Sample Category Title

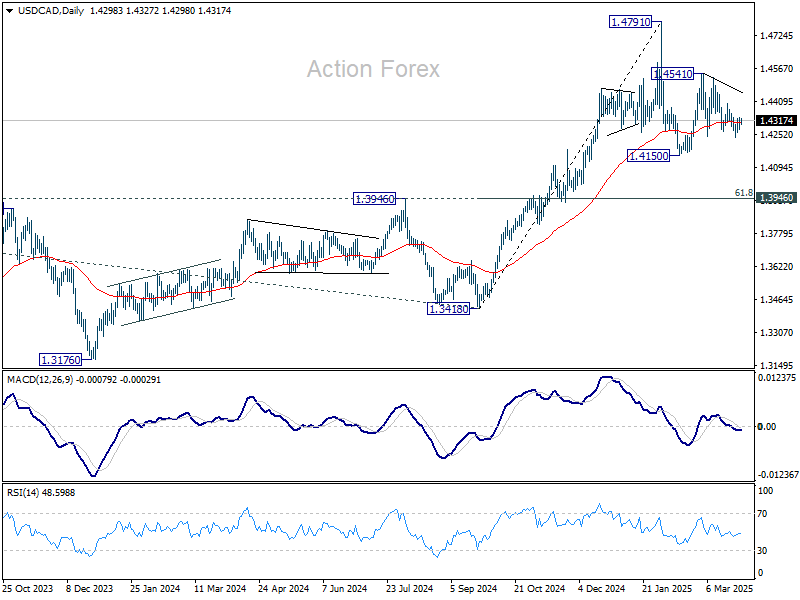

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4286; (P) 1.4310; (R1) 1.4342; More...

Intraday bias in USD/CAD stays neutral for the moment. Overall, corrective pattern from 1.4791 is still extending. On the upside, break of 1.4400 will argue that it's still in the second leg, and turn bias to the upside for 1.4541 resistance. On the downside, break of 1.4238 will suggest that the third leg has already started for 1.4150 and below.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

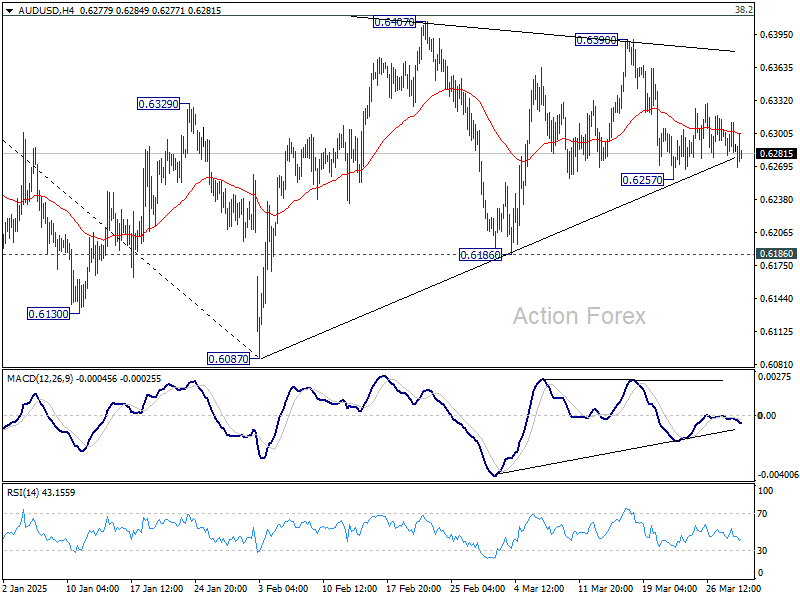

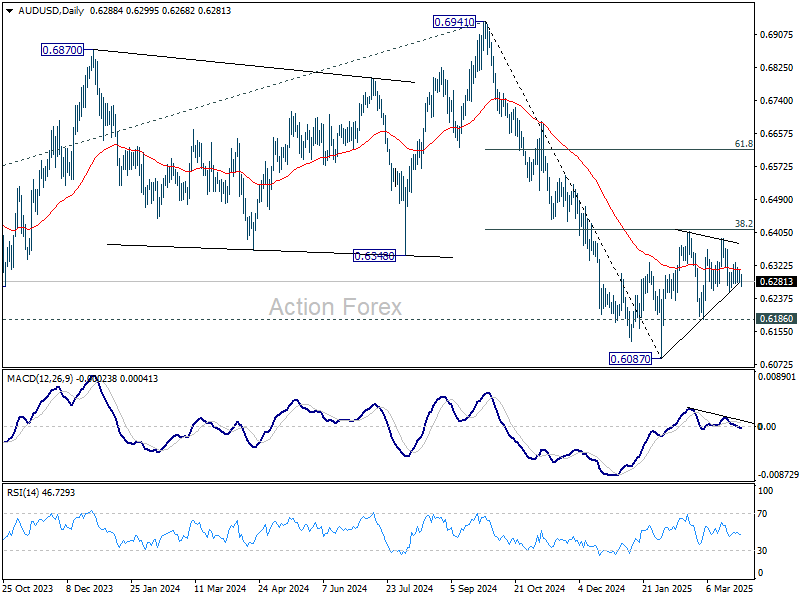

AUD/USD Daily Report

Daily Pivots: (S1) 0.6275; (P) 0.6293; (R1) 0.6306; More...

