Sample Category Title

Fed’s Bostic sees just one rate cut in 2025, warns tariffs may reinforce inflation

Atlanta Fed President Raphael Bostic said in a Bloomberg interview that he's now projecting just one cut by year-end, down from his earlier expectation of two.

Bostic explained the shift was due to his view that inflation will be "very bumpy and not move dramatically and in a clear way to the 2% target”. With inflation unlikely to return to target until 2027, he believes the path to neutral must also be delayed.

Bostic also expressed concern about the inflationary impact of rising tariffs. While such measures are often assumed to cause a one-off increase in prices, Bostic suggested the current environment could be different.

In his view, businesses and consumers may have grown more tolerant of elevated inflation following the pandemic, making price hikes more likely to stick. He noted that many business leaders now feel confident about "a complete pass-through" of higher costs on to customers without fear of losing market share.

BoE’s Bailey calls for trade cooperation and embraces AI as growth catalyst

BoE Governor Andrew Bailey urged greater international cooperation to resolve growing strains in the global trading system. In a speech overnight, he pointed to the disruptions caused by US President Donald Trump’s trade policies, emphasizing that resolving these challenges requires "multilateral setting rather than set tariffs bilaterally".

In a more optimistic tone, Bailey also pointed to artificial intelligence as a transformative force for the UK and global economy. Comparing AI to electricity in the early 20th century, he said the technology could meaningfully raise growth and per capita income over time. He called for policy support to facilitate AI’s development as the "most likely general purpose technology,” capable of driving broad-based economic gains in the years ahead.

ECB’s Escriva warns of extreme uncertainty and skewed growth risks

In remarks delivered overnight, Spanish ECB Governing Council member Jose Luis Escriva highlighted that “growth risks are more downside than upside.” While he acknowledged that supportive fiscal policy could offer some near-term uplift, he stressed that the broader risks — particularly to the downside — are dominating the economic outlook.

Escriva painted a grim picture of the current global backdrop, describing it as “extremely uncertain.” He noted that today’s uncertainty global index levels are at their highest since records began — exceeding those during the Covid-19 pandemic, the war in Ukraine, the 9/11 attacks, and even the peak of the Great Financial Crisis.

Despite the fact that worst-case, disruptive scenarios have yet to materialize, Escriva emphasized that ECB must be “readier than ever” to revise its forecasts and relevant action should conditions change".

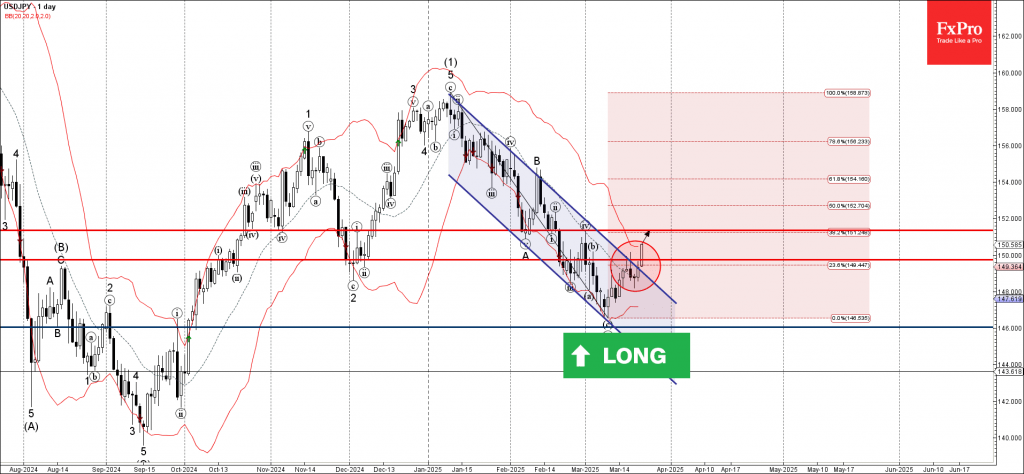

USDJPY Wave Analysis

USDJPY: ⬆️ Buy

- USDJPY broke the resistance zone

- Likely to rise to the resistance level 151.35

The USDJPY currency pair rose strongly after breaking the resistance zone between the resistance level of 150.00 and the resistance trendline of the daily down channel in January.

