Sample Category Title

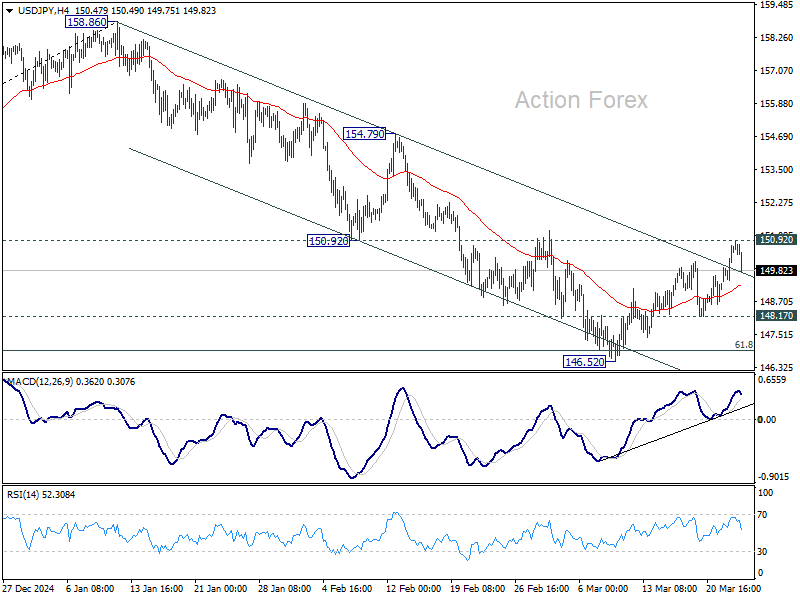

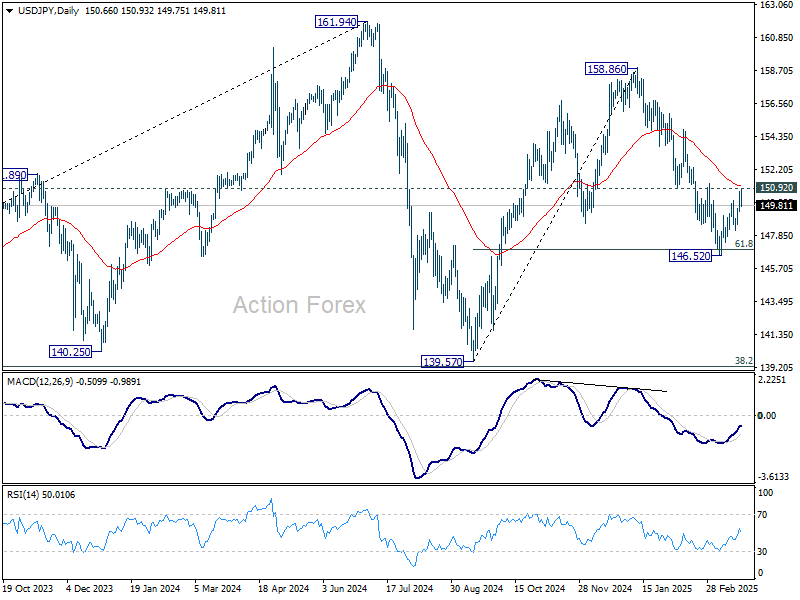

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.78; (P) 150.27; (R1) 151.19; More...

Intraday bias in USD/JPY remains neutral and outlook is unchanged. Strong resistance is expected from 150.92 to complete the corrective recovery from 146.52. On the downside break of 148.17 support will bring retest of 146.52 first. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will resume the fall from 158.86 to 139.57 support. However, firm break of 150.92 will argue that fall from 158.86 has completed and turn bias back to the upside for 154.79 resistance next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

