Sample Category Title

Tariff Talk to Intensify as April Deadline Approaches

US equities saw a precious support from the Federal Reserve (Fed) last week, as policymakers decided to downplay the impact of tariffs on inflation by saying that it would be ‘transitory’ and slowed the pace of QT. As such, the S&P500 closed last week 0.51% higher avoiding further losses into the correction zone despite gloomy outlook from FedEx, Micron Technology and Nike. Nasdaq gained some 0.25% over the week, the Dow Jones rebounded from the 50-week moving average to close the week 1.20% higher, small and mic-cap stocks also recovered. Across the Atlantic, Thursday and Friday were not cheery, as some investors decided to take profit after the German government passed a bill to expand infrastructure and security spending by boosting debt, and before the US tariffs are due to become effective from April 2nd. The Chinese equities, on the other hand, gave back some of the government-stimulus-boosted gains.

This is were we are right now. The week will probably be heavy with tariff talk. The early-week echoes are positive with rumours that the upcoming tariffs would be more measures than previously thought. But, who knows?

PMI numbers

Investors will be watching the March preliminary PMI numbers today. The contraction in Japan’s manufacturing PMI showed an unexpected acceleration of the contraction in the manufacturing activity in early March. Australian figures showed faster expansion in both services and manufacturing. The European figures could confirm an improved set of numbers, as well, due to the positive impact of massive government spending on overall mood across the old continent, while the US numbers are under the threat of a sharp fall in US growth expectations. The latest US GDP update is due Thursday and is expected confirm a slowdown in US economic growth from 3.1% to 2.3 in Q4. Atlanta Fed’s GDPNow Forecast has improved last week but still points at around 1.8% contraction in Q1 of this year.

The US dollar is softer this morning after a three-session rebound that let the major currencies like the euro and sterling take a breather after an impressive rally since the beginning of the year. But – unlike the expectations that the US tariffs would send the euro to parity against the greenback – the outlook for the euro is now positive on improved growth expectations due to the spending boost, and sterling is also challenging the 1.30 mark. But gains in sterling are vulnerable ahead of this week’s budget statement that will confirm that Rachel Reeves is left with less than £10bn of budget headroom to boost growth – meaning that either she will hint at higher taxes or less spending. Both are negative for growth. And in an environment of increased focus on growth expectations from the FX traders, sterling may struggle to clear the 1.30 offers, even against a globally weakened US dollar.

In commodities, gold is in a good position to benefit from tariff shenanigans, while oil remains under the pressure of weak – and weakening – global growth expectations.

CoreWeave IPO

CoreWeave, an Nvidia-backed cloud computing company specialized in GPU infrastructure for AI, will go public on the Nasdaq this week. The IPO pricing is scheduled for Wednesday, the company is expected to start trading on Thursday under the ticker CRWV. The company is expected to offer 49 mio shares priced between $47 and $55 a share, and raise up to $2.7bn. The company announced a net loss of more than $800mio in 2024 but their revenue reached $1.92bn and they secured a 5-year contract worth nearly $12bn with OpenAI and count Microsoft among their big clients. The problem is, it has a handful of big clients and a lot of debt to repay, and the AI craze has been losing momentum since the beginning of the year. The CoreWeave IPO will be an interesting barometer on how excited the tech investors still are despite a more than 20% pullback in Magnificent 7 stocks since the December peak. Nvidia lost up to 30% since its January ATH following an almost 1000% rally between 2023 and the end of the 2024. A set of strong earnings and robust forecast, the announcement of a chip that’s even faster than Blackwell – the next generation chip that started selling a few months ago – and partnerships with companies that are not necessarily in the technology sector couldn’t help reverse losses. Investors flocked into the Chinese tech stocks instead on realization that it’s possible to build AI models on cheaper chips and Chinese-made chips. This week, all eyes are on the Chinese Boao Forum – the Chinese version of Davos – where Xi Jinping will meet with the foreign company CEOs in an effort to strengthen investor confidence to keep the positive momentum going.

The Week Kicks Off With PMIs

In focus today

In the euro area, we receive the flash PMI data for March, which will be crucial for the ECB's rate decision in April. We anticipate the composite PMI to rise from 50.2 to 50.6, driven by continued normalisation in the manufacturing sector. The PMIs have shown a reasonable correlation with the ZEW index, which increased in March. We expect the manufacturing PMI to rise to 48.4 from 47.6 in February, while activity in the services sector is likely to remain broadly unchanged, with the services PMI at 50.6, like February.

In the US, March Flash PMIs will also be released. Some regional leading indicators have pointed towards a downtick in the manufacturing cycle after a promising recovery over the winter.

