Sample Category Title

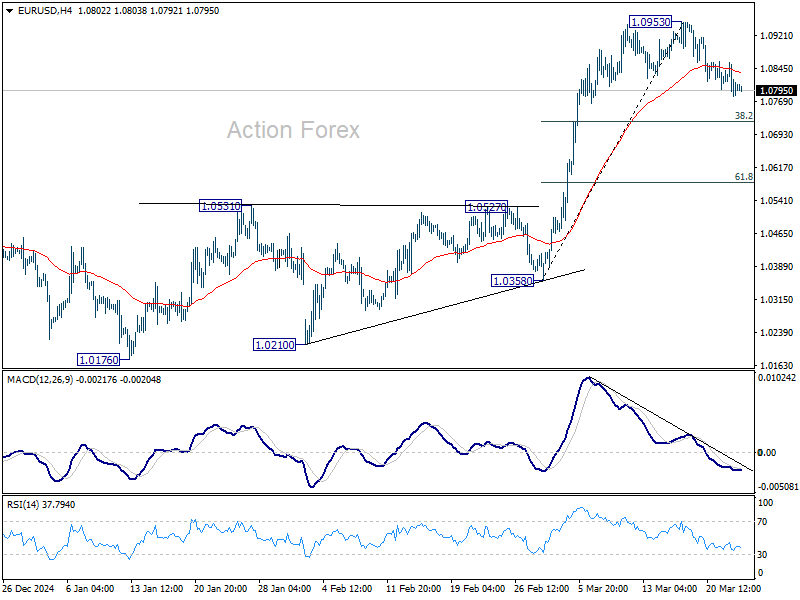

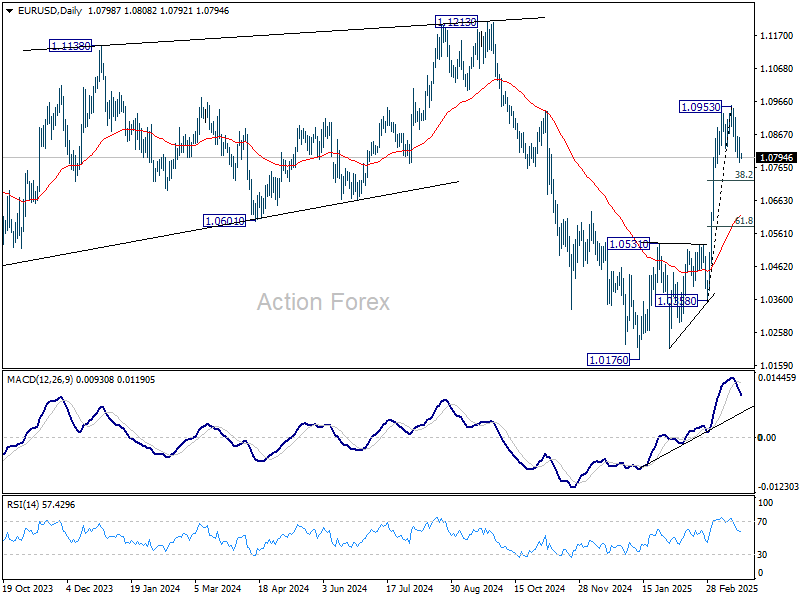

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0769; (P) 1.0814; (R1) 1.0845; More...

Intraday bias in EUR/USD remains mildly on the downside, as correction from 1.0953 short term top would extend to 38.2% retracement of 1.0358 to 1.0953 at 1.0726. Strong support should be seen there to bring rebound. On the upside, break of 1.0953 will resume the rally from 1.0176 towards 1.1274 key resistance.

In the bigger picture, prior strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

