Sample Category Title

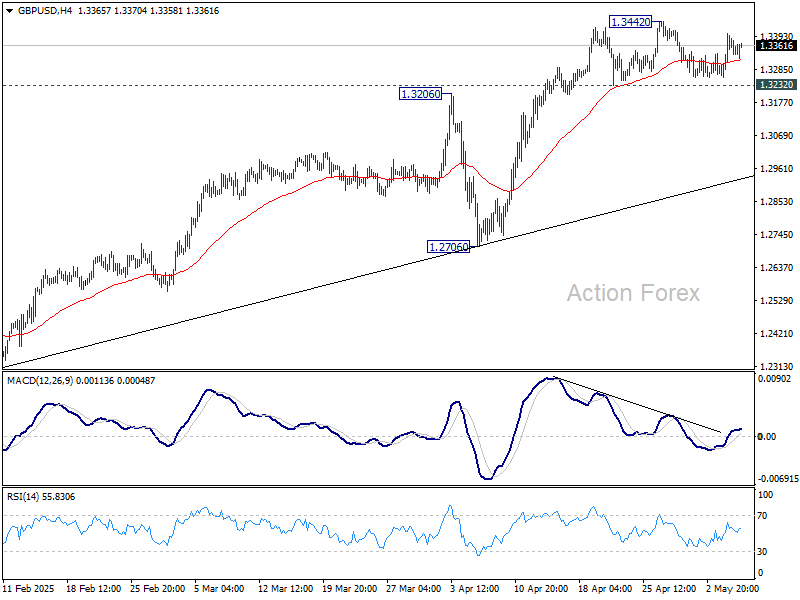

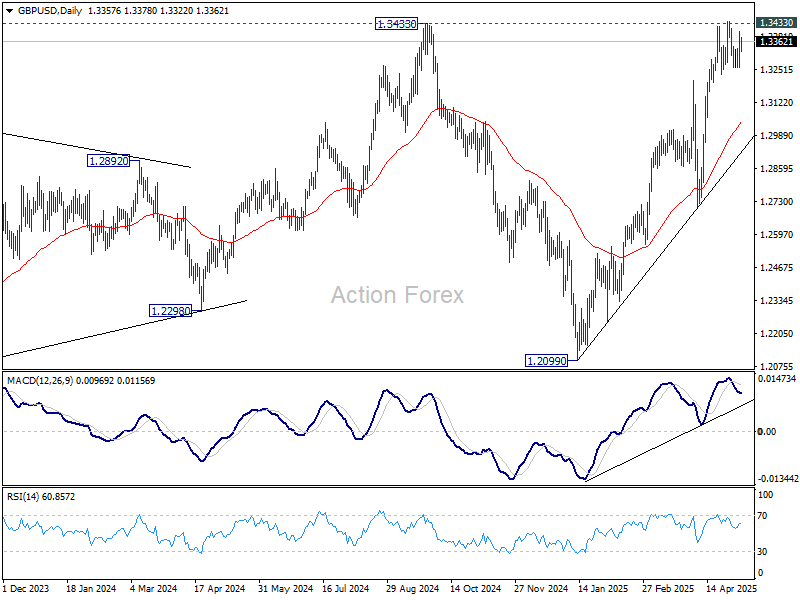

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3286; (P) 1.3344; (R1) 1.3428; More...

Intraday bias in GBP/USD remains neutral and outlook is unchanged. On the downside, firm break of 1.3232 support will indicate short term topping and rejection by 1.3433 key resistance. Intraday bias will be back on the downside for deeper pullback to 55 D EMA (now at 1.3044) and possibly below. On the upside, decisive break of 1.3433 key resistance will confirm larger up trend resumption.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could either be resuming the up trend, or the second leg of a consolidation pattern. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on decisive break of 1.3433 at a later stage.

