how the tariff situation will evolve, how other countries will react, or how it will all play out economically for the US.

So, yesterday’s FOMC decision and press conference made sense. The US 2-year yield rebounded after the decision, the probability of a June cut eased to 20%, and US equities came under pressure.

But the headlines shifted quickly: news that the Trump administration would scrap the AI chip curbs engineered by Biden gave a late boost to major indices in the final half-hour of trading. Nvidia—flat for most of the session—rallied over 3% in the last 30 minutes.

Yet—wait, yet—those AI curbs will not be scrapped. They’ll be replaced by “simpler” rules, said the Commerce Department’s Bureau of Industry and Security. As a result, Nvidia shares were flat to slightly negative in after-hours trading as investors digested the news.

Elsewhere, AMD—Nvidia’s biggest rival—jumped 1.76% after posting strong quarterly earnings and offering a bullish forecast for the current quarter, driven by demand for high-end personal computers capable of running AI software. I still believe AMD is in an interesting position to grow as investors warm up to the idea that cheaper chips can perform relatively well and may be chosen over Nvidia’s premium products. However, the fact that the Middle East could see AI chip restrictions eased is excellent news for Nvidia, as countries in the region have deep pockets and will likely opt for top-tier chips—Nvidia’s.

In other Big Tech news, Apple announced—during its testimony in the US Justice Department’s lawsuit against Alphabet—that it plans to revamp its Safari web browser to highlight AI-powered search engines. This move could mark the end of a $20-billion-a-year (yes, $20 billion per year) deal with Google to be the default search engine on Apple devices. AI search engines will now be part of a list, not the default.

Reaction? A hefty 7.5% slump in Google’s share price, amid rising concerns that AI-powered engines will increase competition and chip away at Google’s decades-long monopoly in online search. That said, Google remains a significant AI player—it has access to vast amounts of data that competitors lack, and it will do everything it can to preserve its dominance. But the arrival of ChatGPT clearly ended Google's uncontested reign in the sector, meaning the company now needs to work harder: invest, innovate, and reinvent. That sounds like the end of easy money.

Zooming out, equities in China and Japan are trading firmer this morning, while US and European futures are in the green ahead of an expected trade deal announcement with a ‘big’ country—reportedly the UK. While the UK isn’t a major exporter to the US, progress there could set the stage for more meaningful deals with heavyweight partners like India, China, Japan, or the EU. Consider it a promising appetizer before the main course.

We’ll get more details later today, but for now, trade optimism is outweighing yesterday’s Fed hawkishness and may help set the tone for the rest of the week—especially with the US and China preparing to meet in Geneva to discuss their unsustainable tariff situation. Reports suggest that Temu and Shein saw double-digit sales declines in the week following price hikes aimed at passing Trump’s tariffs on to US consumers. Positive developments on that front could give markets another boost. That said, anything short of a 50% cut in current tariffs probably won’t move the needle much.