Sample Category Title

Global Trends Hit Pause, Consolidations to Follow Until Trump’s Liberation Day

The dominant trends that shaped Q1 in global markets appear to have run their course, with most major assets entering consolidation phase last week.

US stocks staged a mild recovery from steep selloff since mid-February, but upside momentum was notably weak. Meanwhile, Dollar, which had been under pressure throughout March, appeared to find a near-term bottom. Resilience of hard economic data in the US somewhat offset persistent concerns over trade disruptions.

In Europe, Euro and German DAX also lost steam. Optimism over Germany’s historic EUR 500B infrastructure and defense spending plan helped fuel a strong rally earlier in the month, but now traders are starting to price in political and implementation challenges ahead.

In Asia, sentiment toward China has been broadly positive in recent weeks, driven by policy support and hope for a consumer-led recovery. However, the rally in Hong Kong stocks, in particular, appears stretched.

Even Gold, after a powerful run to record highs, is struggling to overcome a key medium-term resistance zone.

What ties these developments together is a growing sense of caution ahead of the highly anticipated reciprocal tariffs set to be unveiled on April 2.

Market participants remain wary, especially after US President Donald Trump described the date as America’s “liberation day.” His mixed messaging on potential “flexibility” in applying the tariffs — while simultaneously rejecting carveouts — only adds to the confusion and uncertainty.

In this environment, broad-based risk appetite is likely to stay subdued. While tariff concerns may cap further upside in stocks and restrain Dollar’s rebound, traders are unlikely to make aggressive moves until more clarity emerges in early April.

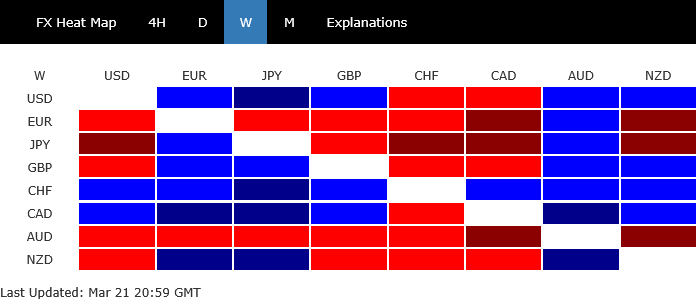

For the week, Swiss Franc led the performance chart, followed by Canadian Dollar and the Greenback. Aussie was the weakest, followed by Euro and Yen, while Kiwi and Sterling ended in the middle of the pack.

Fed Sparks Brief Moves, Markets Consolidate Ahead of April Tariff Showdown

US stock markets saw a brief bounce following Fed's decision to keep interest rates unchanged and maintain the median outlook for two rate cuts later this year. However, the optimism quickly faded, with major indexes settling back into their near-term ranges. Investors seemed to digest the Fed’s stance as largely expected, and without any significant surprises to break the prevailing sentiment stalemate.

The updated Summary of Economic Projections (SEP) hinted at some cautious acknowledgment of the economic toll from trade war. GDP forecasts were revised lower across the board, particularly for 2025 at 1.7%, but remained anchored around Fed’s longer-run estimate of 1.8% growth by 2026 and 2027. On the inflation front, core PCE was nudged higher to 2.8% for this year, up from the previous 2.5%. But projections for 2026 and 2027 held steady at 2.2% and 2.0% respectively.

Overall, the projections suggest that while tariffs may impact near-term economy activity, Fed sees no long-term deviation from trend growth. Also, Fed expects the inflationary pressure from tariffs to be "transitory", fading after the initial pass-through period.

Still, the assumption remains a fragile one. With President Donald Trump’s sweeping reciprocal and sectoral tariff plans due for rollout on April 2, markets are bracing for more clarity—or chaos. The lack of concrete detail on implementation leaves room for policy whiplash, adding to the uncertainty businesses and consumers are already grappling with.

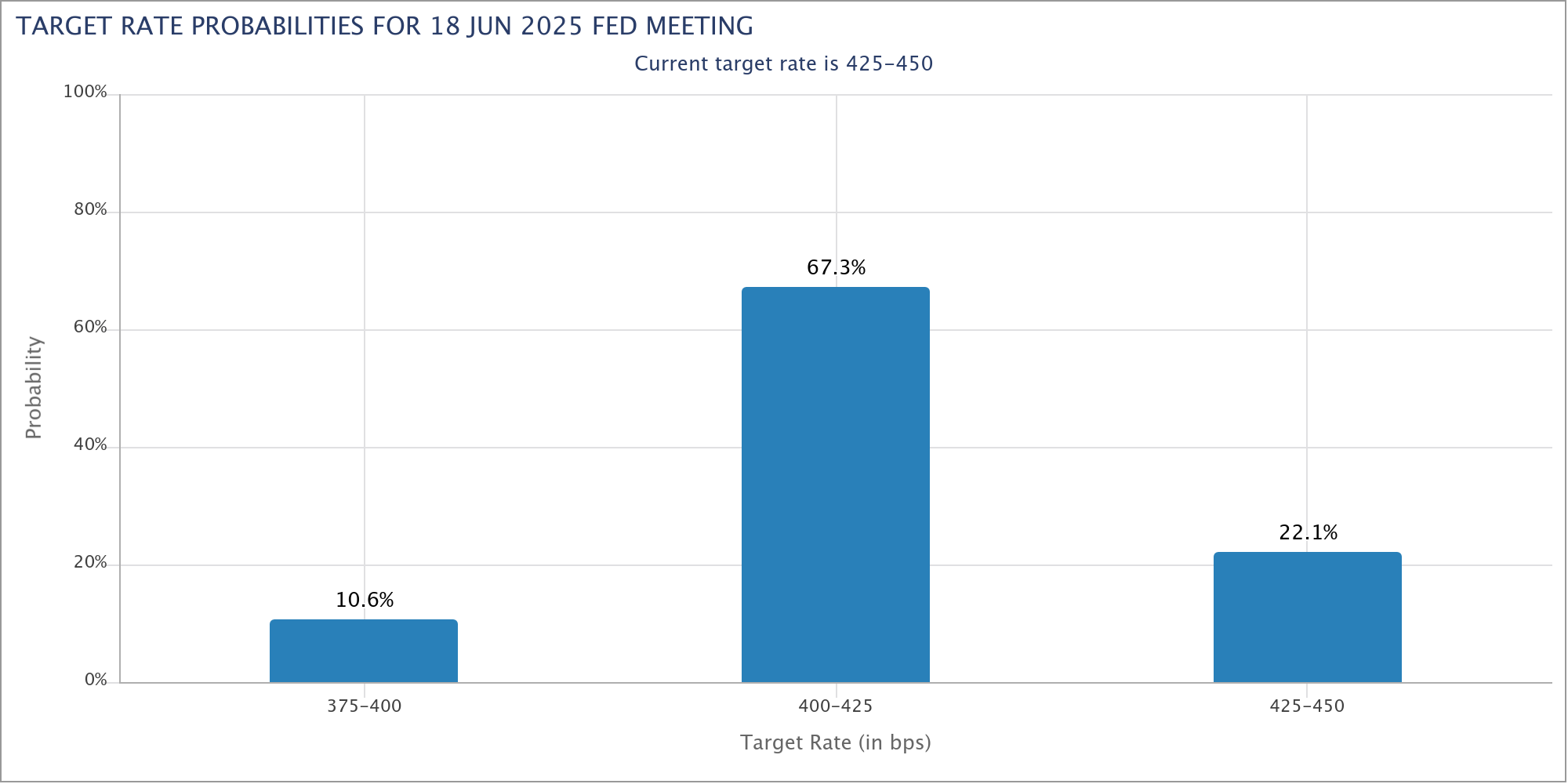

For now, Fed fund futures imply an 88% chance of a rate cut in June, followed by around 70% odds of another cut in September. Still, those odds remain sensitive to upcoming inflation readings, consumer sentiment, and of course, any fresh headlines out of Washington on trade.

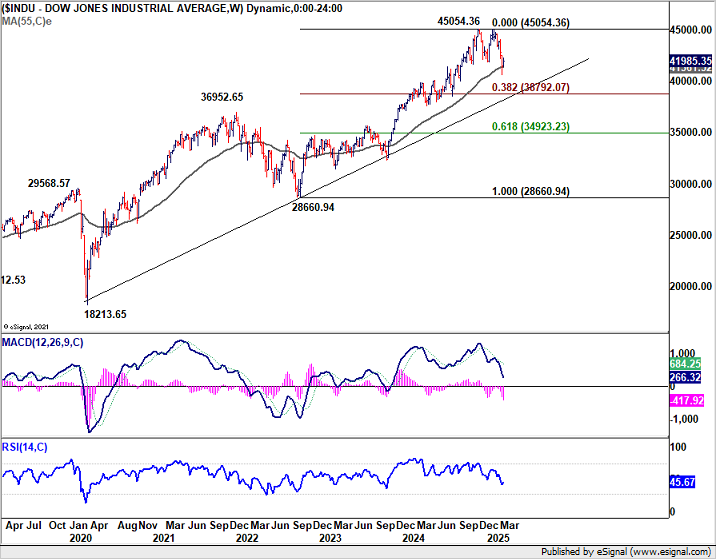

Technically, DOW gyrated higher last week after forming a short term bottom at 40661.77 earlier in the month. The structure of the recovery so far suggests that it's merely a corrective bounce. Further decline is expected as long as 55 D EMA (now at 43027.95) holds. Fall from 45054.36 is seen as corrective the whole up trend from 28660.94. On resumption, DOW should target 38.2% retracement of 28660.94 to 45054.36 at 38792.07.

