Sample Category Title

Habemus a Trade Deal

Not only do we have a new pope this week, but we also have the first deal in Trump’s global trade war - between the UK and the US. Trump’s enthusiastic announcement, complete with a lot of CAPITAL LETTERS, helped inflate sentiment, making this US-UK deal feel bigger than it actually is.

I mean, the fact that the two countries could agree on a few points is a good start, but the UK entered the negotiations with a tariff rate of 10% and left the table with... a tariff rate of 10%. Sure, the tariffs on cars were pulled lower from 27.5% to 10% — leading to an almost 14% jump in Aston Martin. Rolls Royce’s plane engines are exempt from tariffs in exchange for a pledge from British Airways to buy $10bn worth of Boeing planes — Rolls Royce jumped by more than 3.5%. The tariff on UK steel will be cut to zero, while British farmers will benefit from tariff-free quotas — just like their US counterparts. The two countries also agreed to keep working on a digital agreement.

But again, the 10% tariffs remain. So yes, it’s a deal — but is it a big deal? One person at Axios even said that the UK was the "low-hanging fruit of trade deals" and that negotiations won’t be as simple with others. We’ll see. Futures this morning are slightly in the green.

The news of the US-UK deal resonated positively across global financial markets. Major US indices extended gains despite a selloff in US Treasuries that pushed the 10-year yield back to the 4.40% level. Maybe part of the optimism was also fuelled by FOMO after Trump posted “go out and buy stocks now!”

But enthusiasm was dented by questions over the greatness of the deal and the challenges ahead — so sentiment remains fragile.

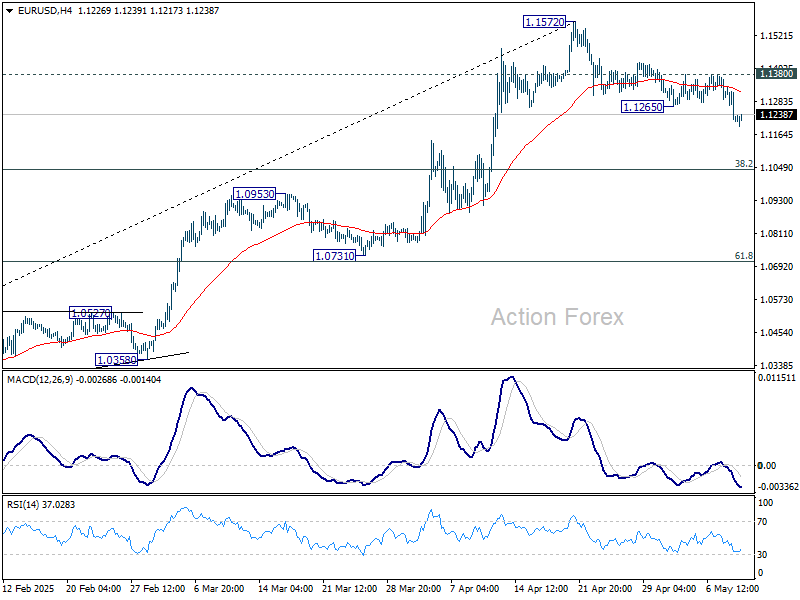

The dollar index rebounded strongly to an almost one-month high. The EURUSD tumbled to the 1.12 level — the minor 23.6% Fibonacci retracement on the year-to-date rally — and is consolidating near that level this morning. Meanwhile, Cable is preparing to test the 1.32 level and the USDCHF rallied past the month-high levels. The FX moves are a suggestion of how markets could react to further progress in tariff talks.

Note, however, that despite strong gains in some sectors, the FTSE 100 closed yesterday’s session in the red. That was partly due to a hawkish cut from the Bank of England (BoE) — where two members didn’t want to cut rates at all due to inflation uncertainty. It was also partly AstraZeneca’s fault — the stock alone shed 270 points from the index — and partly due to losses in miners, as copper prices extended losses for a third straight session on concerns over slowing demand from China. Gold also came under pressure from hopes of easing global trade tensions.

Bitcoin, on the other hand — another proxy for Trump trade — rallied more than 6% to surpass the $100K mark. We’re near $102K as of this morning.

In summary, yesterday’s price action suggests that investors are eager for good news and react positively — even if the news isn’t that great. It’s all in how it’s delivered — and apparently, that’s all that matters.

Now, all eyes are on the first in-person meeting between US and Chinese high-level officials in Geneva tomorrow to discuss tariffs. The goal isn’t to seal a trade deal — that will probably take months, if not years — but to de-escalate tensions between the two countries. And who knows — maybe they’ll agree to pause tariffs while discussions continue. Impossible to tell. In the best-case scenario, talks go well, both countries commit to finding a reasonable deal, markets rally on Monday, the US dollar continues rebounding, and gold and the franc retreat further. Or… the talks break down, Trump says something he shouldn’t, and we wake up to another hectic week — with a global selloff in equities and the dollar, and a rebound in gold and franc. I’d say it’s a 60-40 chance for good versus bad vibes.

In energy, the week ends on a better note than it started. US crude is back at the $60pb level after an early-week plunge to $55 on news that OPEC would accelerate plans to restore output — for reasons that remain unclear.

But whatever the reasons, the medium-term outlook remains comfortably bearish given higher supply and lower demand expectations. Price rallies remain interesting top-selling opportunities, with a target at $50pb. Minor resistance is at $61.75 — the 23.6% Fibonacci retracement on the YTD decline — while stronger offers may appear near the 50-DMA (currently around $64.70pb) and the $65 level, which matches the April peak and major 38.2% retracement. That level should help distinguish between a continuation of the current bearish trend and a potential medium-term reversal.

On a side note, falling oil prices are supporting consolidation in the energy sector as companies look to benefit from synergies. In that context, this week’s news that Shell is exploring a deal to acquire BP — in what would be a historic merger in Europe — has echoed across the energy space. A combined Shell-BP would rival ExxonMobil in scale.

Alas, BP saw limited gains this week… one to keep an eye on.

US and China Set to Meet Over the Weekend to Resolve Current Deadlock

In focus over the weekend

The Norwegian inflation figures for April will be released today. Inflation surprised strongly on the upside in February and dragged the price level into March. In line with consensus, we expect that core inflation decreased from 3.4% to 3.2% in April, driven by somewhat lower growth in food prices and other Norwegian-produced goods than in April last year.

Over the weekend US and China will kick off trade talks in Switzerland after a long deadlock in the trade war. The main goal of the talks will be to agree on lowering tariffs from the current prohibitively high rates, which are a de facto trade embargo on most goods. We believe they will agree on getting tariffs down to around 60% soon, as the economic pain is growing on both sides.

Economic and market news

What happened overnight

In South Asia, India and Pakistan continue to spiral into further tensions as the conflict worsens. Two Indian fighter jets are reported to have been shot down, artillery bombing in the Indian Kashmir region and drone attacks along India's west boarder which Pakistan has denied.

In China, exports increased by 8.1% y/y in April, significantly more than consensus expectations of 1.9% y/y. Imports declined by just -0.2% y/y, defying consensus expectations of -5.9% y/y. The stronger-than-expected data could provide China with additional incentive to stand firm in the upcoming negotiations with the US in Switzerland over the weekend.

In Japan, real labour earnings for March declined 2.1% y/y, while household spending overshot expectations significantly at 2.1% y/y and 0.4% m/m (cons: 0.2% y/y, -0.5% m/m).

What happened yesterday

In the trade war, the UK and US announced a new trade deal. While the flat 10% universal tariff rate on the UK remains in place, the deal between the US and the UK includes a cut of tariffs on UK cars from 27.5% to 10% and a removal of tariffs on steel and aluminum. In return, the UK will offer improved access to US agricultural and industrial products and an agreement on planes. While the deal is a positive development in the trade war, many details are still to be laid out and the impact is limited.

In Germany, industrial production rose more than anticipated in March by 3.0% m/m (cons: 1.0% m/m). With the data for March, it is now more evident that the German industry has bottomed out as production has stopped declining, also seen in the PMIs for April. Data is volatile from month to month and some front loading to the US could also be at play. So, we have yet to see a clear rebound in the German industry, but at least it looks like we have hit the bottom, and we expect production to start rising this year as lower ECB interest rates feed into the sector.

In Norway, Norges Bank kept rates unchanged and avoided giving any new policy signals. The market reaction was non-existent amid very little news and low expectations. We still expect the first rate cut in September as the central bank signalled in March.

