Sample Category Title

EUR/AUD Weekly Outlook

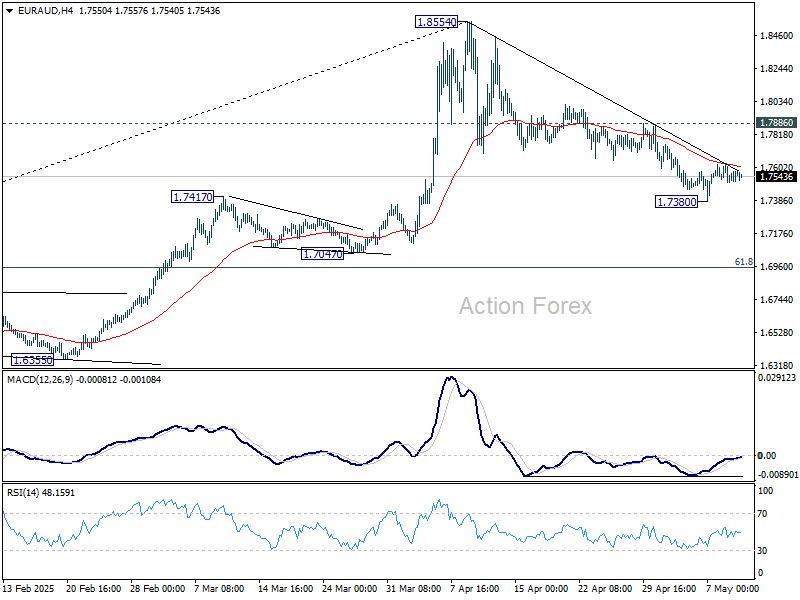

EUR/AUD edged lower to 1.7380 last week but recovered after hitting 55 D EMA (now at 1.7430). Initial bias remains neutral this week first. On the upside, firm break of 1.7886 resistance will argue that fall from 1.8553 has completed as a correction at 1.7380. Intraday bias will be turned back to the upside for retesting 1.8554. However, sustained trading below 55 D EMA will target 61.8% retracement at 1.6953 next.

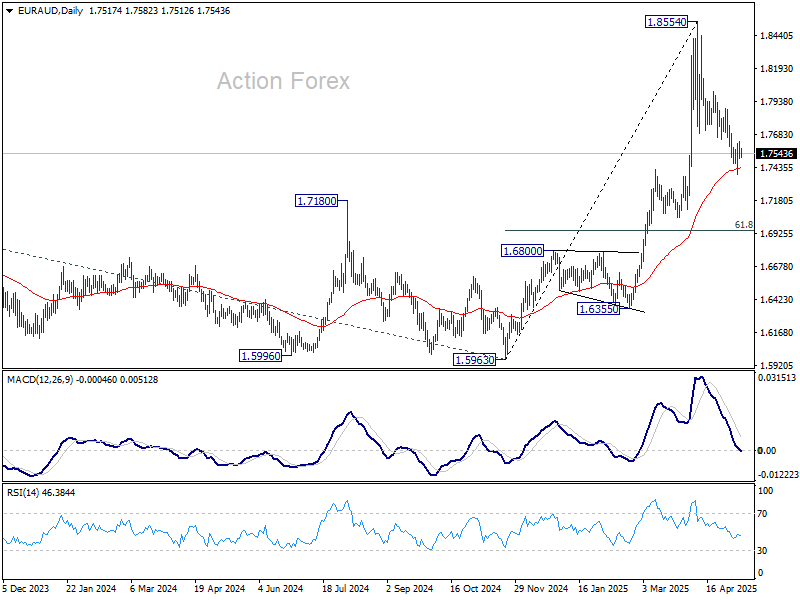

In the bigger picture, as long as 1.7062 resistance turned support (2023 high) holds, up trend from up trend from 1.4281 (2022 low) should still be in progress. Break of 1.8554 will target 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. However, sustained break of 1.7062 will confirm medium term topping and bring deeper fall back to 1.5963 support.

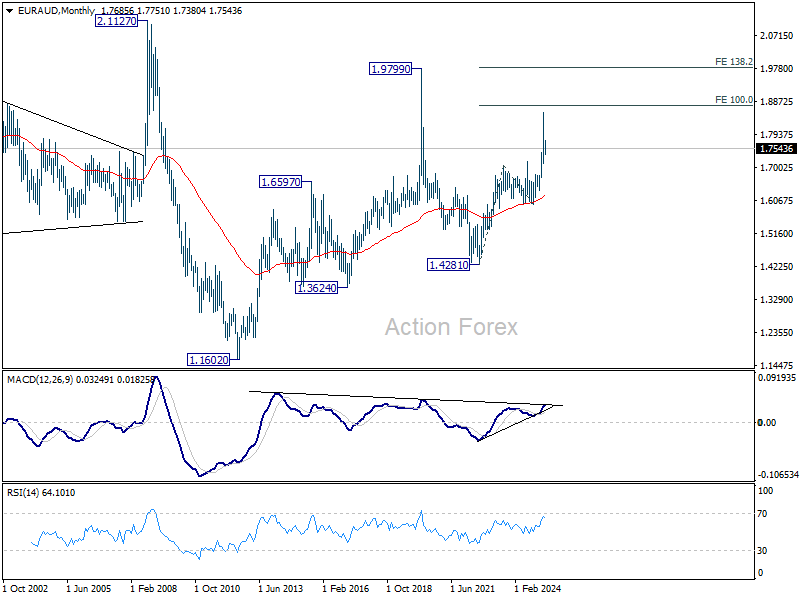

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6199) holds, this second leg could still extend higher. However, firm break of the above mention 1.8744 projection level with strong momentum will argue that it's indeed resuming the up trend from 1.1602 (2012 low).

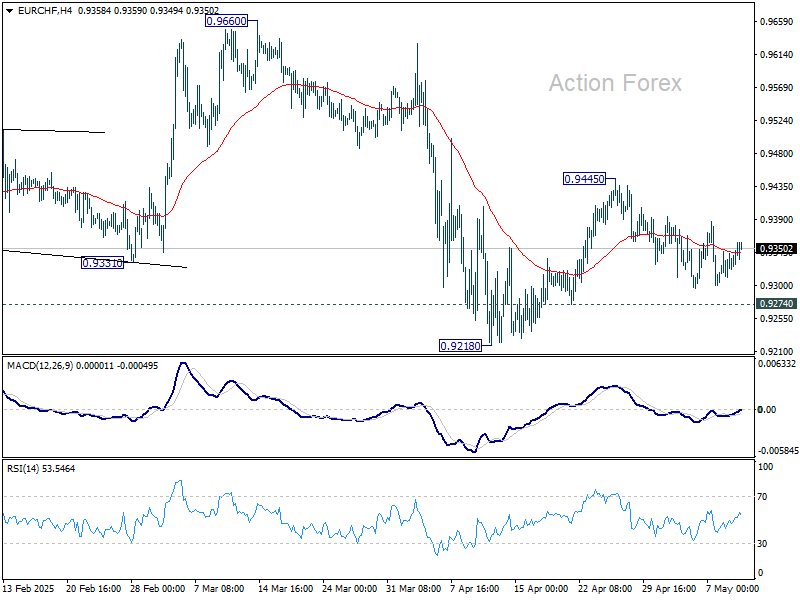

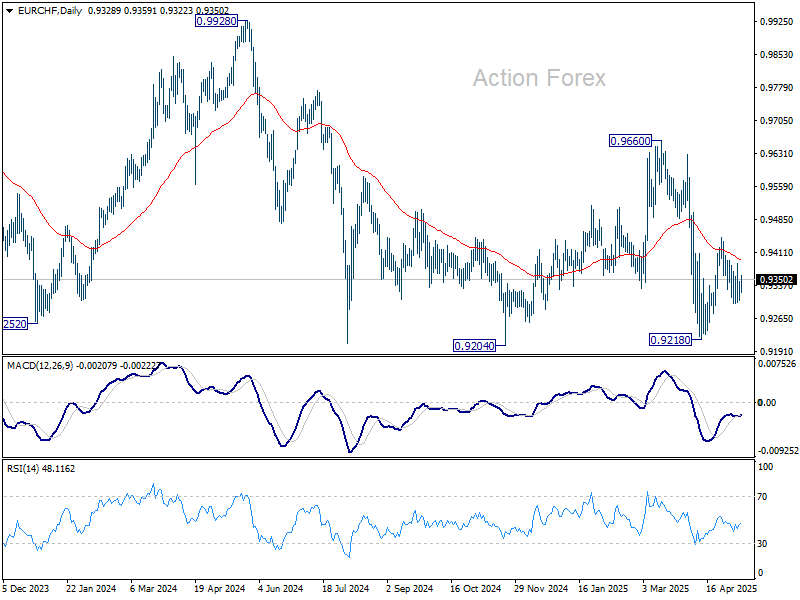

EUR/CHF Weekly Outlook

EUR/CHF's corrective pattern from 0.9445 continued last week. Initial bias stays neutral this week first. On the upside, above 0.9445 will resume the rebound from 0.9218, either as a corrective move or the third leg of the pattern from 0.9204. However, break of 0.9274 will suggest that that recovery has completed, and bring retest of 0.9204/18 support zone.