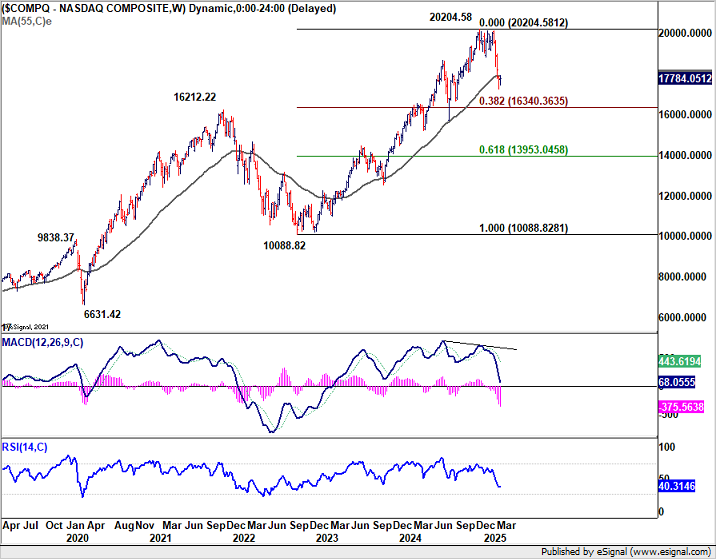

Similarly, NASDAQ turned sideway after forming a short term bottom at 17238.23. While stronger recovery cannot be ruled out, risk will stay on the downside as long as 55 D EMA (now at 18753.98) holds. Fall from 20204.58 is seen as a correction to the ups trend from 10088.82. Break of 17238.23 will target 38.2% retracement of 10088.82 to 20204.58 at 16340.36.

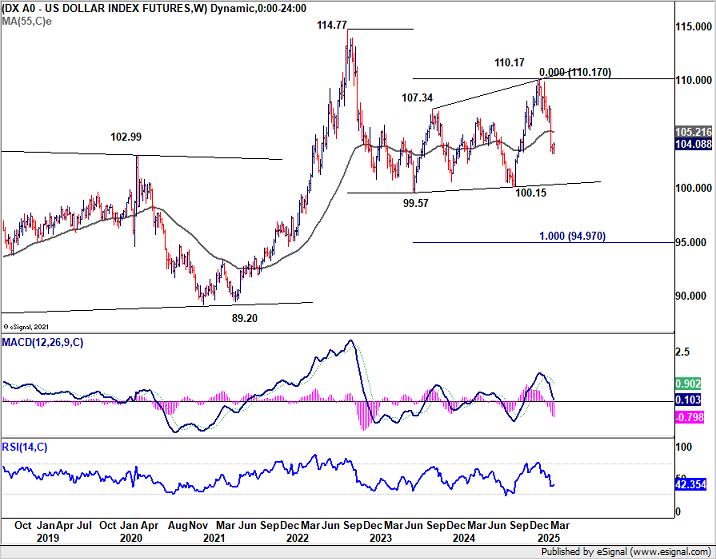

Dollar Index should have formed a short term bottom at 103.19 and turned into consolidations already. Further recovery might be seen in the near term. But there would be strong resistance between 55 W EMA (105.21) and 55 D EMA (now at 105.91) to limit upside. Break of 103.19 will resume the fall from 110.17 to 99.57/100.15 support zone.

Euro and DAX Enter Consolidation as Focus Shifts to German Coalition Talks

Both Euro and German DAX may have peaked in the near term, as the initial optimism surrounding Germany’s sweeping fiscal expansion plan begins to fade. The EUR 500 B infrastructure and defense package, along with reforms to the long-standing debt brake rule, passed the Bundestag earlier in the week and was approved by the Bundesrat on Friday. With the legislative hurdles cleared, investor attention is now turning to the political process of implementing the plan.

Chancellor-in-waiting Friedrich Merz is aiming to finalize a coalition with SPD by Easter, but the path forward is far from certain. Migration policy remains a key stumbling block. At the same time, Merz is already facing internal criticism from parts of his CDU/CSU bloc for what some see as an overly generous fiscal shift. These political frictions would be the uncertainty that could weigh on both sentiment and market performance in the coming weeks.

Even in the absence of external risks like US tariffs, the timeline for tangible economic impact from the spending package remains distant. A regular budget for 2025 may not be passed until mid-year, meaning it could be months before new investments begin to support growth.

A consolidation phase may now set in for German equities and Euro, lasting at least until Merz completes the coalition negotiations.

Technically, while DAX still has some room to climb, considering bearish divergence condition in D MACD, upside will likely be limited by 161.8% projection of 14630.21 to 18892.92 from 17024.82 at 23921.87, or in short 24k mark. Break of 22226.34 support will suggest that a correction has started to digest the rally from 17024.82.