In China, PBOC will set the policy rate overnight, the 1-year Medium-Term Lending Facility rate. We expect it to be unchanged again as we believe the central bank will continue to be sidelined for now until we move closer to another Fed cut. PBOC aims for a stable USD/CNY and thus now tends to move in tandem with Fed rate changes while using other instruments to support the economy, such as specific lending schemes for different sectors.

The US data calendar for the remainder of the week is fairly light, with the Conference Board's consumer confidence on Tuesday and the Fed's preferred measure of inflation, PCE, on Friday. In the euro area, monetary aggregates and credit data is released on Thursday, while we get March inflation data from Spain and France on Friday. In the UK, Chancellor Reeves will present the Spring Statement, and finally Norges Bank will announce their rate decision on Thursday.

Economic and market news

What happened overnight

In Japan, March PMIs were lower across the board, with all indices creeping below the 50-threshold. The manufacturing measure stood at 48.3, recording the lowest reading in a year, while the services counterpart slipped to 49.5. The composite measure fell to its lowest level since August 2020 at 48.5, with firms stating concerns over rising costs, labour shortages and the global trade environment.

BoJ Governor Ueda emphasized that the BoJ will proceed to raise interest rates if the underlying inflation target is likely to meet the 2% target, despite potential losses on its government bond holdings. We forecast the BoJ to deliver two additional 25bp rate hikes this year, with the next likely in July.

What happened over the weekend

In the US, NY Fed's President Williams (hawk and voter) said on Friday that the US central bank's "Modestly restrictive" monetary policy is suitable amidst economic uncertainties - with Chicago Fed President Goolsbee (dove and voter) also sharing similar views. We still look for the next cut in June, followed by quarterly 25bp reductions until the terminal rate of 3.00-3.25% is reached in June of 2026. For more details, please see Research US - Fed review: Cautious stability, 19 March.

On Friday, President Trump called his 2 April reciprocal tariffs "the big one" but signalled there will be flexibility. At the beginning of his term, Trump ordered a comprehensive study into unfair trade practices by other countries, and the results are set to be finished by 1 April. The findings will guide the reciprocal tariffs that will be implemented on a country-by-country basis. Currently the uncertainty remains large about what they might look like; for instance, Trump has previously likened the EU's VATs to a tariff against US imports.

In the euro area, consumer confidence declined to -14.5 (cons: -13.0) from -13.6 in February. Consumer confidence is one of the tier-2 data points that feed into the ECB's decision in April, and the continued weak consumer confidence questions the uptick in private consumption that ECB expects to drive growth this year. Hence, in isolation it was a dovish signal. Following a large increase last year, consumer confidence has fallen in 2025 especially due to consumer's view on the general economic situation over the next 12 months while they are less negative about their personal financial situation.

Moreover, ECB's Stournaras was on the wire, stating that he still sees 2 more cuts in 2025 with a terminal rate of 2%. Importantly, Stournaras is one of the doves and the fact that he only expects rates to come down to 2% suggests that we might not get more than that.

In Germany, the upper house of parliament, the Bundesrat, passed the large fiscal spending bill. Hence, Germany has now changed their constitution to allow higher defence spending, created an EUR 500bn off-budget fund for infrastructure, and eased the regional state budgets. For our assessment of the implications of the package, please see Research Germany - Fiscal policy to boost growth but also inflation concerns, 19 March.

In Canada, PM Carney has called for a snap election on 28 April. It is expected to be a close race between Liberals (PM Carney) and the Conservatives. The Conservatives initially held a substantial lead, but recent political influence of Trump has significantly diminished their advantage.

In geopolitics, Ukrainian and US officials commenced discussions aimed at securing energy facilities and critical infrastructure in Saudi Arabia on Sunday. Despite optimism from the US, both Ukraine and Russia have reported overnight strikes, highlighting the fragile nature of the proposed 30-day ceasefire. According to Bloomberg, the US administration hopes to reach a broad ceasefire within weeks, with plans for a truce agreement by 20 April. For our perspective on the market impacts of a Ukraine deal, please see Research Global - What would a dirty deal in Ukraine mean for markets, 16 February.

Equities: Global equities ended slightly lower on Friday. More importantly, last week equities managed to halt the decline and ended higher for the week. In our opinion due to fewer tariff announcements. The centre of the storm, US tech, performed better, a trend that continued Friday. Additionally, the VIX index subsided and concluded the week below 20.