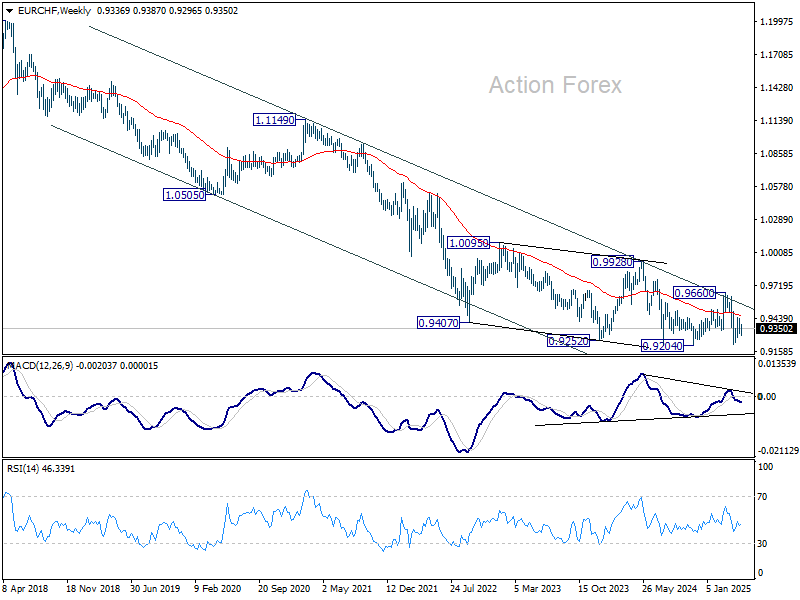

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9548) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.

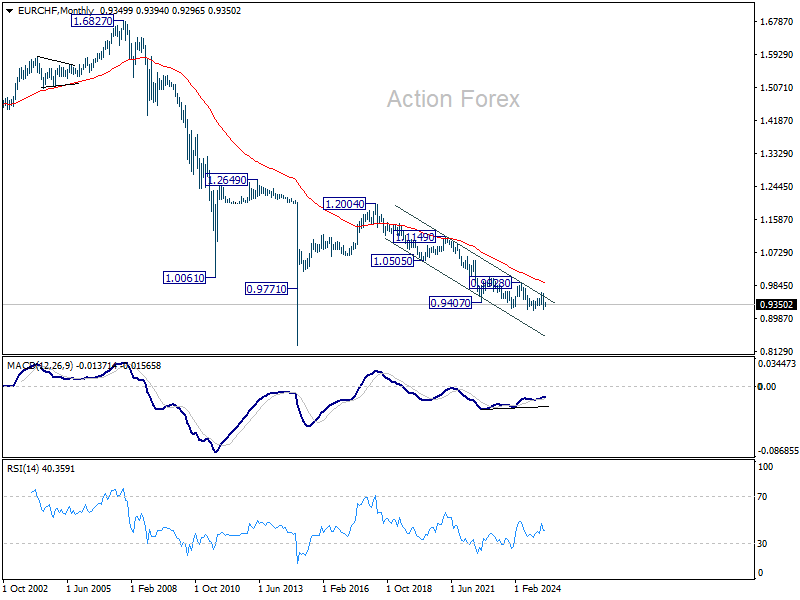

In the long term picture, overall long term down trend is still in force in EUR/CHF. Outlook will continue to stay bearish as long as 55 M EMA (now at 0.9919) holds.

Summary 5/12 – 5/16

Monday, May 12, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Apr | 2.80% | 2.80% |

| 23:50 | JPY | Current Account (JPY) Mar | 2.42T | 2.32T |

| 23:50 | JPY | Trade Balance - BOP Basis Mar | �712.9B | |

| 05:00 | JPY | Eco Watchers Survey: Current Apr | 44.5 | 45.1 |

| 23:50 | JPY | BoJ Summary of Opinions | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Apr | 0.60% | 0.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Apr | |

| Forecast: 2.80% | Previous: 2.80% | ||

| 23:50 | JPY | Current Account (JPY) Mar | |

| Forecast: 2.42T | Previous: 2.32T | ||

| 23:50 | JPY | Trade Balance - BOP Basis Mar | |

| Forecast: | Previous: �712.9B | ||

| 05:00 | JPY | Eco Watchers Survey: Current Apr | |

| Forecast: 44.5 | Previous: 45.1 | ||

| 23:50 | JPY | BoJ Summary of Opinions | |

| Forecast: | Previous: | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Apr | |

| Forecast: 0.60% | Previous: 0.80% | ||

Tuesday, May 13, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence May | -6% | |

| 01:30 | AUD | NAB Business Conditions Apr | 4 | |

| 01:30 | AUD | NAB Business Confidence Apr | -3 | |

| 06:00 | GBP | Claimant Count Change Apr | 22.3K | 18.7K |

| 06:00 | GBP | ILO Unemployment Rate (3M) Mar | 4.50% | 4.40% |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Mar | 5.20% | 5.60% |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Mar | 5.90% | |

| 09:00 | EUR | Germany ZEW Economic Sentiment May | 9.8 | -14 |

| 09:00 | EUR | Germany ZEW Current Situation May | -77 | -81.2 |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment May | -4.4 | -18.5 |

| 10:00 | USD | NFIB Business Optimism Index Apr | 94.5 | 97.4 |

| 12:30 | USD | CPI M/M Apr | 0.30% | -0.10% |

| 12:30 | USD | CPI Y/Y Apr | 2.40% | 2.40% |

| 12:30 | USD | CPI Core M/M Apr | 0.30% | 0.10% |

| 12:30 | USD | CPI Core Y/Y Apr | 2.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence May | |

| Forecast: | Previous: -6% | ||

| 01:30 | AUD | NAB Business Conditions Apr | |

| Forecast: | Previous: 4 | ||

| 01:30 | AUD | NAB Business Confidence Apr | |

| Forecast: | Previous: -3 | ||

| 06:00 | GBP | Claimant Count Change Apr | |

| Forecast: 22.3K | Previous: 18.7K | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) Mar | |

| Forecast: 4.50% | Previous: 4.40% | ||

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Mar | |

| Forecast: 5.20% | Previous: 5.60% | ||

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Mar | |

| Forecast: | Previous: 5.90% | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment May | |

| Forecast: 9.8 | Previous: -14 | ||

| 09:00 | EUR | Germany ZEW Current Situation May | |

| Forecast: -77 | Previous: -81.2 | ||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment May | |

| Forecast: -4.4 | Previous: -18.5 | ||

| 10:00 | USD | NFIB Business Optimism Index Apr | |

| Forecast: 94.5 | Previous: 97.4 | ||

| 12:30 | USD | CPI M/M Apr | |

| Forecast: 0.30% | Previous: -0.10% | ||

| 12:30 | USD | CPI Y/Y Apr | |

| Forecast: 2.40% | Previous: 2.40% | ||

| 12:30 | USD | CPI Core M/M Apr | |

| Forecast: 0.30% | Previous: 0.10% | ||

| 12:30 | USD | CPI Core Y/Y Apr | |

| Forecast: | Previous: 2.80% | ||

Wednesday, May 14, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Apr | 4.00% | 4.20% |

| 01:30 | AUD | Wage Price Index Q/Q Q1 | 0.80% | 0.70% |

| 06:00 | EUR | Germany CPI M/M Apr F | 0.40% | 0.40% |

| 06:00 | EUR | Germany CPI Y/Y Apr F | 2.10% | 2.10% |

| 12:30 | CAD | Building Permits M/M Mar | 1.00% | 2.90% |

| 14:30 | USD | Crude Oil Inventories | -2.0M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Apr | |

| Forecast: 4.00% | Previous: 4.20% | ||

| 01:30 | AUD | Wage Price Index Q/Q Q1 | |

| Forecast: 0.80% | Previous: 0.70% | ||

| 06:00 | EUR | Germany CPI M/M Apr F | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 06:00 | EUR | Germany CPI Y/Y Apr F | |

| Forecast: 2.10% | Previous: 2.10% | ||

| 12:30 | CAD | Building Permits M/M Mar | |

| Forecast: 1.00% | Previous: 2.90% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -2.0M | ||

Thursday, May 15, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | AUD | Consumer Inflation Expectations May | 4.20% | |

| 01:30 | AUD | Employment Change Apr | 20.9K | 32.2K |

| 01:30 | AUD | Unemployment Rate Apr | 4.10% | 4.10% |

| 06:00 | JPY | Machine Tool Orders Y/Y Apr | 11.40% | |

| 06:00 | GBP | GDP Q/Q Q1 P | 0.60% | 0.10% |

| 06:00 | GBP | GDP M/M Mar | 0.00% | 0.50% |

| 06:00 | GBP | Manufacturing Production M/M Mar | -0.80% | 2.20% |

| 06:00 | GBP | Manufacturing Production Y/Y Mar | 0.30% | |

| 06:00 | GBP | Industrial Production M/M Mar | -0.60% | 1.50% |

| 06:00 | GBP | Industrial Production Y/Y Mar | 0.10% | |

| 06:00 | GBP | Goods Trade Balance (GBP) Mar | -19.7B | -20.8B |

| 06:30 | CHF | Producer and Import Prices M/M Apr | 0.20% | 0.10% |

| 06:30 | CHF | Producer and Import Prices Y/Y Apr | -0.10% | |

| 09:00 | EUR | Eurozone GDP Q/Q Q1 P | 0.40% | 0.40% |

| 09:00 | EUR | Eurozone Employment Change Q/Q Q1 P | 0.10% | 0.10% |

| 09:00 | EUR | Eurozone Industrial Production M/M Mar | 1.70% | 1.10% |

| 12:15 | CAD | Housing Starts Apr | 234K | 214K |

| 12:30 | CAD | Manufacturing Sales M/M Mar | -1.90% | 0.20% |

| 12:30 | CAD | Wholesale Sales M/M Mar | -0.30% | 0.30% |

| 12:30 | USD | Initial Jobless Claims (May 9) | 230K | 228K |

| 12:30 | USD | Retail Sales M/M Apr | 0.10% | 1.50% |

| 12:30 | USD | Retail Sales ex Autos M/M Apr | 0.30% | 0.50% |

| 12:30 | USD | PPI M/M Apr | 0.20% | -0.40% |

| 12:30 | USD | PPI Y/Y Apr | 2.70% | |

| 12:30 | USD | PPI Core M/M Apr | 0.30% | -0.10% |

| 12:30 | USD | PPI Core Y/Y Apr | 3.30% | |

| 12:30 | USD | Empire State Manufacturing May | -7.1 | -8.1 |

| 12:30 | USD | Philadelphia Fed Survey May | -8.5 | -26.4 |

| 13:15 | USD | Industrial Production M/M Apr | 0.10% | -0.30% |

| 13:15 | USD | Capacity Utilization Apr | 77.80% | 77.80% |

| 14:00 | USD | Business Inventories Mar | 0.20% | 0.20% |

| 14:00 | USD | NAHB Housing Market Index May | 41 | 40 |

| 14:30 | USD | Natural Gas Storage | 104B | |

| 22:30 | NZD | Business NZ PMI Apr | 53.2 | |

| 23:50 | JPY | GDP Q/Q Q1 P | -0.10% | 0.70% |

| 23:50 | JPY | GDP Deflator Y/Y Q1 P | 3.20% | 2.90% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | AUD | Consumer Inflation Expectations May | |