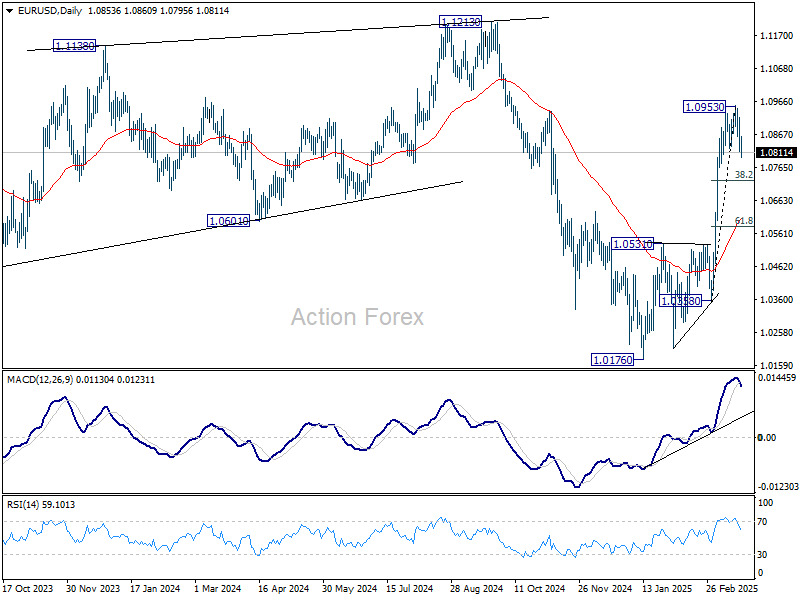

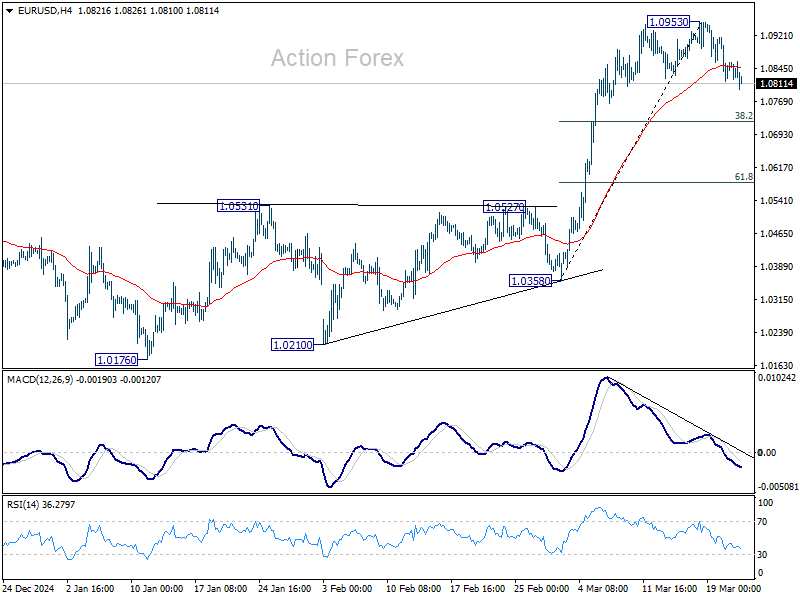

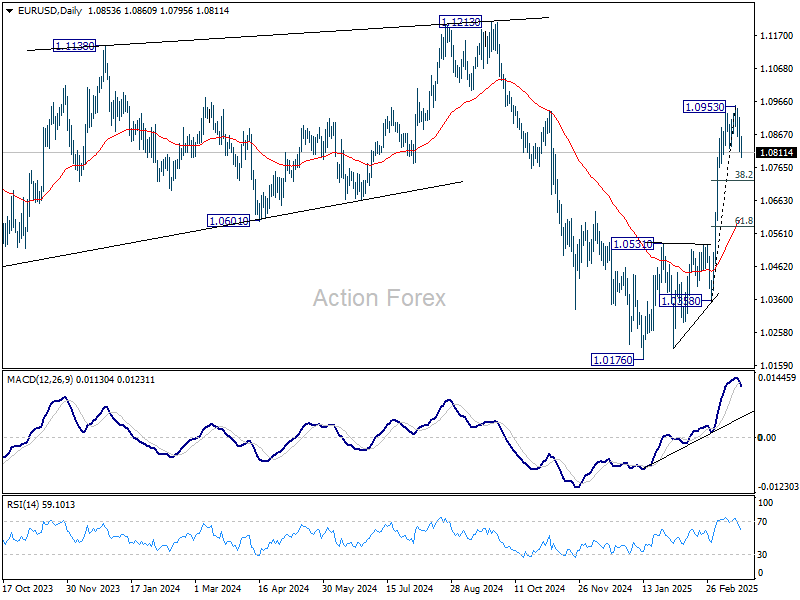

EUR/USD should have completed a short term top at 1.0953 after last week's pull back. Deeper fall might be seen to 38.2% retracement of 1.0358 to 1.0953 at 1.0726. But strong rebound is expected from there to set the range for a near term corrective pattern.

China Optimism and HSI Rally Nears Exhaustion, Aussie at Risk

After weeks of bullish sentiment toward China, markets in Asia may be poised for a meaningful correction. Much of the recent optimism was driven by Beijing’s ambitious "special action plan" to stimulate domestic consumption and the buzz surrounding AI startup DeepSeek. However, as attention shifts from announcements to implementation, investors are turning cautious on whether these initiatives will yield the hoped-for near-term growth.

In particular, the rally in Hong Kong stocks appears increasingly stretched. HSI had made a strong push higher since January, but it's now facing a tough hurdle at the psychologically significant 25,000 mark. That level also aligns closely 100% projection of 16964.28 to 23241.74 from 18671.49 at 24948.95. Combined with bearish divergence in daily MACD, there's a rising risk that profit-taking could be triggered on any failure to break this resistance zone.

Firm break of 23198.13 support would be a key signal that the rally has topped for the near term, opening the door for deeper pullback toward the 55 D EMA (now at 22302.72) or even below.

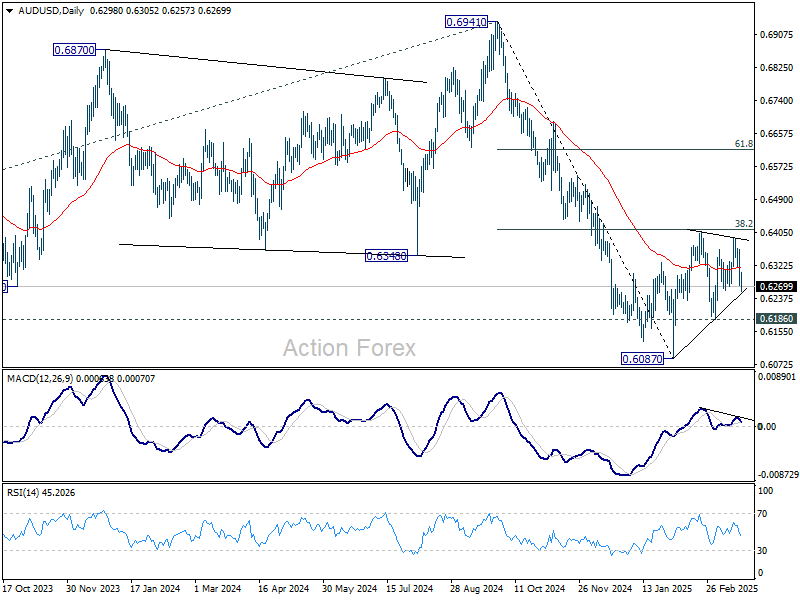

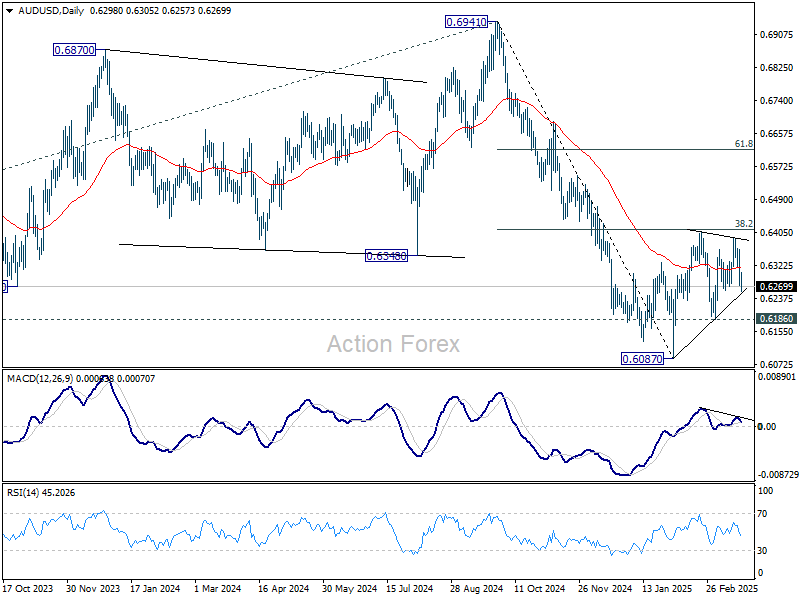

Australian Dollar is especially vulnerable in this bearish scenario, given its strong trade ties with China. Sustained break of near term trend line support (now at 0.6251) will argue that consolidation pattern from 0.6087 has already completed. Further break of 0.6186 support will solidify bearish case and suggest that fall from 0.6941 is ready to resume.

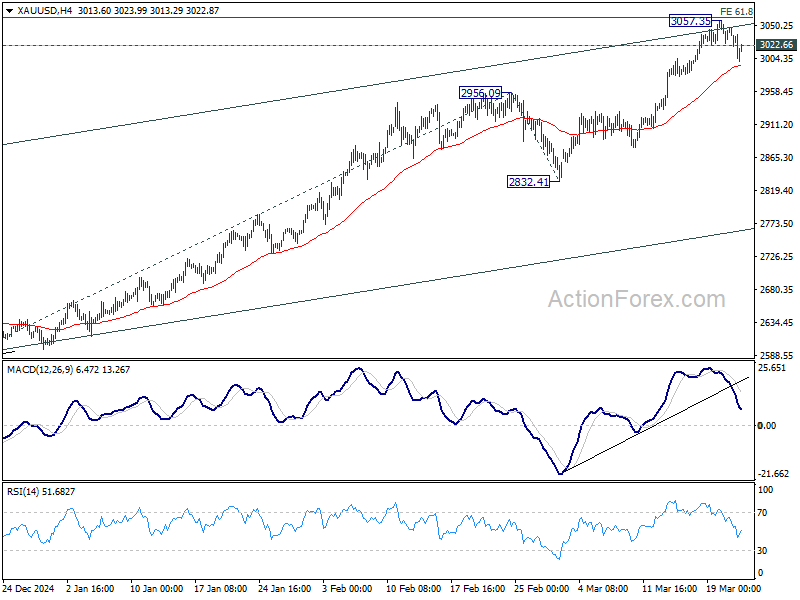

Gold Correction Looms With Rejection by Key Resistance Zone

Gold’s impressive record run may have reached a near-term peak as it ran into a confluence of critical resistance zone. The levels include 61.8% projection of 2584.24 to 2956.09 from 2832.41 at 3062.21, and more importantly, medium-term rising channel resistance.

Sustained break of 55 4H EMA (now at 2993.64) should confirm this view and bring deeper pull back to 2956.09 resistance turned support or a bit lower. But strong support should be seen from 55 D EMA (now at 2862.52) to contain downside, and bring rebound,, at least on first attempt.