Intraday bias in AUD/USD remains neutral as sideway trading continues. On the downside, below 0.6257 will target 0.6186 support first. Firm break there will indicate that corrective pattern from 0.6087 has completed and larger fall from 0.6941 is ready to resume. For now, outlook will stay bearish as long as 38.2% retracement of 0.6941 to 0.6087 at 0.6413 holds, in case of another recovery.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6474) holds.

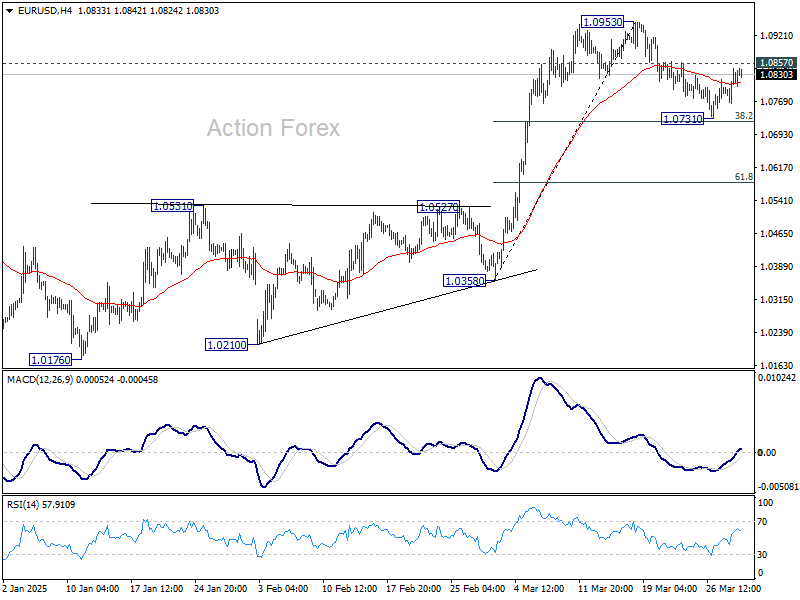

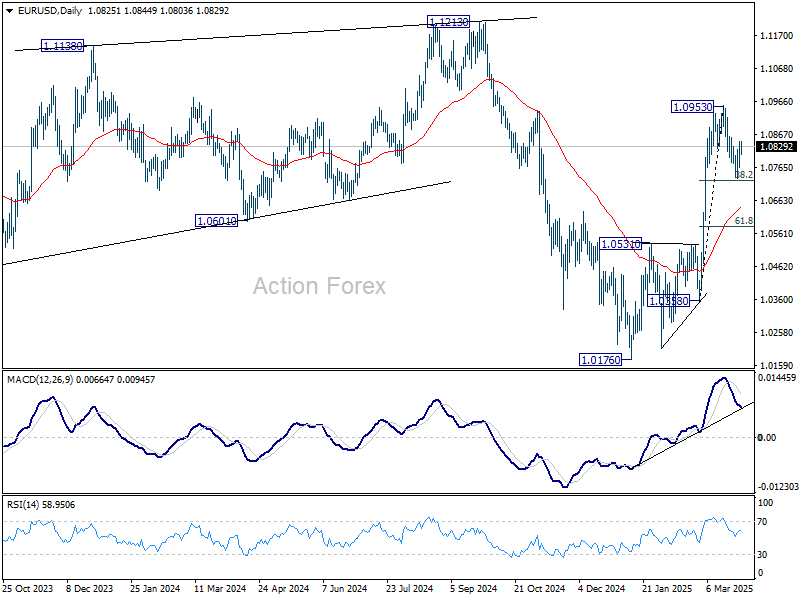

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0782; (P) 1.0813; (R1) 1.0862; More...

Intraday bias in EUR/USD stays neutral for the moment. On the upside, break of 1.0857 resistance will indicate that correction from 1.0963 has completed already. Retest of 1.0953 should be seen first. Firm break there will resume the rally from 1.0176 towards 1.1274 key resistance. In any case, outlook will remain bullish as long as 38.2% retracement of 1.0358 to 1.0953 at 1.0726 holds.