While we must wait for the message on new tariffs on 2 April, and it is too early to determine whether all the political turmoil has had a lasting negative effect on consumers and corporations, we can still conclude for the moment that no news is good news, for risky assets, which was essentially the message last week. In the US on Friday, Dow +0.1%, S&P 500 +0.1%, Nasdaq +0.5%, Russell 2000 -0.6%. This morning, Asian markets are mostly lower. Japanese markets have just turned positive despite a disappointing set of both manufacturing and service PMIs this morning. European and US futures are higher this morning, led by the US and growth/tech sectors.

FI&FX: The USD had a strong end to the week, posting a third consecutive day of strengthening with EUR/USD briefly trading below 1.08 before closing just above. Front-end UST yields traded a few bp lower, driving a slight steepening. Despite the USD support, both SEK and NOK showed strong performance with EUR/SEK below 11.00 and EUR/NOK at 11.40, leaving NOK/SEK above 0.96 once again. Last Friday, we published our monthly FX Forecast Update, where we maintain a bearish medium-term outlook for EUR/USD and continue to see headwinds for both the SEK and NOK.

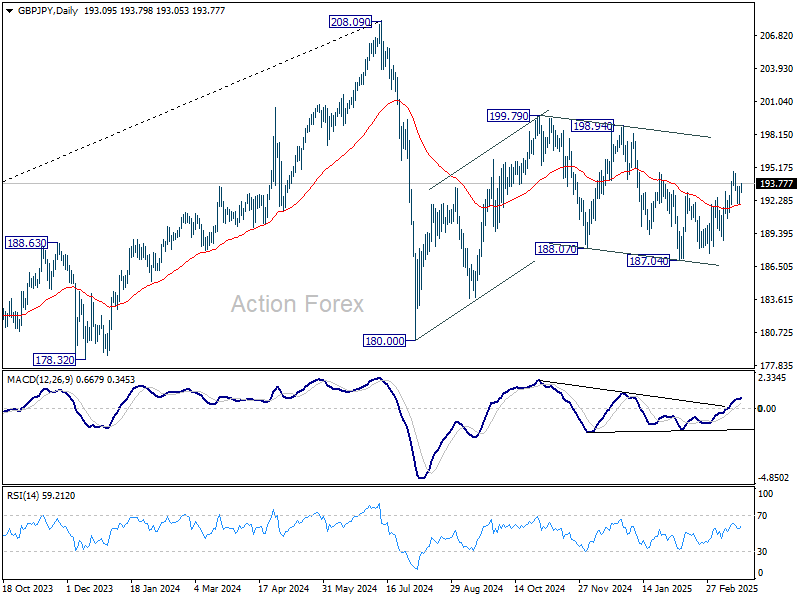

GBP/JPY Daily Outlook

Daily Pivots: (S1) 192.05; (P) 192.82; (R1) 193.62; More...

Intraday bias in GBP/JPY remains neutral for consolidations below 194.89. On the upside, above 194.89 will resume the rebound from 187.04 towards 198.94 resistance. On the downside, break of 190.71 will bring deeper fall back to 187.04 support. Overall, corrective pattern from 180.00 is still be extending.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