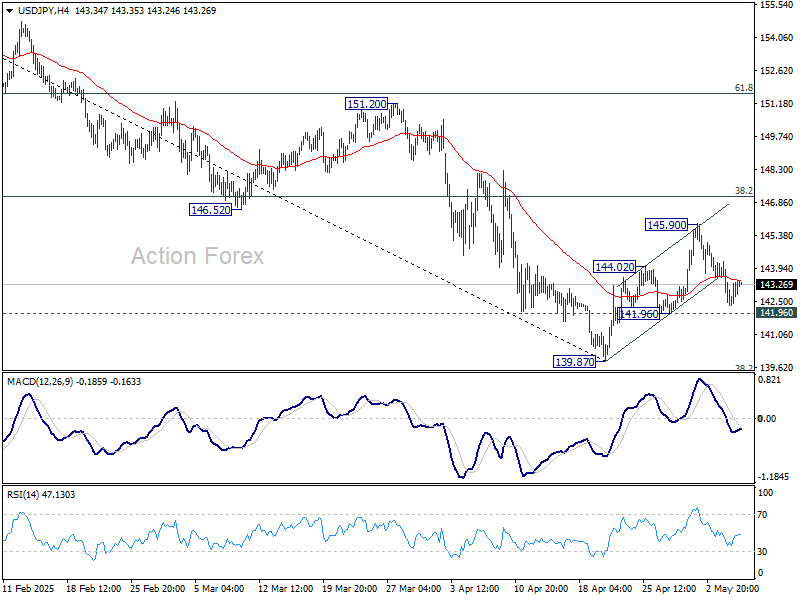

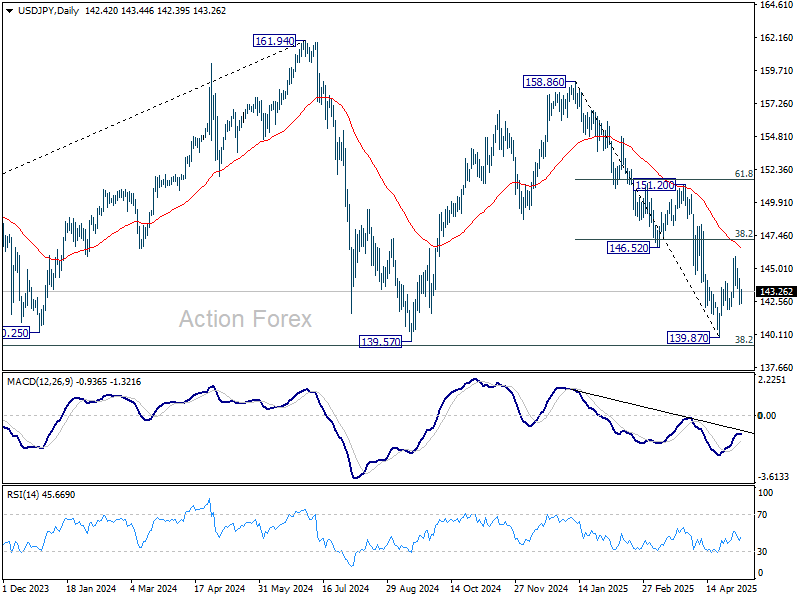

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 141.76; (P) 143.01; (R1) 143.67; More...

Intraday bias in USD/JPY remains neutral at this point. Rebound from 139.87 might still extend higher. But outlook will stay bearish as long as 38.2% retracement of 158.86 to 139.87 at 147.12 holds, in case of another bounce. On the downside, firm break of 141.96 will argue that rebound from 139.87 has completed as a corrective move. Retest of 139.87 should then be seen next in this case.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

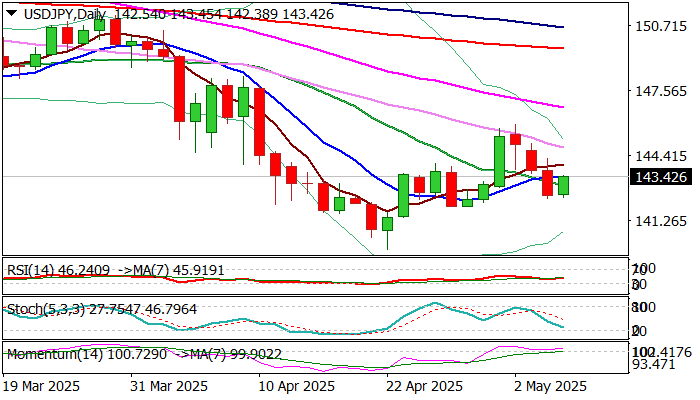

USD/JPY: Markets Focus on Tonight’s Fed Announcement

USDJPY edged higher on Tuesday on partial profit-taking from strong drop in past three days (the pair was down 2%).

Bounce was so far limited (retraced slightly above 23.6% of 145.92/42.35 bear-leg), with mixed technical studies (daily Tenkan/Kijun-sen in bearish setup 14 -d momentum still in positive territory), but near-term action remains weighed by recent formation of bull-trap on daily chart (above 50% of 151.20/139.88 downtrend / daily Kijun-sen).

Latest signals of potential US-China trade deal, partially offset signals for increased safe-haven demand on fresh escalation of India / Pakistan conflict.

Markets focus on tonight’s Fed announcement, looking for more clues about the US central bank’s rate trajectory in coming months.

Daily close above 10DMA (143.32) is seen as minimum requirement to keep in play hopes for stronger recovery and challenge of next pivotal barriers at 143.71/93 (Fibo 38.2% / daily Tenkan-sen).

Conversely, early recovery rejection would signal that larger bears hold grip and keep in play risk of retesting key 140 support zone.

Res: 143.71; 143.93; 144.13; 144.55.

Sup: 143.19; 142.90; 142.35; 141.94.