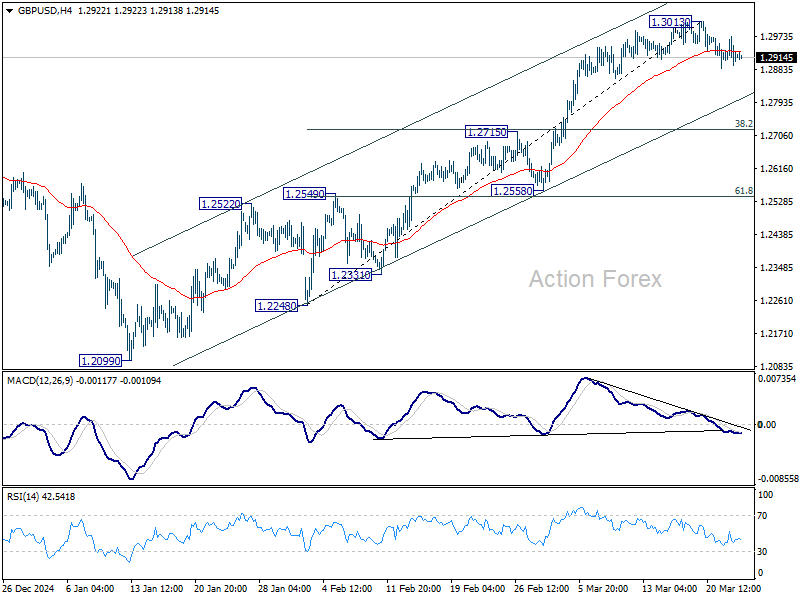

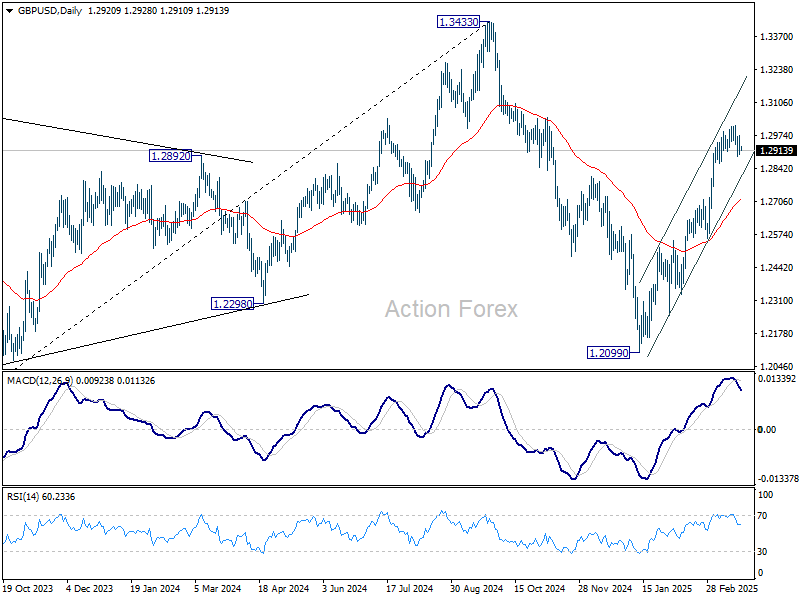

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2881; (P) 1.2927; (R1) 1.2970; More...

Intraday bias in GBP/USD stays mildly on the downside as correction from 1.3013 short term top would extend to 38.2% retracement of 1.2248 to 1.3013 at 1.2721. Strong support should be seen there to bring rebound. On the upside, break of 1.3013 will resume the rally from 1.2099.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance. This will now remain the favored case as long as 1.2099 support holds.