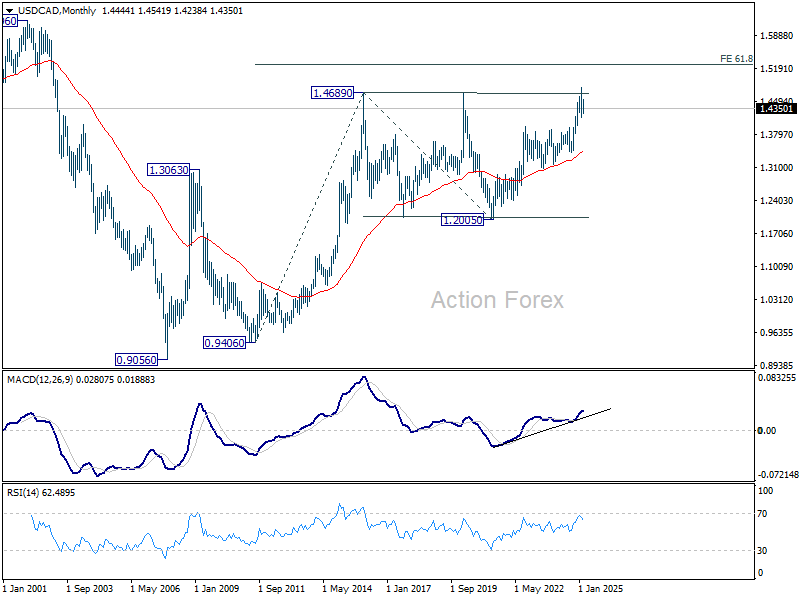

USD/CAD Weekly Outlook

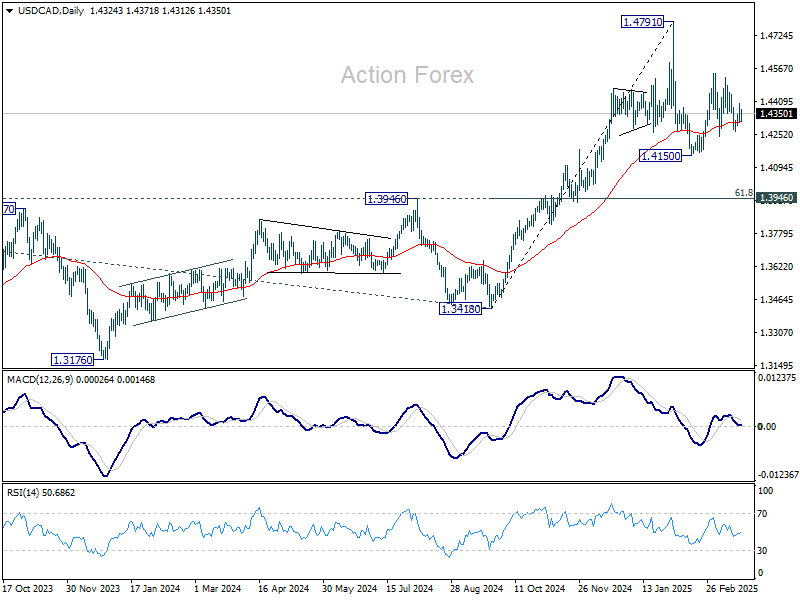

Range trading continued in USD/CAD last week and outlook is unchanged. Initial bias remains neutral this week first. Overall, price actions from 1.4791 are seen as a corrective pattern. On the upside, break of 1.4541 will extend the second leg from 1.4150 to retest 1.4791 high. On the downside, break of 1.4238 will argue that the third leg has already started through 1.4150 support.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

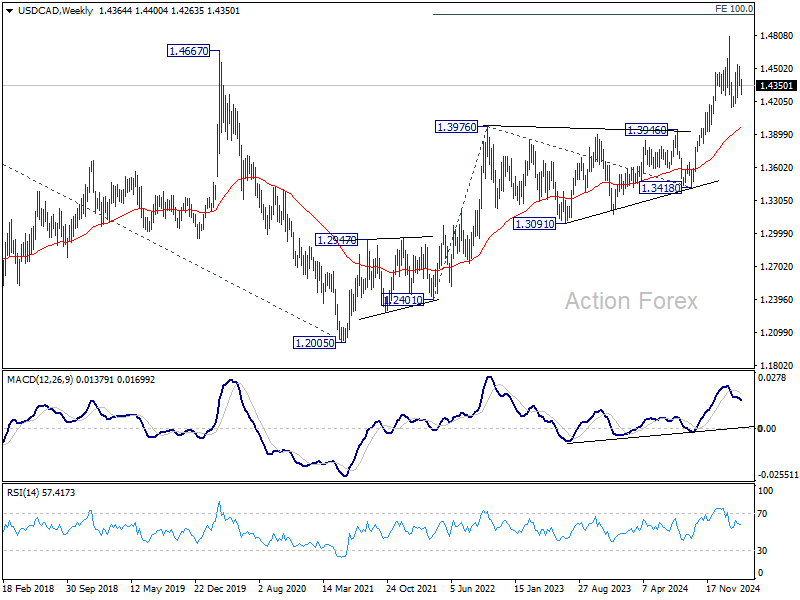

In the longer term picture, up trend from 0.9506 (2007 low) is in progress and possibly resuming. Next target is 61.8% projections of 0.9406 to 1.4689 from 1.2005 at 1.5270. While rejection by 1.4689 will delay the bullish case, further rally will remain in favor as long as 55 M EMA (1.3463) holds.

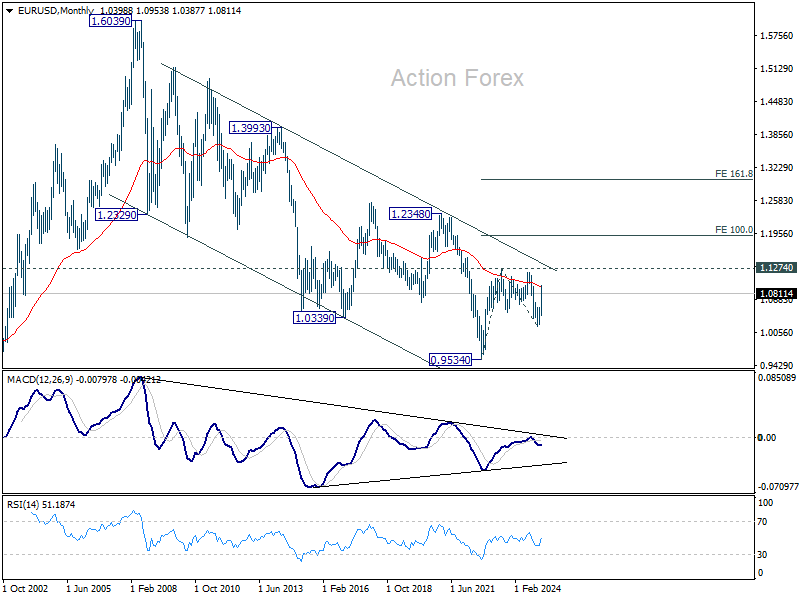

EUR/USD Weekly Outlook

EUR/USD reversed after edging higher to 1.0953 last week and a short term top should be formed. Initial bias is mildly on the downside this week for 38.2% retracement of 1.0358 to 1.0953 at 1.0726. Strong support should be seen there to bring rebound. On the upside, break of 1.0953 will resume the rally from 1.0176 towards 1.1274 key resistance.

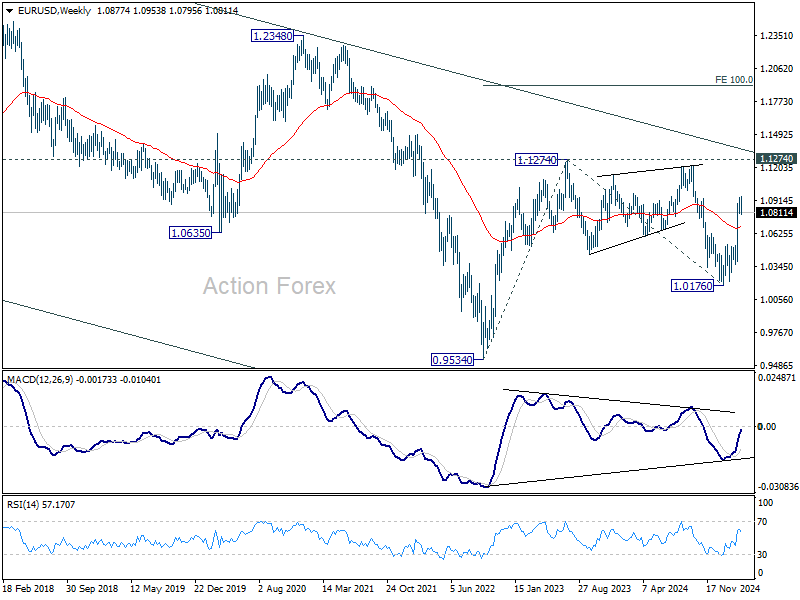

In the bigger picture, prior strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

In the long term picture, the case of long term bullish reversal is building up. Sustained break of falling channel resistance (now at around 1.1400) will argue that the down trend from 1.6039 (2008 high) has completed at 0.9534. A medium term up trend should then follow even as a corrective move. Nevertheless, rejection by the channel resistance will keep outlook bearish.