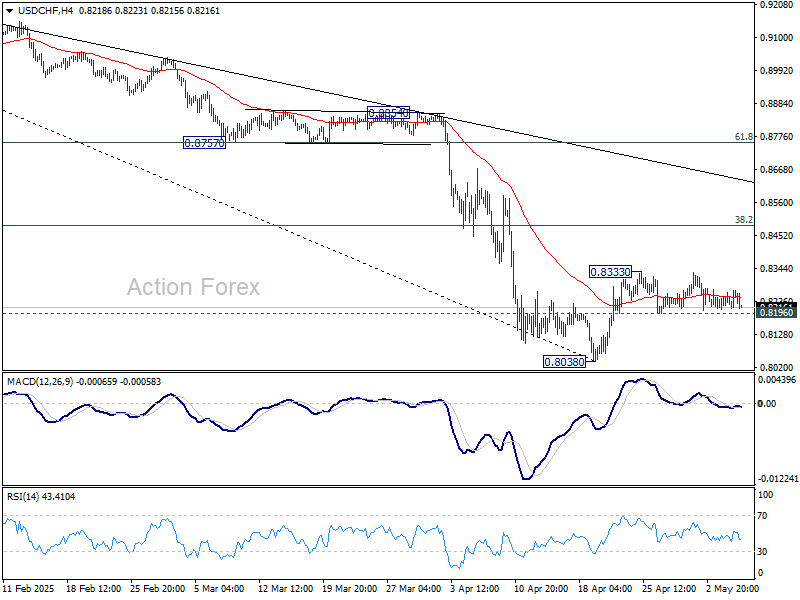

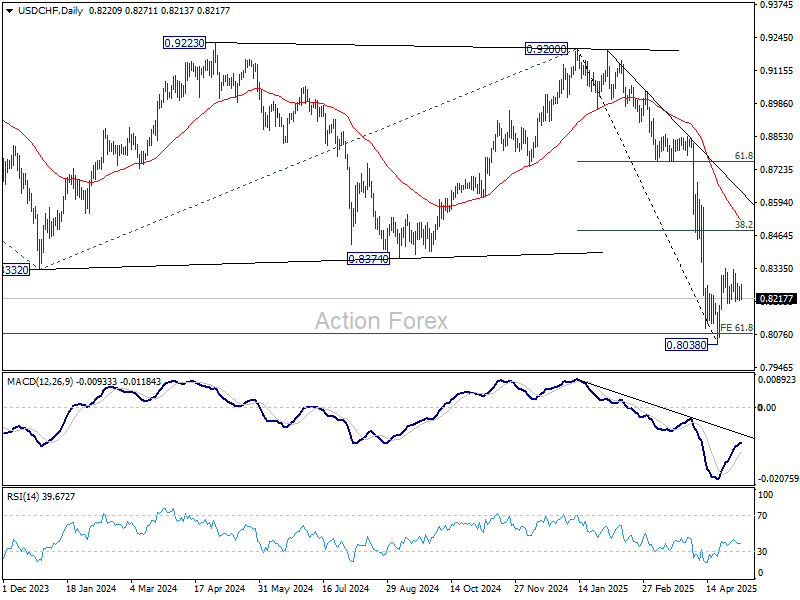

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8201; (P) 0.8233; (R1) 0.8254; More….

USD/CHF is still bounded in right range below 0.8333 and intraday bias remains neutral for the moment. On the upside, above 0.8333 will resume the rebound from 0.8038. However, upside should be limited by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. On the downside, below 0.8196 minor support will bring retest of 0.8038. Firm break there will resume larger down trend.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8763) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

Calm in Currency Markets Ahead of Fed’s Fourth Straight Hold

The forex markets are treading water ahead of today’s FOMC decision. While the announcement typically acts as a volatility trigger, the lack of suspense surrounding this meeting could mean muted price action even after Chair Jerome Powell’s press conference. Markets are pricing in a near-certainty, 99% probability, that Fed will hold the policy rate steady at 4.25–4.50% for a fourth straight meeting, leaving little room for surprise. Adding to the quiet is the absence of updated economic projections and dot plot guidance, which are only due at the June meeting.

Last week's stronger-than-expected non-farm payrolls cooled expectations for near-term easing, with the chance of a June rate cut falling to around 30%. Traders will be closely watching Powell’s tone for any nuanced shift, particularly regarding the timing of the next rate cut. However, officials are likely to maintain their cautious, data-dependent posture given persistent economic uncertainty, especially around the evolving US tariff policies.

Indeed, Powell is expected to reiterate that the Fed is not in a hurry to adjust rates. The ongoing tariff truce and upcoming negotiations—such as this weekend’s Geneva meeting between U.S. and Chinese trade officials—introduce substantial geopolitical risks that could influence inflation, growth, and financial conditions. With so many moving parts, Fed is unlikely to make any forward commitments. For now, the market still leans toward three rate cuts by year-end, which would bring the target range down to 3.50–3.75%, but policymakers are not ready to validate that path.

In terms of price action so far this week, the Dollar has underperformed, joined by Loonie and Swiss Franc near the bottom of the board. Yen has led gains, followed by Kiwi and Sterling. Euro and Aussie are positioned in the middle. But with ranges tightly held, these relative standings could shift quickly depending on today’s Fed tone and incoming trade headlines.