In the bigger picture, prior strong break of 55 W EMA (now at 1.0692) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

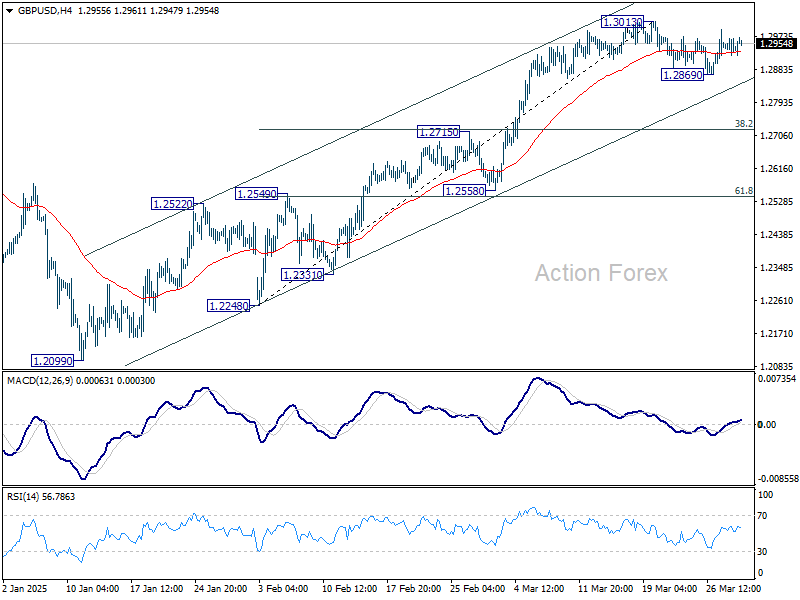

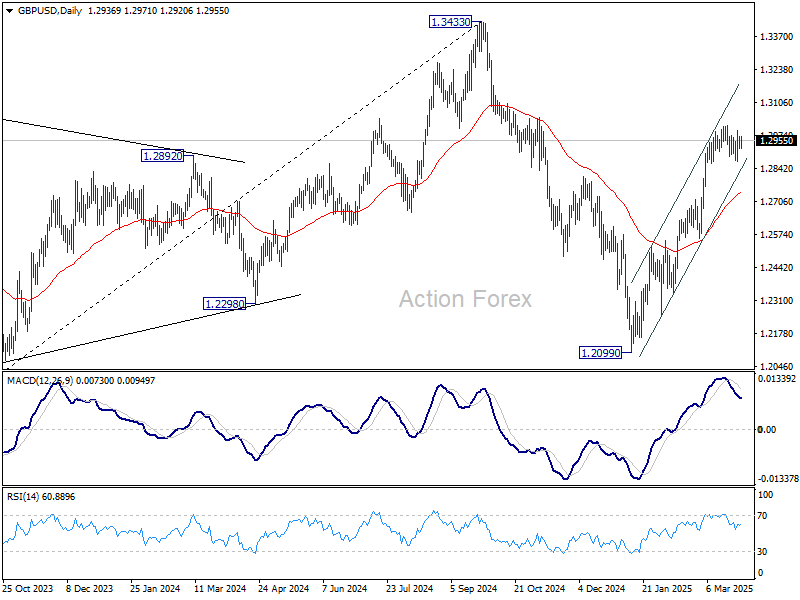

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2922; (P) 1.2945; (R1) 1.2968; More...

Intraday bias in GBP/USD remains neutral for the moment, as consolidations continue below 1.3013. On the downside, below 1.2869 will bring deeper correction. But downside should be contained above 38.2% retracement of 1.2248 to 1.3013 at 1.2721. On the upside, break of 1.3013 will resume the rally from 1.2099 towards 1.3433 high.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance (2021 high). This will now remain the favored case as long as 1.2099 support holds.

