Sample Category Title

Dollar Index: Bullish Bias Above Broken Psychological 100.00 Level

The dollar index edged lower from one month high on Friday, but remains constructive, as the latest bullish acceleration broke and establishes above psychological 100 level, which repeatedly capped attacks in past three weeks.

The dollar is also on track for the third consecutive weekly gain that contributes to signals of possible stronger recovery.

Profit-taking from sharp fall in past three months lifted the dollar’s price, with brightening outlook after the US reached trade deals with a number of large economies and signals of talks with China, adding to supportive factors, along with the latest remarks from US policymakers that persisting uncertainty would continue to offset expectations for rate cuts in coming months.

The recovery is supported by formation of bear trap pattern (under 98.92 Fibo support) on weekly chart, with improving technical picture on daily chart (strengthening positive momentum / 10/20 DMA turned to bullish setup and formed a bull-cross) although more work at the upside will be required to verify positive signals.

Weekly close above 100 level (psychological / near Fibo 38.2% of 104.30/97.65 bear-leg) will be the minimum requirement to keep alive optimisms for further recovery, with lift above 100.97 (50% retracement) to validate bullish signal.

Res: 100.69; 100.97; 101.76; 102.00.

Sup: 100.19; 100.00; 99.22; 98.85.

Fed’s Kugler: Labor market stable, likely near maximum employment

In a speech today, Fed Governor Adriana Kugler described the U.S. labor market as “stable,” noting that key indicators such as the unemployment rate, currently at 4.2%, have remained within a narrow and consistent range.

She highlighted that temporary layoffs have returned to pre-pandemic levels, and both job vacancies and quit rates have plateaued, indicating a moderation in labor market churn.

Kugler further stated that the economy is likely “close to maximum employment,” referencing model-based estimates of the natural rate of unemployment (u*) that align with the current 4.2% level.

Fed’s Barr: Tariffs to push inflation higher, job losses also a major concern

In a speech today, Fed Governor Michael Barr acknowledged that the US economy began the current quarter from a “relatively strong position,” describing overall conditions as “resilient.” However, he cautioned that this solid foundation is being increasingly overshadowed by rising trade policy uncertainty, particularly from the recent wave of tariffs.

Barr expected "tariffs to lead to higher inflation" in the US and “lower growth” starting later this year. He explained that the new tariffs—unprecedented in size and scope in the modern era—could disrupt global supply chains and exert lasting upward pressure on prices. At the same time, he is “equally concerned” that the resulting economic drag could lead to job losses.

Despite these risks, he emphasized that monetary policy is in a “good position” to adjust as needed once the full effects of the tariffs become clearer.

BoE’s Bailey highlights asymmetric risks: Demand weakness warrants sharper monetary response

In a speech following BoE's Monetary Policy Report released yesterday, Governor Andrew Bailey elaborated on the two alternative scenarios laid out alongside the baseline forecast.

The first scenario envisions that heightened global and domestic uncertainty could suppress UK demand more than currently expected, "easing inflationary pressures".

In contrast, the second scenario assumes that recent energy price increases could trigger renewed second-round effects in domestic prices, with tighter supply conditions "increasing inflationary pressures".

Bailey emphasized that these scenarios are not simply stylized upside or downside risks to inflation but are meant to illustrate the underlying mechanisms that could shift the inflation path.

He stressed, "it matters whether inflation differs from the baseline because of demand or supply". And, the size of the required monetary policy response might be different.

From a monetary policy standpoint, Bailey explained that a demand-driven downside scenario would likely warrant a stronger policy response than a supply-driven upside shock. That's "simply because there is more of a trade-off to balance when inflation and activity move in different directions," he added.

ECB’s Simkus and Rehn warn of growth risks

Comments from ECB Governing Council members today reinforced expectations for a rate cut in June, while also highlighting growing concern over the deteriorating macro environment.