In Sweden, the Riksbank held the interest rate at 2.25% as expected. They did however suggest slight easing of monetary policy going forward. Although the tone was somewhat to the dovish side compared to recent communication, it is still quite a bit more restrictive compared to how the Riksbank communicated upcoming rate cuts last year.

In the UK, the BoE decided to cut the Bank Rate by 25bp to 4.25% yesterday. The vote split showed a surprisingly divided MPC with the statement tilting towards a hawkish bias. However, we do not see this as a broad shift in sentiment within the MPC. The statement revealed that BoE still favours a "gradual" and "careful" approach to easing monetary policy whilst highlighting elevated uncertainty. Price action in GBP was also largely driven by good news on the trade front.

Equities: Equities rallied broadly yesterday, with a distinct shift towards pro-cyclical and pro-Trump market dynamics. US equities outperformed their global peers, with cyclicals leading the charge. Small caps notably outperformed large caps, while the VIX declined. A slight note of caution could be noted as yields rose alongside oil prices. However, in the current environment, these moves should be viewed positively - as a reflection of growth optimism and rising investor confidence in the US economy. It is encouraging to witness both a stronger risk appetite and simultaneous increases in yields and oil prices. In the U.S. yesterday, the Dow was up 0.6%, the S&P 500 rose by 0.6%, the Nasdaq climbed 1.1%, and the Russell 2000 surged 1.9%. This morning, Asian equities are trading higher, led by Japan, and both European and US futures point marginally higher.

FI&FX: There was a sharp rise in global bond yields yesterday driven from the long end, where 10Y German govt yields rose some 6bp, while 10Y US Treasuries rose 5.5bp on the back of the announcement of trade deal between US and UK, where the details point to a very modest set of tariffs. Hence, this boosted the risk-on sentiment with higher yields, stronger equity markets and stronger USD.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1181; (P) 1.1259; (R1) 1.1305; More...

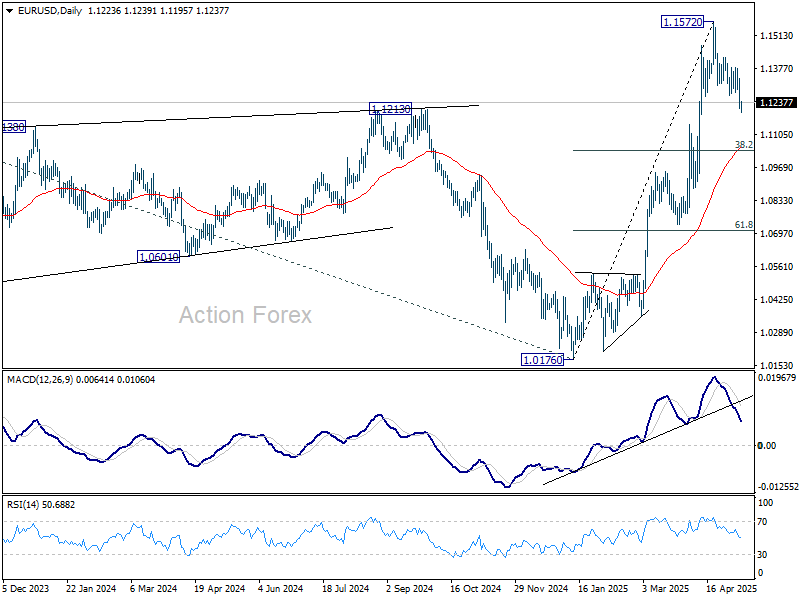

EUR/USD's corrective fall from 1.1572 resumed by breaking through 1.1265 and intraday bias is back on the downside. Deeper fall would be seen to 38.2% retracement of 1.0176 to 1.1572 at 1.1039. But strong support should be seen there to bring rebound. On the upside, break of 1.1380 will suggest that the correction has completed, and bring retest of 1.1572.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0808) holds.

Dollar Strengthens on Trade Deal, But Details Keep Risk Sentiment Tame

Market reaction to the much-anticipated US-UK trade agreement was cautiously positive, though not particularly enthusiastic. While major US equity indices closed higher overnight, DOW, S&P 500, and NASDAQ all gave back early gains to finish near their opening levels, suggesting that the initial optimism faded as details of the deal emerged. The muted tone suggests that while the deal provided a headline boost, its content lacked the depth to drive a more sustained risk rally.

The trade agreement itself, though billed as comprehensive, turned out to be more of a framework than a finalized deal. No formal documents were signed during the Oval Office event, and US President Donald Trump admitted that “final details are being written up,” promising a conclusive announcement in the coming weeks. Crucially, the 10% blanket tariff on UK imports will remain in place, setting a potential precedent that future US trade agreements—whether with the EU, ASEAN, or Canada—may not revert to pre-tariff norms. This signals a structural shift in global trade architecture where tariffs are normalized, not reversed.

Despite the lack of concrete outcomes, Sterling has remained resilient and is currently the second strongest major currency so far this week, trailing only Dollar. Japanese Yen holds third place, while Kiwi, Loonie, and Euro sit at the bottom of the performance chart. Aussie and Swiss Franc are trading near the middle.

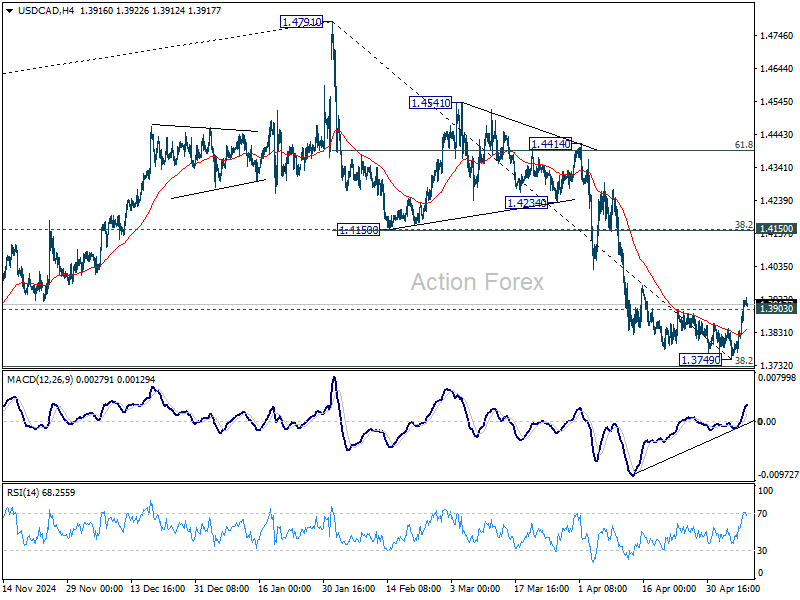

Attention is now shifting to Canada, where April employment data will be released later today. After a surprise job contraction in March, markets are looking for a modest 4.1k rebound in hiring. Unemployment rate is expected to edge up to 6.8%. With inflation risks rising and growth facing external pressure, both from tariffs, BoC is being pulled in opposite directions. Whether it prioritizes stabilizing inflation or supporting the labor market will depend heavily on how data trends evolve in the coming months.

Technically, USD/CAD's break of 1.3903 resistance confirms short term bottoming at 1.3749, on bullish convergence condition in 4H MACD, just ahead of 1.3727 fibonacci level. Further rise should be seen to 1.4150 cluster resistance (38.2% retracement of 1.4791 to 1.3749 at 1.4147). Reaction from there would decide whether fall from 1.4791 is a three-wave corrective move, or a five-wave impulse.

In Asia, at the time of writing, Nikkei is up 1.60%. Hong Kong HSI is up 0.24%. China Shanghai SSE is down -0.14%. Singapore Strait Times is up 0.73%. Japan 10-year JGB yield is up 0.034 at 1.359. Overnight, DOW rose 0.62%. S&P 500 rose 0.58%. NASDAQ rose 1.07%. 10-year yield jumped 0.0987 to 4.373.

Japan wage growth slows while Real incomes shrink, but spending rebounds

Japan’s wage data for March showed a softening trend. Nominal total cash earnings rose 2.1% yoy, below expectations of 2.4% yoy and down from February’s 2.7% yoy. This marked the 39th consecutive month of nominal wage growth, but the pace is clearly losing momentum.

More concerning was the continued decline in inflation-adjusted real wages, which fell -2.1% yoy, down for a third straight month, highlighting the squeeze on household purchasing power as consumer prices remained elevated at 4.2% yoy, particularly for food staples like rice.