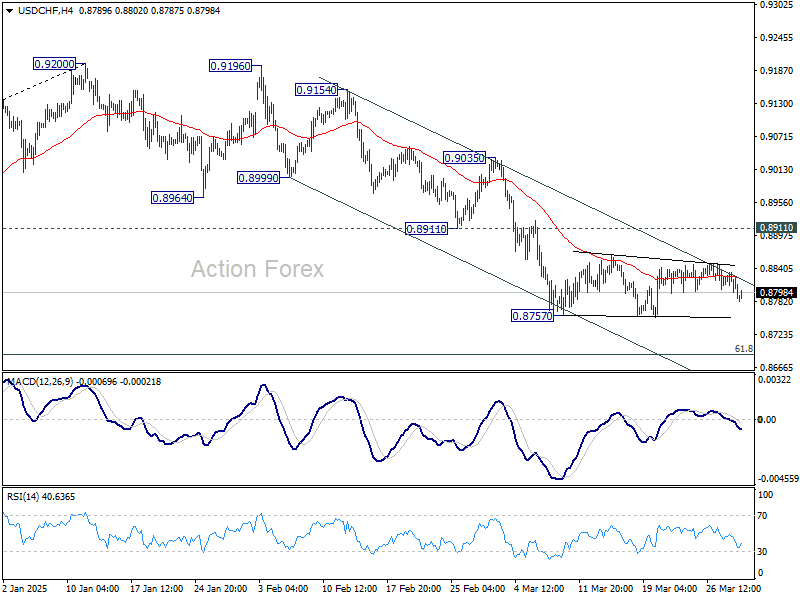

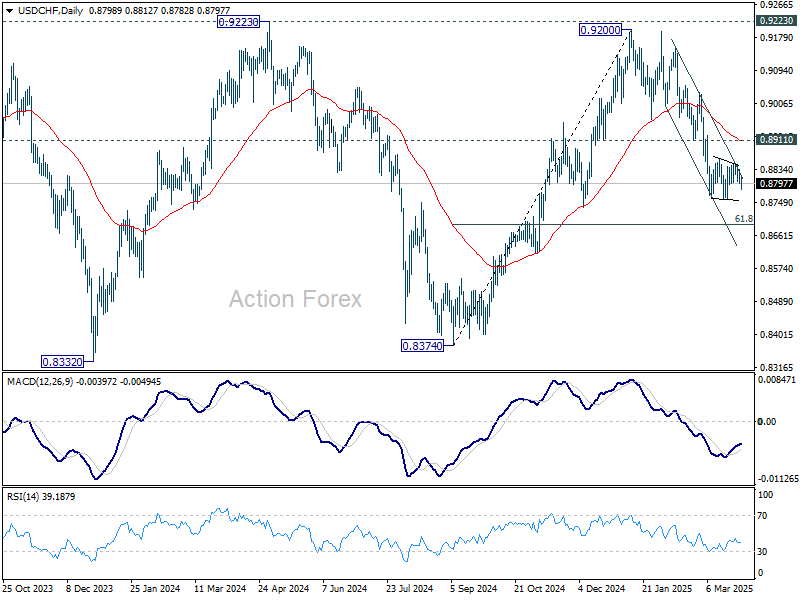

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8794; (P) 0.8814; (R1) 0.8829; More…

USD/CHF is still bounded in range trading above 0.8757 and intraday bias remains neutral. In case of stronger recovery, upside should be limited by 0.8911 support turned resistance. On the downside, break of 0.8757 will resume the fall from 0.9200 to 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

Risk Selloff Continues, Gold Renews Record

The tariff talk remains on the headlines as the Liberation Day approaches. Risk appetite is nowhere to be found, the US dollar is weak, gold continues to extend gains into uncharted territories and oil bulls remain unreactive to the news that Trump is pissed off with Putin for unveiling plans for the next Ukrainian leadership.

Last week’s US GDP update showed a slightly better reading on Thursday but growth in US GDP fell from above 3% to 2.4% in Q4 and is expected to contract by nearly 3% in Q1 according to the latest update from Atlanta Fed’s GDP Now forecast.

The core PCE, on the other hand, advanced to 2.8% instead of a steady 2.7% read expected by analysts. And the University of Michigan’s inflation expectations keep rising while sentiment keeps dropping. In summary, the US data hints at slowing economy and rising inflationary pressures. That’s the worst possible combination for risk sentiment.

Good news is that the Federal Reserve (Fed) doves are not going away with higher inflation numbers as the rapid fall in growth figures look more concerning than the inflation pick up. Therefore the Fed is expected to cut the rates in June – despite unideal trend in inflationary pressures – with more than 80% probability. The pricing in the bond markets tell the same story. The US 2-year yield – that best captures the Fed rate expectations - dropped below 4% last week and has settled near 3.85% this morning. Alas, even the falling yields and the rising dovish Fed expectations are unable to give a smile to investors. The S&P500 lost nearly 2% yesterday and is set to end the month with more than 6% losses – while seasonally speaking, March could’ve been a good month. Nasdaq 100 was hit by a 2.60% selloff. CoreWeave – the Nvidia-backed cloud computing company specialized in AI – had quite a disappointing debut on Nasdaq. The Dow Jones, small and mid-cap indices all traded down between 1.5 and 2% as well. Stocks in Europe returned to the lowest levels in two weeks, as gold continued to advance towards fresh high, the price of an ounce is trading above the $3110 mark this morning as the selloff continues in Asia with Nikkei down 1.5% on Monday despite data pointing at a 2.5% jump in industrial production in February and the CSI 300 is down 1% at the time of writing despite a set of better than expected PMI numbers.

Oil, on the other hand, is down this morning despite Donald Trump being ‘pissed off with Putin’ for suggesting ways to install new leadership in Ukraine by sidelining President Zelensky – a situation that could lead to ‘secondary tariffs’ on Russian oil. Alas, oil bulls are unable to rebound on the news this morning. Last week’s failure to clear the $70pb resistance is now leading to a toppish sentiment, and the latter is reinforced by gloomy growth expectations and OPEC+ plans to start restoring production from next month.

In the FX, the US dollar reversed an attempt to rebound from the March dip and is down for the third session on mediocre growth expectations for the US economy. The EURUSD found support near its 200-DMA last week. Released last Friday, the French and Spanish early inflation figures for March came in softer than expected, providing more room for the European Central Bank (ECB) to stay accommodative to support growth. The euro’s appreciation and the weakening energy prices are also supportive of European growth.

Speaking of growth, the British GDP update surprised to the upside on Friday giving Cable an additional reason to stay strong against the US dollar, though sterling remains offered against the euro.

In summary, the euro is looking stronger than sterling and the dollar, while the US dollar has become the weakest link among the three.

This week, investors will continue to watch the Eurozone inflation numbers and the US jobs data. The expectations are weak. If the Liberation Day doesn’t lead to a relief rebound in the US dollar, the euro could make an attempt above the 1.10 mark against the dollar, and Cable could break the back of the 1.30 offers.