The breakout of this resistance zone accelerated the active intermediate impulse wave (3) from the start of March.

Given the strongly bullish US dollar sentiment seen today, USDJPY currency pair can be expected to rise to the next resistance level 151.35 (the high of wave iv from last month).

Dow Jones Wave Analysis

Dow Jones: ⬆️ Buy

- Dow Jones reversed from support zone

- Likely to rise to resistance level 43000.00

Dow Jones index continues to rise inside the short-term correction iv which started earlier from the support zone located between the support level 41000.00, lower daily Bollinger Band and the 61.8% Fibonacci correction of the upward impulse from August.

The active correction iv belongs to the C-wave of the extended ABC correction (4) from the start of December.

Given the long-term uptrend, Dow Jones index can be expected to rise to the next resistance level 43000.00.

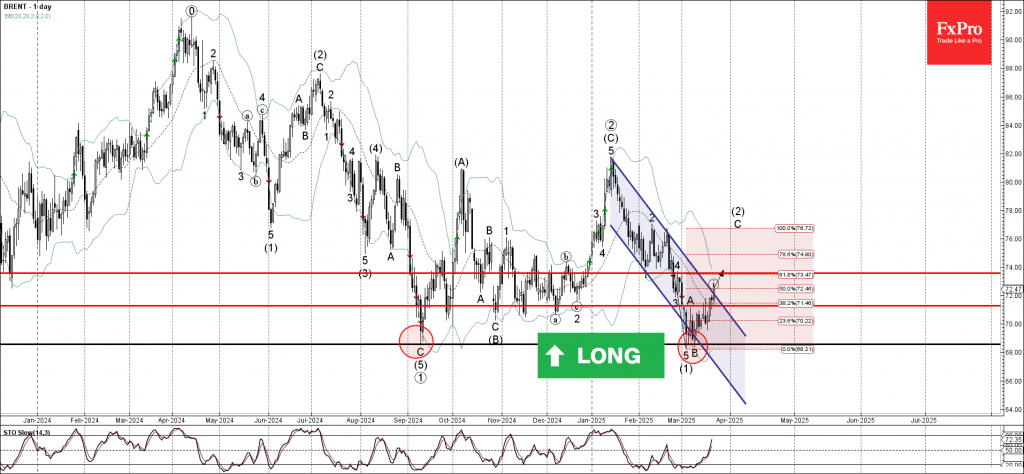

Brent Crude Oil Wave Analysis

Brent crude oil: ⬆️ Buy

- Brent crude oil broke resistance zone

- Likely to rise to the resistance level 73.60

Brent crude oil recently broke the resistance zone between the resistance level 71.30 (top of wave A), resistance trendline of the daily down channel in January and the 38.2% Fibonacci correction of the downward impulse from February.

The breakout of this resistance zone accelerated the C-wave of the active intermediate ABC correction (2) from the start of March.

Brent crude oil can be expected to rise to the next resistance level 73.60 (top of the previous minor correction 4 from the end of February).

XTIUSD: WTI’s Bullish Attempt May Reverse

Technical Analysis

- WTI Crude Oil: Attempting to break out of a consolidation range.

- Key Resistance: $70 (psychological level) & 50-day EMA.

- Key Support: $67-$65 range (historical support for three years).

- Brent Crude: Following a similar pattern, testing the 50-day EMA resistance.

Fundamental Drivers

- U.S. Sanctions on Iran could tighten supply.

- OPEC+ production adjustments may balance increased output against voluntary cuts.

- Ceasefire talks in Ukraine could impact Russian crude supply.

- Tariff uncertainty from the U.S. could influence demand expectations.

Key Takeaway for Traders

- Bullish bias above $67: A breakout past $70 and the 50-day EMA could trigger further upside.

- Buying dips: Strong support at $65-$67 makes pullbacks attractive buying opportunities.

- Volatility ahead: Watch for geopolitical shifts & OPEC+ actions as key catalysts.