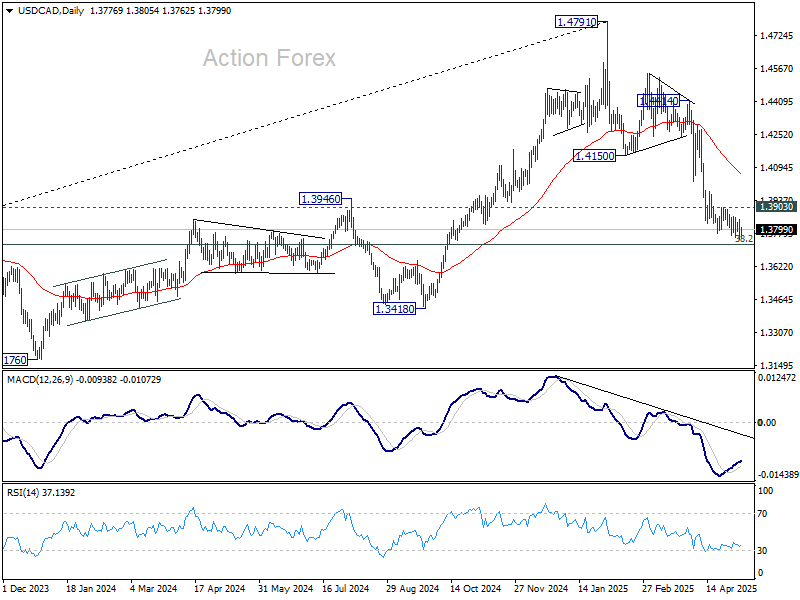

Technically, USD/CAD has clearly lost must momentum, as seen in D MACD, as it approaches 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727. Break of 1.3903 resistance should indicate short term bottoming, and bring stronger rebound back to 55 D EMA (now at 1.4057). However, firm break of 1.3727 could then bring deeper fall to 1.3418 support before USD/CAD tries to bottom again.

In Europe, at the time of writing, FTSE is down -0.53%. DAX is down -0.24%. CAC is down -0.68%. UK 10-year yield is down -0.049 at 4.471. Germany 10-year yield is down -0.04 at 2.503. Earlier in Asia, Nikkei fell -0.14%. Hong Kong HSI rose 0.13%. China Shanghai SSE rose 0.80%. Singapore Strait Times rose 0.13%. Japan 10-year JGB yield rose 0.038 to 1.300.

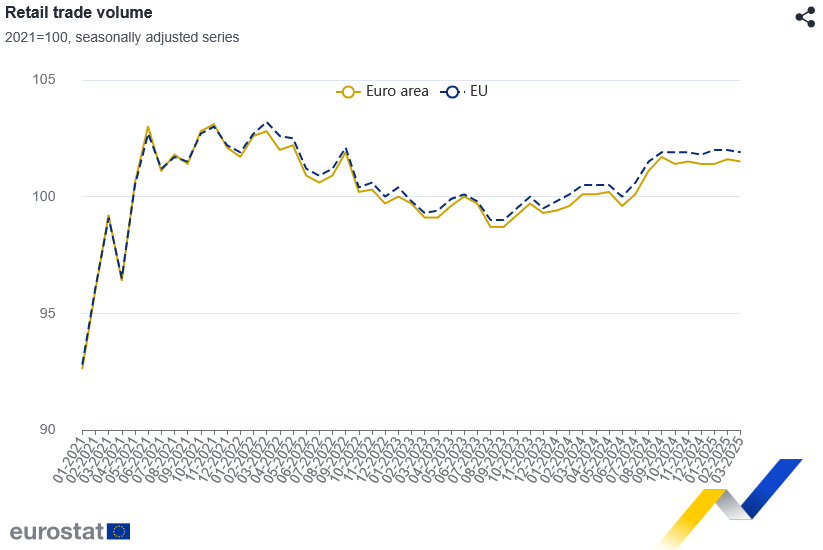

Eurozone retail sales fall -0.1% mom in March

Eurozone retail sales slipped by -0.1% mom in March, in line with expectations. The breakdown shows marginal declines across key categories, with food, drinks, and tobacco sales down -0.1%, and non-food products (excluding fuel) also falling -0.1%. Only automotive fuel recorded a modest rise, up 0.4%.

Across the broader EU, retail trade also declined -0.1% mom. Notable contractions were seen in Slovenia (-2.0%), Estonia (-1.3%), and Slovakia (-0.9%). Malta led the gainers with a 2.0% increase, followed by Belgium, Croatia (both +1.4%), and Bulgaria (+1.1%).

Japan’s PMI composite finalized at 51.2, input inflation jumps to 2-year high

Japan’s private sector returned to expansion in April, as the final PMI Composite rose to 51.2 from March’s 48.9. The improvement was driven entirely by the services sector, with its PMI climbing to 52.4, while manufacturing remained in contraction.

According to S&P Global’s Annabel Fiddes, stronger services activity helped offset the drag from factories, where new orders fell sharply in response to the global tariff environment.

While services firms reported stronger demand, confidence among both services and manufacturing sectors deteriorated. Businesses expressed concern about the broader global outlook and the negative implications of recent US tariff moves on growth potential.

Adding to the pressure, input price inflation accelerated to a two-year high, prompting firms to raise selling prices to protect margins.

NZ employment grow 0.1% in Q1, wages growth cool

New Zealand’s employment grew just 0.1% qoq as expected, while the unemployment rate held steady at 5.1%, better than forecast of 5.3%.

However, the quality of employment deteriorated, with a notable shift from full-time to part-time roles. Over the year, full-time employment dropped by -45k while part-time roles increased by 25k.