Base salaries (regular pay) grew 1.3% yoy, unchanged from February, suggesting underlying wage trends remain stable but not accelerating. However, overtime pay, often viewed as a proxy for labor demand, fell -1.1% yoy, marking its first decline since September and the sharpest drop since April last year.

Despite the income pressures, household spending surprised to the upside. It rose 2.1% yoy, far exceeding the expected 0.2% yoy and marking the first increase in two months. On a seasonally adjusted month-on-month basis, spending climbed 0.4%. The increase was largely driven by higher electricity bills and rising education-related expenses.

China’s exports surge 8.1% yoy in April, ASEAN shipments jump 20.8% yoy, US slide -21% yoy

China’s exports surged 8.1% yoy to USD 315.7B in April, far exceeding expectations of 1.9% yoy. However, the headline strength masks key shifts in trading patterns.

Exports to the US tumbled by -21% yoy, a sharp reversal from March’s 9.1% yoy gain, reflecting the drag from elevated tariffs. In contrast, shipments to the ASEAN bloc jumped 20.8% yoy, with Vietnam, often seen as a transshipment route for Chinese goods, seeing a 22.5% yoy rise.

Yet, with the US now eyeing a steep 46% tariff on Vietnamese imports and imposing a 10% baseline levy, this channel for China could soon come under pressure.

Elsewhere, exports to the European Union also improved, rising 8.3% yoy.

Imports dipped just -0.2% yoy, a much smaller contraction than the expected -5.9% yoy. As a result, trade surplus narrowed from USD 102.6B to USD 96.2B, above the expected USD 94.3B.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1181; (P) 1.1259; (R1) 1.1305; More...

EUR/USD's corrective fall from 1.1572 resumed by breaking through 1.1265 and intraday bias is back on the downside. Deeper fall would be seen to 38.2% retracement of 1.0176 to 1.1572 at 1.1039. But strong support should be seen there to bring rebound. On the upside, break of 1.1380 will suggest that the correction has completed, and bring retest of 1.1572.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0808) holds.

China’s exports surge 8.1% yoy in April, ASEAN shipments jump 20.8% yoy, US slide -21% yoy

China’s exports surged 8.1% yoy to USD 315.7B in April, far exceeding expectations of 1.9% yoy. However, the headline strength masks key shifts in trading patterns.

Exports to the US tumbled by -21% yoy, a sharp reversal from March’s 9.1% yoy gain, reflecting the drag from elevated tariffs. In contrast, shipments to the ASEAN bloc jumped 20.8% yoy, with Vietnam, often seen as a transshipment route for Chinese goods, seeing a 22.5% yoy rise.

Yet, with the US now eyeing a steep 46% tariff on Vietnamese imports and imposing a 10% baseline levy, this channel for China could soon come under pressure.

Elsewhere, exports to the European Union also improved, rising 8.3% yoy.

Imports dipped just -0.2% yoy, a much smaller contraction than the expected -5.9% yoy. As a result, trade surplus narrowed from USD 102.6B to USD 96.2B, above the expected USD 94.3B.

Japan wage growth slows while Real incomes shrink, but spending rebounds

Japan’s wage data for March showed a softening trend. Nominal total cash earnings rose 2.1% yoy, below expectations of 2.4% yoy and down from February’s 2.7% yoy. This marked the 39th consecutive month of nominal wage growth, but the pace is clearly losing momentum.

More concerning was the continued decline in inflation-adjusted real wages, which fell -2.1% yoy, down for a third straight month, highlighting the squeeze on household purchasing power as consumer prices remained elevated at 4.2% yoy, particularly for food staples like rice.

Base salaries (regular pay) grew 1.3% yoy, unchanged from February, suggesting underlying wage trends remain stable but not accelerating. However, overtime pay, often viewed as a proxy for labor demand, fell -1.1% yoy, marking its first decline since September and the sharpest drop since April last year.

Despite the income pressures, household spending surprised to the upside. It rose 2.1% yoy, far exceeding the expected 0.2% yoy and marking the first increase in two months. On a seasonally adjusted month-on-month basis, spending climbed 0.4%. The increase was largely driven by higher electricity bills and rising education-related expenses.

Cliff Notes: Opportunities in Trade

Key insights from the week that was.

In Australia, the latest instalment of the household spending indicator, which covers around 60% of the consumer basket, provided another soft read on the consumer spending pulse. The indicator suggests nominal spending fell –0.3% in March, knocking the quarterly growth pace down to 1.0% which, after accounting for inflation, left real spending flat over the first three months of the year. Although this data is still considered experimental, the signal it provides matches other official ABS data, retail sales volumes flatlining over the same period, and clear signs of weakness within Westpac’s own panel data and card spending insights, as discussed in detail in the Westpac Red Book.

There are still some crucial unknowns when it comes to the full wash-up for household consumption, particularly as it relates to services spending. But the dataflow thus far is clearly pointing to downside risks for Q1 consumption and GDP growth, due in roughly four weeks’ time. Balancing these risks, a positive contribution from net exports is likely amid extensive tariff front-running prior to ‘Liberation Day’.

While immediate and medium-to-long term trade risks remain for the global economy, this week’s essay by Chief Economist Luci Ellis highlights that enduring opportunities are present for countries like Australia. Detailed below, this week also witnessed the first steps towards a hoped-for end to US trade hostility, with a trade ‘framework’ agreed between the US and UK.

Next week, labour market data will be in the spotlight domestically with the release of the Q1 Wage Price Index and April Labour Force Survey. Any further indication of easing labour market conditions will be closely scrutinised in the context of moderating inflation and heightened global uncertainty – dynamics that Westpac and the market believe will support a 25bp rate cut from the RBA at its May 19-20 policy meeting.

Offshore, the focus was the US and the UK.

The FOMC kept rates steady at its May meeting as they await further clarity on trade policy. Notable in the meeting communications is that the FOMC remain sanguine on the immediate outlook for growth and the labour market, emphasising for economic activity that annualised domestic demand growth (which omits net export’s contribution) was around trend at +2.4% in Q1 against GDP’s –0.3% print (net exports sizeable contraction in Q1 the result of tariff front running by business). On the outlook though, the committee “judges that the risks of higher unemployment and higher inflation have risen”.

In the press conference, Chair Powell went on to outline that, in determining the appropriate stance of policy, the deviation from target for both inflation and unemployment and the risks to each trajectory will jointly determine the Committee’s action at each meeting. Westpac continues to forecast just 50bps of cuts in the second half of 2025 and stability through 2026 as inflation and associated risks linger. The market continues to call for more easing, with at least 100bps of cuts priced by mid-2026.

Subsequently in the UK, the Bank of England cut Bank Rate by 25bps to 4.25% as inflation eased and slack builds in the economy. The detail of the vote revealed a wide range of views on the outlook – two members voted to leave policy unchanged, two to cut by 50bps, while five supported the 25bp cut. The committee’s language about their policy stance remained largely unchanged, continuing to emphasise “a gradual and careful approach to the further withdrawal of monetary policy restraint”.

While previous increases in energy prices are expected to push headline UK inflation to 3.5%yr later this year, “progress on disinflation in domestic price and wage pressures is generally continuing”. The BoE’s updated inflation projections showed downward revisions, with inflation now anticipated to reach 2%yr in Q1 2027, three quarters earlier in comparison to the February forecast. And, although the GDP growth this year was revised significantly higher, to 1.1%yr, the change mostly reflected a steeper increase in Q1 2025, with growth in 2026 now expected to be 0.3ppts lower at 1.2%yr – a rate below the BoE’s estimate of supply growth, suggesting weakness in demand will continue to act against remaining inflation pressures.

Uncertainty from global trade policies were also considered. Governor Bailey welcomed emerging news that the US and UK had reached a trade deal (see below). However, he also pointed out that the UK is a very open economy, so it will be impacted through tariffs imposed on other economies. Bank of England analysis suggests that, over the three-year forecast horizon, tariffs are likely to lower UK GDP by around 0.3%. The estimated impact on inflation is inconclusive, affected by exchange rate movements, the health of global demand, global supply chain disruptions and US export prices.