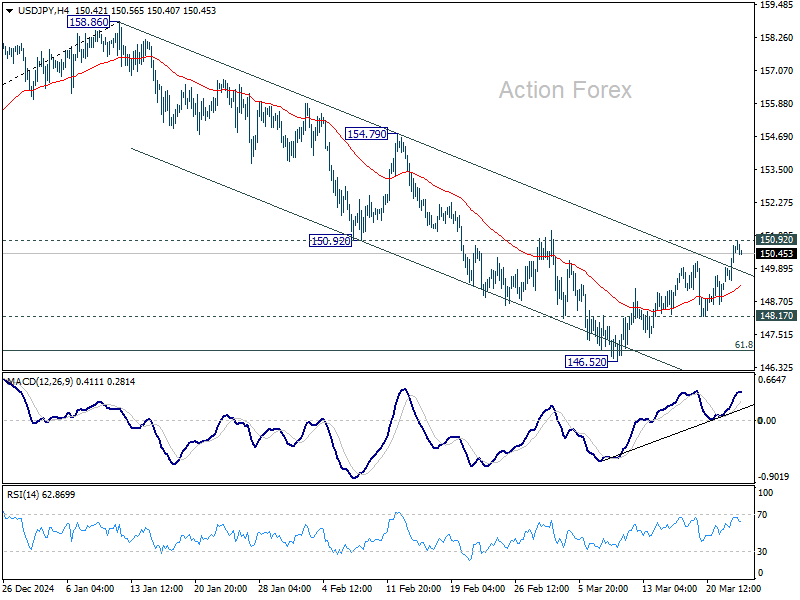

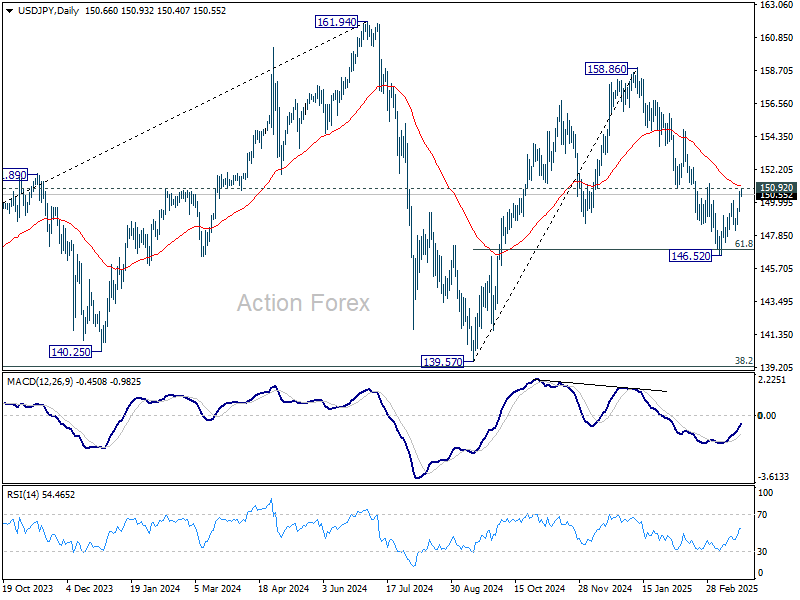

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.78; (P) 150.27; (R1) 151.19; More...

Outlook is USD/JPY is unchanged. Recovery from 146.52 is seen as a corrective move. Upside should be limited by 150.92 support turned resistance. On the downside, break of 148.17 support will bring retest of 146.52 first. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will resume the fall from 158.86 to 139.57 support. However, firm break of 150.92 will argue that fall from 158.86 has completed and turn bias back to the upside for 154.79 resistance next.