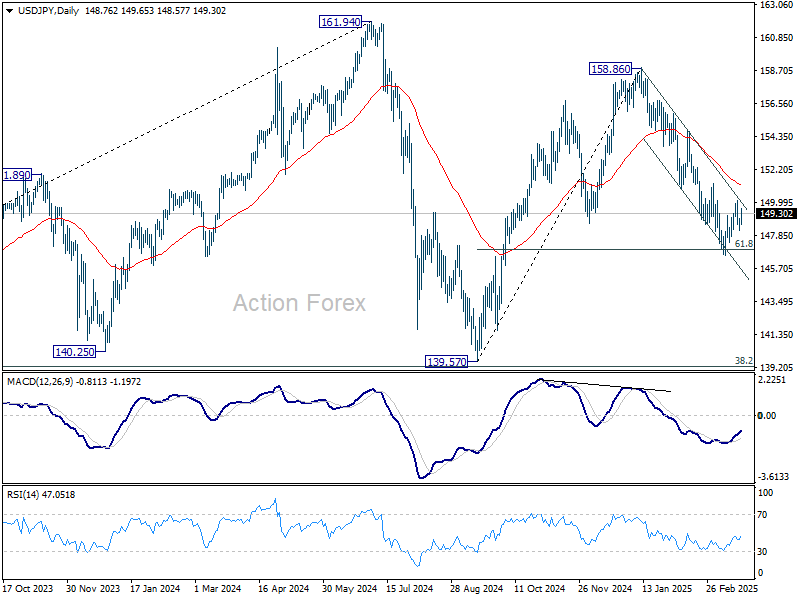

USD/JPY Weekly Outlook

USD/JPY's consolidation pattern from 146.52 extended last week and outlook is unchanged. Initial bias stays neutral this week first. In case of stronger recovery, upside should be limited by 150.92 support turned resistance. On the downside, firm break of 148.17 support will bring retest of 146.52 first. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will resume the fall from 158.86 to 139.57 support.

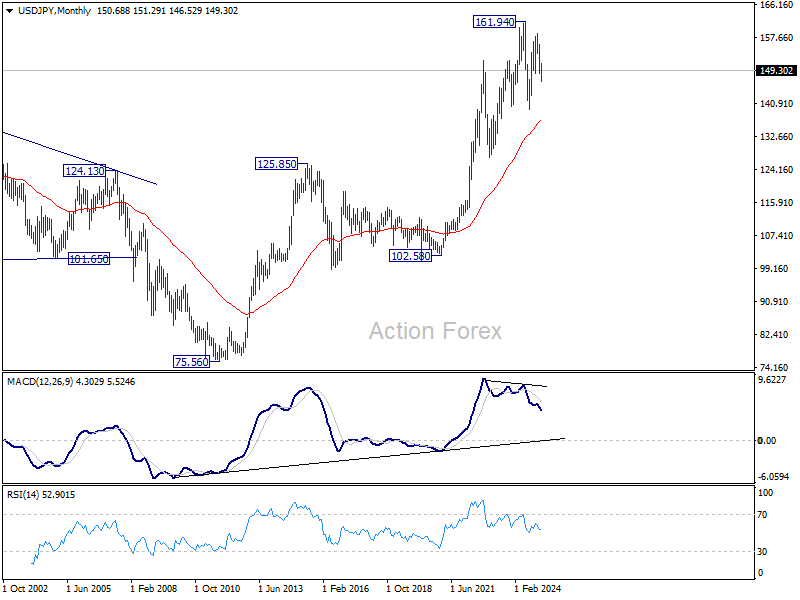

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

In the long term picture, it's still early to conclude that up trend from 75.56 (2011 low) has completed. A medium term corrective phase should have commenced, with risk of deep correction towards 55 M EMA (now at 136.88).