Participation rate edged down to 70.8% and the employment rate slipped to 67.2%, both suggesting a gradual loss in labor market momentum.

Wage growth also moderated, with the labour cost index rising 2.9% annually, down from 3.3% in the previous quarter.

PBoC unleashes broad-based monetary easing including rate and RRR cuts

China’s central bank has announced a sweeping set of monetary policy measures to support its economy, starting with a 10bps cut in the seven-day reverse repo rate to 1.40%, effective May 8. In a more aggressive move, the PBoC will also slash the reserve requirement ratio by 50bps, releasing approximately CNY 1T into the banking system.

The new package is structured into three categories: quantitative, price-based, and structural tools. The quantitative arm focuses on long-term liquidity via the RRR cut. The price-based measures involve lowering benchmark and structural policy rates. The structural component aims to channel credit into strategic areas such as technological innovation, consumption, and inclusive finance.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8201; (P) 0.8233; (R1) 0.8254; More….

USD/CHF is still bounded in right range below 0.8333 and intraday bias remains neutral for the moment. On the upside, above 0.8333 will resume the rebound from 0.8038. However, upside should be limited by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. On the downside, below 0.8196 minor support will bring retest of 0.8038. Firm break there will resume larger down trend.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8763) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

Yen Rally Ends, Markets Eyes Fed Rate Decision and BoJ Minutes

The Japanese yen is in negative territory on Wednesday, after a three-day rally which saw it gain 2% against the US dollar. In the European session, USD/JPY is trading at 143.29, up 0.61% on the day.

The Bank of Japan releases the minutes of its March meeting on Thursday. At the meeting, the BoJ held the key policy rate at 0.5% in a unanimous vote. Members cautioned that there was uncertainty over tariffs, which the US was expected to announce in April.

Since then, the financial markets have see-sawed in response to President Trump's erratic tariff policy. Japan's export-reliant economy could be hit hard, but Tokyo is already negotiating with the US and hopes to carve out an agreement to cancel or at least mitigate the impact of the tariffs.

The Bank of Japan is walking a tightrope, as it wants to continue to normalize policy and raise rates, but is worried about the uncertainty over the tariffs and the real possibility of a global trade war. Bank policymakers are taking a wait-and-see stance, hoping that US trade policy will become more clear.

Fed likely to hold rates at today's meeting

The Federal Reserve is virtually certain to maintain rates at today's FOMC meeting. There's little doubt about the decision but investors will be all ears as to the amount of pushback from Fed Chair Jerome Powell, after President Trump has repeatedly pushed him to lower rates.

The markets have priced in a 30% chance of a cut in June, compared to a 63% likelihood just one week ago, according to CME's Fedwatch Tool. We can expect the pricing of a June cut to continue to swing, as the tariff saga continues.

USD/JPY Technical

- There is resistance at 143.67 and 144.92

- 143.01 and 141.76 are the next support levels

USDJPY 1-Day Chart, May 7, 2025

New Zealand Unemployment Rate Lower Than Expected, Kiwi Declines

The New Zealand dollar is lower on Wednesday, ending a three-day rally. In the European session, NZD/USD is trading at 0.5982, down 0.41% on the day.

New Zealand unemployment rate stays at 5.1%, labor market barely expands

New Zealand's employment report for the first quarter indicated that the labor market remains soft. The good news was that the unemployment rate remained unchanged at 5.1%, below the market estimate of 5.3%. Still, unemployment remains at its highest since Q4 of 2020 - a year ago, the rate was just 3.4%.

Employment change posted a small gain of 0.1%, up from a revised -0.2% in Q4 and in line with the market estimate. Wage inflation edged lower to 0.4% from 0.6%, lower than the market estimate of 0.5%.

How will the Reserve Bank of New Zealand react to the latest jobs report? The central bank has been aggressive, slashing the cash rate by 200 points since August 2024 to 3.5%. Today's employment report supports the case for a rate cut at the May 28 meeting and for further cuts during the year. At the April meeting, members warned that the tariffs created downside risks for growth and inflation in New Zealand.

The RBNZ released its Financial Stability Report on Wednesday with a warning that the impact of US tariffs on New Zealand could be "severe" and that there was considerable uncertainty over the outlook for global trade. The report noted that the impact of indirect tariffs on "key trading partners" (likely as reference to China) could be even more damaging that direct tariffs.

Fed expected to stay on the sidelines

The Federal Reserve is almost certain to maintain interest rates at today's FOMC meeting. There's little doubt about the decision but the markets will be all ears as to the amount of pushback from Fed Chair Jerome Powell, after President Trump has repeatedly pushed him to lower rates.

The markets have priced in a 30% chance of a cut in June, compared to a 63% likelihood just one week ago, according to CME's Fedwatch Tool. We can expect the pricing of a June cut to continue to swing, as the tariff saga continues.