| Forecast: | Previous: 4.20% | ||

| 01:30 | AUD | Employment Change Apr | |

| Forecast: 20.9K | Previous: 32.2K | ||

| 01:30 | AUD | Unemployment Rate Apr | |

| Forecast: 4.10% | Previous: 4.10% | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Apr | |

| Forecast: | Previous: 11.40% | ||

| 06:00 | GBP | GDP Q/Q Q1 P | |

| Forecast: 0.60% | Previous: 0.10% | ||

| 06:00 | GBP | GDP M/M Mar | |

| Forecast: 0.00% | Previous: 0.50% | ||

| 06:00 | GBP | Manufacturing Production M/M Mar | |

| Forecast: -0.80% | Previous: 2.20% | ||

| 06:00 | GBP | Manufacturing Production Y/Y Mar | |

| Forecast: | Previous: 0.30% | ||

| 06:00 | GBP | Industrial Production M/M Mar | |

| Forecast: -0.60% | Previous: 1.50% | ||

| 06:00 | GBP | Industrial Production Y/Y Mar | |

| Forecast: | Previous: 0.10% | ||

| 06:00 | GBP | Goods Trade Balance (GBP) Mar | |

| Forecast: -19.7B | Previous: -20.8B | ||

| 06:30 | CHF | Producer and Import Prices M/M Apr | |

| Forecast: 0.20% | Previous: 0.10% | ||

| 06:30 | CHF | Producer and Import Prices Y/Y Apr | |

| Forecast: | Previous: -0.10% | ||

| 09:00 | EUR | Eurozone GDP Q/Q Q1 P | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 09:00 | EUR | Eurozone Employment Change Q/Q Q1 P | |

| Forecast: 0.10% | Previous: 0.10% | ||

| 09:00 | EUR | Eurozone Industrial Production M/M Mar | |

| Forecast: 1.70% | Previous: 1.10% | ||

| 12:15 | CAD | Housing Starts Apr | |

| Forecast: 234K | Previous: 214K | ||

| 12:30 | CAD | Manufacturing Sales M/M Mar | |

| Forecast: -1.90% | Previous: 0.20% | ||

| 12:30 | CAD | Wholesale Sales M/M Mar | |

| Forecast: -0.30% | Previous: 0.30% | ||

| 12:30 | USD | Initial Jobless Claims (May 9) | |

| Forecast: 230K | Previous: 228K | ||

| 12:30 | USD | Retail Sales M/M Apr | |

| Forecast: 0.10% | Previous: 1.50% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Apr | |

| Forecast: 0.30% | Previous: 0.50% | ||

| 12:30 | USD | PPI M/M Apr | |

| Forecast: 0.20% | Previous: -0.40% | ||

| 12:30 | USD | PPI Y/Y Apr | |

| Forecast: | Previous: 2.70% | ||

| 12:30 | USD | PPI Core M/M Apr | |

| Forecast: 0.30% | Previous: -0.10% | ||

| 12:30 | USD | PPI Core Y/Y Apr | |

| Forecast: | Previous: 3.30% | ||

| 12:30 | USD | Empire State Manufacturing May | |

| Forecast: -7.1 | Previous: -8.1 | ||

| 12:30 | USD | Philadelphia Fed Survey May | |

| Forecast: -8.5 | Previous: -26.4 | ||

| 13:15 | USD | Industrial Production M/M Apr | |

| Forecast: 0.10% | Previous: -0.30% | ||

| 13:15 | USD | Capacity Utilization Apr | |

| Forecast: 77.80% | Previous: 77.80% | ||

| 14:00 | USD | Business Inventories Mar | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 14:00 | USD | NAHB Housing Market Index May | |

| Forecast: 41 | Previous: 40 | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 104B | ||

| 22:30 | NZD | Business NZ PMI Apr | |

| Forecast: | Previous: 53.2 | ||

| 23:50 | JPY | GDP Q/Q Q1 P | |

| Forecast: -0.10% | Previous: 0.70% | ||

| 23:50 | JPY | GDP Deflator Y/Y Q1 P | |

| Forecast: 3.20% | Previous: 2.90% | ||

Friday, May 16, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 03:00 | NZD | RBNZ Inflation Expectations Q2 | 2.06% | |

| 04:30 | JPY | Industrial Production M/M Mar | -1.10% | -1.10% |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Mar | 17.5B | 21.0B |

| 12:30 | USD | Housing Starts Apr | 1.37M | 1.32M |

| 12:30 | USD | Building Permits Apr | 1.45M | 1.48M |

| 12:30 | USD | Import Price Index M/M Apr | -0.40% | -0.10% |

| 14:00 | USD | UoM Consumer Sentiment May P | 53 | 52.2 |

| 14:00 | USD | UoM Inflation Expectations May P | 6.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 03:00 | NZD | RBNZ Inflation Expectations Q2 | |

| Forecast: | Previous: 2.06% | ||

| 04:30 | JPY | Industrial Production M/M Mar | |

| Forecast: -1.10% | Previous: -1.10% | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Mar | |

| Forecast: 17.5B | Previous: 21.0B | ||

| 12:30 | USD | Housing Starts Apr | |

| Forecast: 1.37M | Previous: 1.32M | ||

| 12:30 | USD | Building Permits Apr | |

| Forecast: 1.45M | Previous: 1.48M | ||

| 12:30 | USD | Import Price Index M/M Apr | |

| Forecast: -0.40% | Previous: -0.10% | ||

| 14:00 | USD | UoM Consumer Sentiment May P | |

| Forecast: 53 | Previous: 52.2 | ||

| 14:00 | USD | UoM Inflation Expectations May P | |

| Forecast: | Previous: 6.50% | ||

Markets Weekly Outlook – US-China Trade Talks & Global Economic Data

- Market sentiment improves amid US-China trade talk optimism, despite concerns over tariff impacts on the global economy.

- Key economic data releases are expected across Asia, Europe, and the US, with a focus on inflation and retail sales.

- The US Dollar Index remains a focal point, showing a grind higher and influenced by trade talk developments.

- Federal Reserve's stance on interest rates and potential inflation increases due to tariffs are closely monitored.

Wall Street indexes are looking to finish the week with gains after a shaky start earlier in the week. Improved sentiment and the pending US-China meeting over a potential trade deal this weekend has kept market participants on the optimistic side.

Companies continue to pull their earnings forecasts this week on the back of a number of uncertainties. This has led to US equities being a bit sluggish this week, as even though market participants are optimistic there remains a host of challenges that need to be overcome. Tariff clarity may also allow companies to gain a better sense of how their businesses may be affected moving forward.

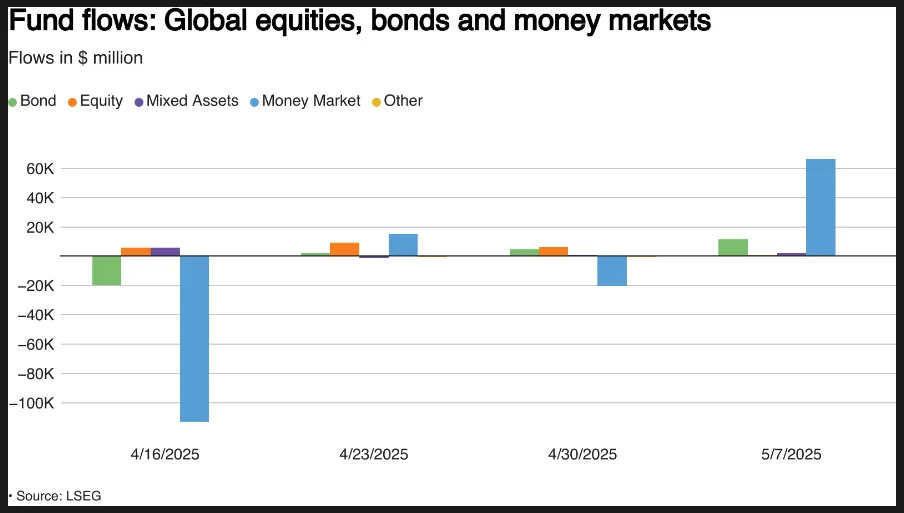

Despite the improving sentiment Global equity funds saw their lowest weekly inflows in four weeks, ending May 7, as worries over tariffs' impact on the global economy and the outcome of U.S.-China trade talks weighed on investors.

LSEG Lipper data shows that investors purchased just $856 million in global equity funds that week, a sharp drop from the $6.13 billion invested the previous week. European equity funds remained popular, drawing $12.81 billion in net inflows for the fourth week in a row.

Asian funds also attracted $3.32 billion in net inflows. However, U.S. equity funds faced net outflows for the fourth straight week, losing $16.22 billion during the same period.

Source: LSEG

Gold enjoyed a rollercoaster week breaching the $3400/oz handle on Tuesdays before edging lower for the rest of the week to trade around the $3340/oz mark at the time of writing.

Oil prices started the week under pressure with a significant gap to the downside after the OPEC + meeting last weekend. Rumors began to swirl that Saudi Arabia would be okay with lower oil prices and that the group may look to be more aggressive with increasing its production and output.