To the deal struck on US/UK trade. Admittedly it is considered a trade ‘framework’ not a ‘full and comprehensive’ agreement as promised previously by US President Donald Trump. Nonetheless, it has been cheered by markets who hope it is the first of many steps towards an end to the heightened uncertainty over global trade. Under the framework, the UK will give the US improved access to UK agriculture (beef and ethanol were noted in particular) and will purchase more aircraft from Boeing. In return, the first 100,000 cars exported from the UK to the US each year will be tariffed at 10% rather than 25%. The UK communications on the deal also referenced the tariff on UK steel and aluminium exports to the US being reduced from 25% to zero, but the US communications referenced only "an alternative arrangement". Pharmaceutical exports from the UK to the US will also reportedly receive preferential treatment, though details are still to be agreed. There is no change to the UK's digital service tax or food safety rules, and UK goods not specified under the agreement will still face a 10% tariff in the US. We expect to see more limited agreements in coming weeks. Whether negotiations continue to build towards comprehensive arrangements remains an open question.

Opportunities Amidst the Chaos

Amidst all the Trump-induced chaos and uncertainty, there are opportunities for other countries.

Tariffs, policy chaos, deportations – even challenges to the rule of law. So much of the Trump administration’s agenda represents an act of economic self-harm for the US. No wonder US consumer sentiment has plummeted in the past few months. Some of that sense of gloom even leaked into other countries such as Australia, though to a much lesser extent. Certainly, global economic growth will take at least some hit because of the US’s travails. Yet for countries other than the US – including Australia – the current situation also presents opportunities, not all of which have been fully appreciated.

The first opportunity stems from the overvaluation of the USD, which is still more than 15% above standard estimates of inflation-adjusted fair value against its trading partners, including the AUD. An overvalued currency means an uncompetitive economy. This opens up opportunities for firms in other countries, either to sell into the US market or to bid business away from US competitors at home or in third-country markets. While tariffs override this advantage for goods sold into the US market, the same is not true for services.

Recent comments about tariffing foreign-made films might suggest that services imports more broadly could soon face similar imposts. However, it is unlikely to be practically feasible to tariff much services trade. Try as it might, the Trump administration will not be able to tax Americans’ spending on overseas holidays – at least not without some severe intervention in global card payment systems, and I don’t want to give them ideas.

Nor will it be feasible to tax the burgeoning trade in software, miscellaneous consulting and other business services. Professional services and software licencing are both large export industries for Australia, each generating more than $7½ billion in export revenue in 2024. Within the former, consulting, accounting & auditing and legal services each generated around $1 billion of export revenue. To put these in perspective, $7½ billion annual export revenue is more than Australia’s

2024 exports of copper metal, or aluminium, pharmaceuticals, alcoholic beverages, wool, rice or barley – and not much less than last year’s wheat exports.

Not all of these services exports go to the US, but it is the largest single destination for both of these broad services categories. While ever the USD remains overvalued, consultants, auditors and all those other providers of professional services will be able to undercut their American competitors for work in the US and elsewhere, whether by traveling or working remotely. And unlike say, manufactured exports, it will be easy to pivot when that overvaluation eventually unwinds.

The second opportunity stems from the revulsion-and-reallocation phase in global asset management. As we have previously discussed, the fading of the ‘US exceptionalism’ narrative means that asset managers globally are deciding that they want to be a bit less long US assets. This process had already started before ‘Liberation Day’, with US equity markets selling off and European equities rising, especially defence companies, over February and March. So far, Europe has been the main beneficiary of this asset reallocation. This is unsurprising given that European and UK-domiciled asset managers are such a large fraction of the global industry.

Australian-domiciled asset managers will nonetheless be contemplating the same issues. Aggregate data on Australia’s international investment position show that US equities were around 55% of portfolio equity assets in 2024, and US debt securities were more than a third of portfolio debt assets. (The share of US investors in Australia’s portfolio liabilities is noticeably smaller for both asset classes.)

This revulsion and reallocation process need not be a case of bringing assets home. It is simply that reallocating out of the US means reallocating into something else, and that something else can be more diversified and include Australian assets, regardless of the location of the end investor. Some of that reallocation will mean more capital, or at least cheaper capital than otherwise, for needed investment in the climate transition, in infrastructure and other areas.

A third opportunity, perhaps related to the second, centres on the defence industry. With the US under Trump looking like a less reliable defence partner and wanting its allies to provide for more of their defence themselves, Europe and other aligned nations such as Canada are looking to re-arm. In doing so, they are looking for alternatives to US equipment.

Again, this is more of an opportunity for Europe, noting that it already has extensive defence and aerospace sectors and other manufacturing industry that can be retooled. Here too, though, Australia can capitalise on this opportunity and is already doing so. We have already noted the offshore interest in Australia’s JORN (Jindalee Operational Radar Network) over-the-horizon radar technology. We are hearing from a range of clients that this interest has broadened to other countries and products. Australia has a significant defence equipment industry and provides overflow production capability for a range of overseas customers. Several offshore-headquartered defence technology firms already have operations here, building equipment for European military forces.

The broader point here is that other countries are not the US and are not constrained to behave in the same way. People adapt to events beyond their control, including the policy gyrations of other countries’ governments. To be fair, the constant renegotiation and uncertainty around some of the Trump administration’s policies makes it difficult to plan and make investment decisions involving the US. Even so, the currently overvalued USD, asset reallocation and defence pivot are all shifts that are robust to the daily headlines.

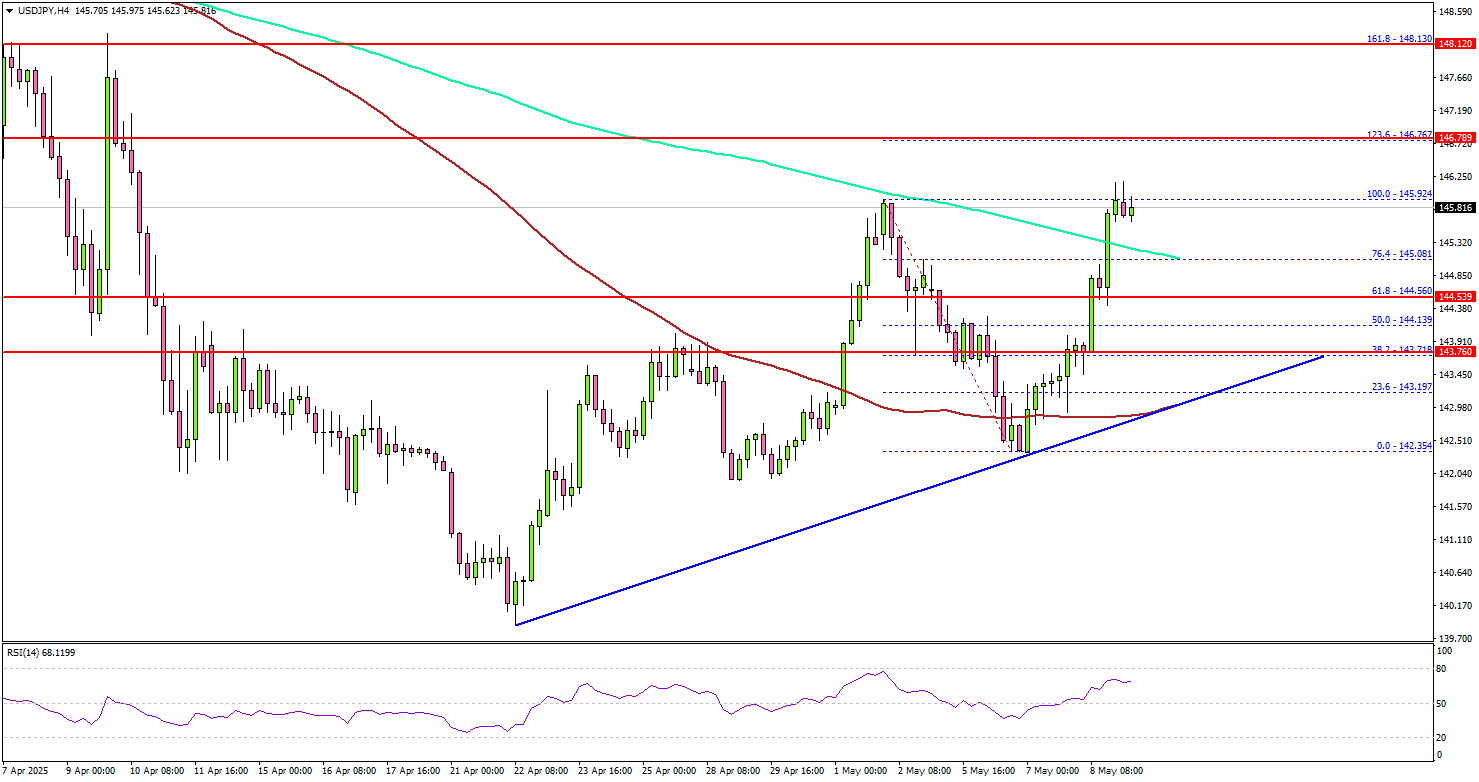

USD/JPY Aims Higher: Technical Outlook Suggests Potential for Further Gains

Key Highlights

- USD/JPY found support near 142.35 and started a fresh increase.