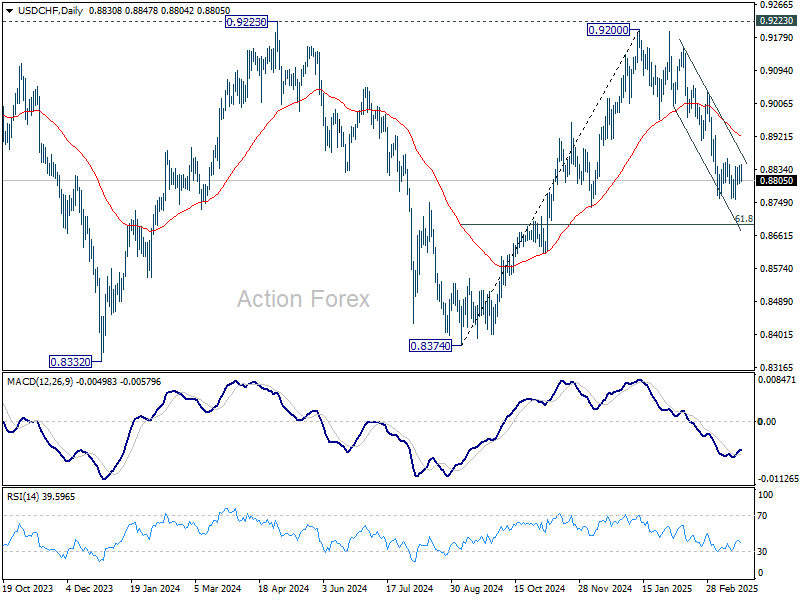

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8804; (P) 0.8825; (R1) 0.8850; More…

Range trading continues in USD/CHF and intraday bias stays neutral. In case of stronger recovery, upside should be limited by 0.8911 support turned resistance. On the downside, break of 0.8757 will resume the fall from 0.9200 to 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

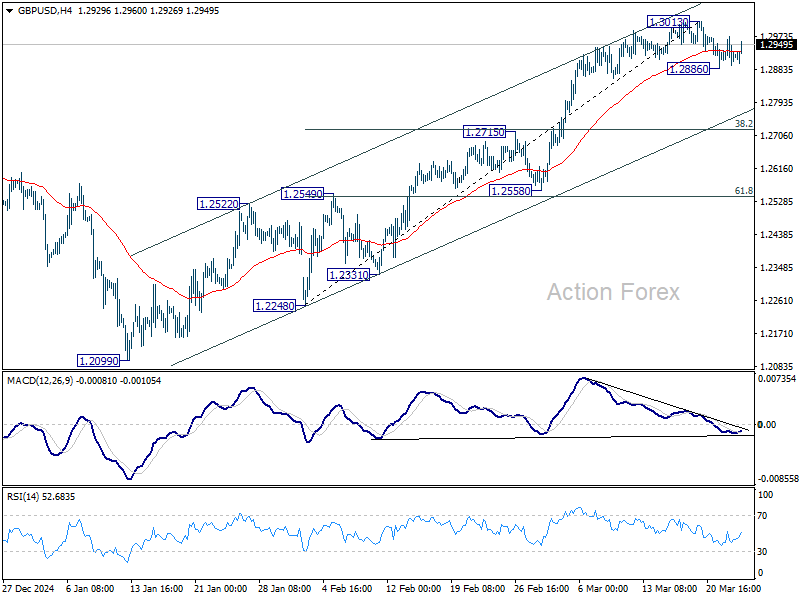

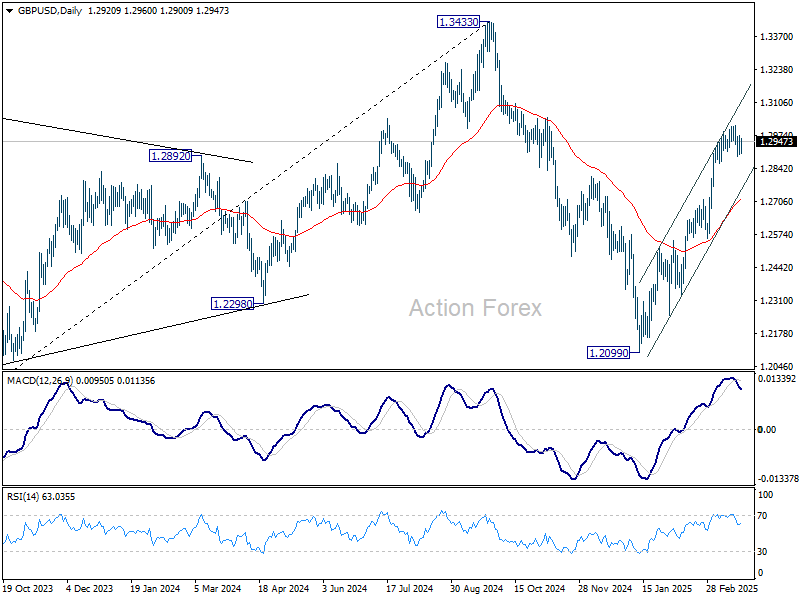

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2881; (P) 1.2927; (R1) 1.2970; More...