NZD/USD Technical

NZD/USD has pushed below support at 0.6006 and is testing support at 0.5986. The next support level is 0.5980

There is resistance at 0.6020 and 0.6026

NZDUSD 4-Hour Chart, May 7, 2025

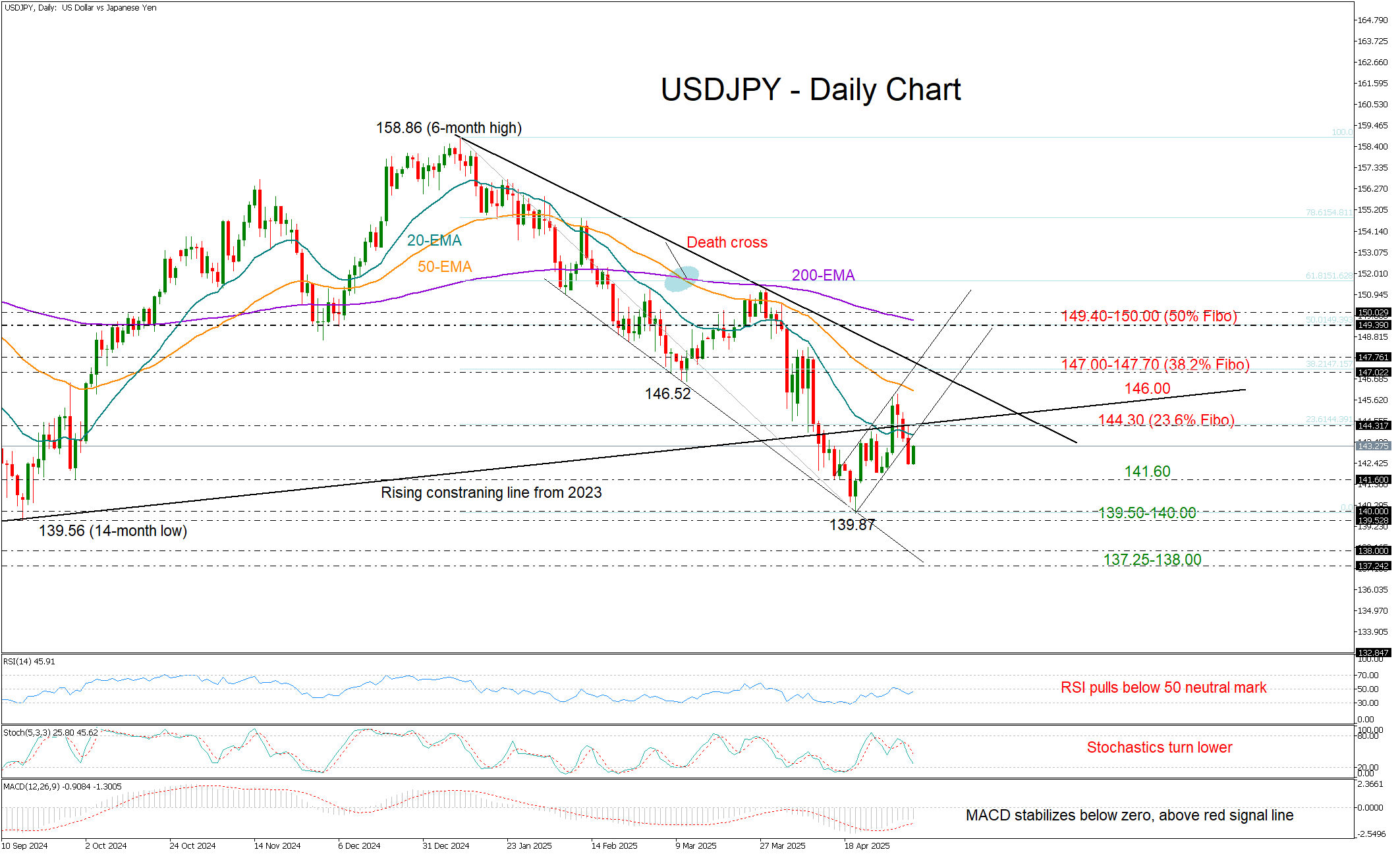

USD/JPY Remains Exposed to Bearish Trend

- USD/JPY erases gains, shifts spotlight to bearish trajectory.

- Resistance at 144.23, support at 141.60.

USDJPY has broken out of a brief bullish channel after failing to push past the constraining zone at 145.35, raising concerns that the bearish trend may still have room to extend.

With the RSI failing to cross above its neutral 50 mark and the stochastic oscillator resuming its downward slope, the likelihood of a meaningful rebound remains low. Adding to the bearish sentiment are the declining exponential moving averages (EMAs), which continue to support the downward trajectory in price. Perhaps any signals that rate cuts are still on the table during today’s FOMC policy announcement, which is expected to keep borrowing costs unchanged, could further weight on the greenback.

The next support may emerge near the key level of 141.65, which has occasionally shielded the market from selling pressure in the second half of 2024. Notably, this area also aligns with the 61.8% Fibonacci retracement of the 2023–2024 uptrend. Therefore, if the bears breach this level as well, attention will likely shift to the critical support zone of 139.50–140.00. A deeper decline could extend toward the 137.25–138.00 area, which served as support from November 2022 to July 2023.