- A connecting bullish trend line is forming with support at 143.80 on the 4-hour chart.

- GBP/USD is correcting gains and trading below the 1.3300 support zone.

- EUR/USD started another decline and traded below the 1.1265 support zone.

USD/JPY Technical Analysis

The US Dollar remained supported above 142.20 against the US Dollar. USD/JPY is again rising and aims for a move above the 146.00 level.

Looking at the 4-hour chart, the pair started a fresh increase above the 143.50 and 144.00 levels. The pair settled above the 100 simple moving average (red, 4-hour) and recently surpassed the 200 simple moving average (green, 4-hour).

There was a clear move above the 76.4% Fib retracement level of the downward move from the 145.92 swing high to the 142.35 low.

Besides, there is a connecting bullish trend line forming with support at 143.80 on the same chart. The pair is now facing resistance near the 146.00 level. The next major resistance is near the 146.75 zone.

A close above the 147.75 level could set the tone for another increase. In the stated case, the pair could even clear the 148.50 resistance. The next major stop for the bulls could be near the 150.00 level.

On the downside, immediate support sits near the 145.00 level and the 200 simple moving average (green, 4-hour). The next key support sits near the 144.20 level. Any more losses could send the pair toward the 143.50 level.

Looking at EUR/USD, the pair started a fresh decline and the bears were able to push the pair below the 1.1265 support.

Upcoming Economic Events:

- Fed's Kugler speech.

- Fed's Goolsbee speech.

- Fed's Waller speech.

- Fed's Williams speech.

Bank of England Cuts Rates, Signals Gradual And Careful Monetary Easing

Summary

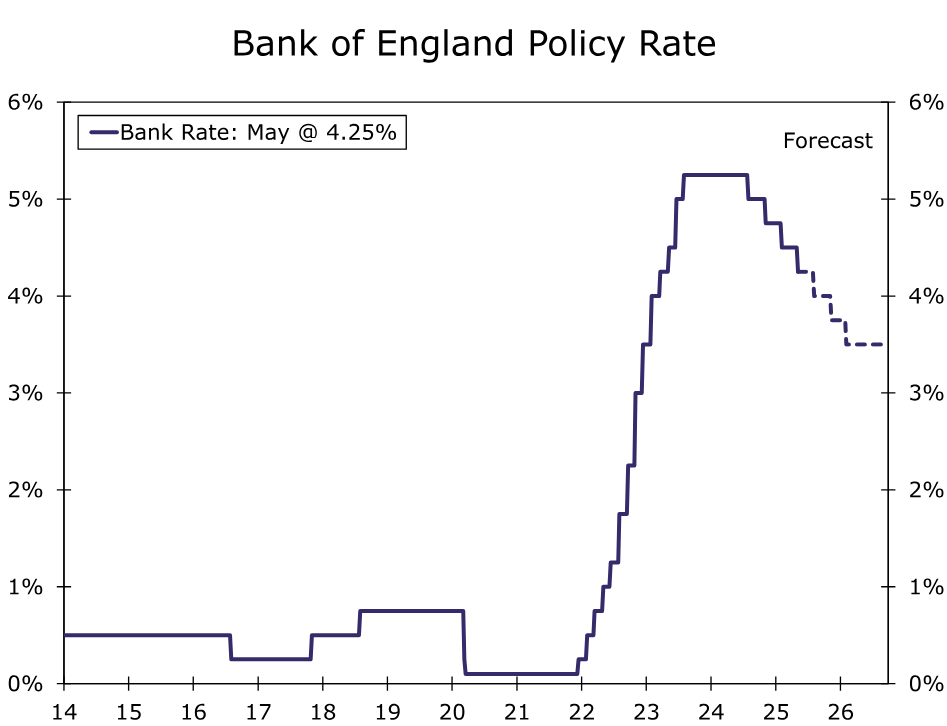

- The Bank of England (BoE) delivered a widely anticipated 25 bps rate cut at today's announcement, bringing the policy rate down to 4.25%. Between the somewhat balanced policymaker vote split, mixed commentary on economic trends, and updated economic projections that did not contain any major surprises, we view the decision as broadly neutral. In terms of forward guidance, BoE officials communicated a desire to maintain a gradual and cautious approach towards further easing.

- In terms of recent economic trends in the United Kingdom, we have yet to see data that would suggest a deviation from this gradual rate cut path. The U.K. economy started 2025 in reasonably good shape, and we see relatively limited impact on the U.K. economy from higher U.S. tariffs. There are areas of caution—such as some degree of fiscal consolidation and a mixed picture for business investment—but we believe policymakers would likely only adopt a shift in stance if these developments were to result in sharply slower overall economic growth.

- As for wage and price growth developments, the picture is somewhat mixed. While in our view the direction of wage and labor cost pressures is broadly favorable, some measures of pay growth are still elevated. On the price front, the news has been more encouraging, with March CPI inflation surprising to the downside. While disinflation progress is noticeable, services inflation is persisting for now, which we see as consistent with a more gradual pace of rate cuts.

- We maintain our view for a once-per-quarter BoE rate cut pace through Q1-2026. We see 25 bps rate cuts in August, November, and February, with the policy rate expected to reach a low of 3.50% by early next year. Given our expectation for only gradual BoE easing, combined with anticipated U.S. economic weakness later this year, we see limited pound weakness against the dollar through the end of this year. However, more pound weakness could be seen in 2026, as the Fed concludes its easing cycle and the U.S. economy recovers.

Bank of England Takes Further Step Along Its Monetary Easing Path

The Bank of England (BoE) delivered a widely anticipated 25 bps rate cut at today's announcement, bringing the policy rate down to 4.25%. The accompanying statement and updated projections were relatively balanced, which we view as consistent with the BoE maintaining a gradual pace of rate cuts for the time being.

Looking more closely at the statement itself, the first balanced element was the 5-2-2 vote split. That is, five policymakers voted for the 25 bps rate reduction, while two policymakers voted for a larger 50 bps cut and two voted for no change. In terms of the other elements of the statement, the BoE said “underlying UK GDP growth is judged to have slowed since the middle of 2024, and the labor market has continued to loosen.” The central bank also observed that “progress on disinflation in domestic price and wage pressures is generally continuing ... although indicators of pay growth remain elevated, a significant slowing is still expected over the rest of the year.”

Importantly, the BoE did not offer any significant adjustment to its future policy guidance. The central bank reiterated that a “gradual and careful approach” to the further withdrawal of monetary policy restraint remains appropriate. Additionally, the BoE also said monetary policy will need to “remain restrictive for sufficiently long” until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further.