Intraday bias in GBP/USD is turned neutral with current recovery. Correction from 1.3013 might still extend lower. But downside should be contained by 38.2% retracement of 1.2248 to 1.3013 at 1.2721 to bring rebound. On the upside, break of 1.3013 will resume the rally from 1.2099.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance. This will now remain the favored case as long as 1.2099 support holds.

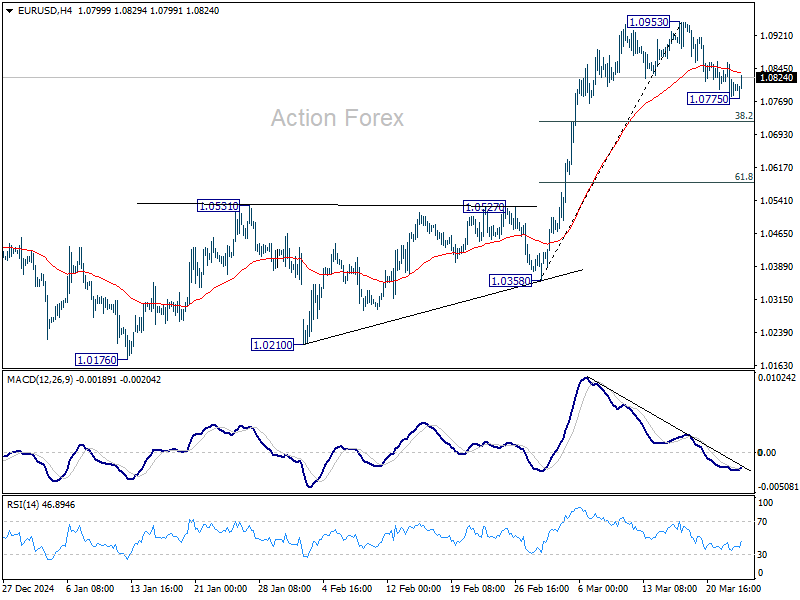

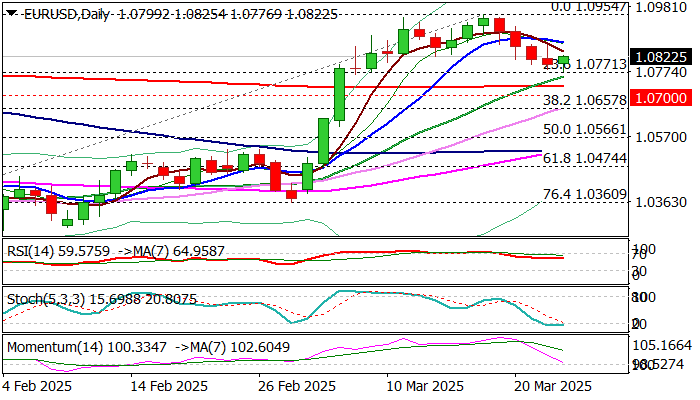

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0769; (P) 1.0814; (R1) 1.0845; More...

Intraday bias in EUR/USD is turned neutral with current recovery. Corrective pattern from 1.0953 could extend with another fall. But downside should be contained by 38.2% retracement of 1.0358 to 1.0953 at 1.0726 to bring rebound. On the upside, break of 1.0953 will resume the rally from 1.0176 towards 1.1274 key resistance.

In the bigger picture, prior strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

Dollar Slips, Euro Bounces, Aussie Awaits CPI

Dollar is once again under pressure as markets head into the US session, with its recent rebound losing steam in the absence of any clear-cut catalyst. While new headlines on tariffs continue to emerge almost daily, these “leaks” could only be seen as reflective of ongoing deliberations within the White House, rather than firm policy. For now, the tariff outlook remains mired in speculation, and traders are growing weary of chasing news that is yet to be confirmed — or could just as easily be reversed.

The latest development suggests US President Donald Trump is eyeing a two-step tariff strategy, set to commence on “Liberation Day,” April 2. The proposal may include a strengthened legal foundation for a broader “reciprocal” tariff regime, which could also serve to raise revenue for future tax cuts. Additionally, a revival of vehicle import tariffs is reportedly being considered, bringing back a national security investigation from Trump’s first term.