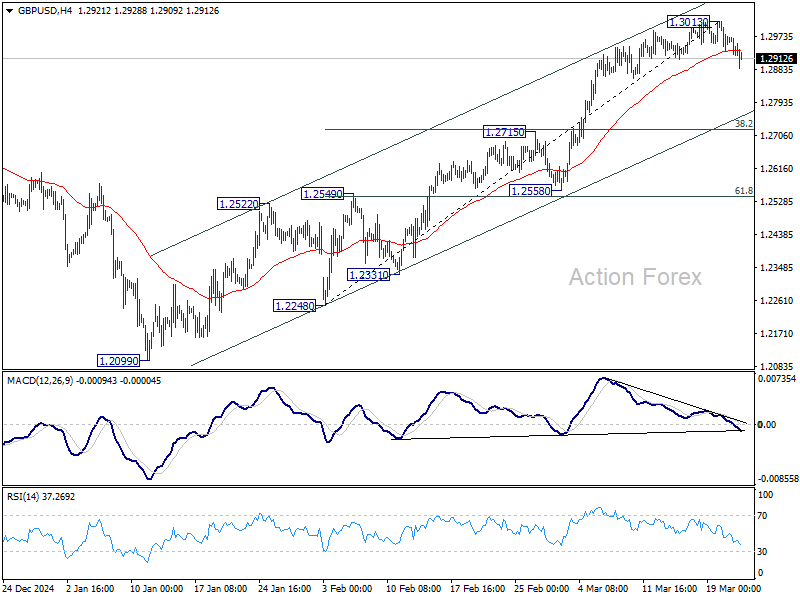

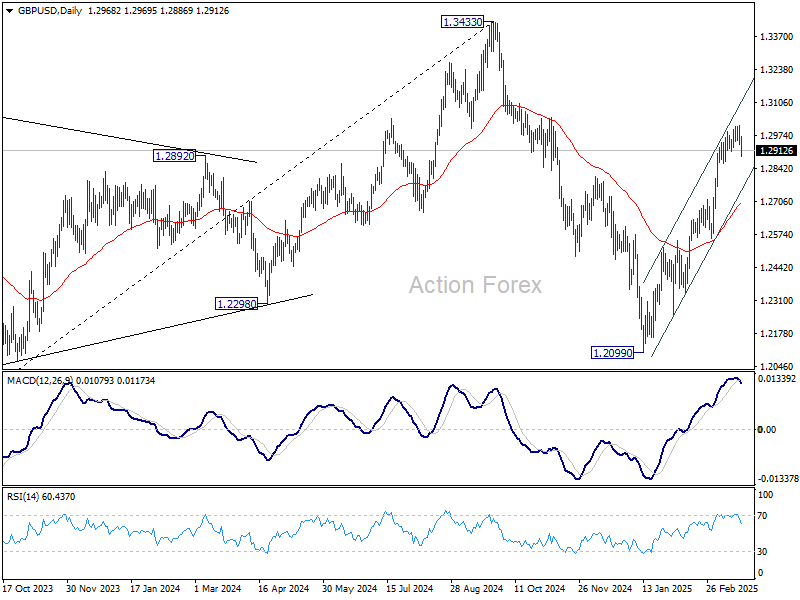

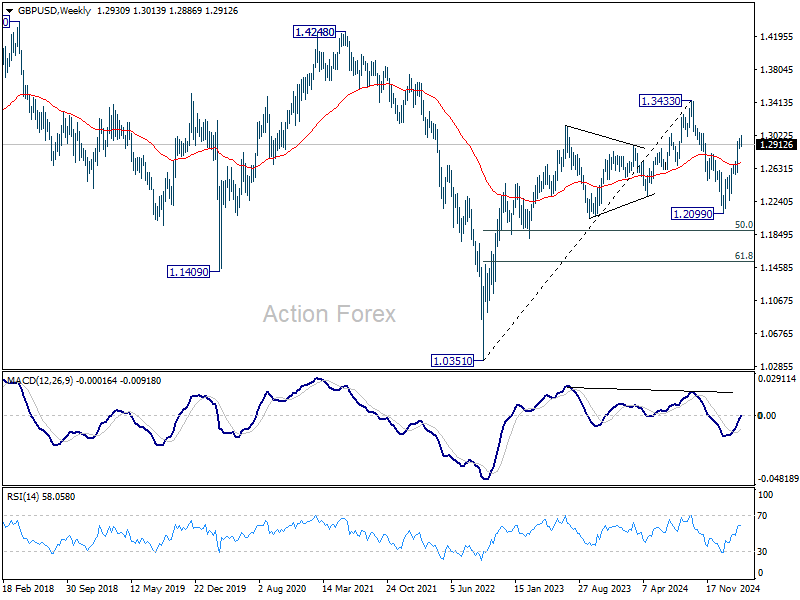

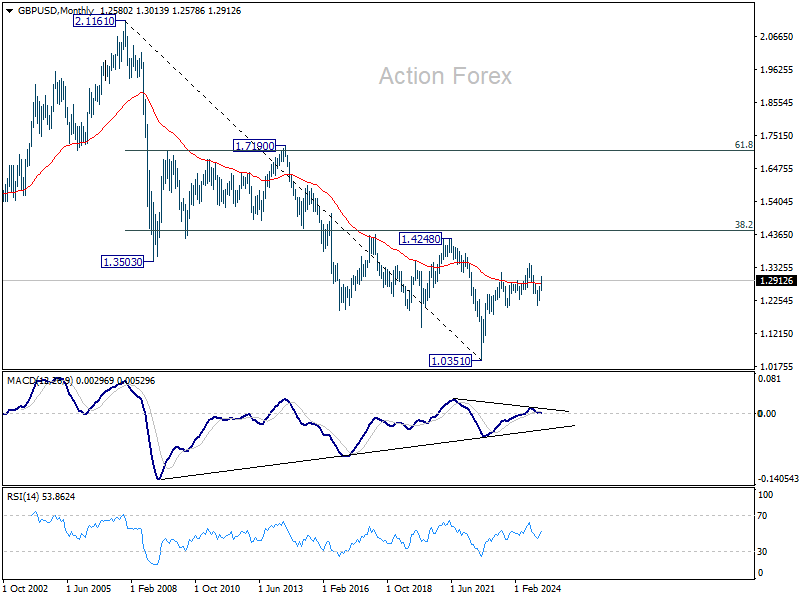

GBP/USD Weekly Outlook

GBP/USD's late decline last week suggests short term topping at 1.3013 on bearish divergence condition in 4H MACD. Initial bias is back on the downside for deeper pull back to 38.2% retracement of 1.2248 to 1.3013 at 1.2721. Strong support should be seen there to bring rebound. On the upside, break of 1.3013 will resume the rally from 1.2099.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance. This will now remain the favored case as long as 1.2099 support holds.

In the long term picture, price actions from 1.0351 (2022 low) are seen as a corrective pattern to the long term down trend from 2.1161 (2007 high) only. Outlook will be neutral at best as long as 1.4248 structural resistance holds, even in case of strong rebound.

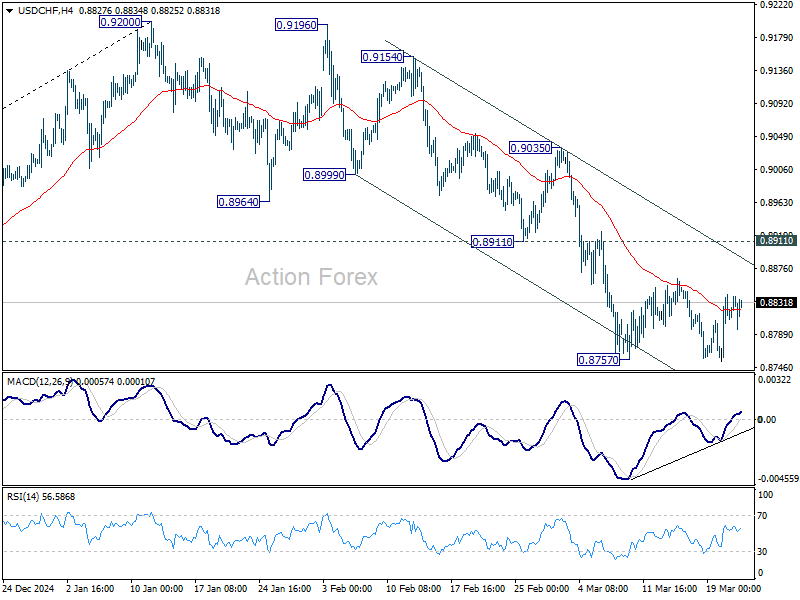

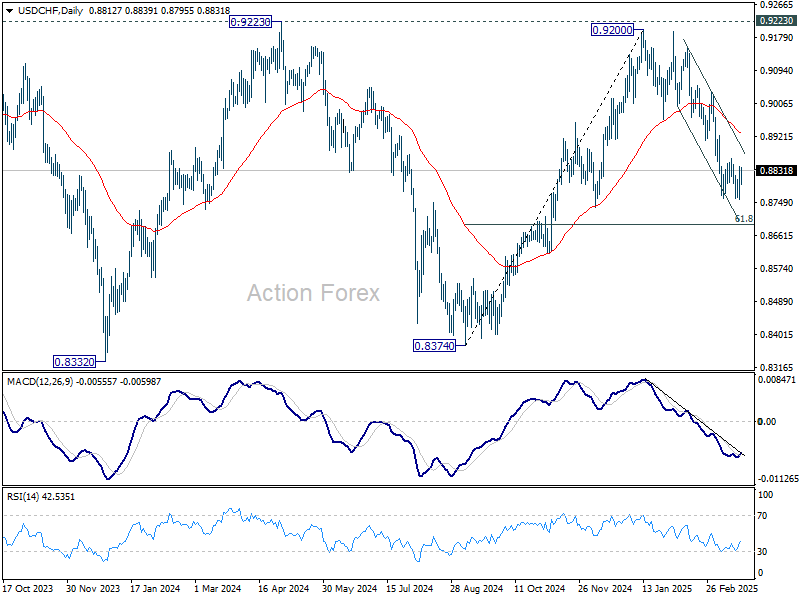

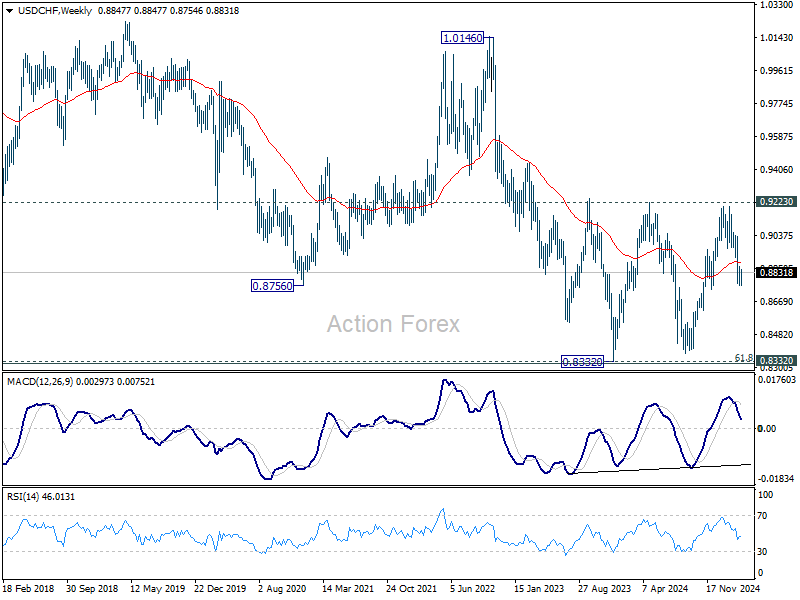

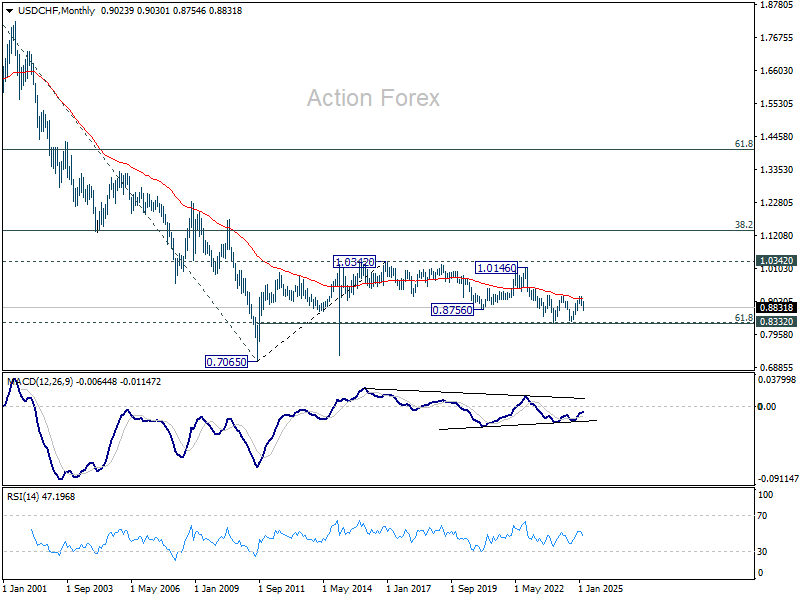

USD/CHF Weekly Outlook

USD/CHF's consolidation from 0.8757 continued last week and outlook is unchanged. Initial bias remains neutral this week first. In case of stronger recovery, upside should be limited by 0.8911 support turned resistance. On the downside, break of 0.8757 will resume the fall from 0.9200 to 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

In the long term picture, price action from 0.7065 (2011 low ) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). Fall from 1.0342 (2016 high) is seen as the second leg. Sustained break of 55 M EMA (now at 0.9115) will indicate that the third leg has already started. However, rejection by 55 M EMA again, followed by break of 61.8% retracement of 0.7065 to 1.0342 at 0.8317, will pave the way back to 0.7065.