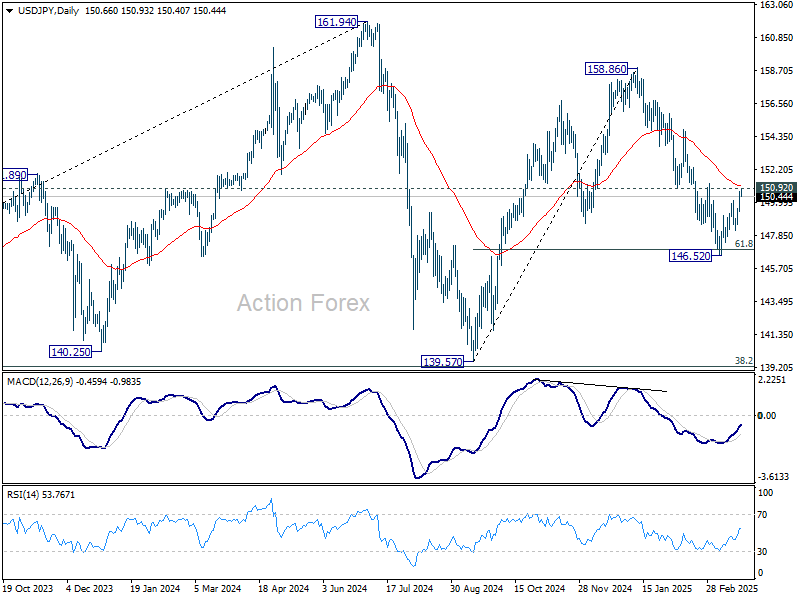

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

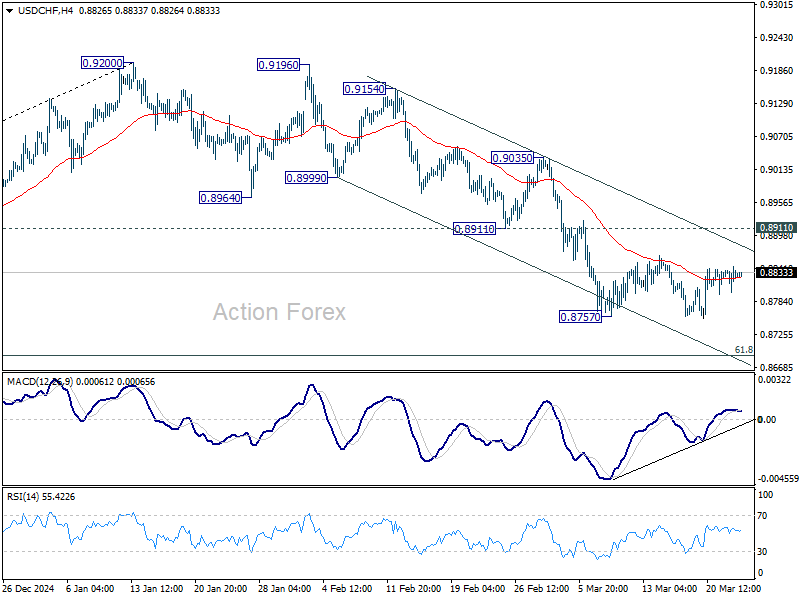

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8804; (P) 0.8825; (R1) 0.8850; More…

USD/CHF is staying in consolidation from 0.8757 and intraday bias remains neutral. In case of stronger recovery, upside should be limited by 0.8911 support turned resistance. On the downside, break of 0.8757 will resume the fall from 0.9200 to 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