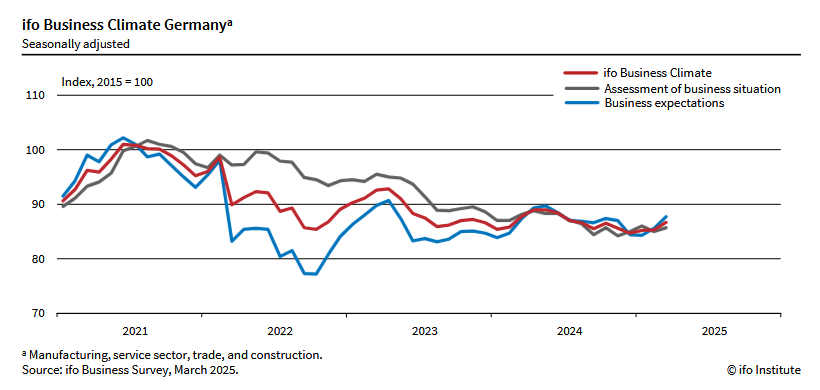

In Europe, German DAX is staging a notable rebound, while Euro tries to firm up against Dollar. . German Ifo data points to improving sentiment and expectations, buoyed by optimism around fiscal expansion plans. Still, questions remain about the sustainability of recovery, especially with persistent weakness in services and complications from coalition talks.

Overall, the mood in Europe remains cautiously optimistic but restrained. While the idea of a cyclical upswing in Germany is gaining traction, it’s offset by global uncertainty, particularly around US trade policy. The lack of clarity around tariffs is also limiting the extent of positive momentum in risk assets.

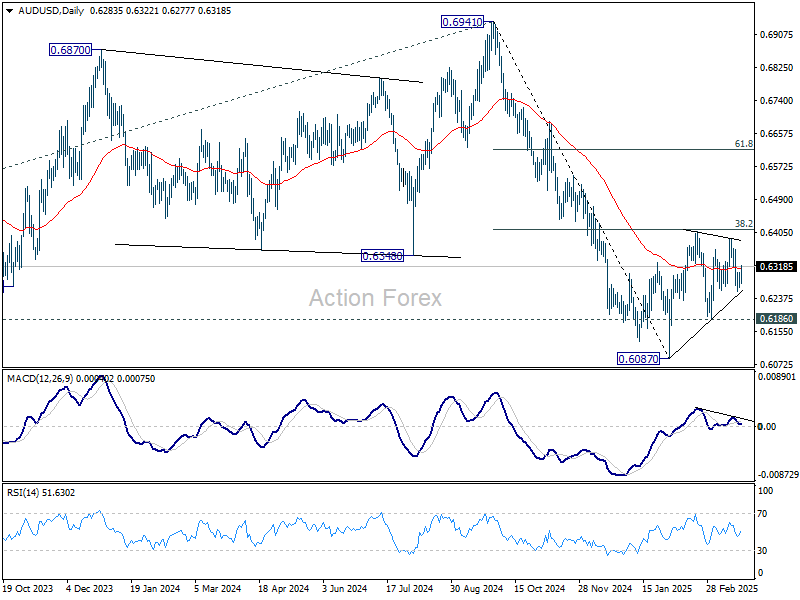

Looking ahead, the spotlight will shift to Australia with the release of monthly CPI data during the upcoming Asian session. Expectations are for inflation to hold steady at 2.5% for February. The data isn’t expected to sway RBA’s decision to hold next week. But any downside surprise would be welcomed as a sign that recent inflation upticks since Q4 have already peaked.

Technically, AUD/USD's price actions from 0.6087 are still seen as a corrective pattern to the fall from 0.6941. This view will hold as long as 38.2% retracement of 0.6941 to 0.6087 at 0.6413 holds. Break of 0.6186 support will argue that the downside is ready to resume through 0.6087 low.

In Europe, at the time of writing, FTSE is up 0.78%. DAX is up 108%. CAC is up 1.24%. UK 10-year yield is up 0.034 at 4.755. Germany 10-year yield is up 0.056 at 2.831. Earlier in Asia, Nikkei rose 0.46%. Hong Kong HSI fell -2.35%. China Shanghai SSE fell -0.00%. Singapore Strait Times rose 0.46%. Japan 10-year JGB yield rose 0.028 to 1.573.