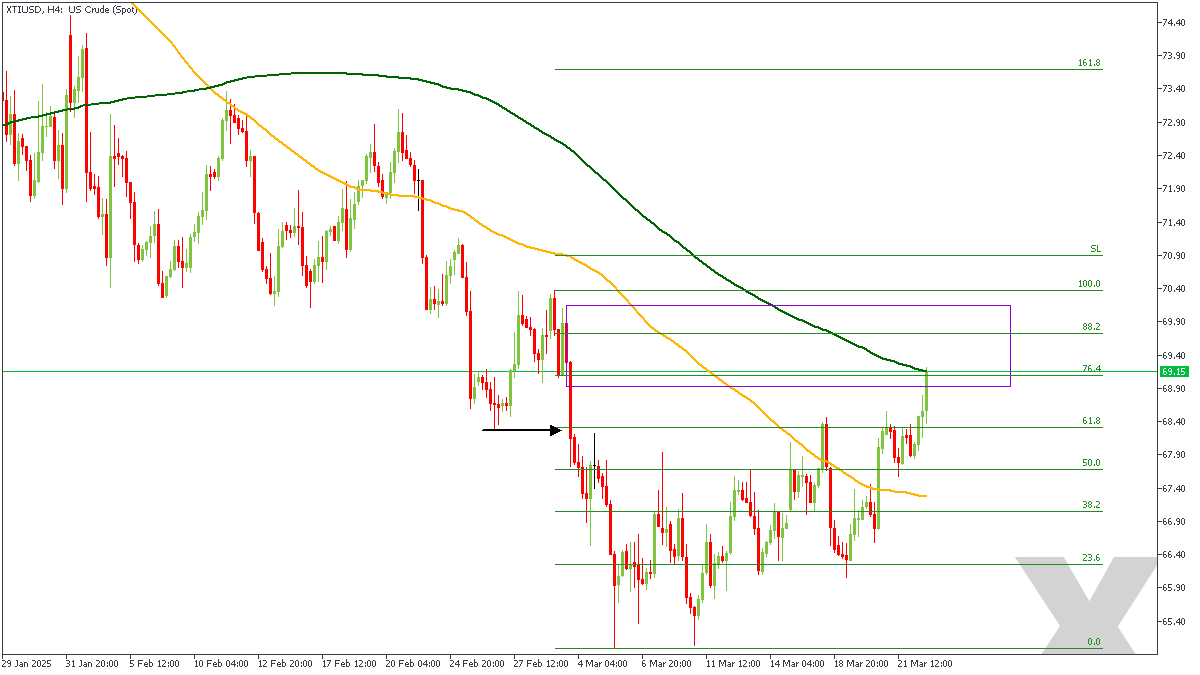

XTIUSD – H4 Timeframe

The price action on the 4-hour timeframe chart of XTIUSD is currently leaning on the 200-period moving average resistance near the 76% Fibonacci retracement level, right in the middle of the rally-base-drop supply. The bearish array of the moving averages is another clue that points to the likelihood of a bearish outcome.