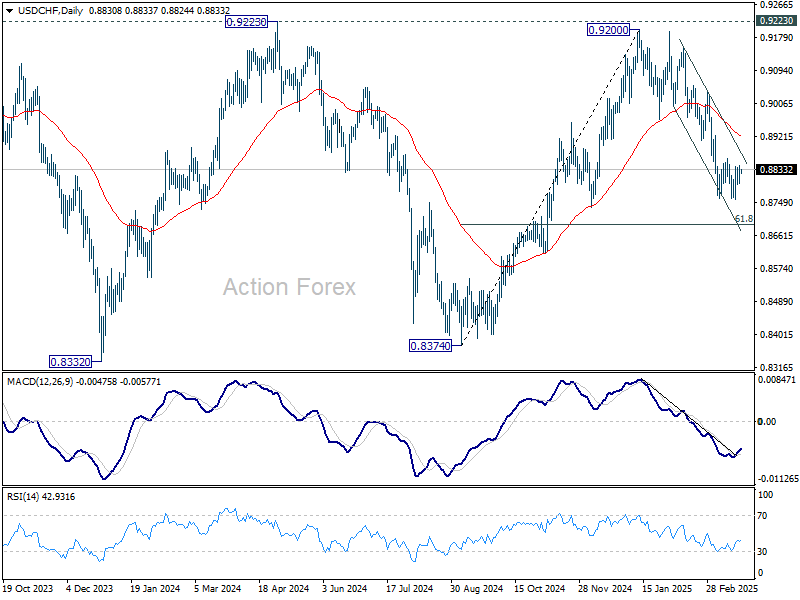

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

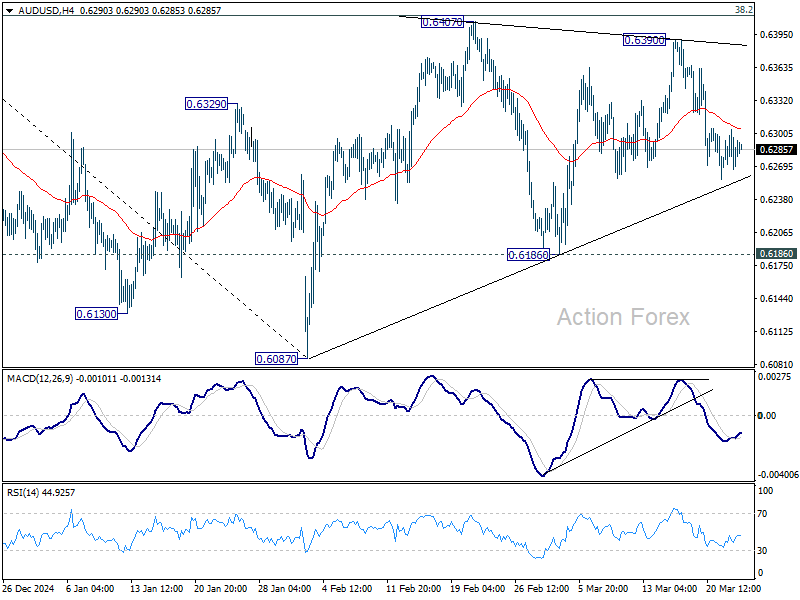

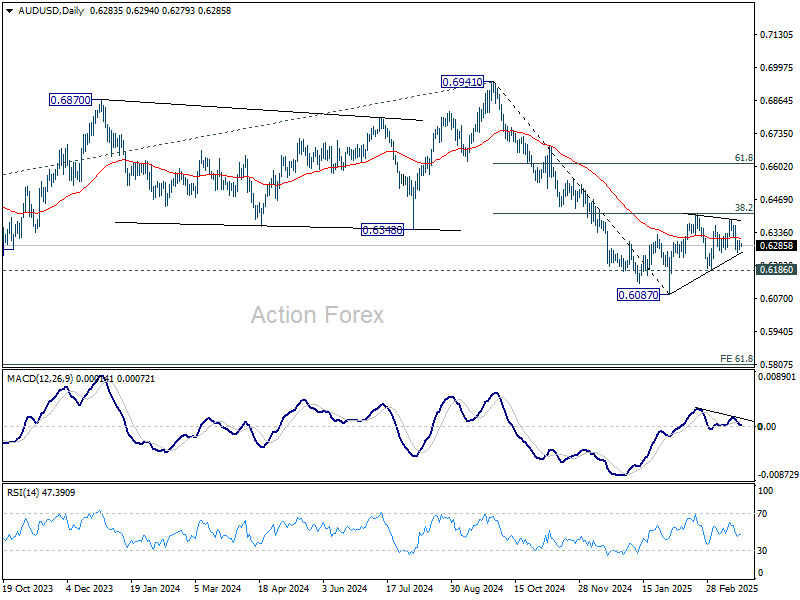

AUD/USD Daily Report

Daily Pivots: (S1) 0.6268; (P) 0.6286; (R1) 0.6305; More...

No change in AUD/USD's outlook and intraday bias stays neutral at this point. On the downside, firm break of near term trend line support (now at 0.6255) will argue that corrective pattern from 0.6087 has already completed. Intraday bias will be back on the downside for 0.6186 support. Further break there will solidify this bearish case and target 0.6087 low. For now, in case of another rise, upside should be limited by 38.2% retracement of 0.6941 to 0.6087 at 0.6413.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6467) holds.

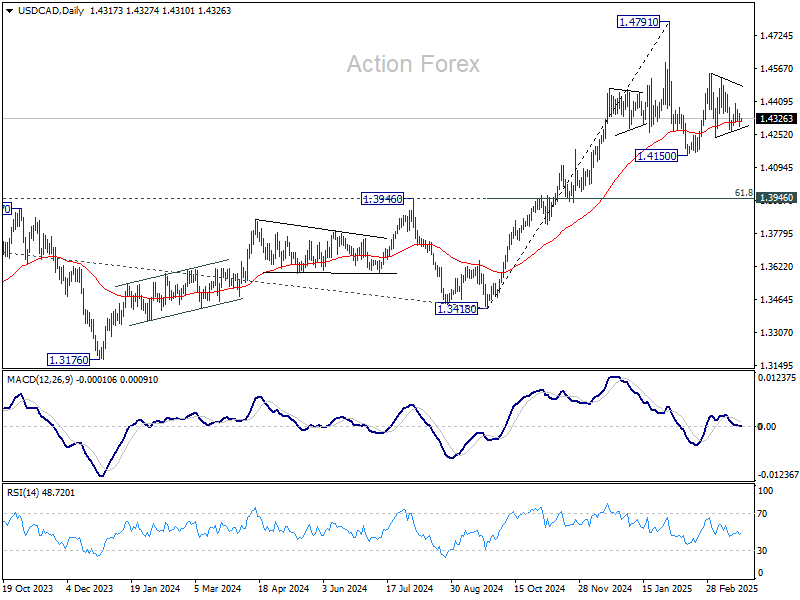

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4287; (P) 1.4322; (R1) 1.4354; More...

Range trading continues in USD/CAD and intraday bias remains neutral for now. Overall, price actions from 1.4791 are seen as a corrective pattern. On the upside, break of 1.4541 will extend the second leg from 1.4150 to retest 1.4791 high. On the downside, break of 1.4238 will argue that the third leg has already started through 1.4150 support.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

Yen Steadies on Hawkish BoJ Tone, USD/JPY Rally Pauses at Key 150 Level

Financial markets entered Tuesday on a subdued note, with the Asian session notably quiet. While US stocks managed a rebound overnight on speculation that the April 2 “Liberation Day” tariff rollout might be narrower in scope than initially feared, sentiment failed to fully carry into Asia. Equity indices across the region were mixed, reflecting ongoing investor caution. In the currency markets, major pairs remained trapped within yesterday’s ranges, signaling a broader wait-and-see mode among traders.