Fed's Kugler: Reaccelerating goods inflation unhelpful

Fed Governor Adriana Kugler expressed growing concern over the recent behavior of inflation. Speaking today, she highlighted that some inflation subcategories "reaccelerated in recent months." In particular, goods inflation, which had been negative in 2024 but has recently turned positive.

She warned that this shift is “unhelpful” as goods inflation "has often kept a lid on total inflation and also affects inflation expectations".

Kugler added that surveys are now pointing to rising inflation expectations among consumers too, with much of the uncertainty tied to ongoing trade policy developments.

Despite these concerns, Kugler reaffirmed confidence in the current policy stance, describing it as restrictive while Fed is "well positioned.

Germany’s Ifo rises to 86.7, hopes build for modest recovery

Germany’s Ifo Business Climate index edged higher from 85.3 to 86.7 in March, While the rise was slightly below market expectations of 87.0, the improvement was broad-based across sectors. Current Assessment Index ticked up from 85.0 to 85.7, above expectations of 85.5. Expectations Index rose from 85.6 to 87.7, though still shy of the 87.9 forecast.

Across sectors, sentiment improved uniformly. The manufacturing index rose notably from -21.9 to -16.6. Services (up from -4.3 to -1.1), trade (up from -26.3 to -23.7), and construction (up from -27.4 to -24.6) all saw smaller improvements, indicating a broad but tentative shift in mood.

Ifo President Clemens Fuest commented that “German businesses are hoping for a recovery,” a sentiment echoed by survey head Klaus Wohlrabe, who projected 0.2% growth in GDP for Q1, after -0.2% contraction in Q4.

BoJ minutes signal readiness to tighten further if outlook holds

Minutes from BoJ’s January 23–24 meeting revealed a growing consensus among policymakers that further tightening would be appropriate, provided the current economic and price outlooks hold.

While the central bank raised policy rate to 0.5%, members acknowledged that real interest rates remained "significantly negative", ensuring "accommodative financial conditions would be maintained."

However, the path ahead is clouded by global uncertainty. While BoJ held rates steady at its latest meeting last week, it flagged increasing risks from escalating US tariffs.

Nevertheless, Governor Kazuo Ueda emphasized that stronger-than-expected wage growth and persistent food price inflation could keep upward pressure on underlying prices, indicating that the case for another rate hike remains very much alive.

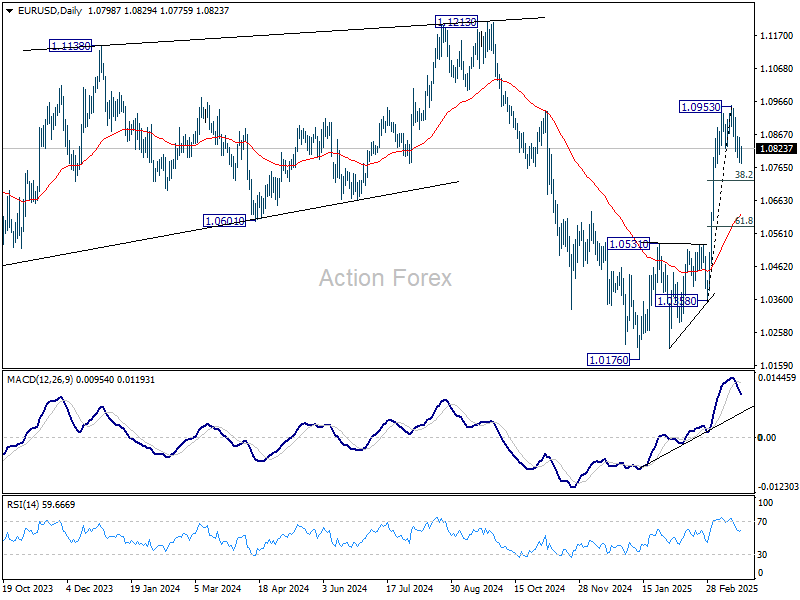

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0769; (P) 1.0814; (R1) 1.0845; More...

Intraday bias in EUR/USD is turned neutral with current recovery. Corrective pattern from 1.0953 could extend with another fall. But downside should be contained by 38.2% retracement of 1.0358 to 1.0953 at 1.0726 to bring rebound. On the upside, break of 1.0953 will resume the rally from 1.0176 towards 1.1274 key resistance.