A Week in the Name of Tariffs

In focus today

In the euro area, focus turns to the German inflation data for March that we receive ahead of the euro area data tomorrow. Last week, inflation in France and Spain came in lower than expected, in a positive sign for the ECB, and it will be interesting if Germany shows the same development. We expect euro area HICP inflation to decline from 2.3% y/y to 2.1% y/y tomorrow due to energy and services inflation.

In China, the Caixin PMI manufacturing, which is the private survey, will be released overnight. Consensus is for a small decline from 50.8 to 50.6 but we see upside risks to this estimate based on stronger signals from other indicators such as the Yicai index and rise in metal prices in March.

In Denmark, the revised 2024 Q4 national accounts are released. The first print showed impressive GDP growth of 1.6% q/q. However, the uncertainty surrounding flash releases is always significant, and it will be interesting to see the extent of any revisions.

In Sweden, today marks the deadline for the major wage negotiations, with significant pressure on industry parties to reach an agreement due to many expiring contracts. The initial offer proposed a three-year deal at 7.7%, which is lower than expected and potentially indicates downward risks for wage forecasts.

In Australia, early tomorrow morning, we expect the Reserve Bank of Australia (RBA) to hold its Cash Rate unchanged at 4.10% in line with consensus. RBA initiated its rate cutting cycle in the previous meeting but did not pre-commit to delivering further easing. Markets price in 2-3 cuts for the rest of 2025 but see a 90% probability of RBA staying on hold tomorrow.

In Japan, the Bank of Japan will publish its quarterly Tankan business survey overnight. PMIs suggest Q1 has been strong overall but based on a sharp decline in March, it will be interesting to see what the Tankan survey shows. Businesses are surveyed from late-February to late-March. Not least favourable wage negotiations this spring supports the outlook for further BoJ hikes, but a solid Tankan survey is also a prerequisite.

The main focus this week will most likely centre on tariffs - particularly from the US, with new broad-based tariffs expected to be enacted and reciprocal tariffs due to be announced, both on Wednesday. Overnight, he said they will include "all countries", ad odds with what has been communicated earlier. Read more on Research US: Trump's 'Liberation Day' - What to expect?, 27 March. We will also closely follow statements regarding Trump's potential new tariffs on Russian oil buyers. The week will conclude with the US March Jobs Report scheduled for release on Friday.

Economic and market news

What happened Friday and over the weekend

In the US, core PCE inflation increased 0.4% m/m (cons. 0.3% m/m) somewhat above expectations, while headline PCE increased 0.3% m/m in line with consensus. Real consumption volume growth remained muted at only +0.1% m/m SA (from -0.6% m/m) as personal savings rate remains somewhat elevated at 4.6%. This could reflect more cautious consumer sentiment.

In China, the official composite PMI index increased to 51.4 in March, up from 51.1 in February. Non-manufacturing PMI rose to 50.8 from 50.4 the previous month, reflecting stronger activity in the services sector, while the manufacturing PMI climbed to a one-year high of 50.5, up from 50.2, in line with expectations as business conditions continued to improve.

In Norway, the unemployment rate (SA) was unchanged at 2.0 % in March, as expected. Also, new vacancies were slightly down which could imply some slowdown in labour demand, though it remains at a historically high level. Retail sales dropped 0.1 % m/m in February, as consensus expected which takes the 3M/3M growth to 1.3 %. So, clear signs of a pick-up in private consumption on the back of higher real wage growth and a strong labour market. Overall, the data should be neutral to Norges Bank.

In Japan, the summary of opinions from the BoJ's March meeting were released on Friday. It contained a lot of recognition of the recent strong wage results, which highlights the importance of this as a prerequisite for hiking rates further. That said, there is also expressed some worry that investment is too weak among SMEs, which potentially indicates that the current wage growth is not sustainable. The uncertainty stemming from the US also gets a lot of attention, which supports our view that the BoJ will move carefully ahead but find room for another two hikes this year.

In geopolitics, U.S. President Donald Trump expressed anger towards Russian President Vladimir Putin and threatened to impose tariffs of 25-50% on imports from countries that purchase Russian oil if Russia obstructs efforts to end the Ukraine war. This move follows Putin's comments about the credibility of Ukrainian President Volodymyr Zelenskiy's leadership. Trump plans to discuss the situation with Putin in a phone call later this week.

Equities: Global equities declined on Friday, led by the US, due to a lack of risk appetite leading up to the weekend and a few days ahead of the quarter turn and "Liberation Day" as the US President has called the 2 April massive tariff increase.

Are there any surprises in this? Yes and no. On one hand, it is known that President Trump wants all negotiating partners to be as uncertain as possible about his next move, and the biggest negotiation effect from tariffs comes in the form of threats of the tariffs.

Hence, it is no surprise that risk-takers should be worried at a time when US trade politics are set to be turned upside down, with average trade-weighted tariffs potentially increasing towards 18% from a mere 3% going into the year.

Thus, one could call it a no no-brainer the VIX is high and risk-appetite is dropping, but on the other hand, there is a fundamental belief that tariffs are not beneficial for the US economy and, at some point, will be rolled back or reduced when Trump can declare a publicity victory against trading partners and tell US citizens he has made America great again.