Yen is seeing some mild recovery after Monday’s selloff, partially supported by signals from BoJ’s latest January meeting minutes. The central bank reaffirmed its readiness to tighten policy further. Still, external developments—particularly the uncertainty over global trade and US tariffs—are making the policy path less clear, forcing BoJ to move with greater caution in coming months.

Looking ahead to the European session, Germany’s Ifo Business Climate data will be watched. Still, most of the optimism linked to Germany’s fiscal expansion appears to be already priced in. Unless there's a sharp upside surprise, the report may not trigger much market movement.

Later in the day, US Consumer Confidence figures are in focus. Expectations are for a continued decline, reflecting growing concerns over the economic fallout from reciprocal tariffs. Yet, this deterioration in sentiment has become a familiar theme, and its market impact may also be muted unless the drop is significantly worse than expected.

What investors truly crave are concrete details surrounding Trump’s tariff due next week. Until then, markets are likely to remain rangebound and headline-driven. With such a pivotal policy move on the horizon, traders are understandably reluctant to take strong directional bets. That has kept volatility suppressed for now, even as the risk environment remains fragile underneath the surface.

Technically, a major focus now is USD/JPY, which has extended the rebound from 146.52 short term bottom this week. Strong resistance is expected from 150.92 support turned resistance, and 55 D EMA (now at 151.08) to limit upside. However, firm break of this zone will argue the fall from 158.86 has completed, and turn near term outlook bullish for stronger rebound. The next move in USD/JPY would determine the overall tone of Yen in the markets.

In Asia, at the time of writing, Nikkei is up 0.56%. Hong Kong HSI is down -1.99%. China Shanghai SSE is down -0.05%. Singapore Strait Times is up 1.11%. Japan 10-year JGB yield is up 0.028 at 1.574. Overnight, DOW rose 1.42%. S&P 500 rose 1.76%. NASDAQ rose 2.27%. 10-year yield rose 0.079 to 4.331.

BoJ minutes signal readiness to tighten further if outlook holds

Minutes from BoJ’s January 23–24 meeting revealed a growing consensus among policymakers that further tightening would be appropriate, provided the current economic and price outlooks hold.

While the central bank raised policy rate to 0.5%, members acknowledged that real interest rates remained "significantly negative", ensuring "accommodative financial conditions would be maintained."

However, the path ahead is clouded by global uncertainty. While BoJ held rates steady at its latest meeting last week, it flagged increasing risks from escalating US tariffs.

Nevertheless, Governor Kazuo Ueda emphasized that stronger-than-expected wage growth and persistent food price inflation could keep upward pressure on underlying prices, indicating that the case for another rate hike remains very much alive.

Fed’s Bostic sees just one rate cut in 2025, warns tariffs may reinforce inflation

Atlanta Fed President Raphael Bostic said in a Bloomberg interview that he's now projecting just one cut by year-end, down from his earlier expectation of two.

Bostic explained the shift was due to his view that inflation will be "very bumpy and not move dramatically and in a clear way to the 2% target”. With inflation unlikely to return to target until 2027, he believes the path to neutral must also be delayed.

Bostic also expressed concern about the inflationary impact of rising tariffs. While such measures are often assumed to cause a one-off increase in prices, Bostic suggested the current environment could be different.

In his view, businesses and consumers may have grown more tolerant of elevated inflation following the pandemic, making price hikes more likely to stick. He noted that many business leaders now feel confident about "a complete pass-through" of higher costs on to customers without fear of losing market share.

BoE’s Bailey calls for trade cooperation and embraces AI as growth catalyst

BoE Governor Andrew Bailey urged greater international cooperation to resolve growing strains in the global trading system. In a speech overnight, he pointed to the disruptions caused by US President Donald Trump’s trade policies, emphasizing that resolving these challenges requires "multilateral setting rather than set tariffs bilaterally".

In a more optimistic tone, Bailey also pointed to artificial intelligence as a transformative force for the UK and global economy. Comparing AI to electricity in the early 20th century, he said the technology could meaningfully raise growth and per capita income over time. He called for policy support to facilitate AI’s development as the "most likely general purpose technology,” capable of driving broad-based economic gains in the years ahead.