Lithuania’s Gediminas Šimkus acknowledged that geopolitical developments since the start of the year have been negative for the economy, adding that inflation is now under "downward pressure". He noted that June projections "may be a little bit worse" and warned of the risk the central bank will undershoot its inflation target.

He also pointed to the risk of China re-routing goods to Europe in response to rising US trade barriers—a trend that could weigh on European industry and import prices.

Šimkus indicated that a June rate cut is needed but remained non-committal on the pace of further easing, saying it’s still unclear whether the next move after June would come in July or September.

Separately, Finland’s Olli Rehn struck a similar tone, citing pervasive uncertainty and reaffirming that the Governing Council will retain "full freedom of action" to meet its price stability mandate.

While Rehn noted that progress has been made in bringing inflation toward the 2% target, he cautioned that global trade tensions pose a meaningful downside risk to growth.

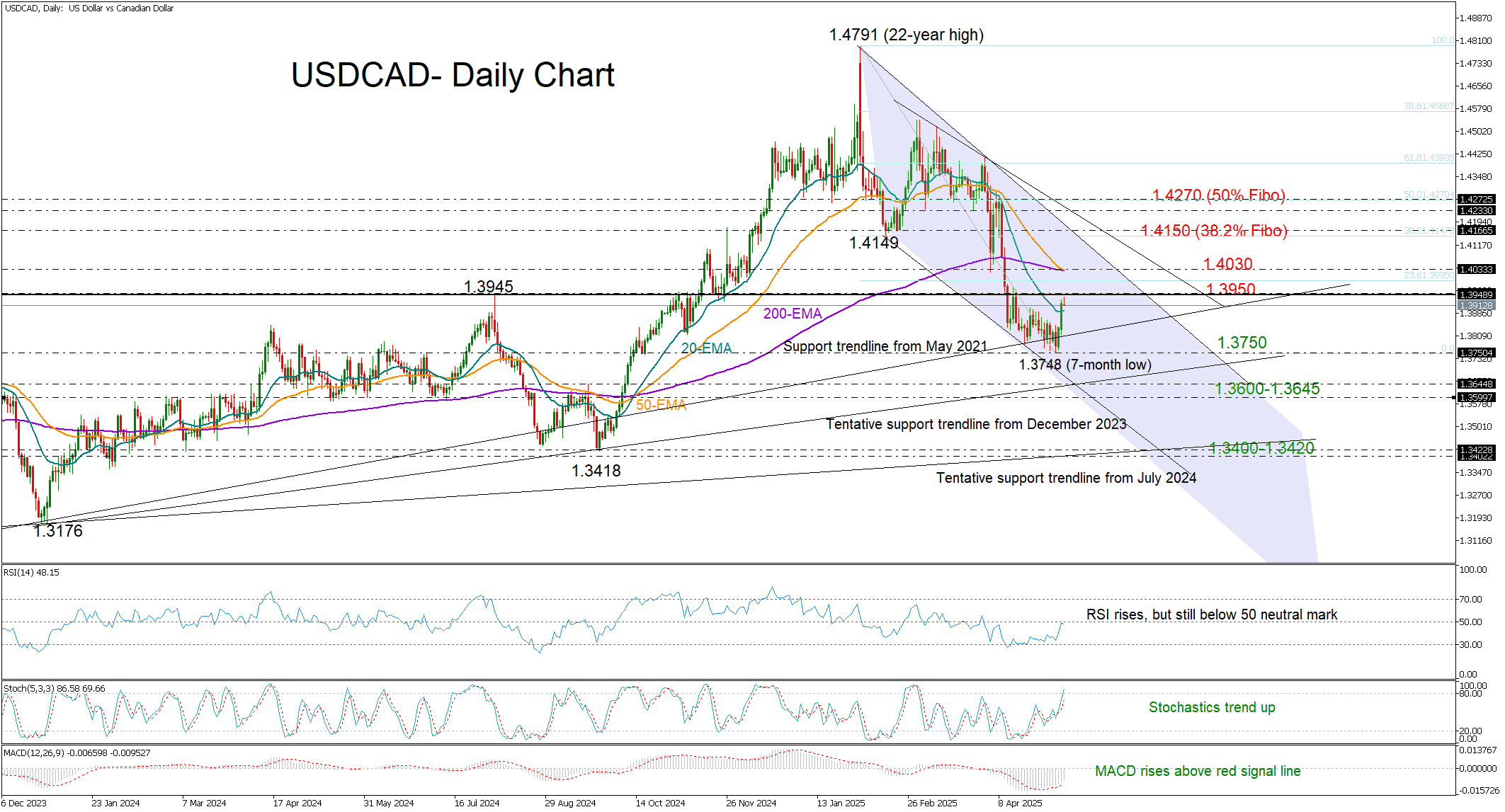

USD/CAD Pivots Higher: Is This Rebound Sustainable?

- USD/CAD finds buyers near a seven-month low.

- Market sentiment shows signs of improvement.

- Key resistance levels remain on the upside.

USDCAD is on the move, climbing off a seven-month low after news broke that the White House struck a trade deal with the UK. Hopes are now rising that more international agreements could be on the horizon, but in the meantime all eyes will turn to the Canadian employment data as the jobless rate is expected to rise back to a three-year high of 6.8%.

From a technical perspective, the rebound kicked in around the October 2024 base of 1.3750. Since then, the bulls have managed to push the pair above the 20-day exponential moving average (EMA) for the first time in seven months, signaling renewed upside interest.

Momentum indicators are starting to catch up, reinforcing the ongoing bullish action. But for a meaningful rally, a clear break above the upper band of the broad sideways trajectory at 1.3950 is essential. Even more important would be a move past the long-term EMAs at 1.4030. If that happens, momentum could accelerate toward the 1.4150 region, where the 38.2% Fibonacci retracement level of the latest downtrend lies, and then potentially stretch towards the 50% Fibo mark at 1.4272.