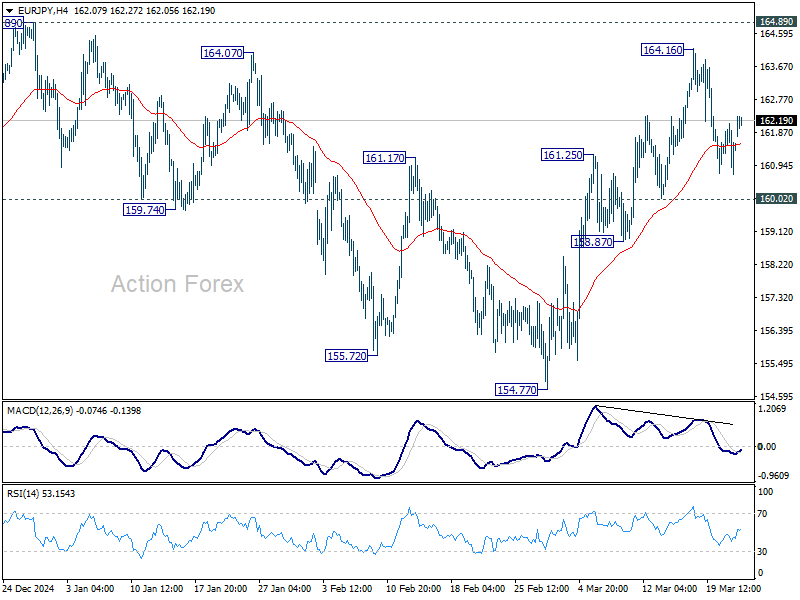

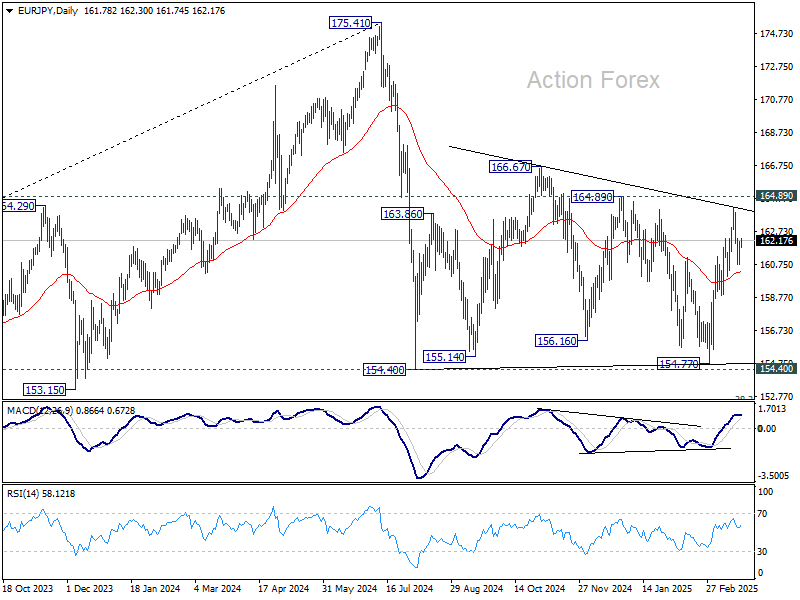

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.77; (P) 161.45; (R1) 162.16; More...

Intraday bias in EUR/JPY remains neutral for consolidations below 164.16. Further rally remains in favor as long as 160.02 support holds. Above 164.16 will target 164.89 and then 166.67. On the downside, however, break of 160.02 will argue that rise from 154.77 has completed and turn bias to the downside. Overall, sideway consolidation pattern from 154.40 is still extending.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

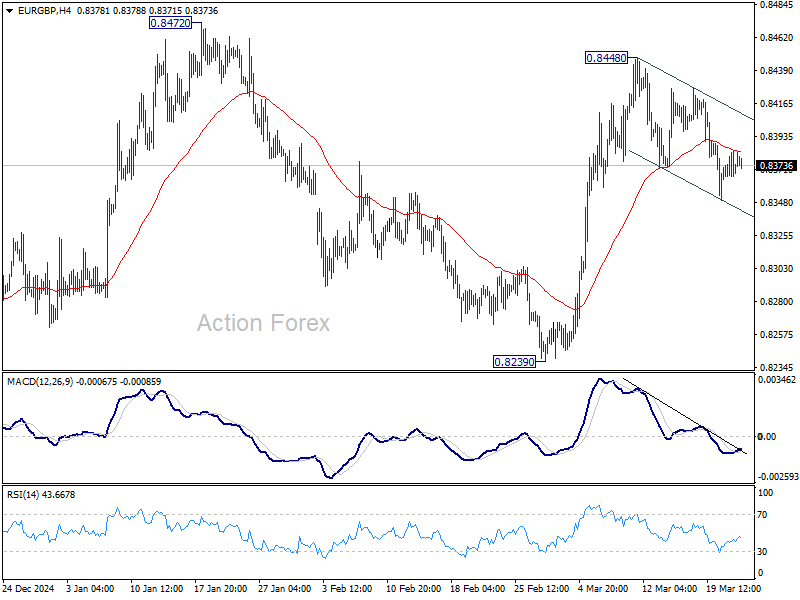

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8364; (P) 0.8374; (R1) 0.8384; More...

Intraday bias in EUR/GBP remains neutral as more consolidations could be seen below 0.8448. On the upside. break of 0.8488 will resume the rise from 0.8239 through 0.8472 resistance to medium term falling channel resistance (now at 0.8495). However, sustained break of 55 D EMA (now at 0.8347) will suggest that rise from 0.8239 has completed and turn bias back to the downside instead.

In the bigger picture, EUR/GBP is still bounded inside medium term falling channel. While rebound from 0.8221 might extend higher, it could still develop into a corrective pattern. Overall outlook will be neutral at best and down trend from 0.9267 (2022 high) could extend, at least until decisive break of channel resistance (now at 0.8495).