ECB’s Escriva warns of extreme uncertainty and skewed growth risks

In remarks delivered overnight, Spanish ECB Governing Council member Jose Luis Escriva highlighted that “growth risks are more downside than upside.” While he acknowledged that supportive fiscal policy could offer some near-term uplift, he stressed that the broader risks — particularly to the downside — are dominating the economic outlook.

Escriva painted a grim picture of the current global backdrop, describing it as “extremely uncertain.” He noted that today’s uncertainty global index levels are at their highest since records began — exceeding those during the Covid-19 pandemic, the war in Ukraine, the 9/11 attacks, and even the peak of the Great Financial Crisis.

Despite the fact that worst-case, disruptive scenarios have yet to materialize, Escriva emphasized that ECB must be “readier than ever” to revise its forecasts and relevant action should conditions change".

Looking ahead

German Ifo business climate ins the main focus in European session. Later in the day, US will release consumer confidence, house prices and new home sales.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4287; (P) 1.4322; (R1) 1.4354; More...

Range trading continues in USD/CAD and intraday bias remains neutral for now. Overall, price actions from 1.4791 are seen as a corrective pattern. On the upside, break of 1.4541 will extend the second leg from 1.4150 to retest 1.4791 high. On the downside, break of 1.4238 will argue that the third leg has already started through 1.4150 support.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

Elliott Wave View: USDJPY Rallying in Double Zigzag

Short Term Elliott Wave view in USDJPY suggests that rally from 3.11.2025 low is in progress as a double zigzag structure. A double zigzag structure is a 7 swing double three Elliott Wave structure. There are 2 sets of ABC zigzag structure connected together, thus why the name is double zigzag. Up from 3.11.2025 low, wave A ended at 149.2 and wave B ended at 147.4. Wave C higher ended at 150.1 and this completed the first zigzag structure and end wave (W) in higher degree as the 45 minutes chart below illustrates. Pullback in wave (X) ended at 148.1 and pair has resumed higher in wave (Y).

Internal subdivision of wave (Y) is unfolding as another zigzag structure. Up from wave (X), wave ((i)) ended at 149.66 and wave ((ii)) pullback ended at 148.6. Up from there, pair is nesting higher in wave ((iii)). Wave (i) ended at 149.95 and wave (ii) pullback ended at 149.48. Wave (iii) higher ended at 150.94. Expect pullback in wave (iv) to find support for more upside. Near term, as far as pivot at 148.16 low stays intact, expect dips to find buyers in 3, 7, or 11 swing for further upside.