Thanks to the improving sentiment Oil prices did edge higher for the majority of the week. Brent is trading higher for the week as it looks to snap a two week losing run which sent Brent to fresh lows around the 58.60 a barrel mark.

On the FX front, the US Dollar regained its bullish momentum on Thursday but has struggled to keep up the momentum on Friday. This has left the US Dollar index largely flat for the week.

The Dollar's Friday weakness has helped the likes of EUR/USD and GBP/USD recover some of Thursday's losses. The Swiss Franc remains one to watch as Swissie strength continues to be of concern to the Business community which is adding pressure on the Central Bank.

Markets will shift their attention to trade talks between the US and China this weekend. On Friday US President Trump posted on TruthSocial saying he thinks 80% tariffs on China would be fair. This was followed by the President saying that it's up to Treasury Secretary Bessent.

President Trump's trade advisor Peter Navarro confirmed what we already expect, this weekend will be an interesting one for global markets.

The Week Ahead: US-China trade talks to drive sentiment

The week ahead has several important data releases lined up. However, with US-China talks taking place over the weekend and the first trade deal already completed, markets may shift their attention to tariff updates, which could take the spotlight away from the economic data.

Asia Pacific Markets

Japan's economy is set to shrink by 0.1% in the first quarter of 2025, down from a 0.6% rise in the last quarter of 2024. Household spending and more foreign tourists are boosting private consumption, but low external demand is holding growth back. The impact of rushing exports before tariffs has been smaller for Japan compared to other big exporters. Imports have shown a recovery. Due to weak growth, the Bank of Japan is likely to hold off on any rate hikes for now.

China's inflation data for April will be shared this weekend, and consumer prices are expected to stay at -0.1% year-on-year, the same as March. Producer prices are likely to remain negative for the 31st month in a row. Deflation could get worse because of tariffs, forcing exporters to find new markets. China will also release its April credit data in the coming week. Credit growth has been improving this year, but April’s numbers are unlikely to reflect the latest measures by the People’s Bank of China to ease monetary policy. More time will be needed for the effects to be felt and transmitted through the data.

Europe + UK + US

The Federal Reserve has made it clear they’re not rushing to lower interest rates. They acknowledge that trade uncertainty could lead to both higher unemployment and inflation. April’s inflation data, due next week, is expected to show that inflation remains high. There may also be signs of early price increases as tariffs start to impact costs. By June, these price hikes could become more noticeable, as it takes time for goods to be shipped, stored, and finally sold in stores or online.

Retail sales are in focus this week. March was strong as people bought big-ticket items early, fearing tariff-related price hikes. This may continue in April for car sales, but worries about inflation, job security, and falling wealth could hurt non-essential spending. Key data like the Michigan sentiment index and industrial production are also due.

If we travel over the pond to the UK, the job market is cooling but not weakening significantly after recent tax hikes. Last month’s drop in payrolls will likely be revised higher. Unemployment is expected to rise, though the data isn’t always reliable. Wage growth should slow, mainly due to earlier high comparisons, with pay pressures easing later this year.

February’s GDP jumped 0.5%, and even with a possible dip in March, first-quarter growth looks solid. This surge is partly due to volatile manufacturing data. Growth in the second quarter is likely to slow but should remain steady, helped by government spending.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Week - US Dollar Index (DXY)

This week's focus remains on the US Dollar Index.

The index which finally closed above the psychological 100.00 level last week looked on course for a positive close heading into Friday.

The index did not push on though and remains above the 100.00 mark at the time of writing but has pulled back significantly from the weekly high at 100.61 which is a resistance area.

The DXY has been making its way higher on a daily timeframe printing higher highs and higher lows but it has been a grind to say the least.

Positive developments on US-China trade talks could lead to a significant rally to the upside and could serve as the jolt in the arm the US Dollar has been waiting for.

Immediate resistance rests at 100.61 before the 101.80 and 102.16 levels come into focus.

If a deeper pullback takes place, support rests at 100.00 before the 99.57 and 99.00 handle comes into focus.

US Dollar Index (DXY) Daily Chart - May 9, 2025

Source: TradingView.Com (click to enlarge)

The Weekly Bottom Line: Mr. Carney Goes to Washington

Canadian Highlights

- Canadian monthly employment data are notoriously volatile, but the trend since January has been toward softer job creation and a rising unemployment rate.

- Data show an increased share of Canadian goods heading to the U.S. in March were traded under the CUSMA agreement, avoiding tariffs.

- Softening growth and some positive developments on trade limit the upside risk to inflation, opening the door for the Bank of Canada to cut its policy rate.

U.S. Highlights

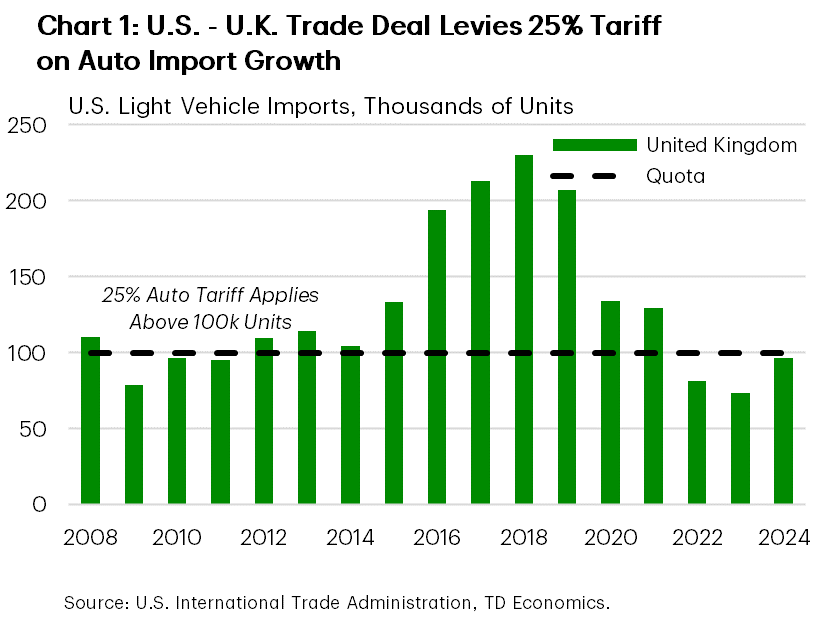

- The U.S. announced a trade deal with the U.K. to reduce several product-specific tariffs, although the 10% reciprocal tariff faced by the U.K. remained in place.

- Formal trade negotiations with China are expected to begin this weekend in Switzerland, as the third largest trading partner of the U.S. remains subject to 145% tariffs.

- The Federal Reserve left interest rates unchanged for the third time this year. Chair Powell noted that it would take time to discern the effects of tariffs on the economy.

Canada – Mr. Carney Goes to Washington

After winning the election last week, Prime Minster Carney travelled to Washington to meet President Trump. The bar was relatively low heading into the meeting, so it was notable for simply being unremarkable. The timing was appropriate though, as March trade data showcased the key economic issue facing the incoming Canadian government – how to diversify trade when there is a superpower next door.

Trade discussions with our southern neighbour are likely to take time and involve renegotiating parts of the CUSMA trade agreement signed in 2018. On the agreement, policymakers were likely keenly aware of President Trump calling it “great for all countries”, before noting that it can be renegotiated or terminated. For the outlook, as long as the uncertainty about tariffs and trade agreements persists, it will hang like a cloud over the economy.

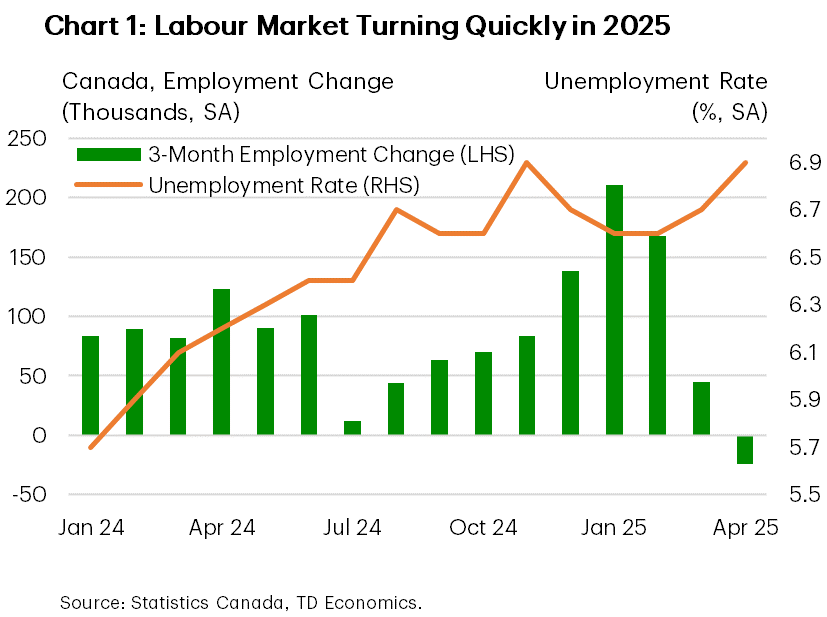

The deceleration is apparent in the labour market. The economy added a modest 7k jobs in April, and those gains were largely thanks to temporary federal election jobs. The private sector has shed jobs for two months in a row. Canadian monthly employment data are notoriously volatile, but the trend has been toward softer job creation since the escalation in trade tensions. As employment growth has petered out, the unemployment rate has steadily crept higher, reaching 6.9% in April. The unemployment rate is now matching its high from November 2024, before a burst of late-year hiring showed some temporary relief for the labour market (Chart 1). Pull the history back further and, excluding the pandemic period, the 6.9% unemployment rate is the highest since January of 2017. It is also apparent that tariffs are behind the deceleration in the labour market, with trade-exposed sectors behind the recent slowdown in hiring - the manufacturing sector has lost 43k jobs over the past three months.