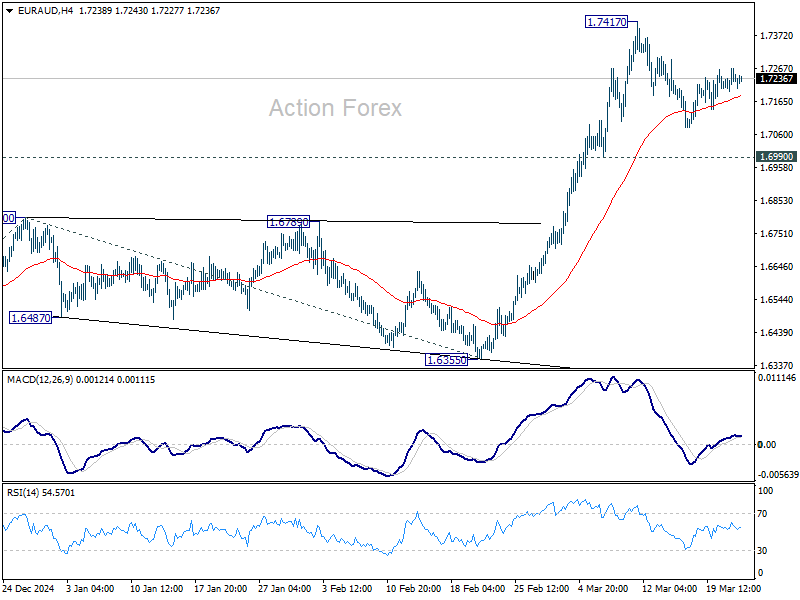

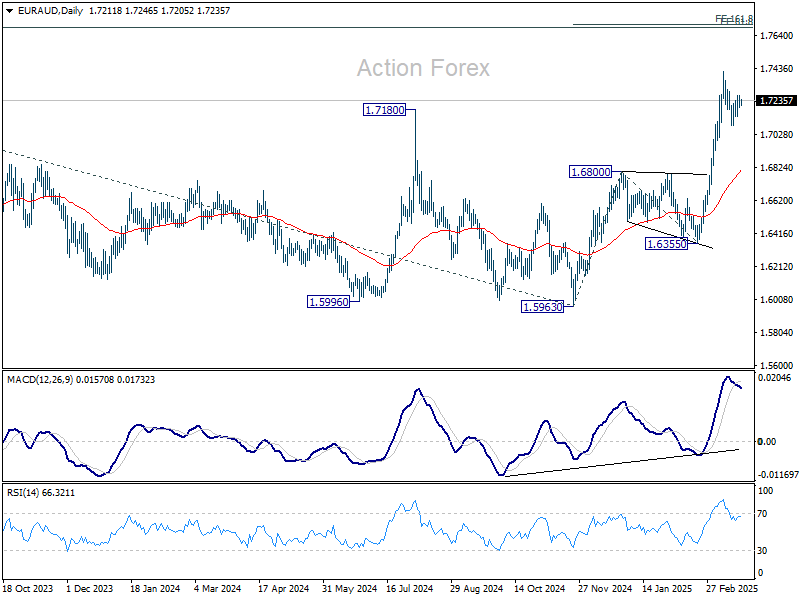

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7202; (P) 1.7237; (R1) 1.7278; More...

Intraday bias in EUR/AUD remains neutral for the moment as consolidations continue below 1.7417. Downside of retreat should be contained by 0.6990 support to bring rebound. On the upside, break of 1.7417 will resume rise from 1.6335 to 161.8% projection of 1.5963 to 1.6800 from 1.6355 at 1.7709 next.

In the bigger picture, the breach of 1.7180 key resistance (2024 high) suggests that up trend from 1.4281 (2022 low) is resuming. Sustained trading above 1.7180 will confirm and target 61.8% projection of 1.4281 to 1.7062 from 1.5963 at 1.7682, which is also close to 61.8% retracement of 1.9799 (2020 high) to 1.4281 at 1.7691. For now, this will remain the favored case as long as 1.6800 resistance turned support holds, even in case of deep pullback.