In the bigger picture, prior strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

Fed’s Kugler: Reaccelerating goods inflation unhelpful

Fed Governor Adriana Kugler expressed growing concern over the recent behavior of inflation. Speaking today, she highlighted that some inflation subcategories "reaccelerated in recent months." In particular, goods inflation, which had been negative in 2024 but has recently turned positive.

She warned that this shift is “unhelpful” as goods inflation "has often kept a lid on total inflation and also affects inflation expectations".

Kugler added that surveys are now pointing to rising inflation expectations among consumers too, with much of the uncertainty tied to ongoing trade policy developments.

Despite these concerns, Kugler reaffirmed confidence in the current policy stance, describing it as restrictive while Fed is "well positioned.

EUR/USD Outlook: Recovery Attempts Above Fibo Support/20DMA

EURUSD ticked higher on Tuesday after four-day pullback from new multi-month high at 1.0954 (larger rally stalled just under Fibo resistance at 1.0969) found temporary footstep at 1.0771 (Fibo 23.6% of 1.0177/1.0954 rally).

Partial profit taking lifts the price, although bounce was not significant so far as the action remains negatively impacted by recent strong loss of positive momentum.

South-heading 14-d momentum indicator is in step descend and approaching the centreline but partially offset by the latest 20/200DMA golden cross formation (1.0727).

Recovery needs to clear 1.0860 zone (Monday’s high / 10DMA) to signal reversal and a higher low.

Fibo level at 1.0771, reinforced by rising 20DMA and nearby 200DMA (1.0729 mark solid supports, with near-term bias to remain with bulls while the price stays above these levels.

Conversely, firm break lower would open way for deeper correction.

Tariff talks remain one of key fundamental points, with today’s release of US Consumer Confidence to also contribute, as markets await release of US PCE data on Friday, Fed’s preferred inflation gauge, which will provide more details about the central bank’s near future steps on monetary policy.

Res: 1.0860; 1.0888; 1.0954; 1.0969.

Sup: 1.0771; 1.0760; 1.0729; 1.0700.