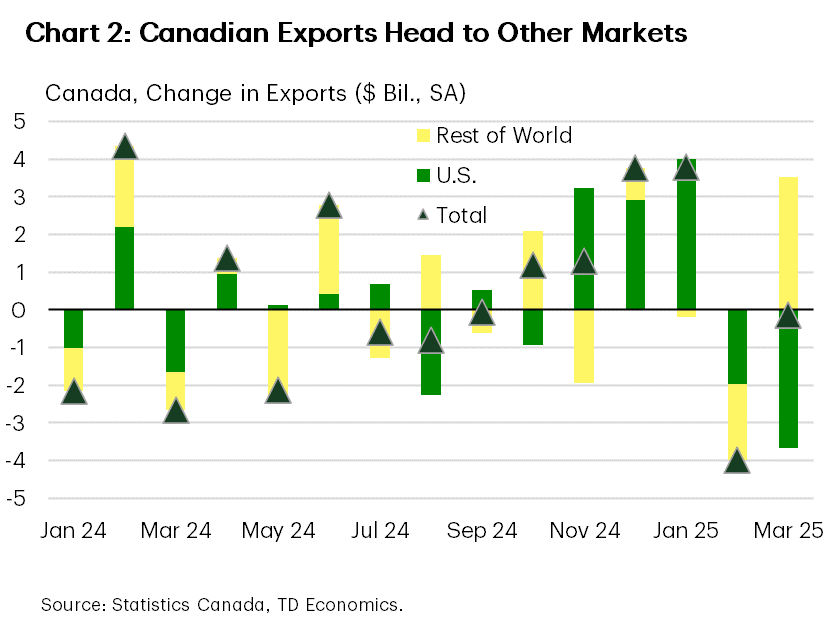

Looking ahead, the challenges are apparent. Part of the lift to first quarter activity was due to American firms attempting to front-run tariffs by stockpiling imports ahead of the new duties. Canadian exports to the U.S. grew nearly 7% per month between November and January, before falling nearly 10% through March once they were applied. However, two silver linings emerged in the March data. First, the steep decline in exports to the U.S. was offset by a rise in shipments to the rest of the world (Chart 2). Secondly, roughly 50% of Canadian goods heading to the U.S. were CUSMA compliant in March, up from the 38% averaged in 2024 and 40% last March. The increased compliance means avoiding the 25% tariff and reducing the economic impact. Nonetheless, as long as the uncertainty about the trade relationship persists, firms are understandably cautious. With the malaise hanging over the economy its unlikely things will turn a corner soon.

Faced with the prospect of domestic activity continuing to soften, we see the Bank of Canada having an opening to cut its policy rate by 25 basis points in June, bringing it down to 2.5%. The risk of higher inflation remains, but there are a few reasons for optimism that the worst-case scenario won’t materialize. First, a greater share of Canadian products have become CUSMA compliant (offsetting the risk of supply chain snarls), retaliatory tariffs have been restrained, and a stronger dollar offset rising cost pressures.

U.S. – The First of Many?

The first full week of May looked like it may provide a modest respite for financial markets, as economic data releases were limited and the Federal Reserve’s decision on Wednesday was short on surprises. However, this proved to be short-lived as the White House announced a preliminary trade deal with the U.K. on Thursday. The S&P 500 ended the week roughly unchanged at time of writing, while the 10-year U.S. Treasury yield rose 4 basis points to 4.36%.

The preliminary trade deal between the U.S. and U.K. (see here), included a full exemption on Section 232 steel and aluminum tariffs for the U.K., in addition to an annual exemption on automotive tariffs for the first 100k units imported (Chart 1). The market reaction to the agreement was relatively tame, as the 10% baseline reciprocal tariff remained in effect. The President noted that this would likely be the global floor for reciprocal tariffs, and that other nations may see levels above this even after negotiations have concluded. It is unclear whether this would be acceptable to other nations. If they take a harder stance during upcoming negotiations, it could delay a broader resolution to the current state of elevated trade tensions.

The EU also outlined a list of goods this week that would be subject to retaliatory tariffs. The list covers nearly a third of U.S. exports to the region. These tariffs would be levied if negotiations do not result in “a mutually beneficial outcome and the removal of U.S. tariffs”. Chinese officials also called on the U.S. to “be prepared to correct its erroneous actions and cancel its unilateral tariff increases”, ahead of the planned start of formal negotiations with the U.S. this weekend. Early on Friday the President floated the idea of lowering the tariff rate on China to 80%, but no final decision has been made. With less than two months until the 90-day suspension of U.S. reciprocal tariffs expires and dozens of deals yet to be made, time will remain of the essence on the trade front in the weeks ahead.

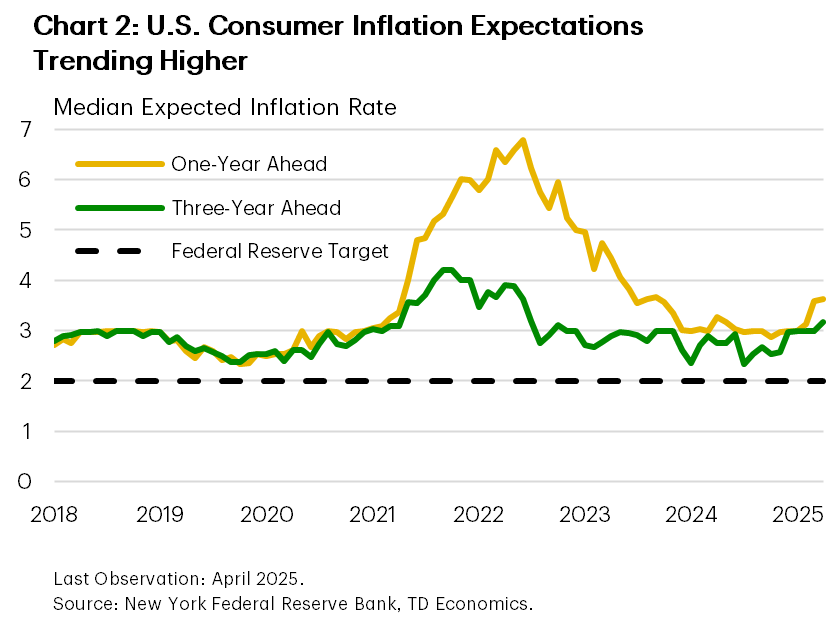

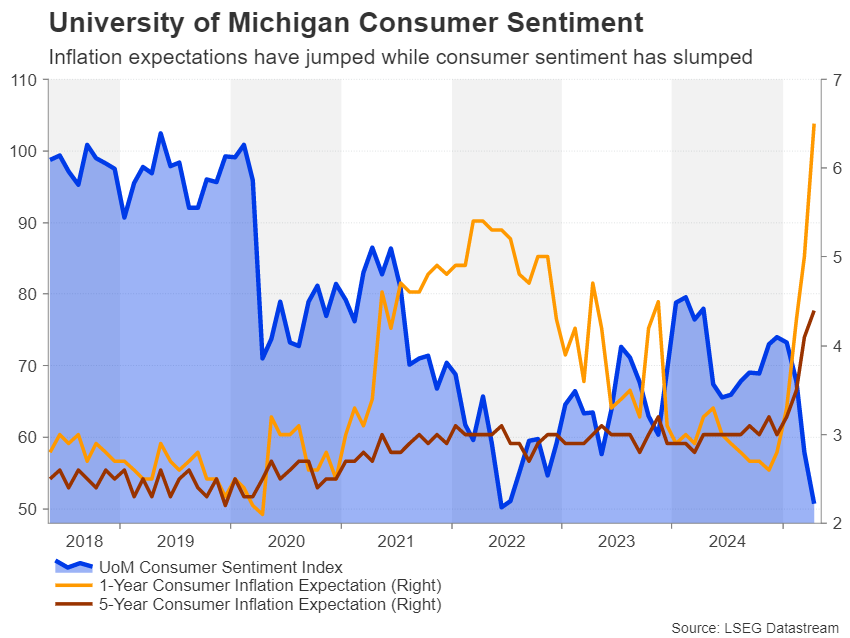

The Federal Reserve pointed to the clouds hanging over the economic outlook in its rate decision on Wednesday. It was the third meeting in a row where the FOMC left the federal funds rate unchanged. During his press conference, Chair Powell highlighted the likelihood that current trade policies would push the unemployment rate and inflation to deviate from the Fed’s dual mandate. However, he also noted that uncertainty remains elevated with respect to the magnitude of the deviation, meriting caution in monetary policy decisions at this time. With survey-based measures of inflation expectations remaining elevated in April (Chart 2), the Fed’s caution would appear prudent at this time.