Similarly, this is adding to the risk a recession, which we ultimately do not believe Trumps is willing to do. Therefore, that is why the destructive politics are not a no-brainer for us when considering risky assets.

One of the most interesting perspectives in the late Friday cash session was the "true" risk-off behaviour.

Firstly, cyclicals massively underperformed defensives, with even defensives being lower.

Secondly, yields took a hit, suggesting the market message is not a stagflationary environment but rather just a hit to growth and increased risk of recession.

US equity indices on Friday: Dow -1.7%, S&P 500 -2.0%, Nasdaq -2.7%, and Russell 2000 -2.1%.

The risk-off mode is continuing in Asia, with the yen being the safe haven. The Nikkei is down more than 4% at the time of writing, and other export and manufacturing countries are heavily down this morning.

Futures in Europe and the US are also sharply down this morning, along with the long end of the US yield curve.

FI&FX: Treasuries ended last week on a strong note as PCE data, University of Michigan and Trump's tariff threats in combination sent markets into stagnation mode. US equities dropped sharply with tech leading the selloff. Within FX JPY outperformed vs G10 peers and EUR/USD climbed above 11.08. EUR/NOK edged higher and ended Friday at 11.35. EUR/SEK gained 4-5 figures and closed the week at 11.84. Today, SEK enters a dividend-heavy period with SEK122bn to be paid out this week alone (see RtM Sweden, 14 Mar for details). In general, markets' eyes and ears are now on this week's tariff announcements.

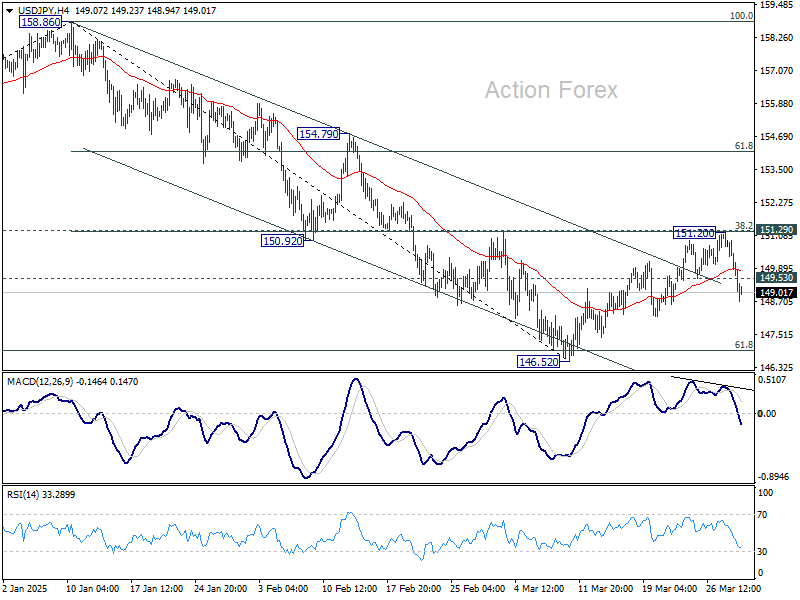

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.26; (P) 150.23; (R1) 150.79; More...

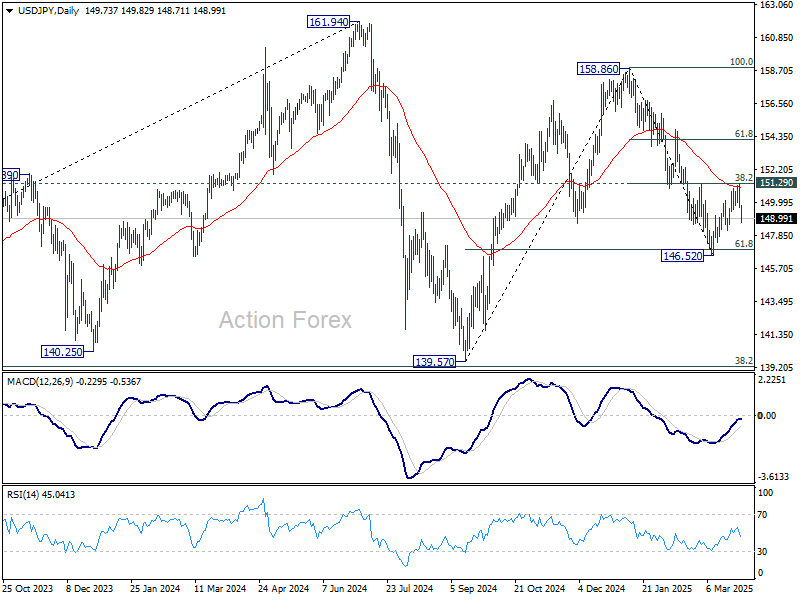

USD/JPY's break of 149.53 support suggests that corrective recovery has already completed at 151.20. That came just ahead of 151.29 cluster resistance (38.2% retracement of 158.86 to 146.52 at 151.23). Intraday bias is back on the downside for retesting 146.52 low first. Firm break there will resume whole decline from 158.86 towards 139.57 support next. For now, outlook will remain bearish as long as 151.23/9 holds in case of recovery.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Nikkei Crashes as Auto Tariff Reality Hits, Yen and Gold Soar as “Liberation Day” Looms

Risk aversion erupted across Asian markets today, with Japan bearing the brunt of the selloff. Nikkei plummeted by nearly than -4%, marking its worst day in months and sending the index to its lowest level since September last year. The sharp move comes as traders scramble to reassess the impact of US President Donald Trump's 25% tariffs on all automobile imports, which are set to take effect Thursday. Previously, there had been some hope that Japan, a long-standing US ally, might be spared. But with no signs of exemption, the market is now forcefully pricing in the worst-case scenario.