On the flip side, failure to hold above 1.3950 and a dip below the 20-day EMA at 1.3890 could squeeze the price back to the 1.3750 support zone. Note that the RSI is still hovering below its neutral 50 level, suggesting buyers haven’t fully taken control. A deeper pullback could find firmer ground at the rising trendline from December 2023 around 1.3645. If the 1.3600 round level gives way too, a more aggressive sell-off toward the August–September double-bottom area of 1.3420 could be on the cards.

In a nutshell, USDCAD has found some bullish momentum – but unless it can decisively clear the 1.3950–1.4030 barrier, the rebound may prove short-lived.

EUR/USD Trims Gains While USD/CHF Regains Strength

EUR/USD extended losses and traded below the 1.1250 support. USD/CHF is rising and might aim for a move toward the 0.8400 resistance.

Important Takeaways for EUR/USD and USD/CHF Analysis Today

- The Euro struggled to clear the 1.1380 resistance and declined against the US Dollar.

- There is a key bearish trend line forming with resistance at 1.1240 on the hourly chart of EUR/USD at FXOpen.

- USD/CHF is showing positive signs above the 0.8265 resistance zone.

- There is a connecting bullish trend line forming with support at 0.8300 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair failed to clear the 1.1380 resistance. The Euro started a fresh decline below the 1.1300 support against the US Dollar.

The pair declined below the 1.1250 support and the 50-hour simple moving average. Finally, the pair tested the 1.1200 level. A low was formed at 1.1196 and the pair is now consolidating losses. The pair is showing bearish signs, and the upsides might remain capped.

There was a minor increase toward the 23.6% Fib retracement level of the downward move from the 1.1381 swing high to the 1.1196 low. Immediate resistance on the upside is near the 1.1240 level.

There is also a key bearish trend line forming with resistance at 1.1240. The next major resistance is near the 1.1290 zone and the 50-hour simple moving average or the 50% Fib retracement level of the downward move from the 1.1381 swing high to the 1.1196 low.

The main resistance sits near the 1.1335 level. An upside break above the 1.1335 level might send the pair toward the 1.1380 resistance. Any more gains might open the doors for a move toward the 1.1420 level.