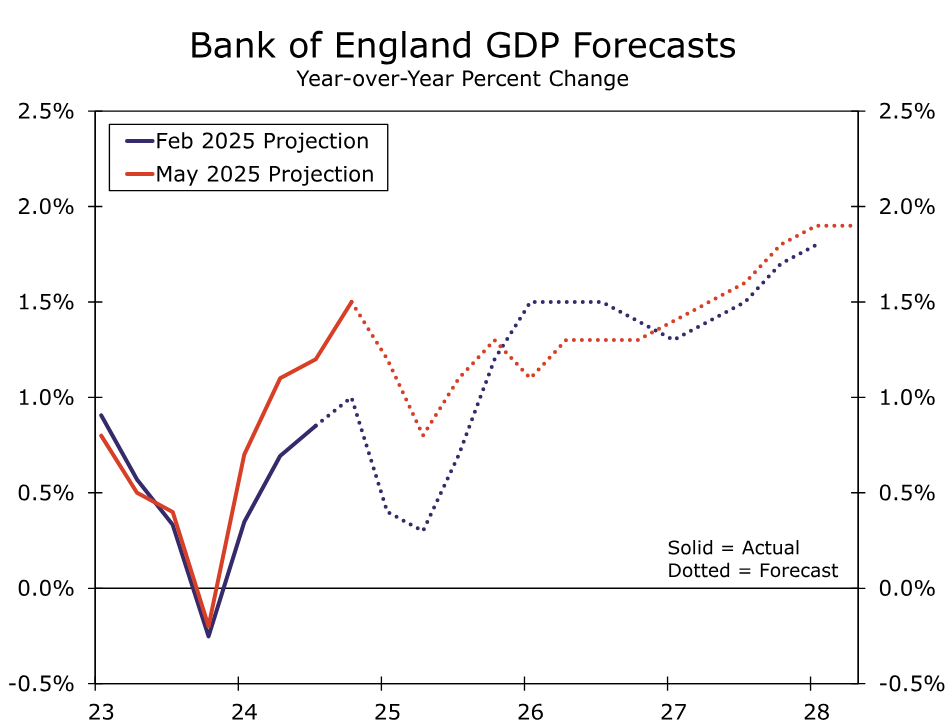

Turning to the BoE's updated economic projections, there is little to suggest an acceleration in the pace of rate cuts. The forecasts are based on an assumption that the BoE's policy rate will decline gradually to 3.50% by Q2-2026. With respect to economic growth, U.K. GDP is expected to jump 0.6% quarter-over-quarter in Q1-2025 before slowing sharply thereafter. In terms of its overall GDP forecasts, the BoE raised its growth forecast for 2025 to 1% (previously ¾%), lowered its growth forecast for 2026 to 1¼% (previously 1½%), and kept its 2027 growth forecast at 1½%.

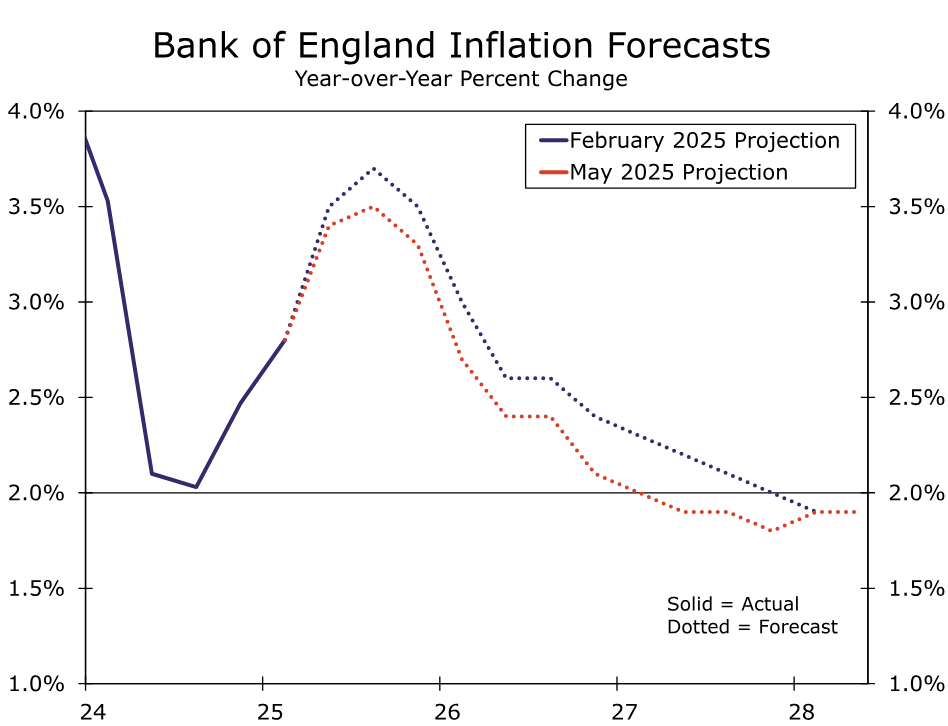

Meanwhile, the central bank lowered its CPI inflation forecast for 2025, 2026 and 2027. For a start, the BoE now sees a lower inflation peak of 3.5% in Q3-2025, compared to a previous forecast peak of 3.7%. CPI inflation is expected to return to the 2% target by early 2027, and to fall slightly below that target at 1.9% in both Q2-2027 and Q2-2028. The slowdown of inflation is predicated, in part, on a significant slowing in wage growth over the rest of this year.

A Slowdown in U.K. Growth Could Allow For Faster Rate Cuts...

Overall, today's BoE announcement was broadly neutral and, so far, the central bank has not deviated from its once-per-quarter rate cut pace. Looking forward and thinking about what could prompt a shift in approach from the central bank, we think that growth dynamics have the most potential to prompt a shift to a faster pace of BoE easing, though probably not for some time.