Japanese Yen surged broadly on the wave of safe-haven buying, with investors rushing to unwind risk trades amid intensifying global trade tensions. The Yen's rally was amplified by the direct blow to Japan's key auto sector, a pillar of its export economy. The sharp shift in sentiment underscores how markets had underappreciated the possibility of Japan being caught in the crossfire of Trump's aggressive trade policy.

The turbulence comes just days ahead of the so-called "Liberation Day" on Wednesday, when the US is expected to announce sweeping reciprocal tariffs on trading partners. The threat of a global trade war escalation is now overtaking all other themes in the market, overshadowing this week’s otherwise significant calendar including the US ISM indexes, non-farm payrolls, Eurozone inflation, and RBA rate decision.

Overall in the currency markets, Yen is by far the top performer today so far, followed by another safe haven Swiss Franc. Sterling is holding up better than most, helped by reports that British Prime Minister Keir Starmer and President Trump had “productive” trade talks over the weekend, suggesting the UK may be spared from some of the harsher tariff measures.

Commodity currencies are the clear losers, with Kiwi and Aussie at the bottom of the board amid their risk-sensitive profiles and economic ties to China. Loonie, Dollar, and Euro are also under pressure, though less dramatically.

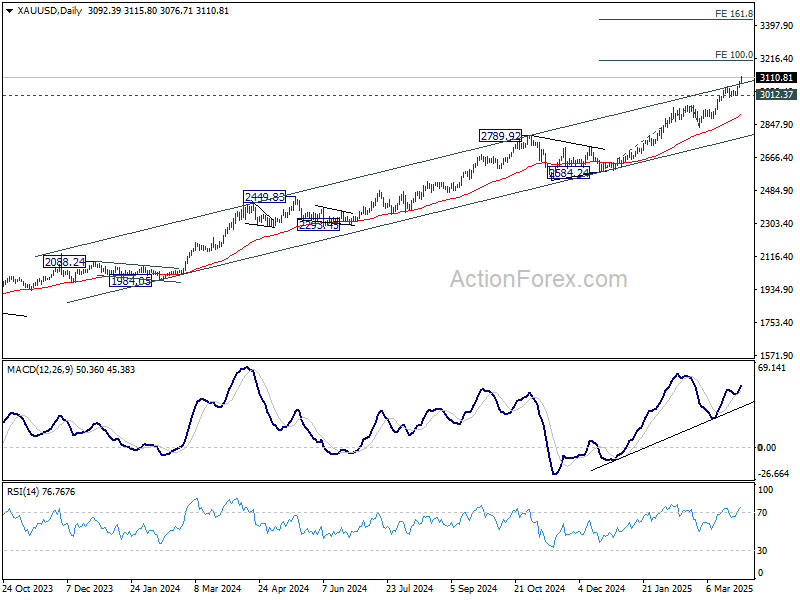

Risk aversion also pushed Gold to new record high above 3100 mark. Technically, the break of medium term channel resistance is a significant sign of upside acceleration. For now, near term outlook will stay bullish as long as 3012.27 support holds. Next target is 100% projection of 2584.24 to 2956.09 from 2832.41 at 3204.26. But considering current momentum, Gold might indeed be having an eye on 161.8% projection at 3434.06, or even 3500 psychological level already.

In Asia, at the time of writing, Nikkei is down -3.95%. Hong Kong HSI is down -1.48%. China Shanghai SSE is down -0.68%. Singapore Strait Times is down -0.23%. Japan 10-year JGB yield is down -0.044 at 1.510.

Japan's industrial production beats with 2.5% mom growth in Feb

Japan's industrial production rose 2.5% mom in February, beating market expectations of 1.9% mom gain. The strong growth was driven by key tech-related sectors, with chipmaking machinery output jumping 8.2% and electronic parts and devices surging 10.1%.

A survey by Ministry of Economy, Trade and Industry projects continued, albeit modest, gains in output of 0.6% mom in March and 0.1% mom in April.

While the headline data is encouraging, the METI acknowledged that the outlook could quickly shift. Though no direct production impact from the proposed US tariffs has been reported yet, METI emphasized the need to monitor the situation more closely going forward.

On the consumer side, retail sales grew just 1.4% yoy, missing expectations of a 2.4% rise.