On the downside, immediate support on the EUR/USD chart is seen near 1.1200. The next major support is near the 1.1165 level. A downside break below the 1.1165 support could send the pair toward the 1.1120 level.

USD/CHF Technical Analysis

On the hourly chart of USD/CHF at FXOpen, the pair started a decent increase from the 0.8200 support. The US Dollar climbed above the 0.8245 resistance zone against the Swiss Franc.

The bulls were able to pump the pair above the 50-hour simple moving average and 0.8300. A high was formed at 0.8340 and the pair is now consolidating gains above the 23.6% Fib retracement level of the upward move from the 0.8185 swing low to the 0.8340 high.

There is also a connecting bullish trend line forming with support at 0.8300. On the upside, the pair is now facing resistance near 0.8340. The main resistance is now near 0.8350.

If there is a clear break above the 0.8350 resistance zone and the RSI remains above 50, the pair could start another increase. In the stated case, it could test 0.8400. If there is a downside correction, the pair might test the 0.8300 level.

The first major support on the USD/CHF chart is near the 0.8265 level and the 50% Fib retracement level of the upward move from the 0.8185 swing low to the 0.8340 high.

The next key support is near the 0.8245 level. A downside break below 0.8245 might spark bearish moves. Any more losses may possibly open the doors for a move toward the 0.8200 level in the near term.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