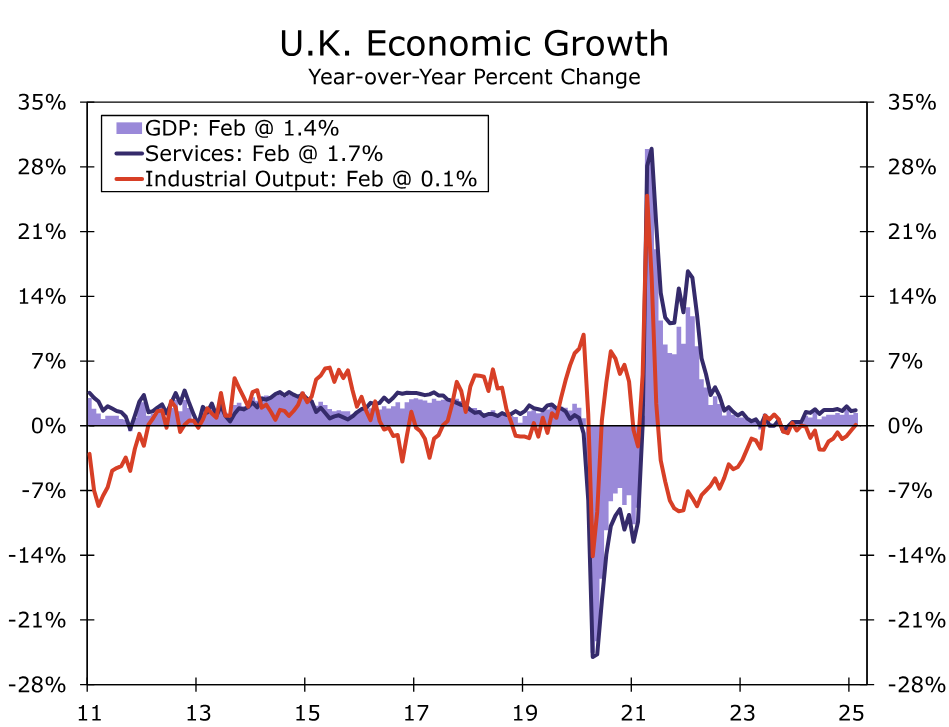

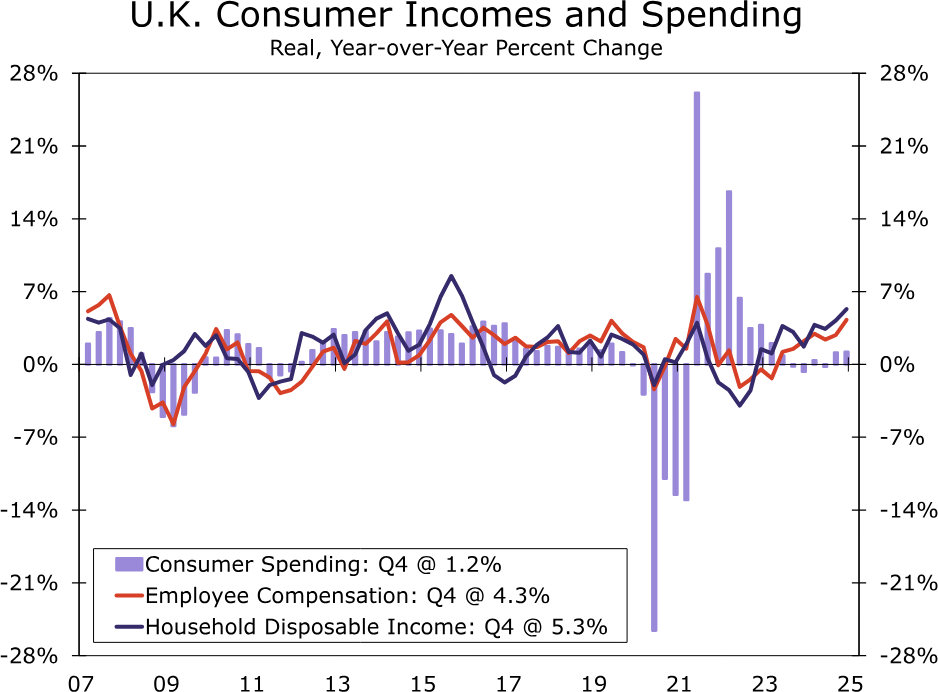

The U.K. economy started 2025 on a relatively solid footing. Retail sales rose every month during the first quarter, and February GDP registered a sizable 0.5% month-over-month gain. Considering the gains during the January-February period, the United Kingdom appears on track for Q1 GDP growth of around 0.5% overall. Some underlying dynamics behind the recent U.K growth details also appear favorable. Notably, the latest available data show real household disposable income grew 5.3% year-over-year in Q4-2024, well in excess of growth in consumer spending. Coupled with early-year advances seen in both services output and retail sales, this suggests that the U.K. consumer could provide some support for activity this year. That said, there are some cautionary factors to watch for. One concern on the consumer front is the increase in National Insurance Contributions that took effect in April, a factor that could lead some firms to adjust employment or wages, which could offer some headwinds to real income growth. Finally, while higher U.S. tariffs are certainly not a positive for the United Kingdom, the British economy could be less negatively impacted by U.S. tariffs than some other regions. We would argue the United Kingdom's direct exposure to higher U.S. tariffs is somewhat limited. U.K. exports of goods the United States (which are subject to tariffs) accounted for a relatively modest 2.1% of U.K. GDP in 2024, while U.K. exports of services to the United States (which for now are not subject to tariffs) accounted for a more sizable 4.8% of U.K. GDP last year.

While the consumer outlook appears reasonably solid and the direct negative impact from tariffs could perhaps be limited, there are nonetheless still reasons for concern regarding the U.K. outlook. For one, the government's fiscal stance has turned more cautious in recent months. Faced with a shortfall in tax revenues and increased debt interest costs, the Chancellor of the Exchequer Rachel Reeves announced in the Spring Budget Statement in late March a package of £8.4B of welfare reductions and day-to-day spending cuts, an extra £3.4B from higher revenues from planning reforms, and £2.2B from more efficient tax collection. Even with the measures, the government has only a slim £9.9B fiscal buffer, meaning slower economic growth and tax revenues, or alternatively, higher yields, could still lead to further consolidation measures ahead.

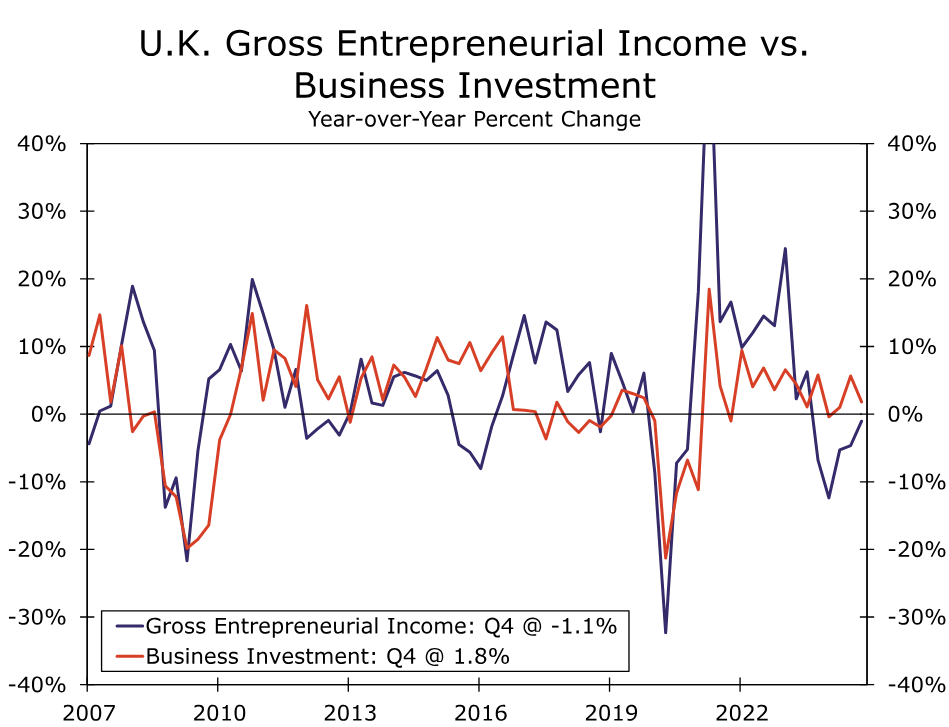

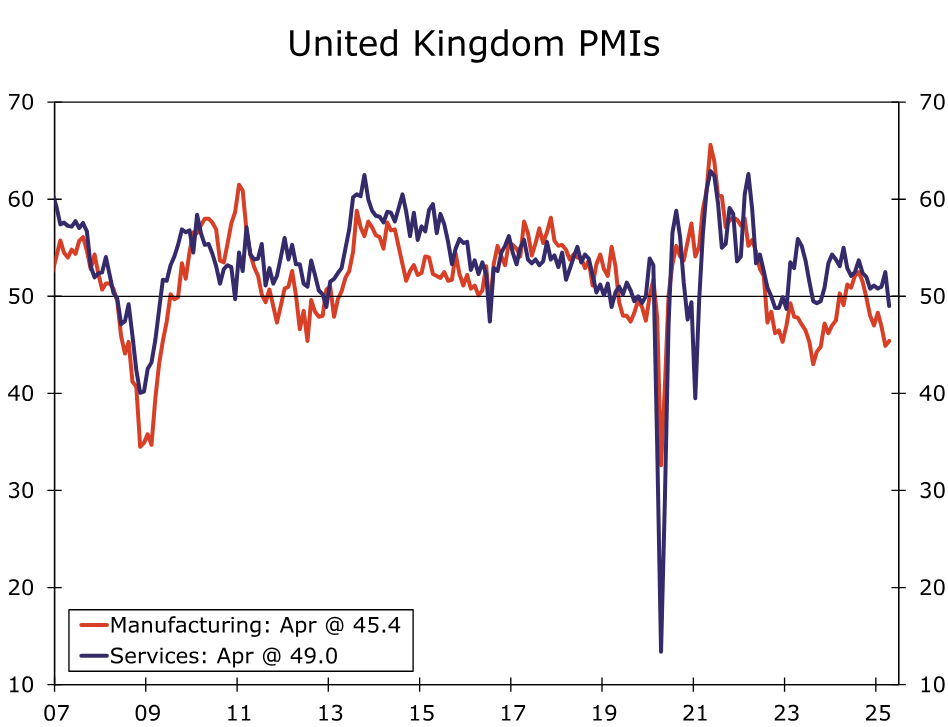

The business sector outlook also remains decidedly mixed. According to the OECD, gross entrepreneurial income of non-financial corporates fell 1.1% year-over-year in Q4-2024, a potential restraining influence on business investment moving forward. The increase in the employers' National Insurance Contributions that took effect in April could also be a factor that weighs on profits, at the margin. More broadly, while the United Kingdom was spared the worst of the direct impact from higher U.S. tariffs, the indirect impact on the U.K. economy could still be significant. Given the likelihood of higher prices and/or lower growth across many major economies—including the United States, Eurozone and China—we have lowered our global GDP growth forecast to just 2.3% for both 2025 and 2026. The rather mixed outlook for U.K businesses is also reflected in the April PMI survey. It showed a modest improvement in the manufacturing PMI to 45.4, a reading that nonetheless remains very much in contraction territory. Meanwhile, the services PMI fell sharply to 49.0 from 52.5 in March, also entering contraction territory. Especially as this year progresses, and the full impact of higher U.S. tariffs and slower global growth takes effect, we expect the U.K. economy to underperform. Indeed, we forecast U.K. GDP growth of just 0.7% in 2025, rising to 1.5% in 2026. Our outlook for 2025 GDP growth is modestly below the BoE's own forecast, and cumulatively, our growth forecast is also below the central bank's estimates of potential growth, which it sees as around 1.5% over the medium term. Against this backdrop, we view our subpar U.K growth outlook as consistent with slowing employment growth, rising unemployment, and some easing in wage pressures—trends that could eventually be consistent with a more accelerated pace of Bank of England monetary easing.