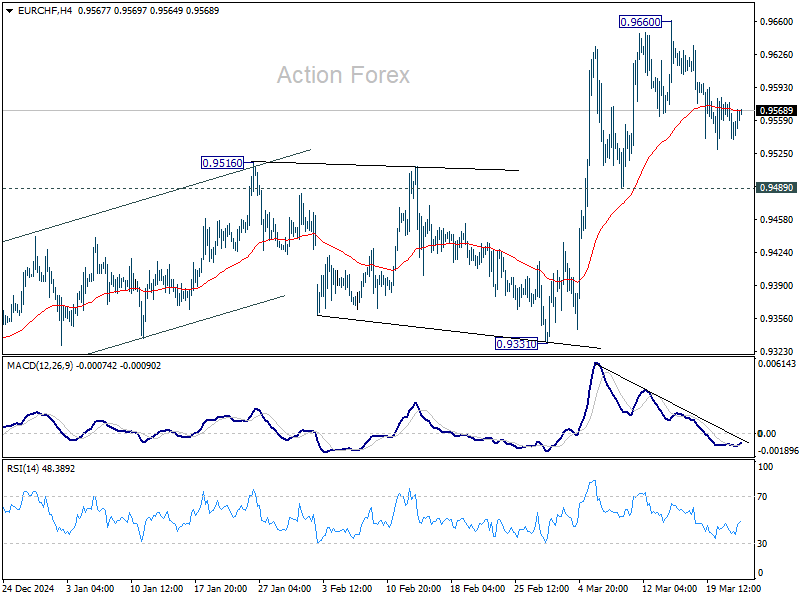

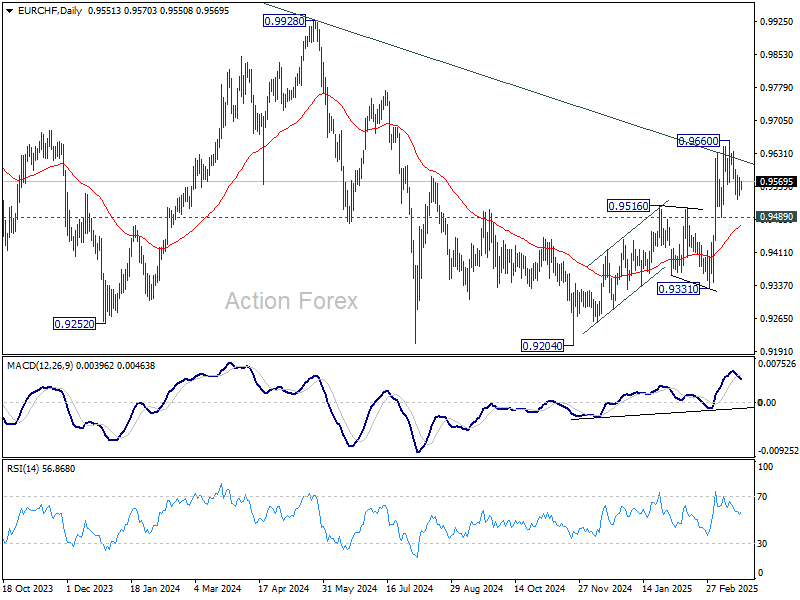

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9532; (P) 0.9560; (R1) 0.9580; More....

EUR/CHF is extending the consolidation from 0.9660 and intraday bias stays neutral. After all, further rally is expected as long as 0.9489 support holds. Break of 0.9660 will resume whole rise from 0.9204.

In the bigger picture, prior strong break of 55 W EMA (now at 0.9487) is a medium term bullish sign. Sustained break trading above long-term falling channel resistance (at around 0.9618) would suggest that the downtrend from 1.2004 (2018 high) has bottomed at 0.9204. Stronger rally should then be seen to 0.9928 key resistance at least.