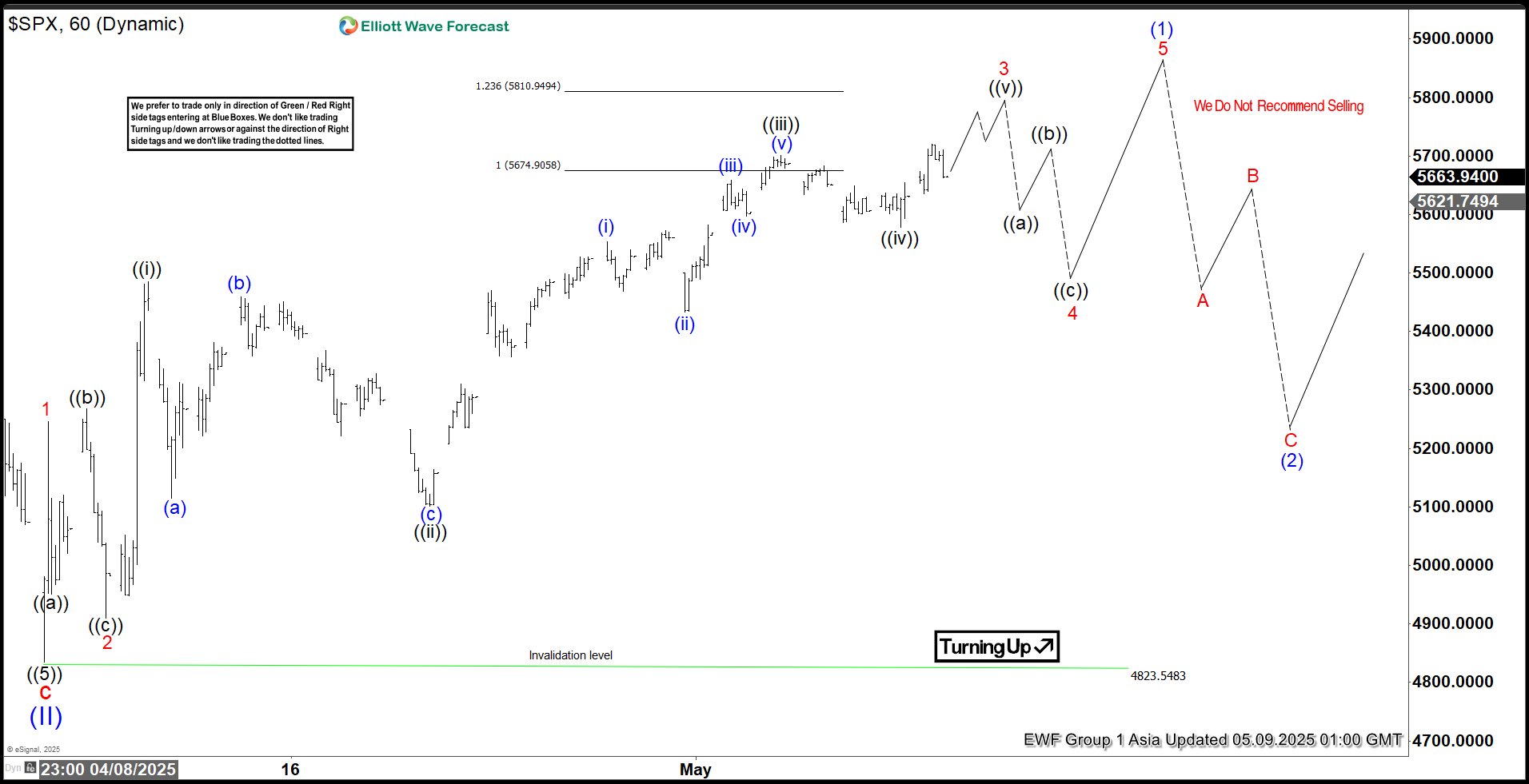

Elliott Wave Framework Highlights S&P 500 (SPX) Bullish Impulse

The S&P 500 ($SPX) has shown significant correction since its peak on February 17, 2025, before a tariff announcement. We propose that the corrective phase, labeled as wave (II), concluded at 4823. However, for the index to confirm the end of this correction and rule out a potential double correction, it must surpass the prior wave (I) high of 6147.43. Since the wave (II) low, the SPX has embarked on an upward trajectory, characterized as a nesting impulse—a pattern where waves build momentum in a structured, upward climb.

From the wave (II) low, the rally began with wave 1 peaking at 5246.57, followed by a pullback in wave 2 to 4910.42. The index then surged in wave 3, which is unfolding in a five-wave impulse pattern on a smaller degree. Within wave 3, the first sub-wave ((i)) reached 5456.9, with a dip in wave ((ii)) to 5101.63. The index climbed again in wave ((iii)) to 5700.7, followed by a minor pullback in wave ((iv)) to 5578.64. We anticipate the index will extend higher to complete wave ((v)) of 3, followed by a wave 4 correction. Then the Index should do one final push to finish wave 5 of (1). After this, a broader correction from the April 7, 2025 low is expected in wave (2) before the uptrend resumes. As long as the 4823.5 pivot holds, any near-term pullbacks should find support in a 3, 7, or 11-swing pattern, paving the way for further gains. This analysis, rooted in Elliott Wave theory, suggests a bullish outlook for the SPX in the near term, provided key support levels remain intact.

S&P 500 (SPX) 60 Minute Elliott Wave Chart

SPX Video Analysis

https://www.youtube.com/watch?v=XQpDAUFG9i0

Trump Sparks Risk-On Sentiment Amid US-China Trade Talks Hints

US President Trump reignited risk-on sentiment across global markets on 8 May, coinciding with the announcement of a US–UK trade deal framework. During a White House press Q&A, he hinted at the possibility of lowering China tariffs if upcoming trade talks in Switzerland go well. He added, “You better go out and buy stock now,” echoing a similar statement from 9 April: “This is a great time to buy.”

US equities surged on the remarks, led by mega-cap tech and small-cap stocks. The Nasdaq 100 gained 1.9%, and the Russell 2000 jumped 2.5% intraday. However, a wave of late-session profit-taking trimmed gains, with the S&P 500 ending up 0.6%, down from an earlier 1.6% rise.

The renewed risk appetite also buoyed the US dollar. The US Dollar Index (DXY) rose 0.8%, climbing above its 20-day moving average, and extended its gains by another 0.2% in the current Asian session.