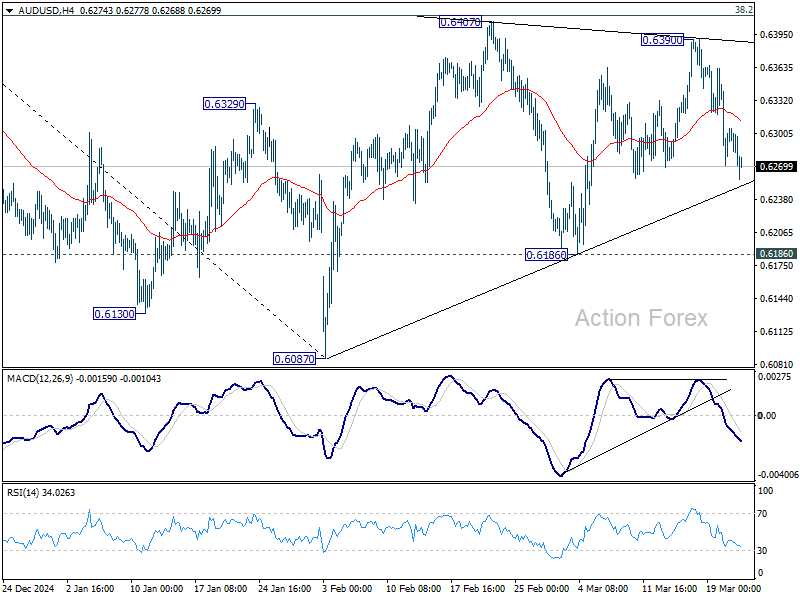

AUD/USD Weekly Report

AUD/USD edged higher to 0.6390 last week but reversed from there. Nevertheless, initial bias stays neutral this week first. On the downside, firm break of near term trend line support (now at 0.6250) will argue that corrective pattern from 0.6087 has already completed. Intraday bias will be back on the downside for 0.6186 support. Further break there will solidify this bearish case and target 0.6087 low. For now, in case of another rise, upside should be limited by 38.2% retracement of 0.6941 to 0.6087 at 0.6413.

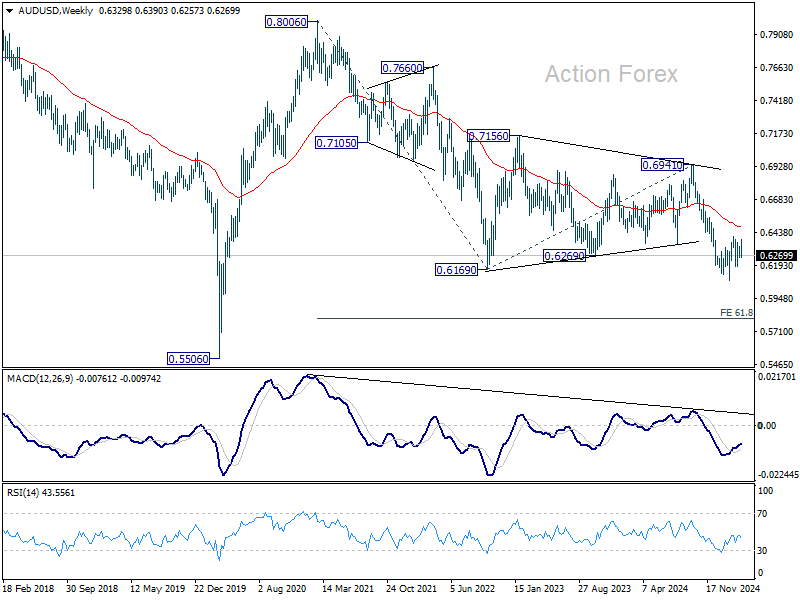

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6482) holds.

In the long term picture, prior rejection by 55 M EMA (now at 0.6801) is taken as a bearish signal. But for now, fall from 0.8006 is still seen as the second leg of the corrective pattern from 0.5506 long term bottom (2020 low). Hence, in case of deeper decline, strong support should emerge above 0.5506 to contain downside to bring reversal. However, this view is subject to adjustment if current decline accelerates further.

USD/CAD Weekly Outlook

Range trading continued in USD/CAD last week and outlook is unchanged. Initial bias remains neutral this week first. Overall, price actions from 1.4791 are seen as a corrective pattern. On the upside, break of 1.4541 will extend the second leg from 1.4150 to retest 1.4791 high. On the downside, break of 1.4238 will argue that the third leg has already started through 1.4150 support.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

In the longer term picture, up trend from 0.9506 (2007 low) is in progress and possibly resuming. Next target is 61.8% projections of 0.9406 to 1.4689 from 1.2005 at 1.5270. While rejection by 1.4689 will delay the bullish case, further rally will remain in favor as long as 55 M EMA (1.3463) holds.