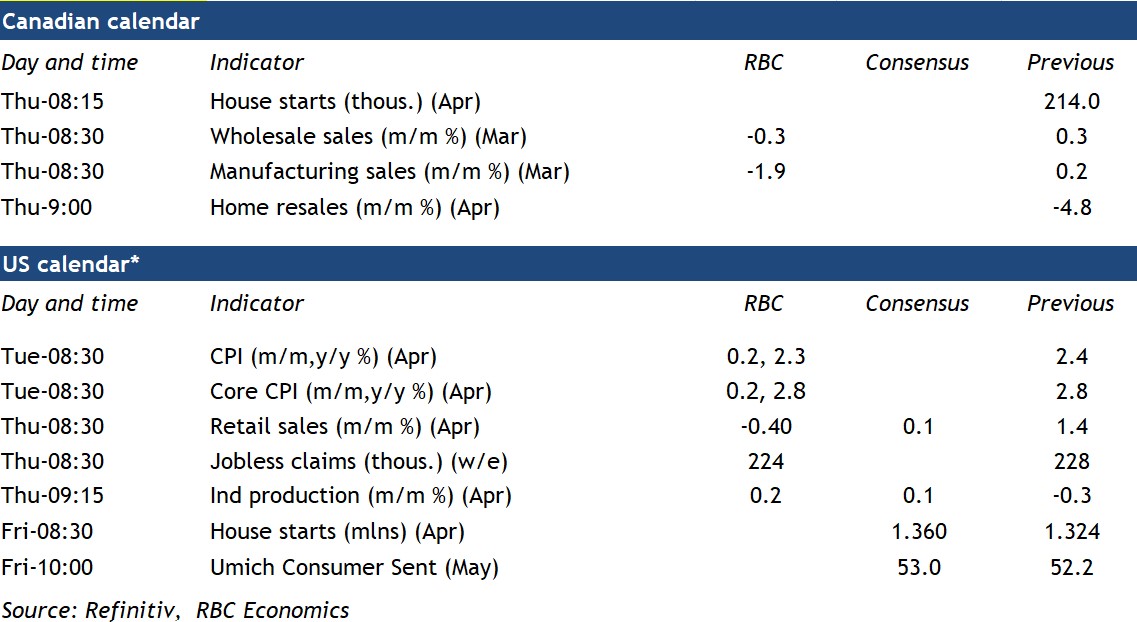

Next week, we’ll receive a first look at inflation data for April with the CPI data release, in addition to April retail sales. Although neither is expected to be materially influenced by tariff impacts yet, they will provide a pulse check on consumer and price trends. Also on the docket for next week is the reconciliation bill markup for the House Ways & Means Committee, which could provide insight on the specific tax cut provisions being considered by Congress. Although fiscal policy may not fully offset the influence of tariffs on the economy this year, it could help to prevent a more material slowdown.

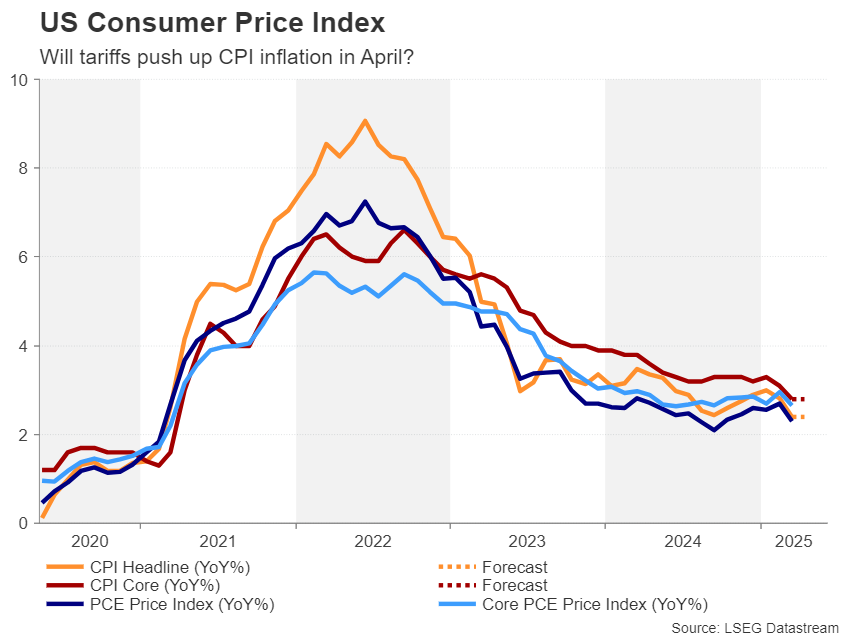

U.S. Consumer Prices in April in Focus for Early Tariff Impact

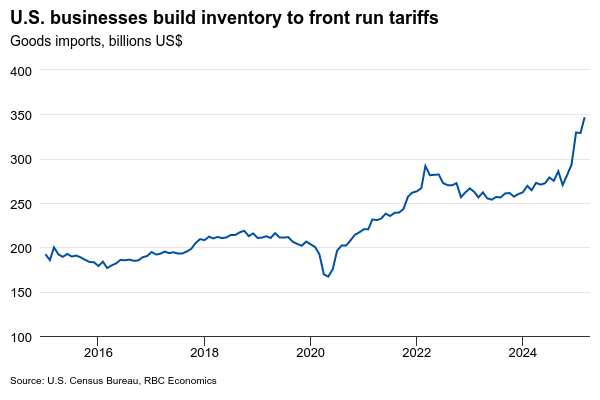

U.S. tariffs rose sharply in early April, but a ramp up in Q1 inventories by businesses is expected to delay the full impact on consumer prices. Q1 imports surged higher, in part as businesses built up inventories in anticipation of disruptions to satisfy near term consumer demand and avoid raising prices.

The core U.S. Consumer Price Index (excluding food and energy) is expected to have stayed at 2.8% year-over-year in April, as rent inflation broadly continues to moderate. Energy inflation likely dropped further below year ago levels despite April's slight gasoline price increase. Overall, headline CPI likely eased to 2.3% in April from March's 2.4%.

Still, the details will be closely monitored for early price impacts from substantial tariff hikes already imposed in February and March. Those include the spike to a 25% average tariff on imports from China and new steel and aluminum tariffs. These earlier increases may already appear in products like motor vehicles, parts, and certain Chinese-sourced consumer goods like apparel and electronics.

Early signs that trade tensions could de-escalate make risks around our base case outlook more balanced compared to a month ago, when risks were firmly tilted to the downside on growth and to the upside on inflation. But, without a significant pullback in actual tariff rates imposed, U.S. inflation is still expected to accelerate in coming months, and core CPI to rise above 4% later this year.

Week ahead data watch

Canadian manufacturing and wholesale sales likely declined by 1.9% and 0.3%, respectively in March, aligned with Statistics Canada's preliminary estimates. Lower petroleum prices and weaker demand tied to steel and aluminum tariffs likely contributed to manufacturing weakness.

Advanced regional data shows continued cooling in Canada’s home resale market in April. Most markets experienced annual sales declines with increasing price pressures. National resale data in the coming week is expected to confirm these trends.

U.S. retail sales are expected to decline 0.4% after jumping 1.5% in March. Unit auto sales fell 3% in April after jumping 12% in March.

Weekly Economic & Financial Commentary: What’s the Deal?

Summary

United States: Risks Have Risen (but Haven't Materialized Yet)

- The trade deficit blew a hole in Q1 productivity growth, and tariffs are anecdotally increasing price pressures in the services sector. But beyond temporary trade-related distortions, tariffs have yet to meaningfully impact the economic data. We anticipate that tariffs will be negotiated down from current levels but still create a stagflationary environment by year-end.

- Next week: Federal Budget Balance (Mon.), CPI (Tue.), Retail Sales (Thu.)

International: Foreign Central Banks in Focus

- It was a busy week for foreign central bank announcements. The People’s Bank of China, Central Bank of Poland, Czech National Bank and the Bank of England all lowered their central bank policy rates. Sweden's and Norway's central banks held rates steady and kept the door open for more cuts later in the year, while Brazil's central bank raised its Selic rate by 50 bps and signaled the possibility of more tightening going forward.

- Next week: India CPI (Tue.), Australia Employment (Wed.), Japan GDP (Thu.)

Interest Rate Watch: FOMC's Holding Pattern Continues

- As universally expected, the Federal Open Market Committee decided to keep the target range for the federal funds rate unchanged at 4.25%-4.50% this week. After cutting rates by 100 bps last year, the Committee has now been on hold for three consecutive meetings.

Topic of the Week: What's the Deal?

- President Trump and U.K. Prime Minister Keir Starmer announced a U.S.-U.K. trade deal on Thursday. While this marks the first agreement since President Trump reignited the trade war earlier this year, the few details disclosed at this point don't necessarily set the precedent that other agreements will be quickly forthcoming or extensive in nature.

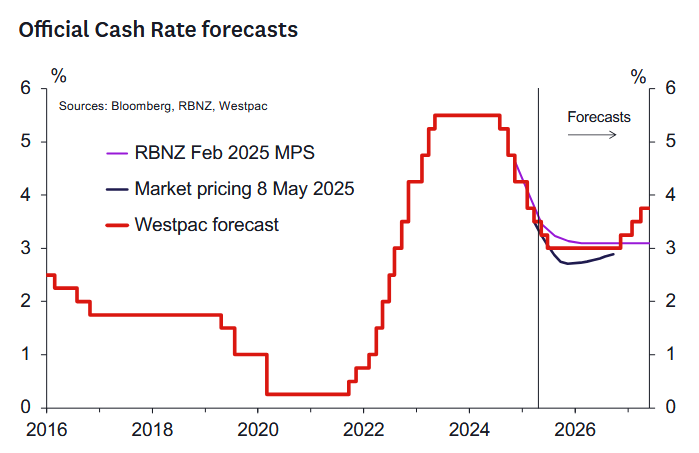

Updated RBNZ OCR Forecast Profile

Pencilling in an extra OCR cut to 3% while risks persist

- Past data look consistent with a gradually recovering economy as expected.

- In the near term, inflation looks set to remain in the top half of the 1-3% range.

- But downside risks from global growth suggest the RBNZ may continue easing beyond May.

- We have pencilled in an additional cut of the OCR to 3% in July as we doubt uncertainty will be resolved by then.

- We also have pushed back the timing of the forecast tightening cycle to end 2026 – after the next General Election.

Next Tuesday we will be releasing updated economic forecasts in our May Economic Overview. These forecasts will update for the evolution of the economy since February as well as making a first cut at quantifying the downside risks to the domestic economy stemming from the potentially weaker and more uncertain global trade environment. It’s entirely unclear what state the global the economy will be in 3-6 months from now and what that could mean here in New Zealand. Some weakness in global trading partner growth looks inevitable but the extent of that weakness and the ultimate impact on New Zealand is totally up for grabs.

We have tried to balance between two scenarios: a baseline scenario of a continued economic recovery; and an alternative scenario of a decent sized global downturn that slows the domestic recovery. That latter scenario, if realised, would imply further cuts to the OCR into what would be quite stimulatory territory (remembering our view of the neutral OCR remains at 3.75%).