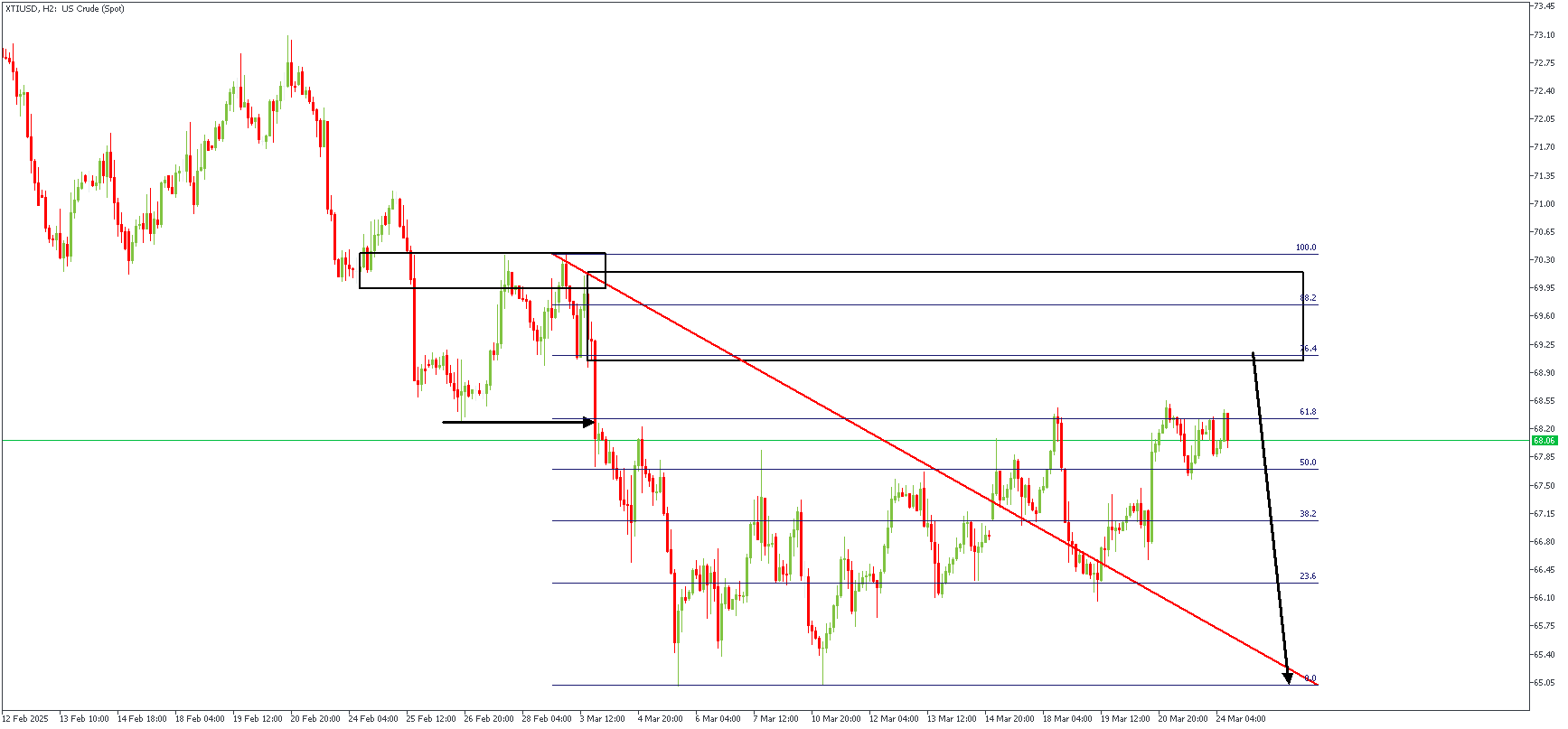

XTIUSD – H2 Timeframe

On the 2-hour timeframe chart of XTIUSD, we see the previous bearish break of structure, the FVG (Fair Value Gap) created by the breakout momentum, and the inducement from the internal structure highs. Comparing this with the higher timeframe sentiment leaves the bearish sentiment as the more probable option.

Analyst’s Expectations:

- Direction: Bearish

- Target- 65.05

- Invalidation- 70.50

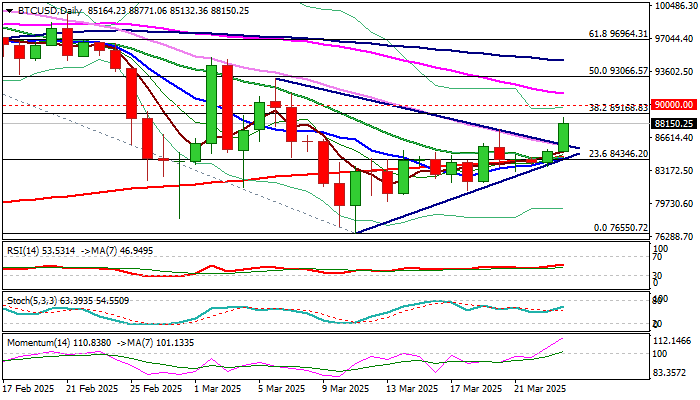

Bitcoin: Bulls Regain Traction on Softer Tariff Rhetoric

Bitcoin jumped on Monday, advancing 2.7% until early US trading, as softer tones on tariffs from Trump’s administration revived positive sentiment.

Fresh strength emerges above multi-day range and generates positive signal on break of the upper boundary of triangle on daily chart.

Daily close above triangle (upper line lays at 86113) will be minimum requirement to keep fresh bulls in play.

Key barriers at 89168 (Fibo 38.2% of 109582/76550) and 90K (round figure, former range floor and key support) are coming in focus, with break here to generate initial reversal signal and open way for stronger recovery (91295 – 55DMA and 93066 – Fibo 50% mark next targets).