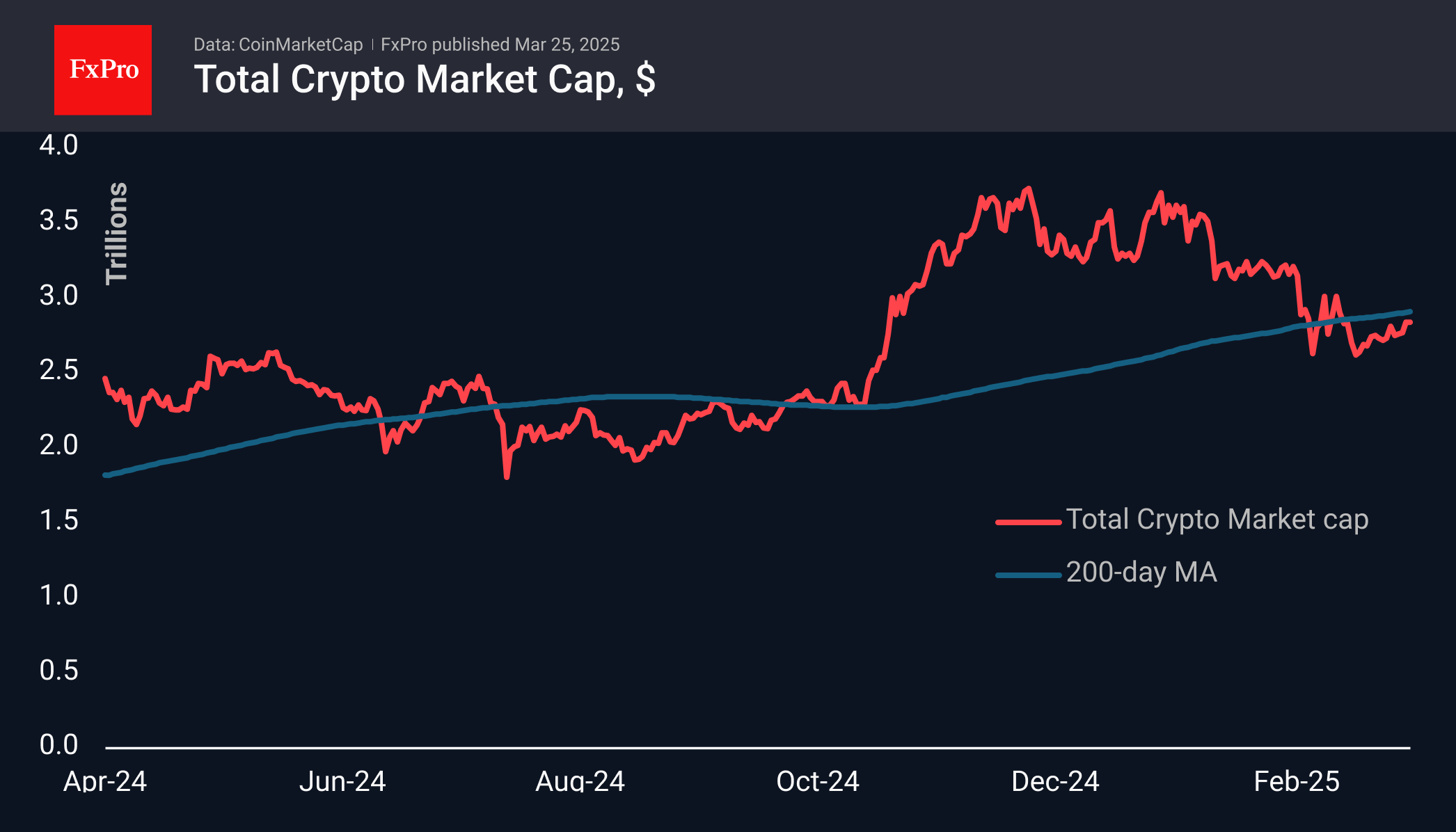

Crypto Market Prepares to Storm the Trend Line

Market Picture

The crypto market is losing slightly early Tuesday afternoon, cutting the gains of the past seven days to 4.4%. Acting on classic market trends, selling pressure intensified on the approach to the 200-day moving average near $2.90 trillion. A dip under that curve intensified selling in early March, but the market has generally held near that line and is now storming it.

Success could whet the appetite of doubters, validating the continuation of the cryptocurrency bull market.