On the upside, bulls must overcome resistance at 144.30 to reach the 146.00 region, where the 50-day EMA is currently situated. A further rise above the 38.2% Fibonacci retracement level at 147.00, along with the tentative resistance trendline from the 2025 peak, may be required to trigger a rally toward the 50% Fibonacci level at 149.40 and the 200-day EMA.

Overall, USDJPY has failed to enter bullish territory despite its recent recovery attempt. The bearish trajectory is likely to continue unless the 141.60 support level holds firm.

Crypto Market Tests Range Ceiling

Market picture

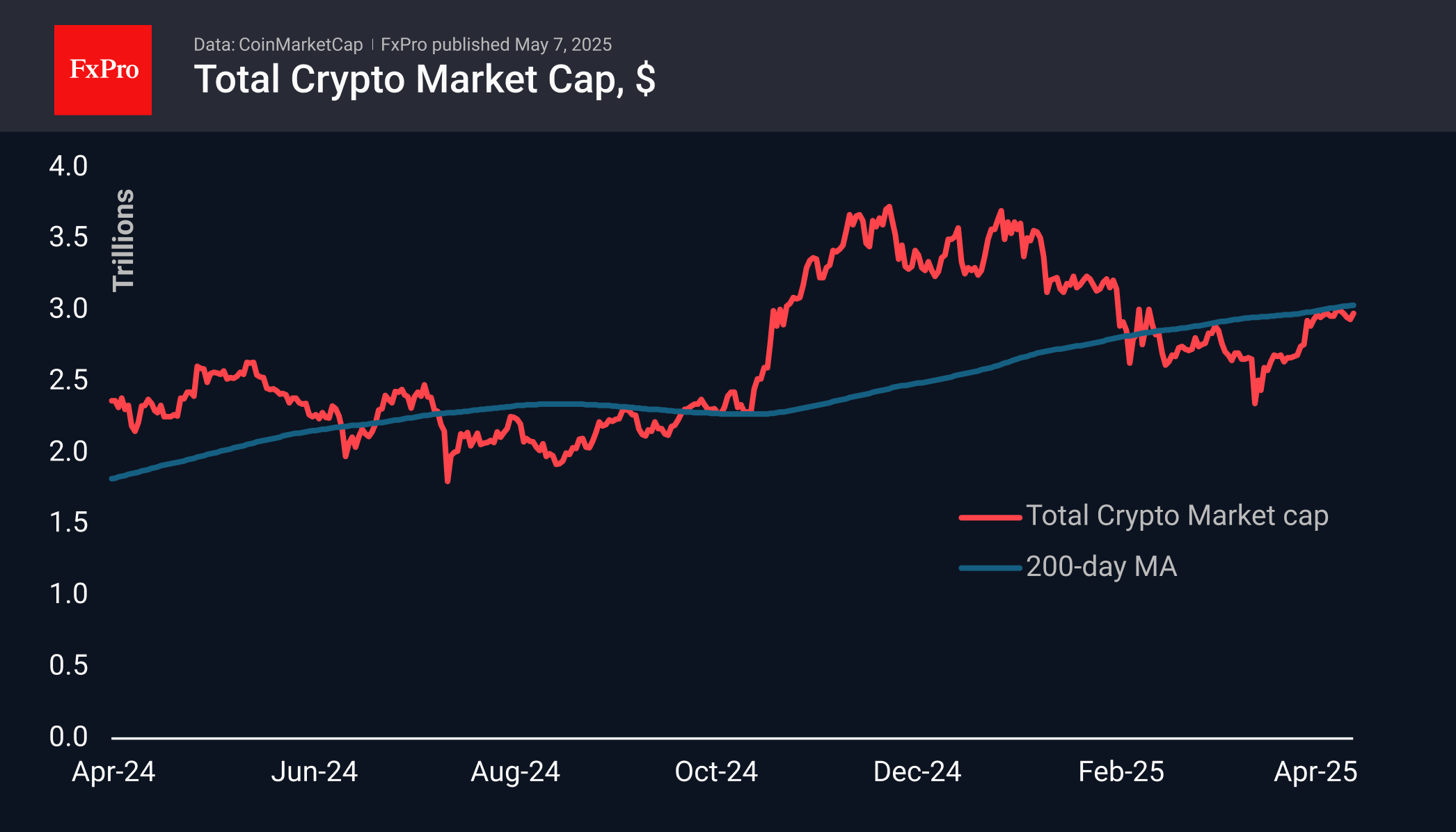

Market capitalisation rose 1.7% in the last 24 hours to $2.98 trillion, approaching the upper end of the consolidation range where the market has been hovering for almost two weeks. The previous consolidation in April took about the same amount of time before the last move up. Rest after the rise may favour further growth.

Greed characterised market sentiment on Tuesday, with the corresponding index rising to 67, repeating the highs of May 2.