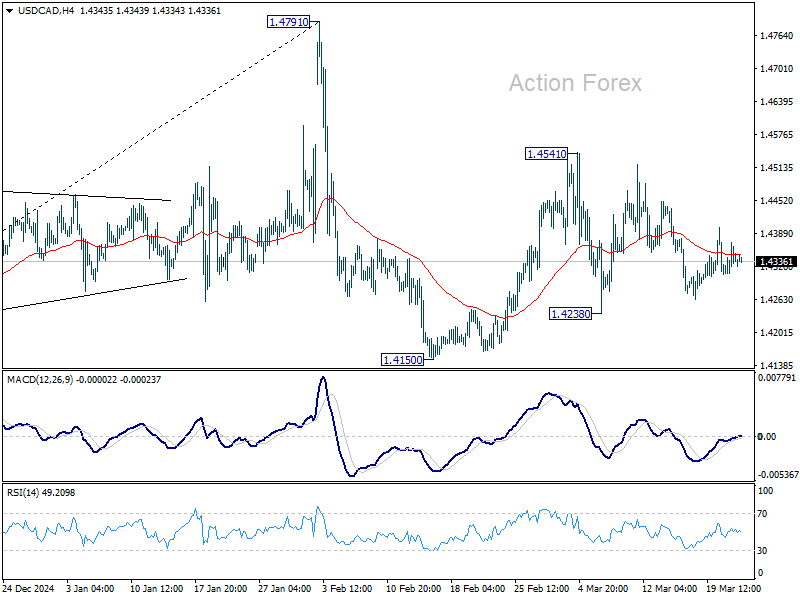

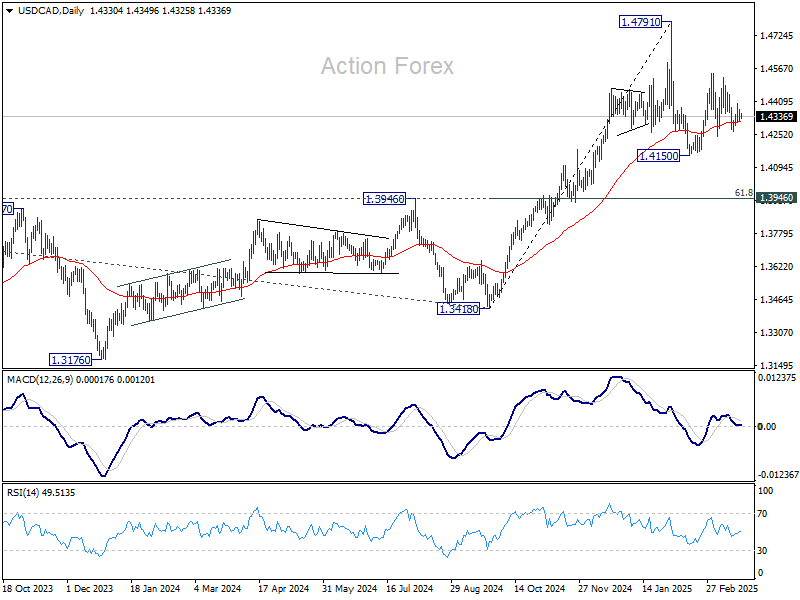

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4322; (P) 1.4348; (R1) 1.4381; More...

Intraday bias in USD/CAD remains neutral for the moment as range trading continues. Overall, price actions from 1.4791 are seen as a corrective pattern. On the upside, break of 1.4541 will extend the second leg from 1.4150 to retest 1.4791 high. On the downside, break of 1.4238 will argue that the third leg has already started through 1.4150 support.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

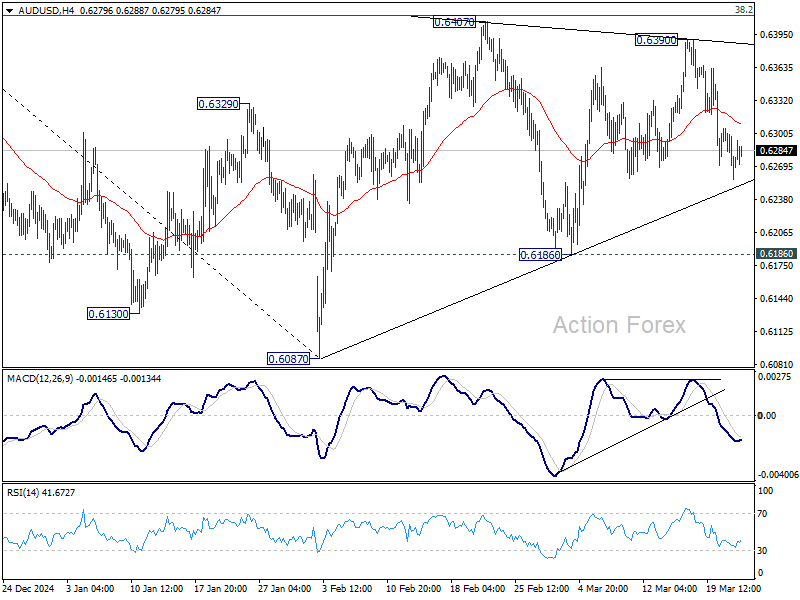

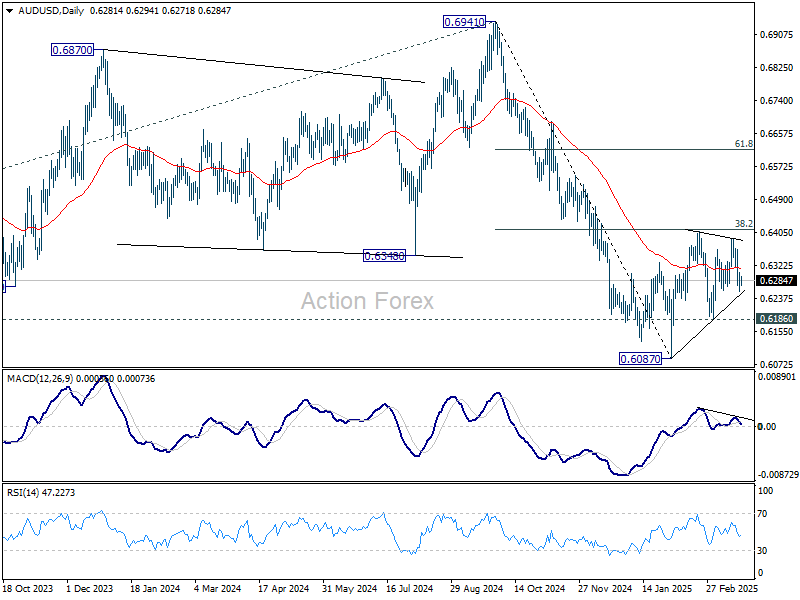

AUD/USD Daily Report

Daily Pivots: (S1) 0.6252; (P) 0.6279; (R1) 0.6300; More...