In practice, we don’t think the RBNZ will be able to see its way through the fog of war by July or even August. Hence, it’s likely they will continue to cut the OCR beyond the 3.25% trough in the OCR we previously forecast. We have pencilled in an additional 25bp cut to 3% in July (noting that August is also a real possibility) to reflect that the RBNZ will likely continue to perceive downside risks for a while after May.

The baseline view – continued recovery.

The New Zealand economy continued its slow-but- steady recovery up until the trade shock hit. Data in April generally confirmed the view that growth was continuing – albeit with some normal month-to-month volatility. Consumer confidence picked up, business confidence remained robust, the manufacturing and composite PMIs remained in expansionary territory, while activity in the housing market has continued to gradually rise. Economic indicators haven’t all been positive, however. For instance, consumer spending took a step back in March. At the same time, labour market conditions have been more mixed – the March quarter saw a modest gain in employment and the unemployment rate remained unchanged at 5.1%, but wage growth continued to cool, and the number of hours worked declined.

This picture of gradually improving economic activity has been in line with our expectations from earlier this year. Given that inflation pressures show no signs of undershooting the RBNZ’s 2% target mid-point, it's likely we would have been nearing the end of the easing cycle in the absence of current trade shock.

Interest rates have fallen a long way and are delivering significant stimulus that's just hitting the bloodstream right now. The RBNZ delivered the expected 25bp cut to 3.5% at its April meeting as had been signalled in the February Monetary Policy Statement. That brings the total amount of OCR cuts delivered this cycle to 200bps. With large numbers of borrowers due to re-fix their mortgages over the next few months, the associated cuts in mortgage costs will generate a significant increase in monthly disposable income for many households. In fact, for the average household with a mortgage, that fall in their minimum repayments would be equivalent to roughly 4% of their annual income. That compares favourably with other periods of monetary easing in the last 30 years. Indeed, it was only the large reduction seen in the wake of the Global Financial Crisis that has been larger.

Lower interest rates have come at a time when commodity markets are delivering the key NZ primary sector a boom in incomes that's helping underpin growth. Spending in the regions where the primary sector and tourism gains have a higher weight shows strength compared to the major urban areas.

The downside risks.

But nevertheless, growth remains narrowly based and remains vulnerable to a setback. Concerns that such a setback could be upon us have arrived now, with threats to the global outlook coming from record high levels of trade policy uncertainty amidst the wildly fluctuating trade policy and tariff outlook. The direct impact of New Zealand’s 10% tariff is unwelcome but, in the end, manageable. It's the possible indirect effects that are of greater importance.

Markets will remain alert for the potential that the uncertain operating environment is impinging on the nascent recovery in consumption and investment. Businesses indicated some risks here in the ANZ’s April business confidence survey where firms that responded later in April took a much more pessimistic view on the outlook for investment and employment than those who answered earlier in the month.

But critical will be the extent to which weaker global growth reduces the terms of trade that's contributing to the recovery thus far. News to date has been encouraging. Export prices haven't fallen and by and large orders have not been cancelled. While damage has been done in some areas (for example, for some local manufacturers with facilities based in Asia but exporting to the United States), opportunities beckon for others. For example, suppliers of beef and dairy products to China may see increased demand, replacing highly-tariffed exports from the US.

The behaviour of the exchange rate will be critical in managing the damage done by the indirect tariff effects. The volatility in the exchange rate in the last month is testament to the uncertainty on the outlook. The NZD/ USD exchange rate fell below 55 cents in early April on the tariff announcements but recovered to just above 60 cents as sentiment regarding the US dollar soured and as better news emerged on the tariff front. On a trade weighted basis, the NZD has traded in a 6% range in the last month. While our forecast is for the NZD to track around current levels versus the USD for the remainder of this year, there is a risk of further weakness and volatility.

We see further trend weakness in the NZD on a trade weighted basis around a volatile path as views wax and wane on the US dollar and global uncertainty. We have considered a downside scenario for the global economy that is perhaps around a quarter of the intensity seen during the GFC, which would slow growth and push inflation somewhat lower in New Zealand. That downside scenario is realistic, but by no means certain. The actual outcome could be better or worse than assumed – both in terms of the size of the hit to trading partner growth and its impact on the economy.

The starting point for inflation is still uncomfortably high for the RBNZ. For various reasons, domestic inflation continues to fall more slowly than expected given past weakness in the economy. While we see cyclical elements of inflation moving lower, there are plenty of other sources of inflation that are more persistent – for example in less competitive parts of the economy including in areas dominated by central and local government. On its own, that persistence in domestic inflation pressures would not argue for further cuts into more stimulatory territory, especially when compounded by the rise in prices for food and other commodities.

The implications for monetary policy now.

We should consider and put some weight on the downside risks for global growth. It's those risks that markets have responded to recently and which the RBNZ MPC will likely act on when cutting the OCR a further 25bp at their May meeting.

We had thought that the easing cycle would be over by mid-2025. But trade uncertainty is likely to persist for longer than that, which means the downside risks will be with us until at least August and possibly longer. A corollary is that once reaching this new lower trough, the OCR could remain there for longer. Given a General Election is likely in late 2026 it seems prudent to assume at this point the tightening cycle might begin at the end of 2026 as opposed to mid-2026 as previously assumed. We also note that Treasury and the Minister of Finance have been vocal in suggesting that interest rates should be cut in the event of the downside risks crystallising. It's likely the interim RBNZ Governor and the MPC will have that in mind when determining the best path forward.

It's by no means clear that the downside risks will eventuate, but we expect the RBNZ to continue to move methodically in the easing direction while those downside risks remain. A move in the OCR to 3% now seems likely by August. We don't expect a lurch lower - it would take tangible signs of a more significant impact on the NZ economy and critically the inflation outlook to cause the MPC to move more quickly. It will be important to ensure the MPC’s actions now don't necessitate the need for an aggressive rise in interest rates down the track should conditions not prove as weak as feared by markets. Policy is likely stimulatory now.

Week Ahead – All Eyes on US CPI and Trade Talks Amid No End to Tariff Uncertainty

- US CPI report takes centre stage to gauge tariff impact.

- Progress in trade negotiations will also be watched, especially with China.

- US Retail Sales, UK and Japanese GDP on the agenda too.

Will reciprocal tariffs show up in April CPI?

Despite lingering worries about a recession, the available data suggests the US economy is at worst, headed for a slowdown. There are no signs yet either that inflation is accelerating, as both the CPI and PCE measures declined in March. However, the cooldown in inflation is likely to be temporary as the broad-based reciprocal tariffs kicked in on April 9. Although the higher levies that were set above the 10% universal rate were delayed for 90 days and some other exemptions were announced too, the price of most imports is expected to have gone up by at least the same amount, with many imports from China facing steeper 145% tariffs.

Yet, it’s expected that very little of those costs were passed on to consumers in April. Many businesses frontloaded their imports before ‘Liberation Day’, while others are likely hoping that most of the tariffs will disappear soon and are holding off from raising prices. But this is contingent on the Trump administration reaching trade deals with its main trading partners within months, something that may not be very realistic.

However, it does mean that the April CPI report won’t be the disaster it could have been. The consumer price index is expected to have increased by 0.3% month-on-month, staying unchanged at 2.4% on a yearly basis. Core CPI is also forecast to have risen by 0.3% over the month and to remain unchanged at 2.8% year-on-year.

The Fed warned of rising risks to both inflation and unemployment at its May policy meeting so any upside surprises to the data on Tuesday could lead investors to further pare back their rate cut expectations for 2025.

US Retail Sales, UoM survey also eyed

But with the Fed also having full employment as part of its dual mandate, rate cut bets are a tradeoff between inflation and what’s happening in the rest of the economy. At the moment, the Fed is being careful about managing inflation expectations, hence, it’s holding firm on its wait-and-see stance. But any sudden deterioration in the economy would prompt it to reconsider this position, as has already been indicated by some Fed officials.

Retail sales is one such dataset that could go in the opposite way of the inflation report. After surging by a revised 1.5% m/m in March, retail sales probably increased by just 0.1% in April. Those figures are out on Thursday alongside producer prices, industrial production and the Philly Fed manufacturing index. There’s a further flurry of releases on Friday, including building permits, housing starts, the Empire State manufacturing index and the University of Michigan’s preliminary consumer sentiment survey.

The latter will be particularly important as the UoM’s inflation expectations metrics have jumped significantly in recent months, likely contributing to the Fed’s caution.

Hopes are high for US-China trade progress

But as investors desperately dissect all the data for clues, it’s possible that tariff-related headlines might have a bigger impact on the markets. US Treasury Secretary Scott Bessent and Trade Representative Jamieson Greer are due to hold talks with senior Chinese officials in Switzerland on Saturday.

This is the first high-level meeting between the two countries since the escalation of trade tensions in February and the stakes are high. Markets are for the moment simply cheering the fact that two sides have agreed to engage in direct talks. But there’s plenty to suggest that Washington and Beijing are quite far apart on their starting points, so any disappointment could bring about a reversal in the positive sentiment, pulling risk assets lower at the start of the trading week.

Can UK data propel the Pound higher?

Any potential selloff might be less severe for the pound and UK stocks following the deal reached between the US and Britain on trade that reduces the 25% tariffs on cars and steel to the baseline 10% rate. Whilst it doesn’t appear that the UK has managed to win many concessions in this preliminary agreement, it comes hot on the heels of a deal with India too, as well as improving relations with the European Union.

Subsequently, the pound has established strong support just above the $1.32 level, but at the same time, it’s lacking the momentum to make a convincing break above $1.34. In the absence of a global risk rally, next week’s UK economic releases might not be enough to recharge the bulls.