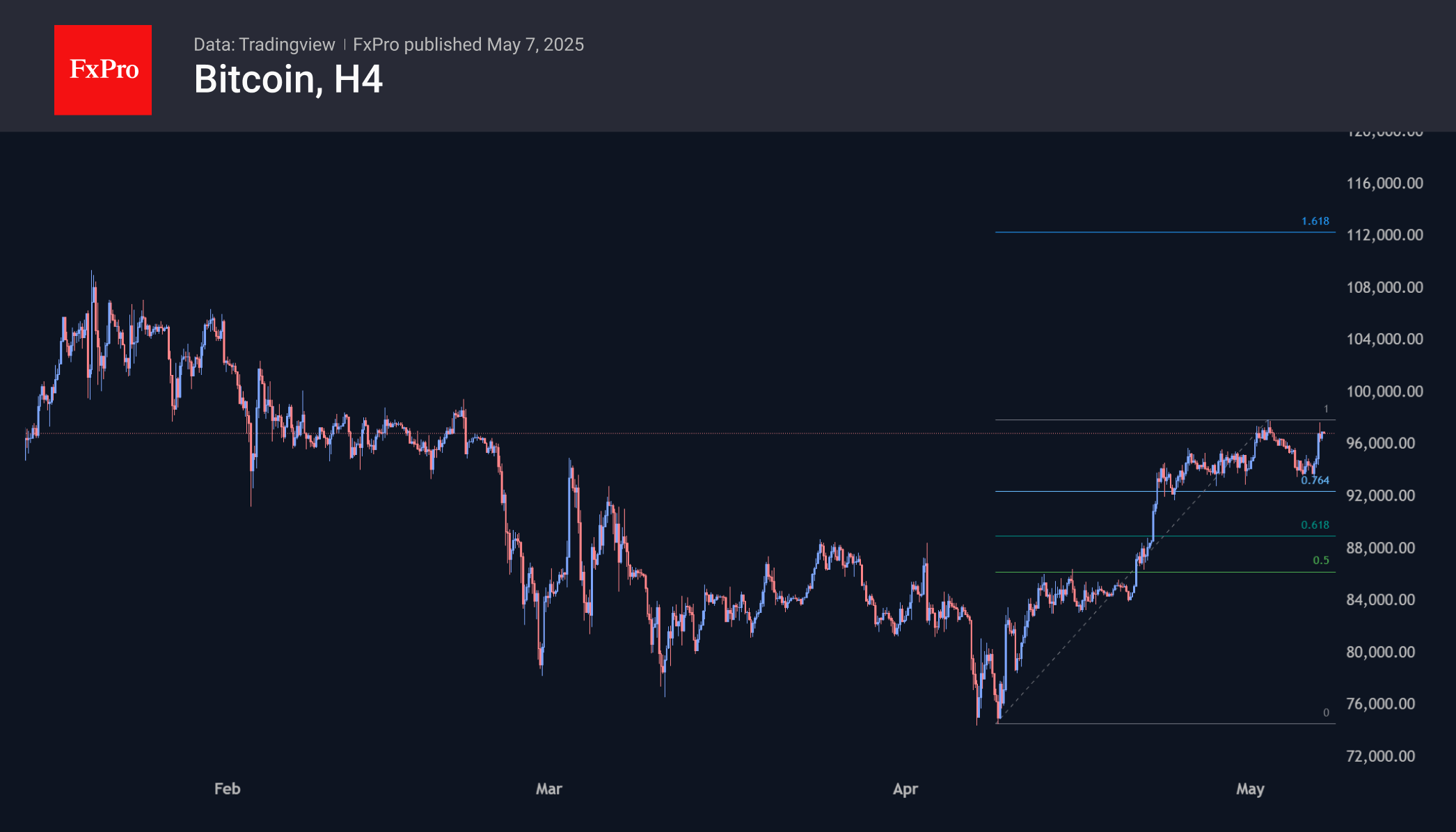

Bitcoin rose significantly on reports of events in India and Pakistan, briefly surpassing the $97.5K level. This growth momentum has not yet found support in other assets – gold is getting cheaper, and the equity index is mostly down. Perhaps the assault on local highs will continue soon. A consolidation above $98K may trigger a growth scenario up to $112K.

News background

Riot Platforms, the fourth-largest bitcoin mining company by bitcoin reserves, mined 463 BTC in April and sold 475 BTC for $38.8 million. The firm sold coins from the reserve for the first time in about a year.

BlackRock’s IBIT is the defining contribution to the ETF’s positive performance. According to Lookonchain, BlackRock additionally purchased 5,613 BTC (over $529 million). The company now holds 620,252 BTC (worth over $58bn).

Bitwise investment director Matt Hougan said the crypto market could face difficulties this summer if the US Congress does not continue to work on profile bills. He noted a bill to regulate stablecoins, the passage of which has been delayed.

Eurozone retail sales fall -0.1% mom in March

Eurozone retail sales slipped by -0.1% mom in March, in line with expectations. The breakdown shows marginal declines across key categories, with food, drinks, and tobacco sales down -0.1%, and non-food products (excluding fuel) also falling -0.1%. Only automotive fuel recorded a modest rise, up 0.4%.

Across the broader EU, retail trade also declined -0.1% mom. Notable contractions were seen in Slovenia (-2.0%), Estonia (-1.3%), and Slovakia (-0.9%). Malta led the gainers with a 2.0% increase, followed by Belgium, Croatia (both +1.4%), and Bulgaria (+1.1%).