Safe-haven demand weakened, with gold (XAU/USD) falling for the second straight session, closing down 1.7% in the US. In today’s Asian trade, it initially dropped a further 0.9% to an intraday low of $3,275 but has since reversed course to post a 0.4% gain at the time of writing.

Asian equity markets opened mixed. Japan’s Nikkei 225 advanced 1.5%, Hong Kong’s Hang Seng Index posted a modest 0.2% gain, while China’s CSI 300 slipped 0.2%.

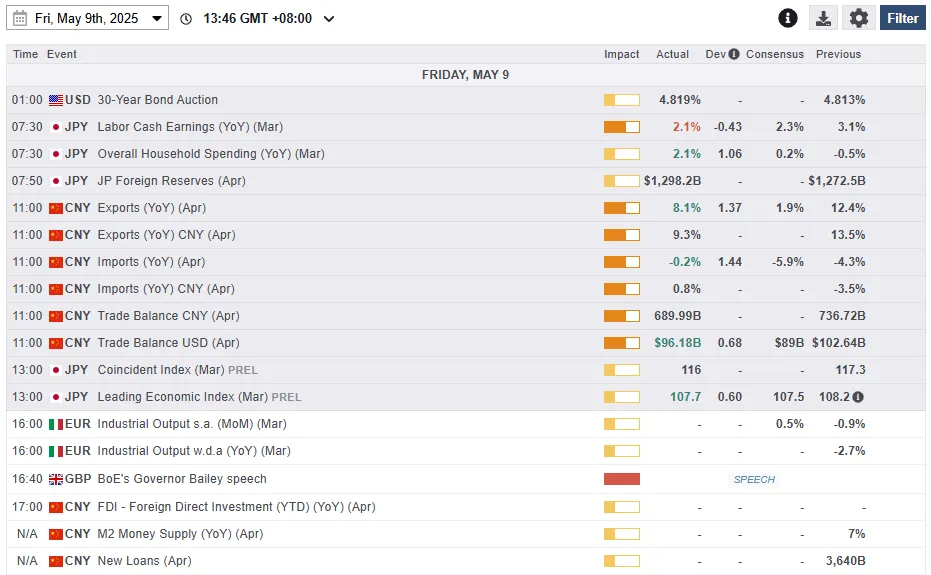

Economic data releases

Fig 1: Key data for today’s Asian mid-session (Source: MarketPulse)

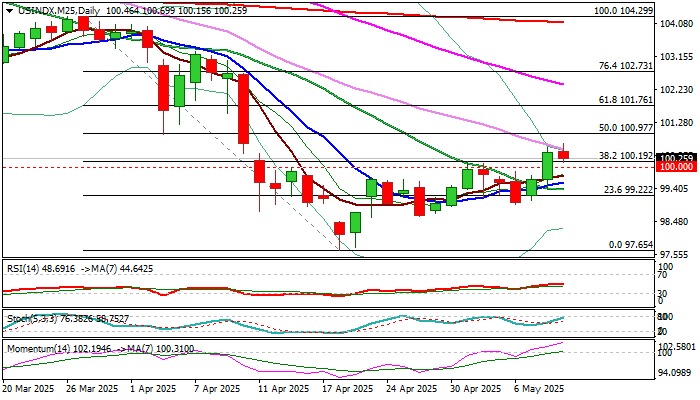

Chart of the day – Nasdaq 100 bulls may face a roadblock at the key 200-day MA

Fig 2: US Nasdaq 100 CFD Index minor trend as of 9 May 2025 (Source: TradingView)

Yesterday’s intraday swift rally on the US Nasdaq100 CFD Index (a proxy of the Nasdaq 100 E-mini futures), ex-post US President Trump’s “you better go out and buy stock now” remark, has now started to display signs of fatigue right below its key 200-day moving average.

The hourly RSI momentum indicator has flashed out a bearish divergence condition at its overbought region, which suggests yesterday’s US session bullish momentum has waned.