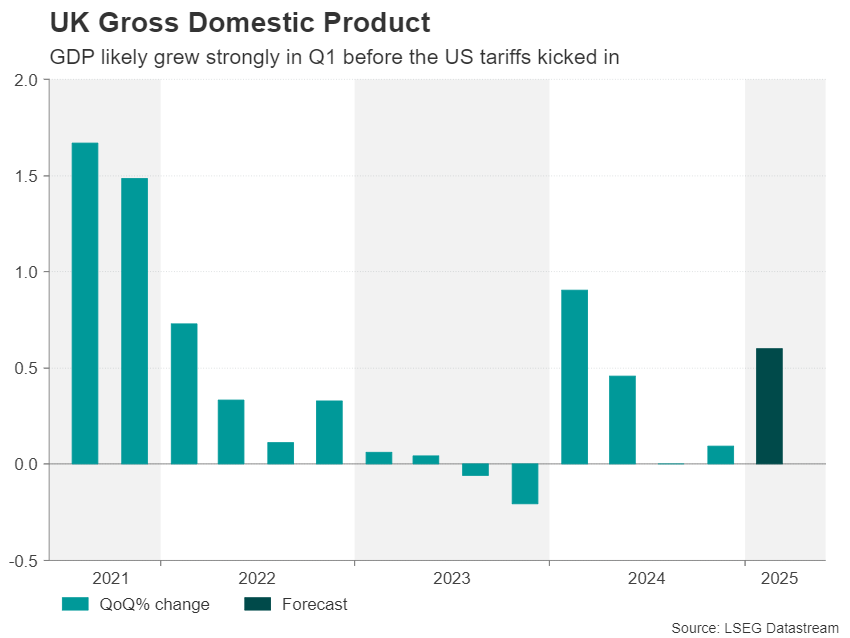

UK employment numbers for March are out on Tuesday, with the Bank of England keeping a close watch on wage growth, which is proving very sticky. The BoE doesn’t expect inflation to reach its 2% target until 2027 but concerns about growth are keeping it on an easing path. An update on the economy is due on Thursday when first quarter GDP readings are published.

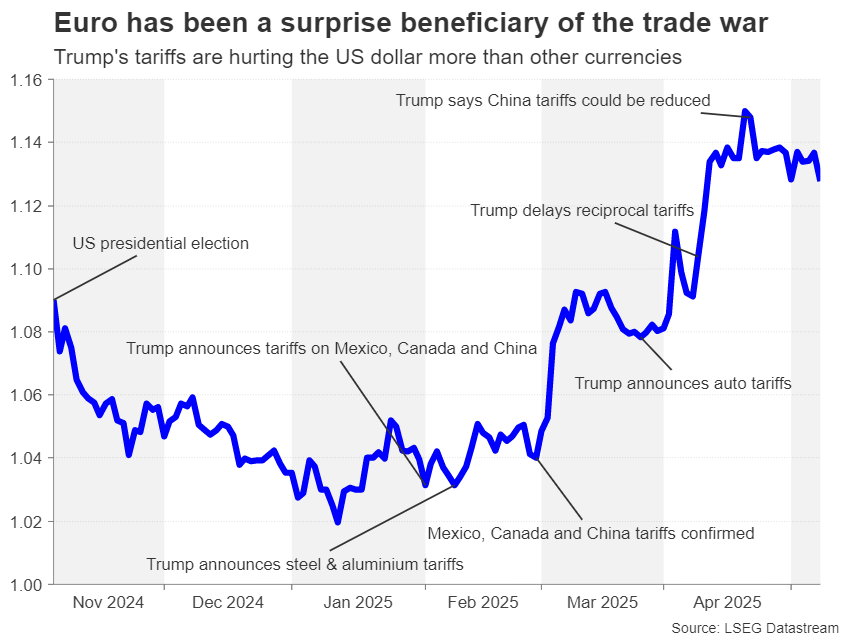

Euro uptrend loses steam as US trade talks drag on

Across the channel, it will be a relatively quiet week for the euro area, with US-EU trade negotiations likely being the main focus for investors. The EU is reportedly mulling higher tariffs on up to 95 billion euros worth of US goods that the bloc could impose should the talks fail. On the other hand, any signs of progress could spur the euro, which has been consolidating its trade war-led gains over the past three weeks.

On the data front, the ZEW economic sentiment index out of Germany might attract some attention on Tuesday, while on Thursday, quarterly employment and the second estimate of Q1 GDP growth for the Eurozone will hit the wires.

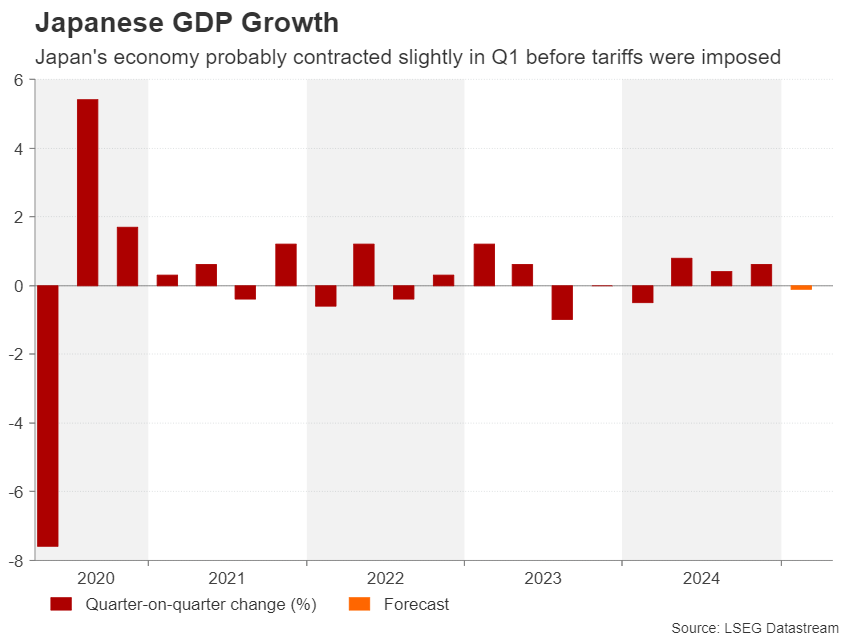

Japanese GDP might dent BoJ rate hike bets

Japan is also eager to reach a new deal on trade with the United States as the fragile economic recovery likely ran into trouble in the first three months of 2025. GDP figures out on Friday are expected to show that the Japanese economy contracted mildly, by 0.1%, in Q1.

The sluggish performance even before Trump’s tariffs have come into effect is one of the reasons why the Bank of Japan has turned less confident about hiking interest rates again. Having said that, policymakers are becoming increasingly concerned about the stickiness in food inflation, which may eventually push up underlying price pressures.

Hence, a rate hike is by no means off the table and any unexpected strength in the economy would increase the likelihood of further tightening later in the year, boosting the yen.

There might also be some hints on rate hike prospects in the BoJ’s Summary of Opinions of the April-May meeting that will be published on Monday. The Summary should shed some light on how strongly board members are sticking to their determination to normalize policy.

Australian employment on tap

Finally, in Australia, the labour market will be in the spotlight, as Q1 wage growth numbers are out on Wednesday, to be followed by the employment report for April on Thursday. Investors have priced in about a 90% probability that the Reserve Bank of Australia will cut rates for only a second time at its policy meeting later in May. It’s hard to see the job figures materially shifting those odds.

Nevertheless, any big surprises could move the Australian dollar, although at the start of the week, the aussie’s focus will be on the developments from the weekend’s US-China trade talks, as well as on China’s CPI and PPI release on Saturday.

Weekly Focus – Fed, and the Economy, in Wait-and-See Mode

Not without reason, the US central bank is unsure about the direction of the economy and inflation given the tariff increases and the uncertainty about what will happen to them. That was clear from the monetary policy decision this week where the bank kept interest rates unchanged and stated that risks have increased in both directions - both the risk of higher inflation and the risk of a weaker economy. The Fed can to some extent afford to be patient as the labour market continues to look strong, with 177,000 jobs added in April. However, the labour market reacts with a delay to the rest of the economy, and we expect to see a clear tariff impact on growth in the second half of the year. On the other hand, inflation is still a bit higher than targeted and inflation expectations have risen strongly, which in itself is a problem for the Fed. In the coming week, we will get consumer prices for April where we could start to see an effect of higher tariffs, and new consumer confidence data including inflation expectations. That could have a significant impact on whether the Fed can cut rates at its next meeting in June. We see a June cut as the most likely outcome, but of course with significant uncertainty.

However, we could see markets paying more attention to trade talks than to data releases. Thursday this week, the US and the UK reached a trade agreement which reduces the tariffs that the US have recently introduced on British cars and metals, but still maintains the general 10% tariff even though the US has a trade surplus in goods with the UK. If this is a template for future trade deals - that extra tariffs on for example cars can be reduced or scrapped, but that the "reciprocal" tariffs announced on 2 April stand - then the deals will not make much difference for the overall tariff level. It is of course highly uncertain if other deals will resemble the UK one, though.

Progress towards a much more significant tariff deal could come already this weekend as US and Chinese negotiators meet in Geneva. Tariffs far above 100%, as they currently have against each other, are clearly going to have a seriously negative effect on both countries' economies as supply chains are disrupted and there is a risk of empty shelves in US stores. Hence, there is a strong incentive to reach a deal to lower the tariffs. In our interpretation, markets are expecting tariffs to land around 60%, and there are possibilities for both positive and negative surprises relative to that.

This week, we also got the approval of the new German government which plans to ease fiscal policy by maybe 2% of GDP and hence give a boost to growth and interest rates in Europe. The new government had to be voted on twice though, as it lost its first vote, a reminder that it only has a narrow parliamentary mandate. We expect that the fiscal easing will have only a limited impact on the economy in 2026 with the full effect seen the following year, and hence that it is not a hindrance for the European Central Bank in lowering interest rates further over the coming months. Next week, the European Commission publishes its economic forecasts which will likely discuss that issue in more detail and could influence also how the ECB sees the situation.

The Bank of England cut interest rates as expected by 25bp, but the Monetary Policy Committee is highly divided.