USDJPY 45 Minutes Elliott Wave Chart

USDJPY Video

https://www.youtube.com/watch?v=7-b4izTOKPk

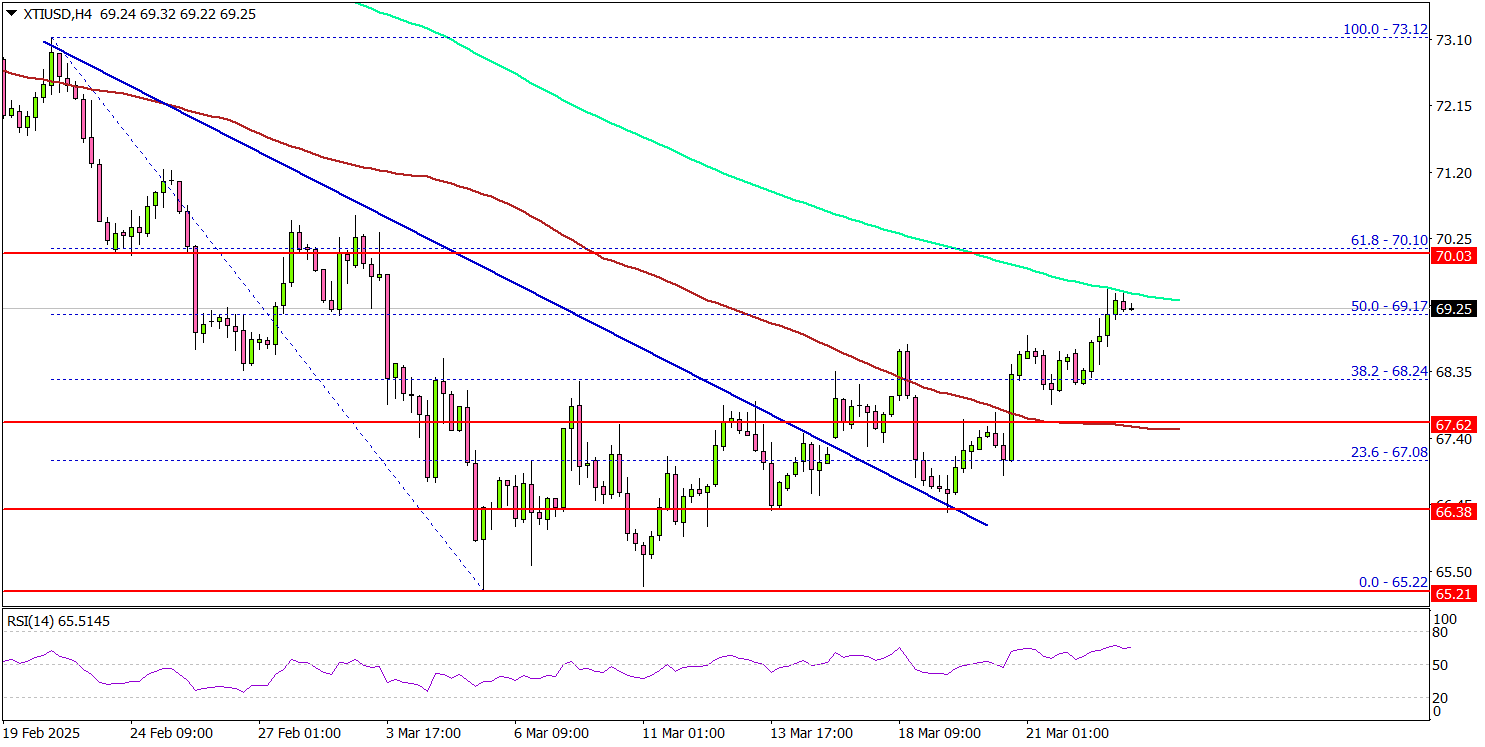

WTI Crude Oil Price Begins Rebound—Can Bulls Sustain the Momentum?

Key Highlights

- WTI Crude Oil prices started a recovery wave from the $65.20 zone.

- It traded above a connecting bearish trend line with resistance at $67.40 on the 4-hour chart.

- Gold prices corrected some gains from the $3,050 resistance.

- Bitcoin recovered ground and cleared the $86,500 resistance.

WTI Crude Oil Price Technical Analysis

WTI Crude Oil price extended losses below $70.00. The price tested the $65.20 zone and recently started a recovery wave.

Looking at the 4-hour chart of XTI/USD, the price was able to clear the $66.50 and $67.00 resistance levels. It cleared the 38.2% Fib retracement level of the downward move from the $73.12 swing high to the $65.22 low.

The price traded above a connecting bearish trend line with resistance at $67.40 on the same chart. There was a move above the 100 simple moving average (red, 4-hour) and a spike above the 50% Fib retracement level of the downward move from the $73.12 swing high to the $65.22 low.

On the upside, the price is facing hurdles near the $69.80 level and the 200 simple moving average (green, 4-hour). The main hurdle is now near the $70.10 zone, above which the price may perhaps accelerate higher.

In the stated case, it could even visit the $71.50 resistance. Any more gains might call for a test of the $72.00 resistance zone in the near term.

On the downside, the first major support sits near the $67.60 zone. A daily close below $67.60 could open the doors for a larger decline. The next major support is $66.40. Any more losses might send oil prices toward $65.00 in the coming days.

Looking at Gold, there was a strong increase above the $3,020 level and the price is now correcting some gains.

Economic Releases to Watch Today

- US Housing Price Index for Jan 2025 (MoM) - Forecast +0.2%, versus +0.4% previous.

- US New Home Sales for Feb 2025 (MoM) – Forecast -0.8% versus -10.5% previous.

BoJ minutes signal readiness to tighten further if outlook holds

Minutes from BoJ’s January 23–24 meeting revealed a growing consensus among policymakers that further tightening would be appropriate, provided the current economic and price outlooks hold.

While the central bank raised policy rate to 0.5%, members acknowledged that real interest rates remained "significantly negative", ensuring "accommodative financial conditions would be maintained."

However, the path ahead is clouded by global uncertainty. While BoJ held rates steady at its latest meeting last week, it flagged increasing risks from escalating US tariffs.

Nevertheless, Governor Kazuo Ueda emphasized that stronger-than-expected wage growth and persistent food price inflation could keep upward pressure on underlying prices, indicating that the case for another rate hike remains very much alive.