NZ ANZ business confidence dips to 57.5, rising inflation expectations stir doubts over RBNZ cuts

New Zealand’s ANZ Business Confidence dipped slightly from 58.4 to 57.5 in March. Own Activity Outlook improved from 45.1 to 48.6.

However, the data also brought a clear warning on inflationary pressures. Cost expectations surged from 71.3 to 74.1, the highest level in a year. Pricing intentions climbed from 46.2 to 51.3, marking the strongest since May 2023.

Perhaps more importantly, one-year inflation expectations also ticked up from 2.53% to 2.63%, inching further above the RBNZ’s 2% midpoint target.

ANZ flagged the rising inflation signals as “a little disconcerting,” cautioning that these developments could influence how enthusiastic RBNZ will be about delivering further rate cuts.

A rate cut at the April meeting appears locked in, and a second in May is viewed as likely. However, ANZ noted that the odds of a third cut in July are now “more of a coin toss.”

China’s official PMI manufacturing rises to 50.5, but labor market lags

China’s official PMI data for March offered modest optimism, with the manufacturing index rising from 50.2 to 50.5, matching expectations and marking its highest level in a year.

Sub-indices for production and new orders both improved to 52.6 and 51.8, respectively. However, employment index slipped to 48.2, highlighting persistent weakness in labor market conditions within the manufacturing sector.

Non-manufacturing activity also improved slightly, with the PMI climbing from 50.4 to 50.8, beating expectations of 50.5.

Still, employment in the non-manufacturing sector deteriorated, with the index falling to 45.8, as both the services and construction sectors shed workers.

Central banks and top-tier data share spotlight with tariffs

Markets are understandably fixated on the looming April 2 announcement of reciprocal tariffs by the US. However, this week is also packed with central bank events and high-impact economic data that could shift sentiment and market direction.

RBA will be a key event, with broad consensus pointing to a hold at 4.10%. Despite some recent softness in data, RBA officials have maintained a modestly hawkish stance following the February rate cut. A follow-up move in April appears unlikely, especially with the next quarterly inflation report not due until April 30. The big four banks—CBA, Westpac, NAB, and ANZ—all expect the central bank to stay on hold this month.

Meanwhile, the US will release a slate of economic data, including ISM manufacturing and services indexes and the all-important non-farm payrolls report. ISM manufacturing dipped back into contraction in February, but the services side has remained resilient. So far, tariff threats have not shown up in the ISM data, but it's unclear whether that changes in March’s readings. The labor market remains a key variable—strong job growth would support Fed’s patient stance. But a sudden deterioration, though likely viewed as noise, could still rattle policymakers.

The Eurozone’s flash CPI will be equally important as speculation builds over a potential rate pause by the ECB. While some members have floated the idea of holding rates in April, data hasn’t been convincing enough to justify it. This week’s inflation print could be the deciding factor. Additionally, ECB minutes from the March meeting will be dissected for clues about internal divisions and how much weight is being placed on the evolving external risks like tariffs.

Beyond these, there are several key international releases to keep an eye on. Japan's Tankan business sentiment survey, Canada’s employment data, Swiss CPI, and China’s PMIs will round out a dense calendar.

Here are some highlights for the week:

- Monday: Japan industrial production, retail sales; New Zealand ANZ business confidence; China official PMIs; Germany import prices, retail sales, CPI flash; US Chicago PMI.

- Tuesday: Japan Tankan survey, PMI manufacturing final; China Caixin PMI manufacturing; RBA rate decision, Australia retail sales; Swiss retail sales; Eurozone PMI manufacturing final, CPI flash, unemployment rate; UK PMI manufacturing final; Canada PMI manufacturing; US ISM manufacturing.

- Wednesday: Japan monetary base; US ADP employment, factory orders.

- Thursday: Australia trade balance; China Caixin PMI services; Swiss CPI; Eurozone PMI services final, PPI, ECB accounts; UK PMI services final; Canada trade balance; US jobless claims, trade balance, ISM services.

- Friday: Japan household spending; Swiss unemployment rate; Germany factor orders; UK PMI construction; Canada employment; US non-farm payrolls.

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.26; (P) 150.23; (R1) 150.79; More...

USD/JPY's break of 149.53 support suggests that corrective recovery has already completed at 151.20. That came just ahead of 151.29 cluster resistance (38.2% retracement of 158.86 to 146.52 at 151.23). Intraday bias is back on the downside for retesting 146.52 low first. Firm break there will resume whole decline from 158.86 towards 139.57 support next. For now, outlook will remain bearish as long as 151.23/9 holds in case of recovery.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

China’s official PMI manufacturing rises to 50.5, but labor market lags

China’s official PMI data for March offered modest optimism, with the manufacturing index rising from 50.2 to 50.5, matching expectations and marking its highest level in a year.

Sub-indices for production and new orders both improved to 52.6 and 51.8, respectively. However, employment index slipped to 48.2, highlighting persistent weakness in labor market conditions within the manufacturing sector.

Non-manufacturing activity also improved slightly, with the PMI climbing from 50.4 to 50.8, beating expectations of 50.5.

Still, employment in the non-manufacturing sector deteriorated, with the index falling to 45.8, as both the services and construction sectors shed workers.