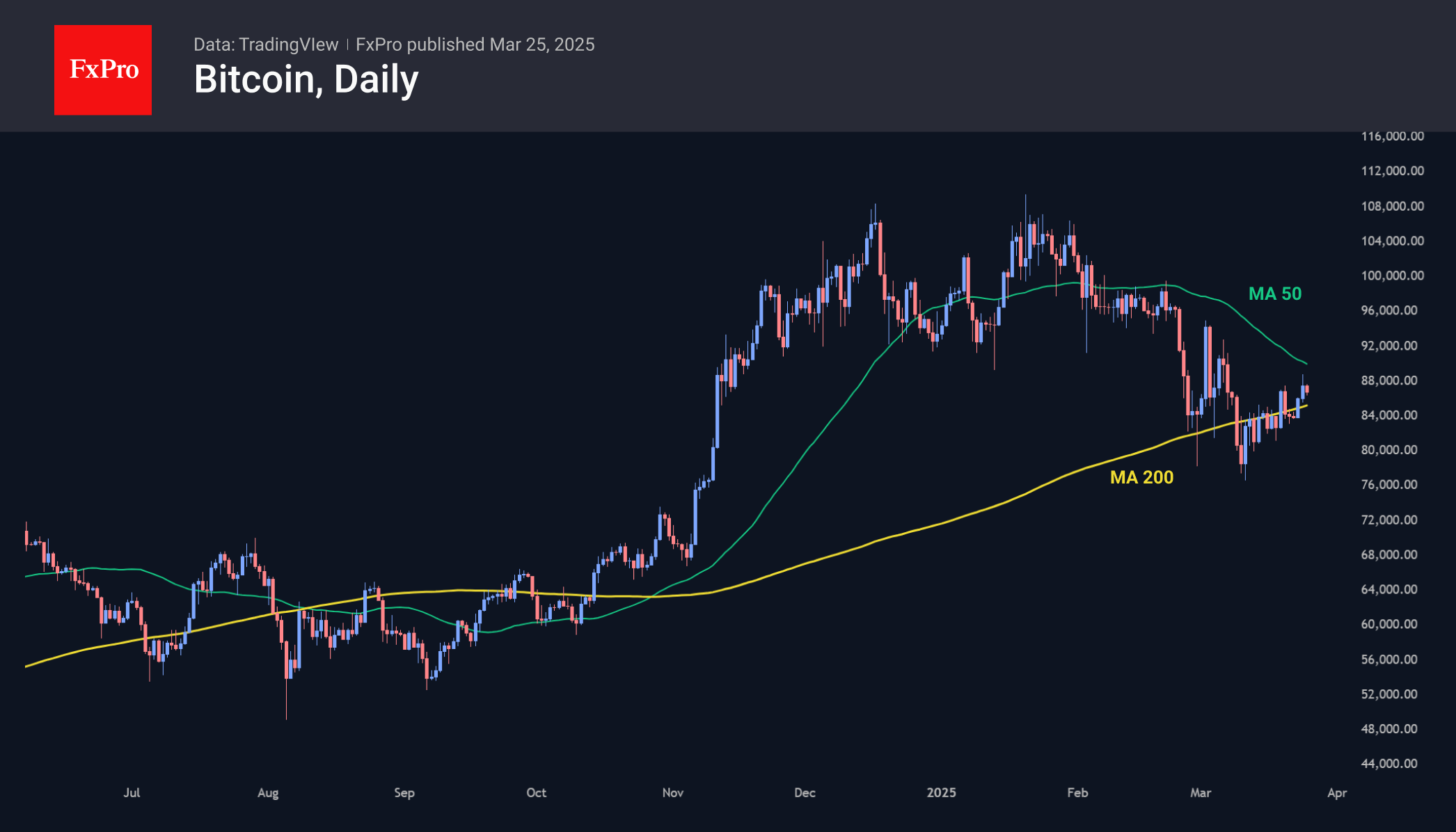

Bitcoin started the week with a solid move above its 200-day average, peaking just below 89K on Monday. However, it failed to overcome the next milestone—the 50-day average.

Bitcoin started the week with a solid move above its 200-day average, peaking just below 89K

At this stage, the recovery may be helped by the positive dynamics of the stock market, shifting the balance in favour of buyers. Successfully overcoming the $90K level will open a fast track to $97K, where there was a previous long consolidation. If FOMO joins this uptrend, we could see a move to all-time highs before the summer even begins.

Germany’s Ifo rises to 86.7, hopes build for modest recovery

Germany’s Ifo Business Climate index edged higher from 85.3 to 86.7 in March, While the rise was slightly below market expectations of 87.0, the improvement was broad-based across sectors. Current Assessment Index ticked up from 85.0 to 85.7, above expectations of 85.5. Expectations Index rose from 85.6 to 87.7, though still shy of the 87.9 forecast.

Across sectors, sentiment improved uniformly. The manufacturing index rose notably from -21.9 to -16.6. Services (up from -4.3 to -1.1), trade (up from -26.3 to -23.7), and construction (up from -27.4 to -24.6) all saw smaller improvements, indicating a broad but tentative shift in mood.

Ifo President Clemens Fuest commented that “German businesses are hoping for a recovery,” a sentiment echoed by survey head Klaus Wohlrabe, who projected 0.2% growth in GDP for Q1, after -0.2% contraction in Q4.

Forex Traders Focus on Trump’s Tariff News

As April 2 approaches—the date when Trump's international trade tariffs are set to take effect—traders are increasingly concentrating on this highly uncertain issue.

Yesterday, the U.S. president stated that:

→ Tariffs on cars would be introduced "soon" (but not all possible tariffs would be imposed);

→ Some countries might receive exemptions;

→ Nations purchasing oil from Venezuela could face 25% tariffs.

Following these remarks:

→ Oil prices rose;

→ U.S. stocks gained as Wall Street (according to Reuters) interpreted the comments as a sign of flexibility in trade negotiations.

Given this backdrop, the EUR/CAD chart is particularly interesting, as both Europe and Canada frequently feature in news related to the White House's trade policies.

EUR/CAD Exchange Rate Today

As seen on the EUR/CAD chart, the pair has slightly declined at the start of the week, dipping towards 1.54450. However, market volatility remains high:

→ The pair has gained approximately 2.85% since early March;

→ The decline from March’s peak is around 2.6%.

Technical Analysis of EUR/CAD

The pair’s volatile price swings have formed a trend channel (marked in blue).

Notably, the 1.57750 level has shifted from support to resistance, signalling bearish dominance. This is further reflected in the price movement within the red channel. If bears maintain control, EUR/CAD may drop towards a support zone, which includes:

→ The median of the blue channel;

→ The 1.54000 support level, drawn from early March’s local low.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.