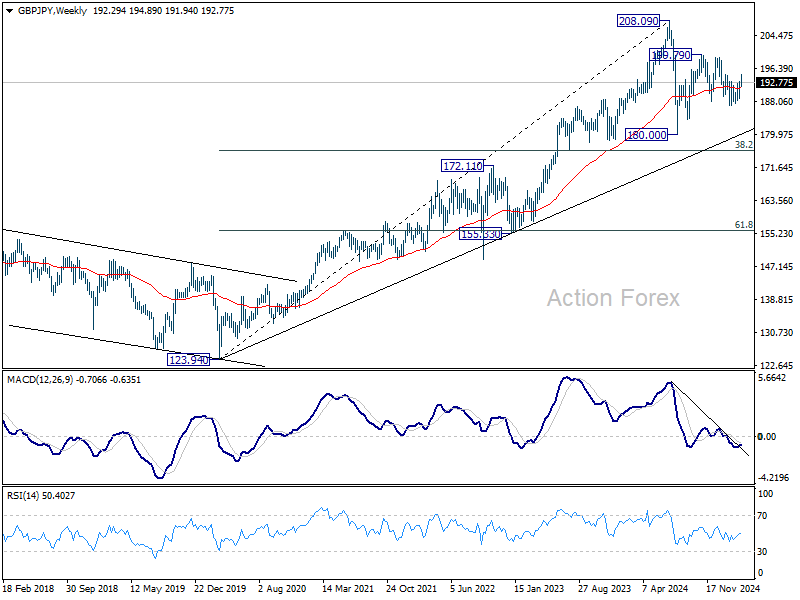

GBP/JPY Weekly Outlook

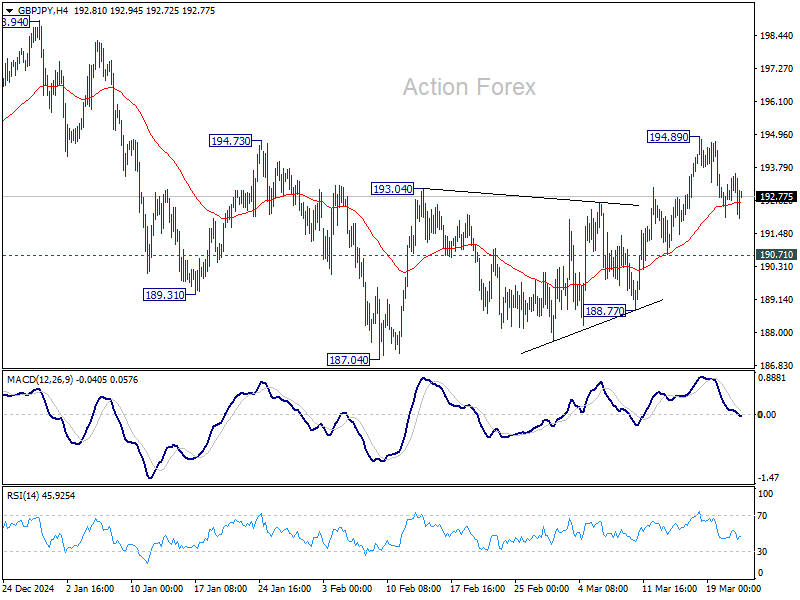

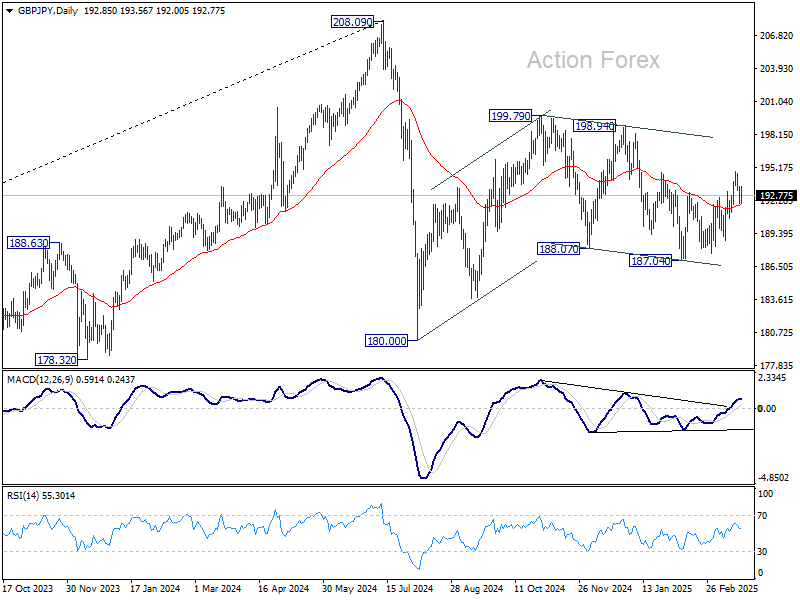

GBP/JPY edged higher to 194.89 last week but quickly retreated again. Initial bias stays neutral this week first. On the upside, above 194.89 will resume the rebound from 187.04 towards 198.94 resistance. On the downside, break of 190.71 will bring deeper fall back to 187.04 support. Overall, corrective pattern from 180.00 is still be extending.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

In the longer term picture, while a medium term top was formed at 208.09 (2024 high), it's still early to conclude that the up trend from 122.75 (2016 low) has completed. But GBP/JPY is at least in a medium term corrective phase, with risk of correction to 55 M EMA (now at 174.62).

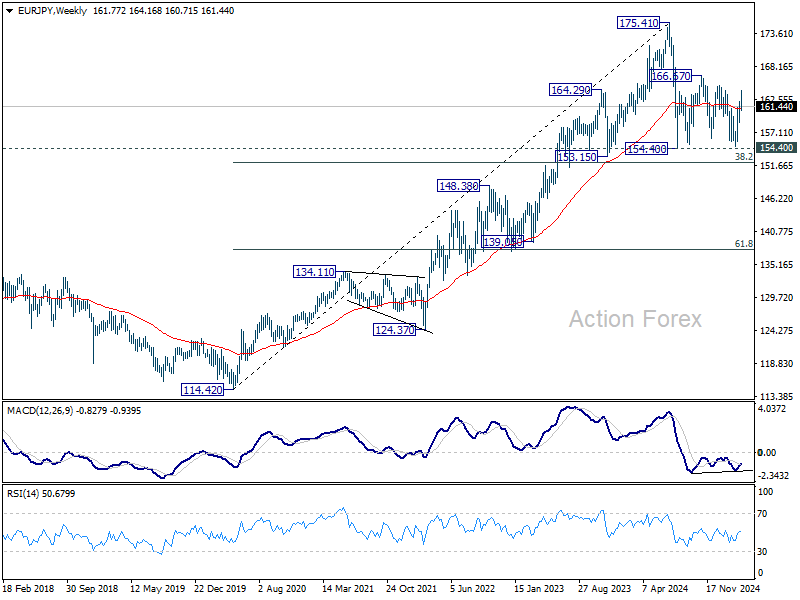

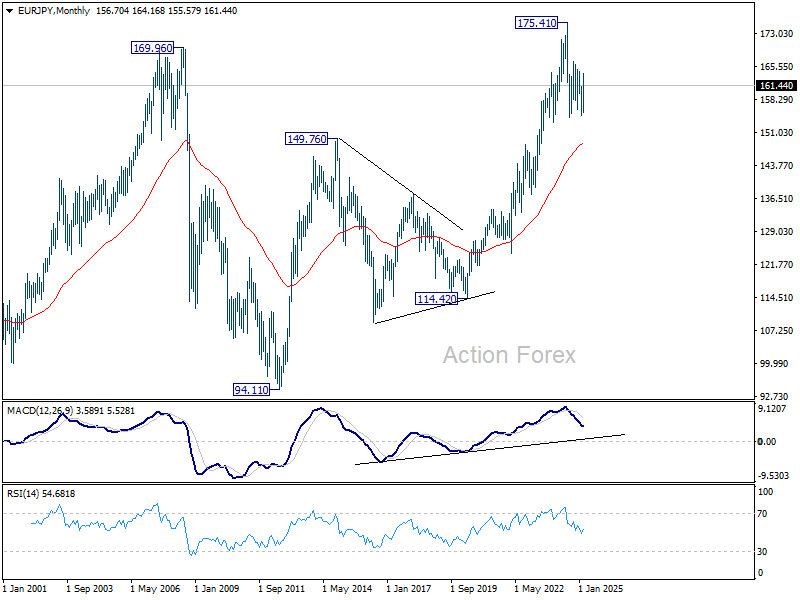

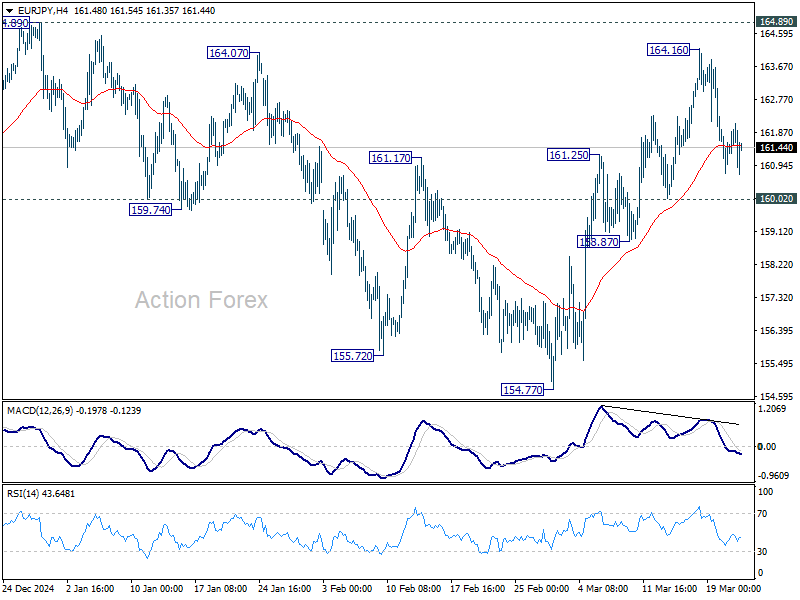

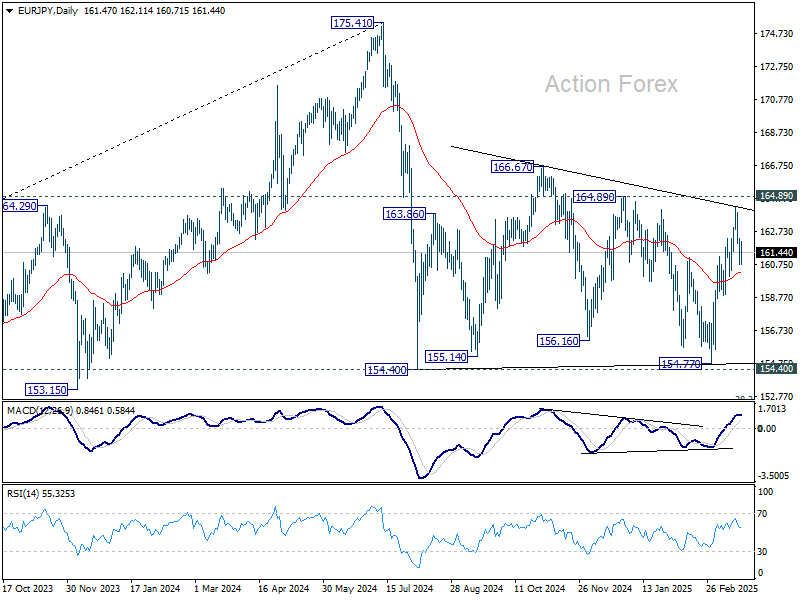

EUR/JPY Weekly Outlook

EUR/JPY edged higher to 164.16 last week but quickly retreated again. Initial bias stays neutral this week for consolidations. Further rally remains in favor as long as 160.02 support holds. Above 164.16 will target 164.89 and then 166.67. On the downside, however, break of 160.02 will argue that rise from 154.77 has completed and turn bias to the downside. Overall, sideway consolidation pattern from 154.40 is still extending.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

In the long term picture, while 175.41 is at least a medium term top, it's still early to conclude that up trend from 94.11 (2012 low) has completed. A medium term corrective phase is in progress with risk of deeper fall back to 55 M EMA (now at 148.45).