Watch the 20,250/390 medium-term pivotal resistance on the US Nasdaq100 CFD Index for a potential minor slide to expose near-term support of 19,600, and a break below it may expose the next intermediate supports at 19,345 and 19,020 (see Fig 2).

However, a clearance above 20,390 invalidates the bearish scenario for a further potential recovery towards the next intermediate resistances at 20,630 and 21,055.

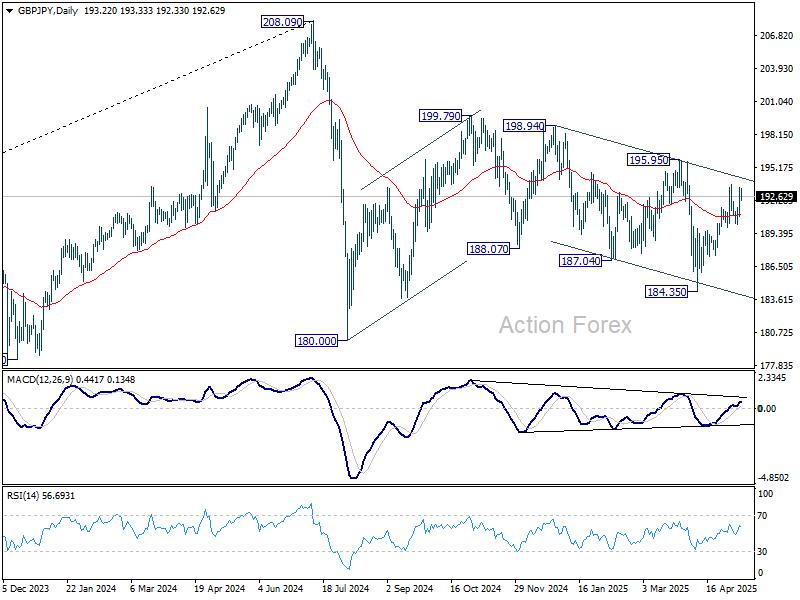

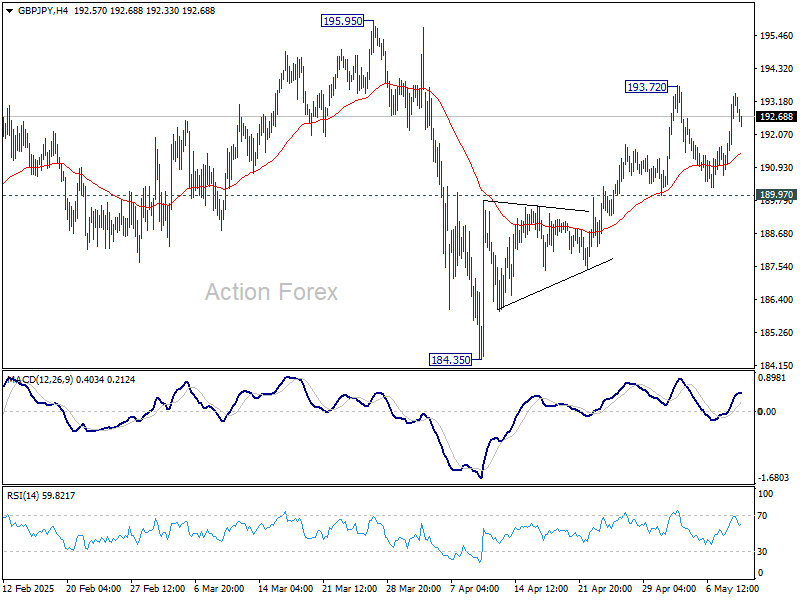

GBP/JPY Daily Outlook

Daily Pivots: (S1) 191.63; (P) 192.57; (R1) 194.20; More...

GBP/JPY is staying in range below 19372 and intraday bias remains neutral. With 189.97 support intact, further rise is favor. Above 193.72 will resume the rally from 184.35 and target 195.95 resistance next. However, firm break of 189.97 will turn bias back to the downside for deeper decline.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.