Res: 89168; 90000; 91294; 93066.

Sup: 87497; 86113; 84500; 83098.

Sunset Market Commentary

Markets

European PMIs offered a first glimpse of the impact on the German-European defense initiative on business. So far, though, the huge government spending announcements only lifted the forward looking indicator (sentiment towards future activity), specifically in Germany. That makes sense of course since all of this still needs to translate into actual policy decisions and thus into the real economy. It’s against that backdrop we shouldn’t be too worried about an overall slight miss of the composite European PMI, which came in at 50.4 vs 50.7 expected and picking up from 50.2. It’s nonetheless the highest print in seven months. Manufacturing was responsible for the improvement. While the overall indicator is still in contraction territory, the 48.7 was the highest reading since February 2023. In addition, the output subseries returned to growth for the first time in two years. Germany contributed to this due to what is seen as a production boost ahead of import tariffs. While this is likely to fade again, the effects of the large infrastructure & defense package may take over afterwards. The services gauge fell to a four-month low of 50.4. New orders dropped in both sectors and with a faster rise in services employment and softer reduction of the work force in manufacturing, backlogs of work fell once again. Input costs inflation eased due to a services-lead slowdown, be it to a still sharp rate. This resulted in the slowest pace of rising selling prices year-to-date. Interestingly though, the manufacturing sector raised output prices for the first time in seven months. In theory today’s outcome support the case for a final, tactical ECB rate cut in April before moving into an extended pause, our preferred scenario. Euro area money market thinking, however, remains split with implied probabilities only marginally rising to 63% compared to 58% on Friday. That’s also keeping European yields in check. They erased some kneejerk losses quickly to trade between 1-3 bps higher in a steepening move. We suspect reports of the US pursuing a more targeted approach in the reciprocal tariff threat (April 2 is the due date) instead of blunt, widespread and/or cumulative (on existing levies) increases to have helped in the background as well.

Divergence again between the US and Europe, but this time with the US Global March PMI printing substantially stronger than expected (53.5 from 51.6). Still the report contained some ‘mixed’ signals. Services activity improved sharply from 51.0 to 54.3, the highest level in 3 months. The manufacturing PMI declined from 52.7 to 49.8. Despite the overall improvement, S&P indicated that business expectations for the year ahead fell to their second lowest since October 2022 as companies grew increasingly cautious about the economic outlook. Cost pressure also intensified across the economy and fed through in selling prices, especially in manufacturing. Despite the uptick, S&P assess that the survey still points to slower growth in Q1 (1.5% Q/Qa) and that sentiment darkened further. Markets apparently gave more weight to the positives. US yields jumped after release to currently trade 6.0 to 8.0 bps higher across the curve. Despite persistent uncertainty, US equities (Nasdaq +2.0 %) and the dollar DXY (104.3) outperform. The euro initially weathered a slightly disappointing EMU PMI quite well, but dropped back to the 1.08 area after the stronger than expected US PMI. In the UK, the PMI also showed a surprise rebound (52.0 from 50.5, highest in 6 months) due to a sharp improvement in services activity (53.2). S&P also indicted a robust increases in prices charged. The reaction of UK markets was a bit mixed with only a limited changes in UK yields, but sterling performing solidly, especially against a bleak euro. EUR/GBP declined to test the 0.8350 area.

News & Views

Data published by Statistics Poland showed February real retail sales declining by 6.0% M/M to be 0.5% lower Y/Y. The outcome was substantially weaker than expected. In a monthly perspective, sales declined 13.6% for textiles, 7.1% for household goods, 4.9% for food and 3.9% for pharmaceuticals. Monthly retail sales data are notoriously volatile and Statistics Poland indicates that the data was influenced by a smaller number of trading days compared to February last year. Even so, the disappointing retail sales releases follow weaker than expected production data and softer than expected wage growth data early published last week. Recent softer than expected data question the hawkish stance from central bank governor Glapinski and might at least support the case of some of the more dovish members within the MPC to keep the debate open on possible interest rate cuts, e.g. in the second half of the year. The Polish 2-y swap yield eases 4 bps to 4.92% but the zloty remains well bid, with EUR/PLN declining to 4.176.