...But Wage And Price Trends Will Hold The Key To Whether Faster Easing Occurs

While the U.K. growth outlook in isolation might suggest scope for an eventual faster pace of easing, whether the Bank of England ultimately pursues that approach will in large part depend on whether wage and inflation trends show clearer and more decisive deceleration. The BoE has been regularly surprised in recent years, during and following the pandemic, initially by how quickly wages and inflation spiked surrounding the pandemic, and subsequently by how persistent and stubborn wage and price pressures have been in the years since. Thus, although the BoE's analysis and modeling might suggest an expected slowdown in wage and prices, the central bank might need to see more evidence of that slowdown before transitioning to a more frequent cadence of rate cuts.

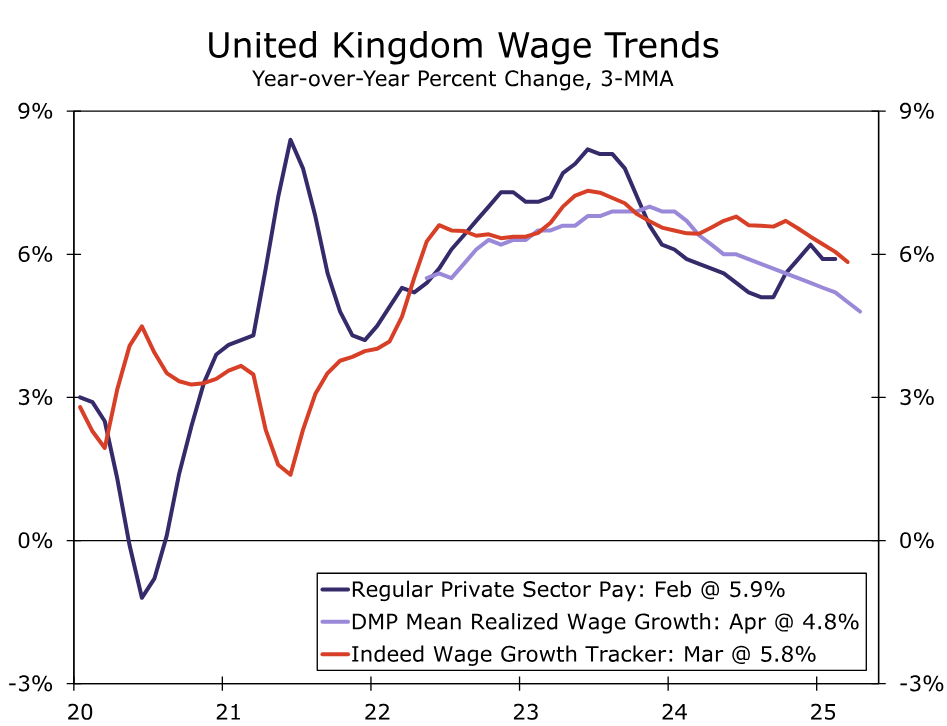

So far, the evidence on wage growth is mixed. For the December-February period, average weekly earnings for the private sector excluding bonuses—a measure closely watched by BoE policymakers—rose 5.9% year-over-year, in line with the consensus forecast and steady compared to the prior reading. This measure of wage growth has also quickened slightly since late 2024. Still, recent pay growth has come in somewhat below the BoE's previous projections. Other indicators of wage growth hint at the potential for further deceleration ahead. For example, realized wage growth as reported by the BoE's Decision Makers Panel slowed to 4.8% year-over-year in the three months to April. Similarly, the U.K. Indeed Wage Tracker has also slowed recently, though it remains elevated at 5.8% year-over-year in the three months to March. While somewhat dated, the most recent estimate of U.K. unit labor costs showed a gain of 4.5% year-over-year in Q3-2024, a level that we view as likely too high to be compatible with the BoE's 2% inflation target on a sustained basis. A modest improvement in U.K. productivity since then may have seen unit labor costs soften a bit further. Altogether, our sense is that the direction of wage and labor cost pressures is broadly favorable from the BoE's inflation targeting perspective. At the same time, we suspect that policymakers will want to see clearer evidence of a more pronounced slowdown in wage pressures before they would contemplate accelerating the pace of rate cuts.

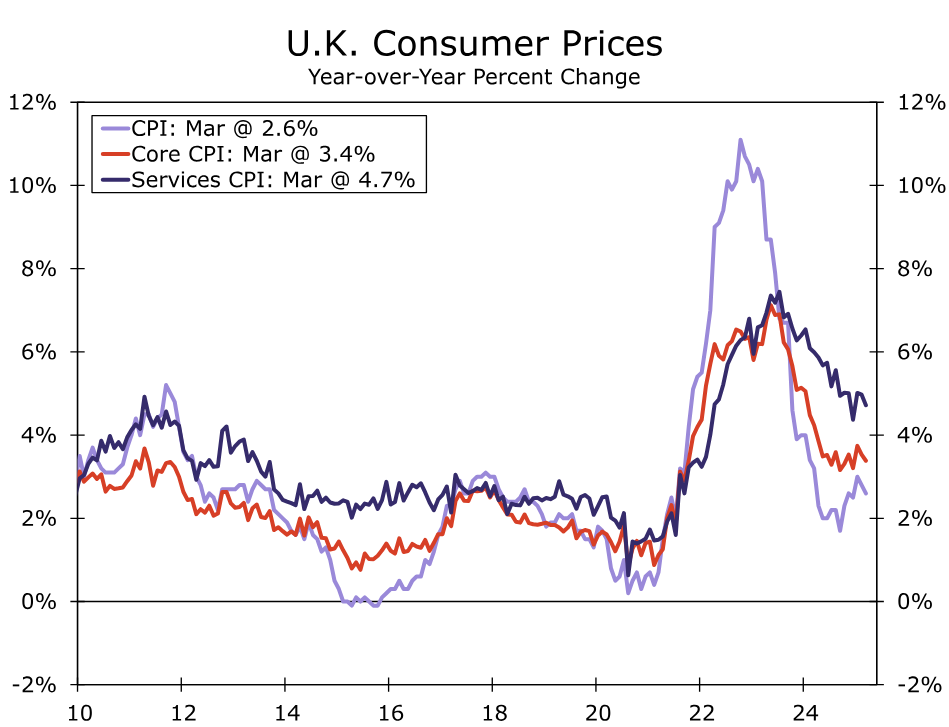

Regarding prices, the latest inflation news has been a bit more encouraging, with the March CPI surprising modestly to the downside. Headline inflation slowed to 2.6% year-over-year, and a sharp slump in oil prices since early April could help restrain headline inflation in the immediate months ahead. March core CPI inflation eased to 3.4%, and services inflation slowed a bit more than forecast to 4.7%. Specifically with respect to services prices, our own seasonally adjusted measures suggest that services inflation has advanced at around a 4.50%-4.75% annualized rate over the past six months. The key takeaway, in our view, is that while the recent price trends in U.K. core inflation and services inflation are encouraging, they remain more consistent with a steady rather than accelerated pace of monetary easing by the Bank of England at this stage.

Overall, we view today's policy announcement as broadly neutral and are not yet convinced the Bank of England will shift to an accelerated rate cut path. For the time being, our base case remains for Bank of England easing to continue at a 25 bps rate cut per quarter pace. We forecast 25 bps rate cuts in August and November of this year, and February of next year, which would bring the policy rate to a low of 3.50%. While we view the growth outlook as potentially consistent with an eventual acceleration of monetary easing, we think policymakers will need to see more convincing evidence that wages and prices are indeed slowing in a manner that is more compatible with sustained convergence towards the 2% inflation target before adjusting rates more frequently. We think it will be several months, at the earliest, before sufficient evidence emerges on the wage and price front for BoE policymakers to be comfortable picking up the pace of easing. Moreover, we think it could be several months before the full effect of higher U.S. tariffs and weaker global growth are fully apparent, prompting the Federal Reserve to also begin lowering interest rates from later this year. Thus, while we would view the risks to our outlook as tilted toward faster and more pronounced rate cuts, that appears unlikely until late this year at the earliest. Indeed, we think the most plausible risk scenario would see the BoE deliver 25 bp rate cuts in August, November and also December this year, along with February of next year, for a policy rate low of 3.25%. However, that outcome would probably only happen if U.K. growth and inflation data surprise consistently to the downside. Finally, the relatively gradual easing we expect from the BoE, combined with the economic challenges the United States should face in the second half of this year, in our view, suggests only limited weakness in the pound through most of 2025. We see more potential for sterling to weaken in 2026, as U.S. economic growth recovers and as Fed easing comes to an end. Our medium-term outlook anticipates a GBP/USD exchange rate of $1.3100 by the end of 2025, declining to $1.2800 by late 2026.