Intraday bias in AUD/USD stays neutral for the moment. On the downside, firm break of near term trend line support (now at 0.6250) will argue that corrective pattern from 0.6087 has already completed. Intraday bias will be back on the downside for 0.6186 support. Further break there will solidify this bearish case and target 0.6087 low. For now, in case of another rise, upside should be limited by 38.2% retracement of 0.6941 to 0.6087 at 0.6413.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6467) holds.

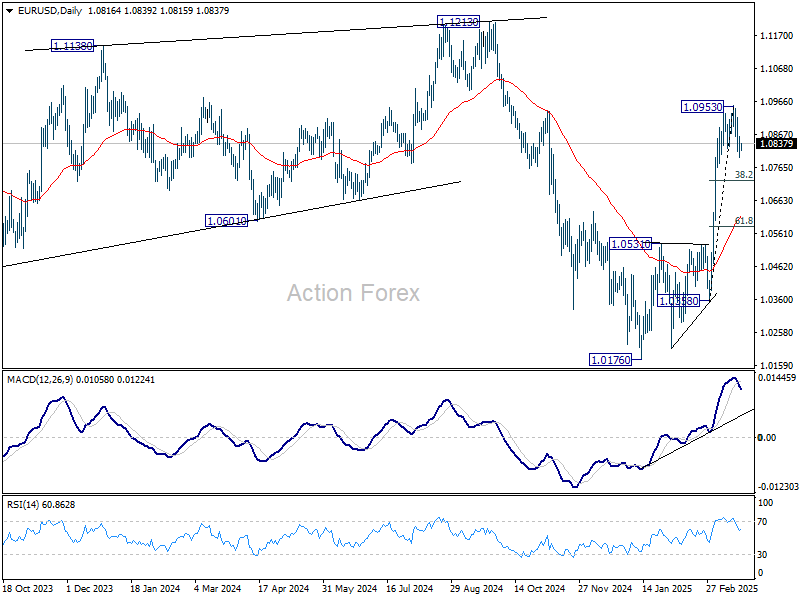

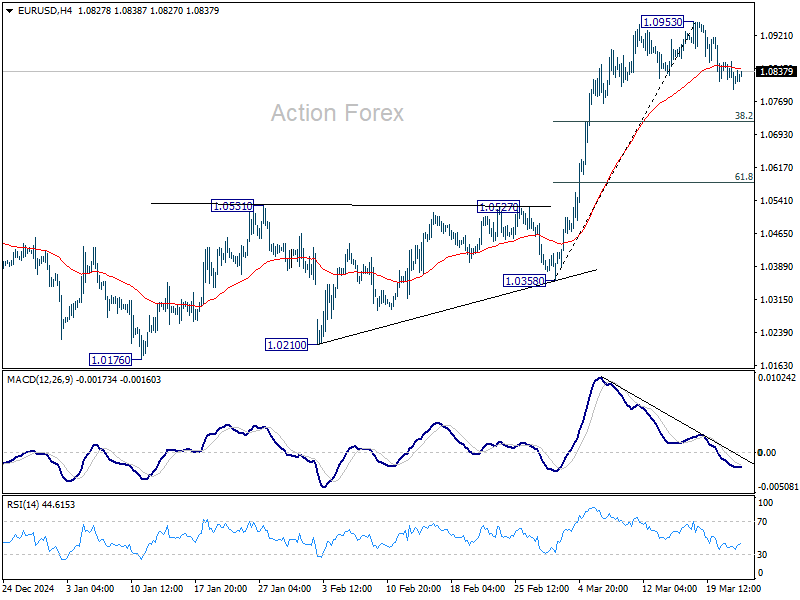

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0787; (P) 1.0824; (R1) 1.0852; More...

Intraday bias in EUR/USD remains mildly on the downside for the moment. Correction from 1.0953 short term top would extend to 38.2% retracement of 1.0358 to 1.0953 at 1.0726. Strong support should be seen there to bring rebound. On the upside, break of 1.0953 will resume the rally from 1.0176 towards 1.1274 key resistance.

In the bigger picture, prior strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.